Softening is Evident Beneath the Headlines

- Nonfarm employment once again topped consensus expectations, with employers adding a net 275,000 jobs in February.

- While hiring rose in most industries, gains were concentrated in health care, leisure and hospitality and government.

- Weather also boosted job growth, lifting construction payrolls, and also contributed to a big rebound in weekly hours.

- Job growth was revised lower by a combined 167,000 jobs for the prior two months.

- The unemployment rate also jumped 0.2 pp to 3.9%, as household employment fell by 184K and the labor force grew by 150K, lifting unemployment by 334K.

- Newly released data indicate third-quarter payrolls were also significantly overstated.

- The monthly employment data remain confounding, with initial reports continuing to come in well ahead of market expectations but downward revisions to prior data allaying fears of the economy overheating. We believe hiring is slowing more than the headlines suggest and look for payroll growth to meaningfully decelerate this spring.

Nonfarm employment blew past consensus expectations, with employers adding 275,000 jobs in February. Upside surprises to monthly payroll growth are becoming the norm. The markets appear to be discounting the strong headline gains; however, data have repeatedly been revised lower.

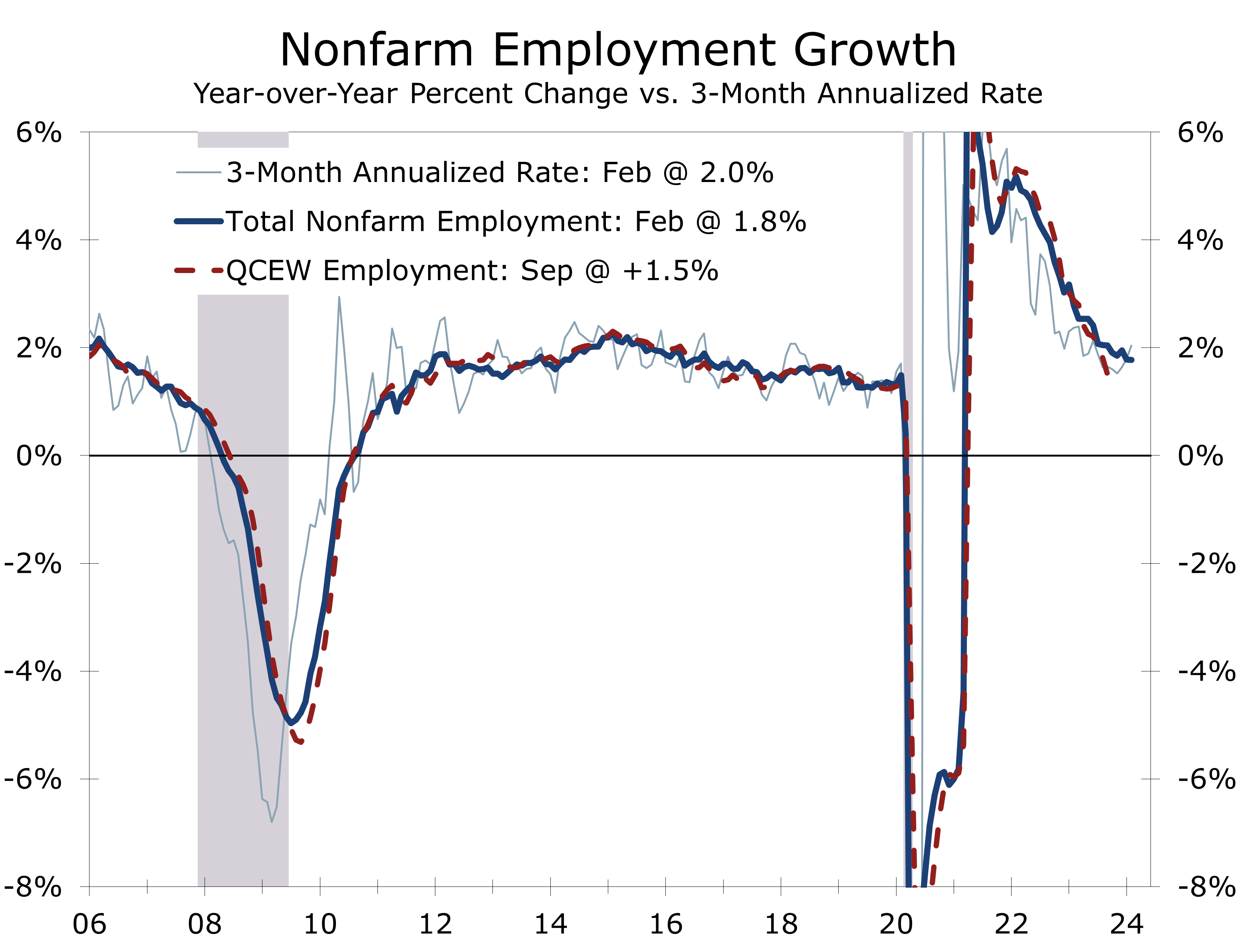

This was the case in the February report, which saw payroll growth revised lower for January and December by a combined 167,000 jobs. Even after the downward revisions, payroll growth for the past three months still averaged a whopping 265,000 jobs per month. Nonfarm employment has risen at a 2% annual rate over the past three months, slightly ahead of the 1.8% pace maintained over the past year.

We suspect job growth is currently significantly overstated and look for hiring to decelerate.

Job growth around yearend is notoriously volatile and may be even more so today, given the wide swings in economic activity during and after the pandemic lockdowns. These wider swings likely distorted seasonal adjustments.

We suspect payrolls are now overstated, as recently released QCEW data reveal only a 1.5% year-to-year increase in Q3 2023, approximately 800,000 jobs fewer than the currently reported 2.4% growth. The smaller job gain will show up in next year’s annual revisions.

We do not believe there is anything nefarious in today’s overstated jobs figures. For starters, the response rate to the monthly employer survey is well below its pre-pandemic norm, resulting in larger revisions to prior month’s data. Seasonal adjustment is also likely being exaggerated by the larger swings in payrolls that occurred around the pandemic. Additionally, employers are holding onto seasonal hires amidst a persistently tight labor market.

Hiring was broad based, as improved weather lifted hiring in a number of industries.

Job growth was broad-based in February, as hiring rebounded in several industries previously hindered by unusually harsh winter weather in January. Construction payrolls rose by 23,000 in February, driven by significant gains in heavy construction. Hiring also saw a resurgence in transportation, warehousing, retail, and restaurant sectors. Overall, we estimate that the improvement in weather contributed to around 50,000 of February’s net job gains.

Although hiring rebounded in many industries, job growth remained highly concentrated, with health care (+66.7K) and social assistance (+24K) accounting for nearly one-third of February’s gain. Government (+52K) and leisure and hospitality (+58K) also experienced robust job gains. However, manufacturers cut 4,000 jobs.

We expect nonfarm payroll growth to decelerate to 160,000 jobs per month this spring. The unemployment rate is also expected to edge higher to just over 4%. This should allow the Fed to cut the federal funds rate by a quarter point in June, followed by similar cuts in September and December.

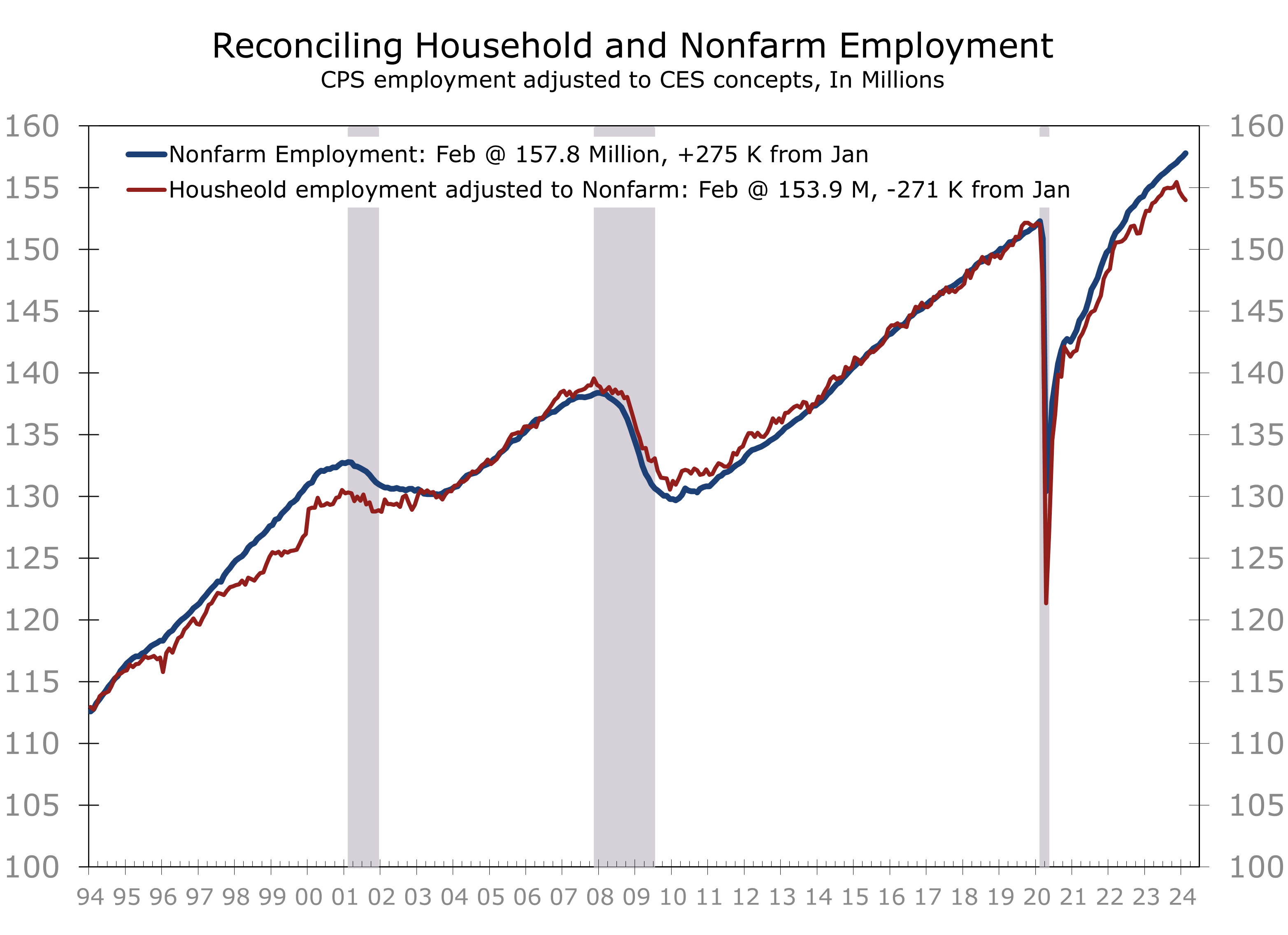

February’s household employment data was surprisingly weak. The number of employed individuals fell by 184,000, while the labor force increased by 150,000, resulting in 334,000 more unemployed. As a result, the unemployment rate rose to 3.9%.

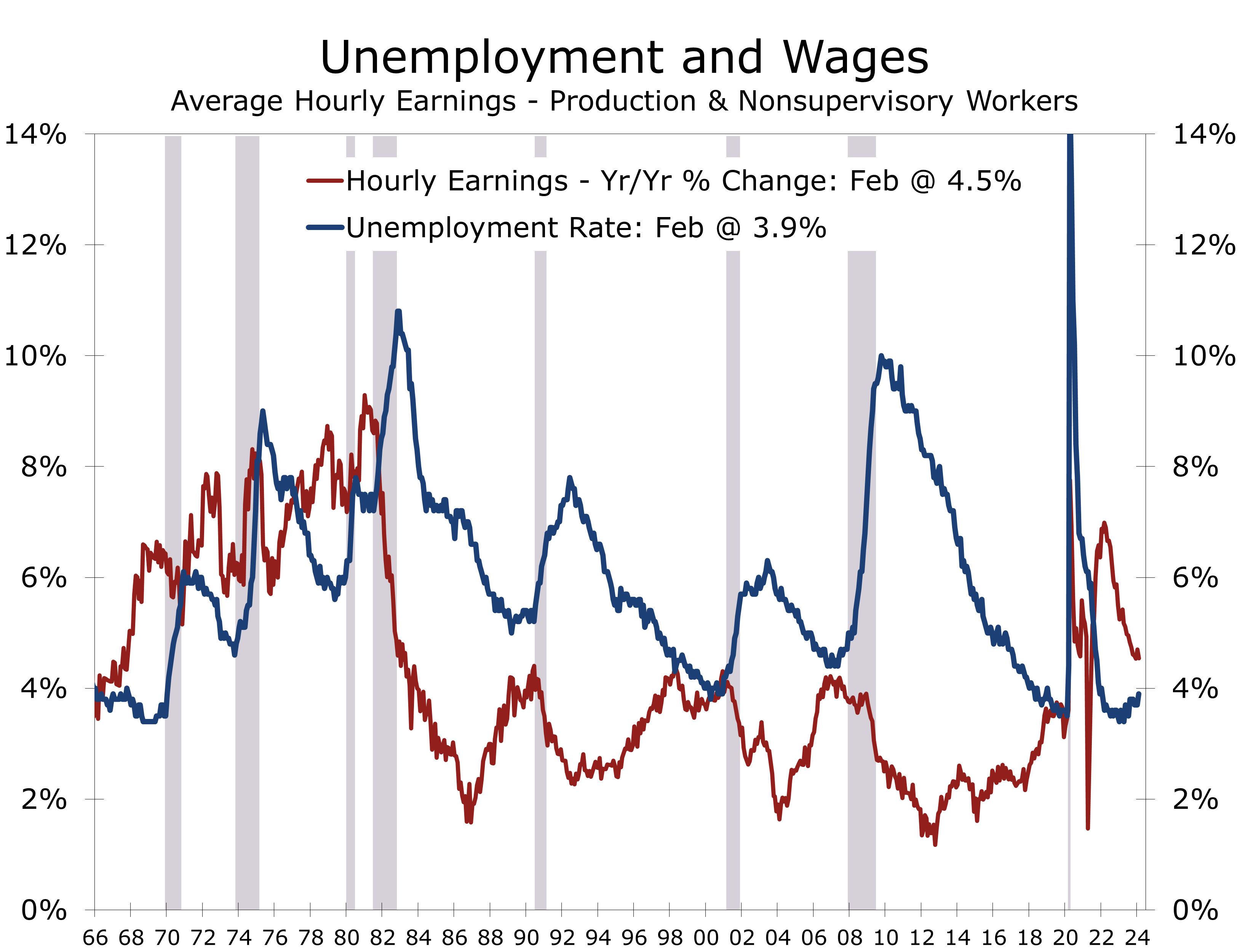

A rebound in weekly hours helped reverse last month’s spike in average hourly earnings.

Household employment, which has historically been good at detecting turning points, is meaningfully weaker than the payroll data when viewed on a consistent basis. Adjusted household employment has now fallen for three consecutive months and is down a collective 1.474 million jobs since November.

Rising unemployment should help contain inflation. Average hourly earnings grew by just 0.1% in February and are now up 4.3% over the past year.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.