A Mixed Bag Ahead of the Holidays

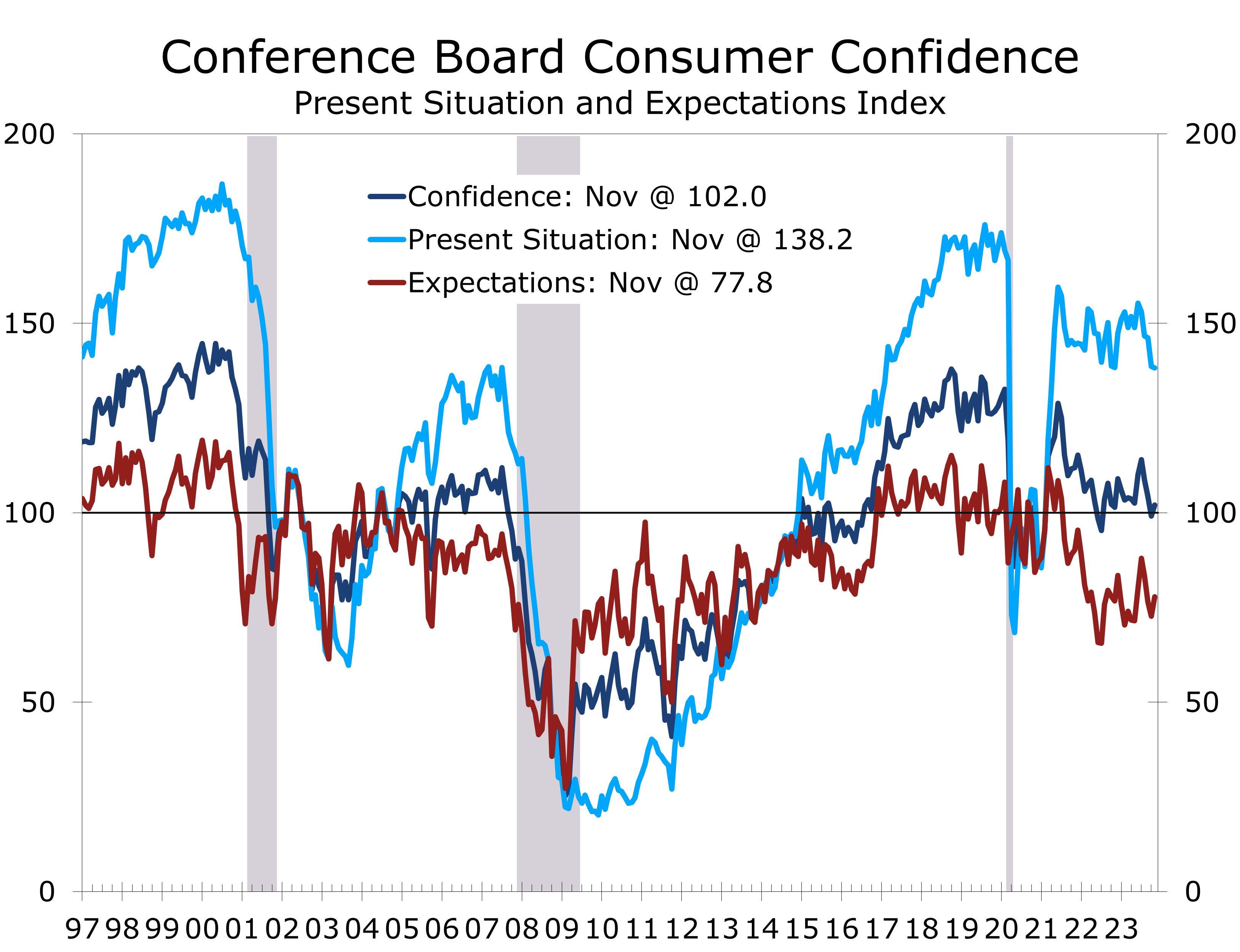

- Consumer Confidence rose a stronger-than-expected 2.9 points to 102.0 in November, following three consecutive declines.

- The expectations component rose 5.1 points to 77.8, accounting for all of November’s increase. By contrast, current conditions slipped 0.4 points to 138.2.

- Consumers’ assessment of current labor conditions was mixed, with the share stating jobs are ‘plentiful’ (+1.4 pp to 39.3%) and the share stating that jobs were ‘hard to get’ (1.3 pp to 15.4%) both rising in November.

- Consumers are more optimistic about their income prospects, however, with 17.2% expecting their incomes to increase over the next six months (+1.6 pp), and just 12.1% expecting their incomes to decline (-1.3 pp).

- Consumers remain generally upbeat about employment and income prospects, which is a bit of good news ahead of the holiday season. We still look for holiday retail sales to rise at the lower end of the National Retail Federation’s 3% to 4% forecast.

November’s 2.9-percentage point increase in the Consumer Confidence Index exaggerates the extent of the improvement seen this past month. While Consumer Confidence posted its first increase since July, the gain was only possible because of a 3.5 percentage point downward revision to the prior month’s data, from 102.6 to 99.1. In other words, Consumer Confidence is actually lower today it was initially reported to be a month ago and currently sits at the second lowest level for this year.

All of November’s increase in Consumer Confidence came from an improvement in the expectations series, which rose 5.1 points to 77.8. That still leaves expectations at a fairly low level, however. Any reading below 80 is generally consistent with a recession.

Expectations for business conditions over the next six months remain guarded at best, with 17.3% of consumers expecting conditions to improve over the next six months (+1.8 pp) against 19.5% expecting conditions to worsen (- 1.4 pp). Consumers are also looking for continued moderation in employment conditions, with 19.6% expecting fewer jobs to be created (-0.1 pp) and just 16.1% expecting more jobs to be created (+0.8 pp).

Consumers are slightly more optimistic about the outlook for their personal finances.

Consumers remain more upbeat about their personal finances. The share expecting their income to increase rose 1.6 pp to 17.2% in November, while the share expecting their incomes to decline fell 1.3 pp to 12.1%.

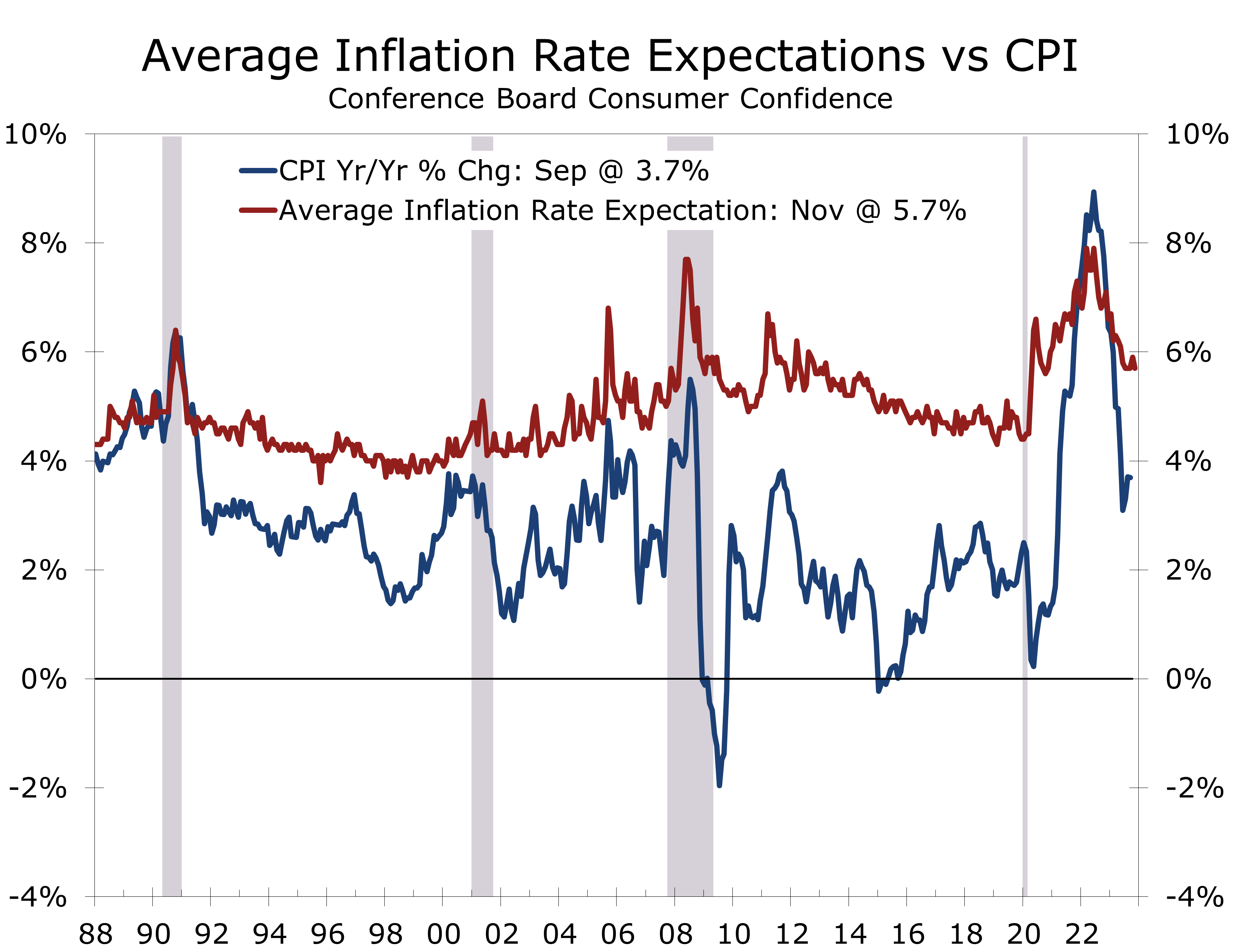

Consumer expectations are generally a better predictor of consumer behavior than either current conditions or consumer confidence. Despite the low level, the improvement is a positive for the holiday season and aligns with our forecast of a 3.2% rise in holiday retail sales. Several other measures of consumer expectations also improved, including the share expecting interest rates to drop over the next year as well as year-ahead inflation expectations, which fell from 5.9% to 5.7%.

Consumers’ outlook for stock prices continued to weaken, despite the early start to the Santa Claus rally that began following October’s better than expected CPI report. That improvement came only a couple days before the preliminary November Consumer Confidence Survey concluded on November 15.

Consumers are looking for a continued moderation in employment conditions.

Consumers’ assessment of current employment conditions remains unambiguously positive, yet hiring is clearly moderating and expected to continue to do so. The share of consumers perceiving jobs were plentiful in November rose 1.4 pp to 39.3%, while the share seeing jobs as hard to get rose 1.3 pp to 15.4%. Nonfarm employment growth has closely followed the jobs plentiful series and should continue to moderate.

The recent uptick in the jobs ‘hard to get’ series is consistent with the recent rise in the unemployment rate, from 3.4% in April to 3.9% currently. That said, consumer confidence remains more consistent with a soft landing rather than a recession, a point that is amplified by the 0.2 pp drop in year-ahead inflation expectations to 5.7%. The improvement comes at a time when gasoline prices have been sliding and prices for other goods and services have generally been rising less rapidly.

Consumer Confidence remains confounding, yet it aligns more with a soft landing than recession.

Consumers’ perceived likelihood of recession over the next 12 months, as tracked by the Conference Board, fell more than 3 pp in November to its lowest level this year. Hold the champagne, however, as even after this drop nearly two-third of consumers expect a downturn over the next 12 months. The Conference Board also noted November’s increase in consumer confidence was concentrated on householders aged 55 and up, while confidence among those aged 35 to 54 declined slightly. This split reinforces our cautious view on spending this holiday season.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.