Still No Sign of the Big Bad Wolf

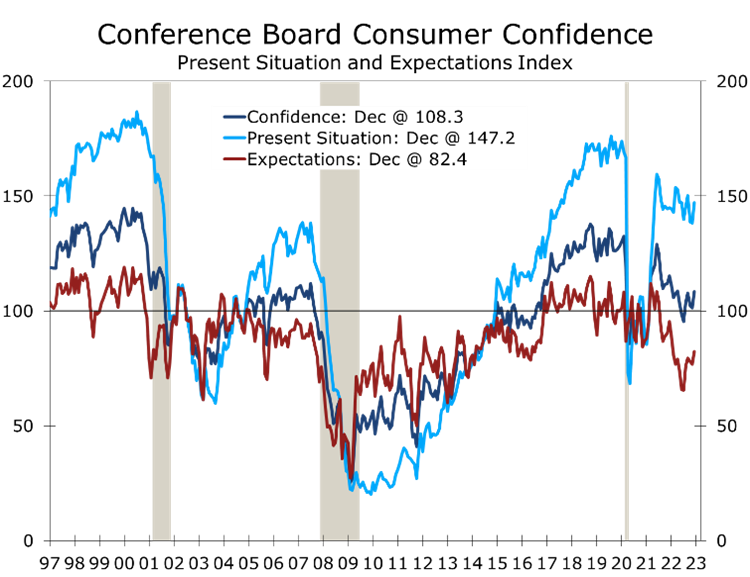

- Consumer Confidence rebounded 6.9 points in December to 108.3, pushing back on any notion the economy is on the precipice of recession, at least at the end of 2022.

- Consumers’ assessment of current economic conditions rose 8.9 points in December to 147.2, likely benefitting from falling gasoline prices.

- Expectations for business conditions 6 months from now rose 5.7 points to 82.4, a level historically consistent with a mild recession but still well above prior lows.

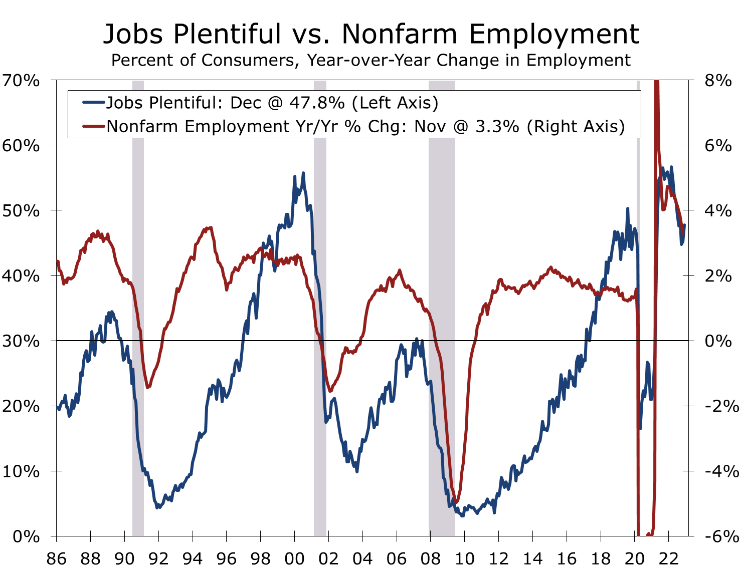

- The share of consumers stating jobs were plentiful in December rose 2.6 points to 47.8, while the share that felt jobs were hard to get fell 1.7 points to 12.

- Inflation expectations for the coming year also declined but remain historically high at 6.7%. Inflation expectations had been around 4.5% prior to the pandemic.

The Consumer Confidence Index rebounded 6.9 points to 108.3 in December, as falling gasoline prices and the continuing abundance of job openings offset concerns about rising interest rates and a wobbly stock market. Consumers assessment of the present economic situation rose 8.9 points to a lofty 147.2, while expectations for future economic conditions rose 5.7 points to a less ominous 82.4 in December.

The stronger consumer confidence numbers downplay the risk a recession is now imminent. While most economists, business leaders and policymakers still see a recession as more likely than not, many forecasters are pushing out the timing of when a downturn would begin or diminishing the odds that one will occur at all. We put the odds of recession in 2023 at around 60%. That is far from a slam dunk but far from more cautious than usual. The next most likely outcome would be a series of rolling recessions in the tech sector, housing, and commercial real estate, which would combine to keep real GDP growing at 1% pace or less. This scenario would be a on the soft side of soft landings.

The split between consumers’ assessment of present economic conditions and expectations for future conditions is not unusual in the latter part of the business cycle. The present situation is being supported by the red-hot job market. With help-wanted signs visible nearly everywhere, the share of consumers reporting jobs were plentiful rose 2.6 points to 47.8%, while just 12% of consumers felt jobs were hard to get, down 1.7 points from November.

The share of consumers rating current business conditions as ‘good’ rose by a more modest 1.2 points to 19%, while the share of consumers rating current business conditions as bad fell 2.5 points to 20.1%. It is highly unusual to have a larger number of consumers rate current business conditions as ‘bad’ than ‘good’ and still rate jobs as extremely plentiful.

The net share of consumers reporting jobs are plentiful remains consistent with strong overall job growth and is another piece of data hinting that job growth remained strong in December. The mix of jobs is likely not as strong as the overall number being added, however, with a large share of current job growth coming from restaurants and lower paying occupations in health care, education, and other services.

The split between consumers’ positive attitudes about the availability of jobs and their less sanguine view on expectations for the overall economy likely reflects concerns about lack of availability of higher paying jobs. The overall expectations series rose 5.7 points in December, with the share of consumers expecting business conditions to improve rising 0.6 points to 20.4% and narrowly edged out the share expecting business conditions to worsen (20.3%).

Expectations for job growth remain positive. The share of consumers expecting more jobs to be created over the next 6 months rose 1 point to 19.5%, while the share expecting fewer jobs to be created fell 1.9 points to 18.3%. While that is positive, it is far less upbeat than consumers’ assessment of current employment conditions. Expectations for job growth have likely been scaled back by the growing list of marquee employers announcing cutbacks in the tech sector and elsewhere. Those layoffs have not yet shown up in the weekly unemployment claims or monthly employment data.

Expectations for income growth were mixed, with the share expecting their incomes to rise falling 0.4 percentage points to 16.7%, and the share expecting their income to fall sliding 2.5 points to 13.3%. The mixed response likely reflects the challenges facing some higher paying sectors (tech, housing, and commercial real estate) amidst the continued rebound in lower-paying sectors hit hardest by the lockdowns at the start of the pandemic (restaurants, physician’s offices, nursing homes and day care).

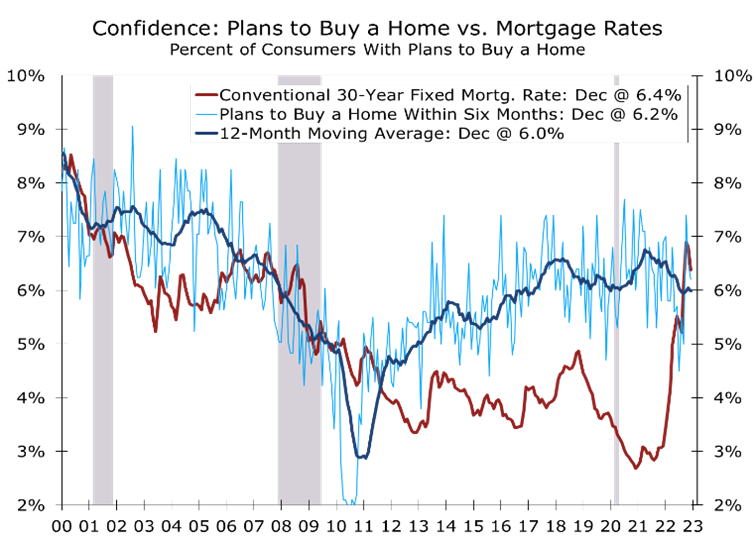

Buying plans were also mixed. Plans to take vacations increased but plans to purchase automobiles, major appliances and homes fell. The Conference Board’s measure of plans to buy a home has held up much better than alternative measures from the University of Michigan and Fannie Mae and has been above its 12-month moving average the past two months. The modest rebound may signal some let up in this past year’s slide in new and existing home sales.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.