Rough Start, Rough Year?

- The New Year got off to an inauspicious start, with an individual inspired by ISIS driving a car through a crowd of New Year’s revelers on New Orleans’ iconic Bourbon Street. This attack was followed by an explosion involving a Tesla Cybertruck at the Trump Hotel in Las Vegas, which was later determined to be a suicide incident rather than a terrorist act. Shortly thereafter a spate of horrendous wildfires broke out across Los Angeles that will have far-reaching consequences.

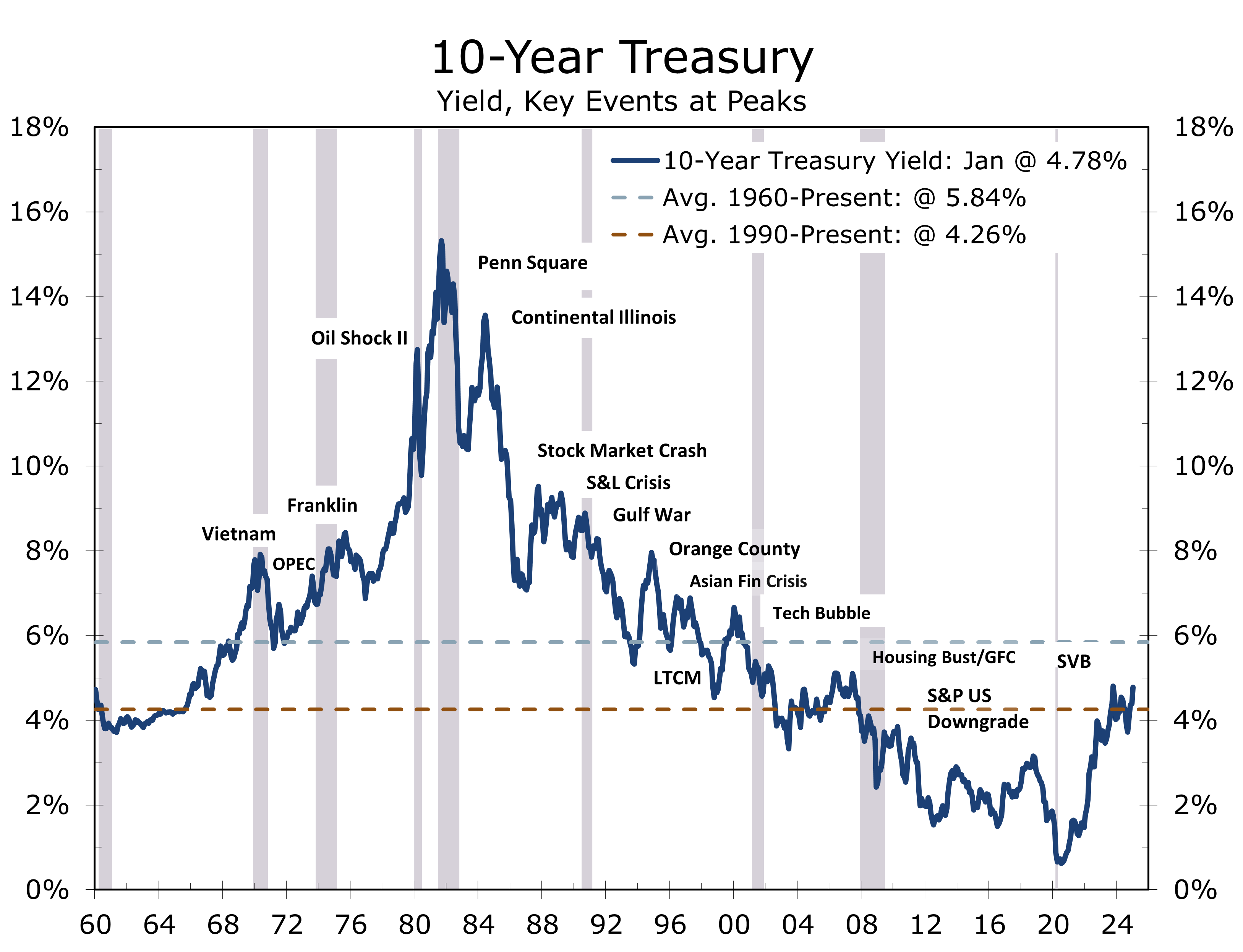

- The financial markets also got off to a rough start, with stronger economic growth and heightened inflation concerns driving the 10-year bond yield to their highest levels in more than a year. The jump in interest rates, further erased any remaining post-election gains in the stock market.

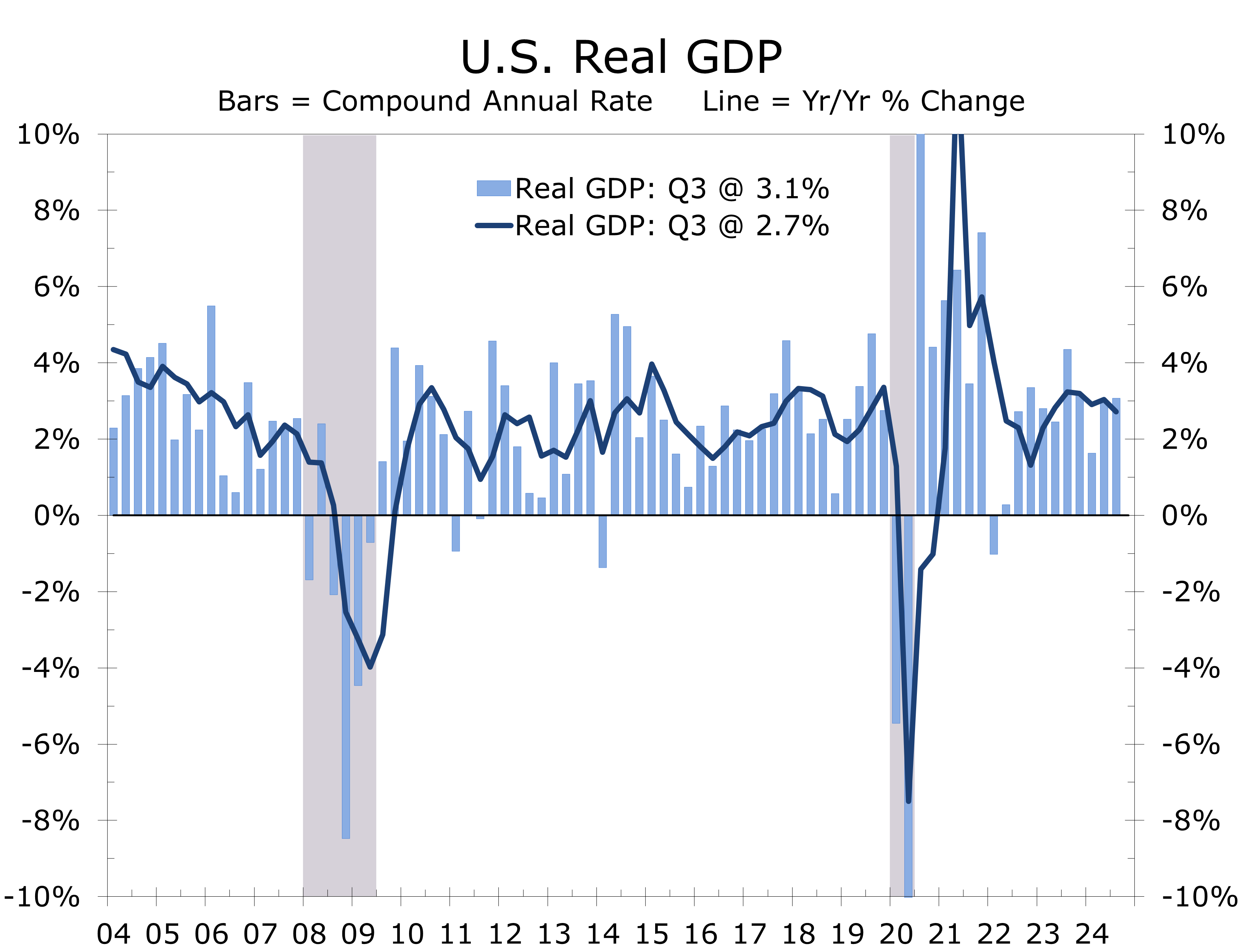

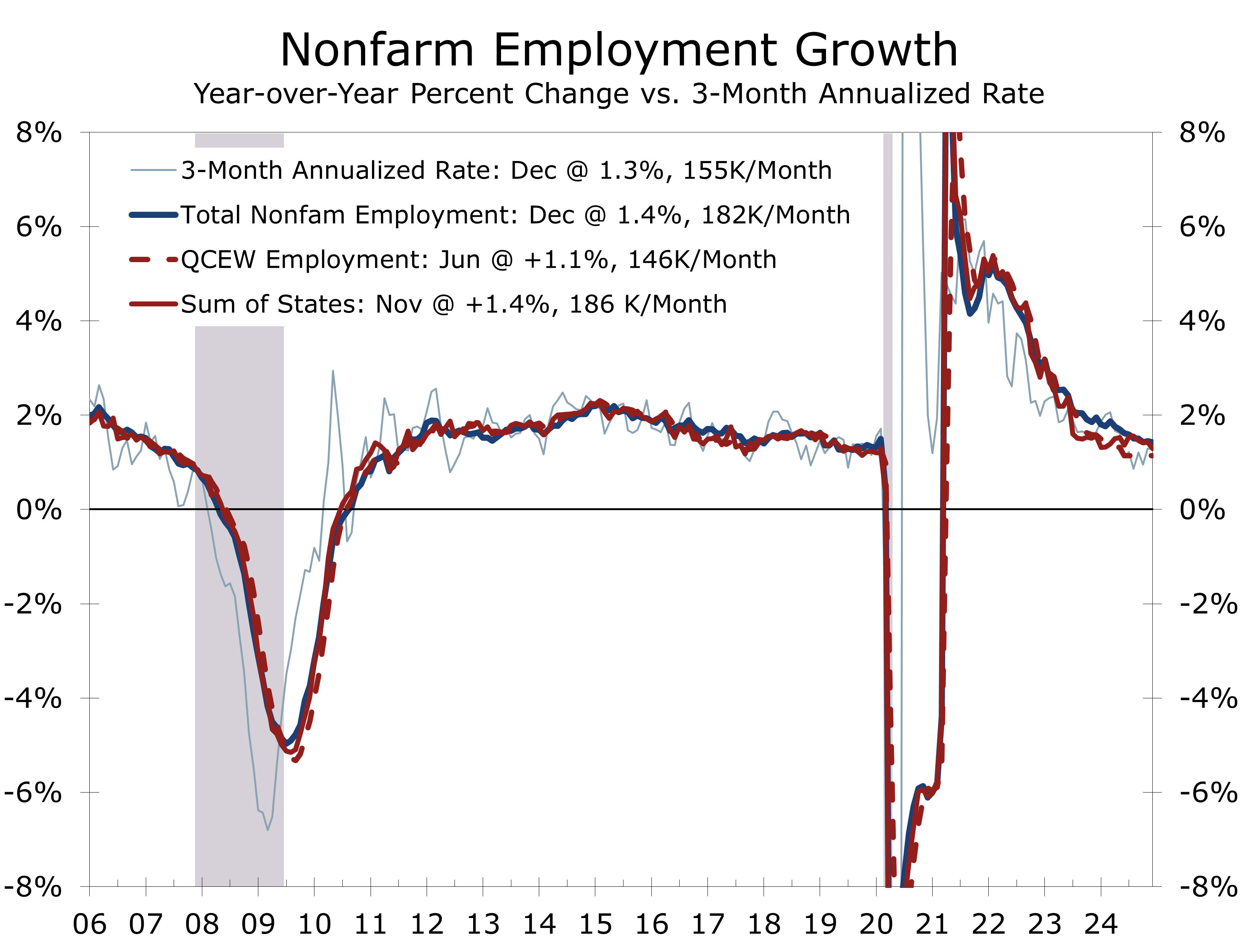

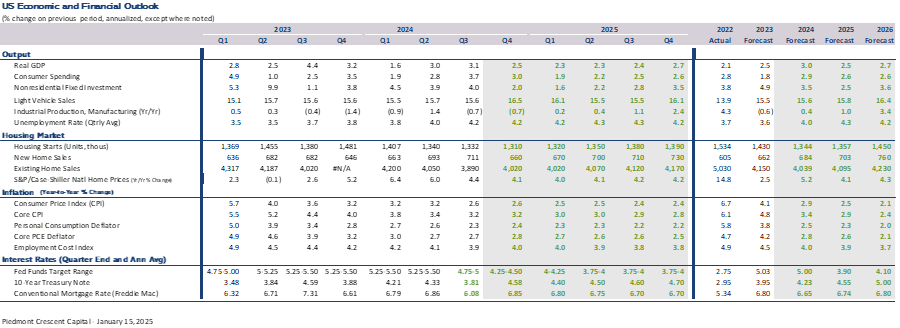

- Inflation concerns are tied to the surprisingly resilient U.S. economy, which began the New Year with strong momentum. While the ISM manufacturing survey shows the goods sector remains under pressure, the services side of the economy remains buoyant, and employers continue to add jobs in large numbers. Nonfarm payrolls ended 2024 on a strong note, with employers adding 256,000 net new jobs and the unemployment falling back to 4.1%. The latest Atlanta Fed GDPNow forecast pegs Q4 real GDP growth at a 2.7% pace.

- The prospect of higher tariffs is clearly impacting businesses and consumers. The University of Michigan’s Consumer Sentiment Survey showed a significant rise in near- and medium-term inflation expectations. Some evidence suggests preemptive buying ahead of potential tariff increases. However, we expect the tariff concerns to have limited impact, with consumer prices rising only 0.3 percentage points higher than otherwise this year.

- Stronger economic growth and rising inflation concerns are expected to keep interest rates elevated this year. After December’s stronger-than-expected jobs report, the expected timing for the Fed’s next rate cut shifted to September. However, this shift seems premature. The underlying jobs data were weaker than the headlines suggest, with gains concentrated in lower-paying, hard-to-fill roles. Additionally, upcoming annual revisions are likely to reveal that 2024 job growth was overstated.

- The geopolitical landscape under Trump 2.0 is marked by renegotiation on multiple fronts. Talks about Greenland, Canada, and the Panama Canal seem to be trial balloons or strategic diversions. Trump’s immediate priority is assembling his cabinet, followed by focusing on immigration and trade, with hopes of securing a deal alongside an extension of his first-term tax cuts.

The start of the New Year was marred by a series of tragic events, casting a pall over the nation’s hopes for a more peaceful and prosperous year. New Year festivities in New Orleans were abruptly shattered when an individual inspired by ISIS drove a vehicle into a crowd of revelers on Bourbon Street, leaving a trail of devastation in its wake. This act of violence, reminiscent of similar attacks in other parts of the world, served as a stark reminder of the ongoing threat of terrorism and raised questions about whether the world will see a revival of ISIS, particularly in the wake of the collapse of the Assad government in Syria.

Following this horrific incident, another shocking event unfolded in Las Vegas, where an explosion involving a Tesla Cybertruck at the Trump Hotel which injured several people and caused minor damage to the entry area of the hotel. While later investigations revealed the explosion to be a suicide rather than a terrorist act, the incident further heightened anxieties and underscored the fragility of safety and security in public spaces. These incidents also raise the prospect of more federal resources going toward combating terrorism at a time that the incoming Trump Administration would like to find ways to trim the federal budget and reduce the deficit.

President-elect Trump’s 2024 election victory was certified by congress without issue on January 6. Recently, Trump has garnered attention with proposals to purchase Greenland, reclaim the Panama Canal, and redefine relations with Canada. While his ambitions regarding Greenland appear grounded in strategic considerations, his positions on Panama and Canada seem aimed at enhancing negotiating leverage. These initiatives reflect a broader focus on countering the growing influence of China and Russia in the Arctic and addressing China’s dominance over key global shipping choke points.

Just as events appeared to be shifting to a more positive track, a series of devastating wildfires erupted across Los Angeles, wreaking havoc on the region. The infernos raged out of control, causing widespread destruction, displacing thousands of residents, and leaving behind a trail of devastation. The latest estimates show at least 24 people have died and more than 12,000 homes, businesses and public structures have been destroyed. Early estimates put the monetary damages at more than $90 billion, only a portion of which is insured. The impact of these fires will undoubtedly be far-reaching, affecting much more than the local economy and families impacted. Part of the runup in bond yields and selloff in the stock market is likely in anticipation of the billions of dollars insurance companies and governments will need to raise to fund recovery and rebuilding efforts.

Despite the inauspicious start to the year, the economy continues to display a great deal of resilience. Early January reports show robust service sector activity, solid holiday spending, and a strong labor market, with 256,000 jobs added in December and unemployment falling to 4.1%. The Atlanta Fed GDPNow projects 2.7% Q4 GDP growth. Our own forecast for Q4 growth is a touch softer at 2.5%.

The December jobs report appears stronger at first glance than it is beneath the surface. The data reflects a resilient but moderating labor market. While nonfarm payrolls surged by 256,000, significantly exceeding expectations, underlying trends suggest employment conditions are decelerating, albeit less sharply than anticipated. The labor market remains tight but is gradually rebalancing.

Payroll growth, though strong and technically broad-based, remains concentrated in just a few sectors. The 1-month diffusion index, measuring the share of industries adding jobs, fell 2.6 points in December to 56.4. While this still indicates broad gains, most job growth stems from health care, social services, leisure and hospitality, retail, restaurants, bars, and government. A sizable proportion of these roles, such as home health aides, staff at medical offices, hospital workers, social workers, restaurant employees, retail clerks, bus drivers, sanitation workers, and maintenance staff, are lower-paying, on-site positions. These essential roles have been difficult to fill, particularly when higher-paying jobs with more flexible work arrangements were more abundant.

The unemployment rate fell to 4.1% from 4.2%, while the underemployment rate also decreased, signaling a tightening labor market. Household employment increased by 478,000 in December, but when adjusted to the same standard as nonfarm payrolls, the rise was only 106,000. The labor force participation rate remained unchanged at 62.5%. Wage growth was modest, rising 0.3% month-over-month and just 3.9% year-over-year. These modest gains reflect compositional shifts, with bulk new jobs in lower-paying occupations, which dampened average hourly earnings. Alternative measures show slightly greater wage pressure.

The market reacted strongly to the unexpectedly robust jobs report, with the 10-Year Treasury yield surging and expectations for a Fed rate cut pushed back to September. We believe this reaction overstates the labor market’s strength. The annual payroll employment revisions will be released with January’s employment report on February 7. We expect these revisions to show about 600,000 fewer jobs added last year than currently reported, based on QCEW and state employment data. However, the revisions primarily affect data from March 2023 to March 2024 and influence estimates for the remainder of the year. Stronger immigration this past year, including the use of temporary work visas, may lead to a smaller revision than expected. If that proves to be the case, the recent tightening in immigration suggests a lower potential growth rate moving forward.

The financial markets were further unnerved by unexpectedly poor results from the early January University of Michigan Consumer Sentiment Survey. Consumer sentiment dipped slightly, falling to 73.2 from 74.0 in December, which was only modestly worse than expected. The decline was entirely driven by the expectations component, which fell 3.1 points to its lowest level in six months, reflecting increased concerns over future economic conditions and inflation. In contrast, the current conditions index rose 2.8 points, as low gasoline prices and solid employment conditions continued to bolster perceptions of personal finances.

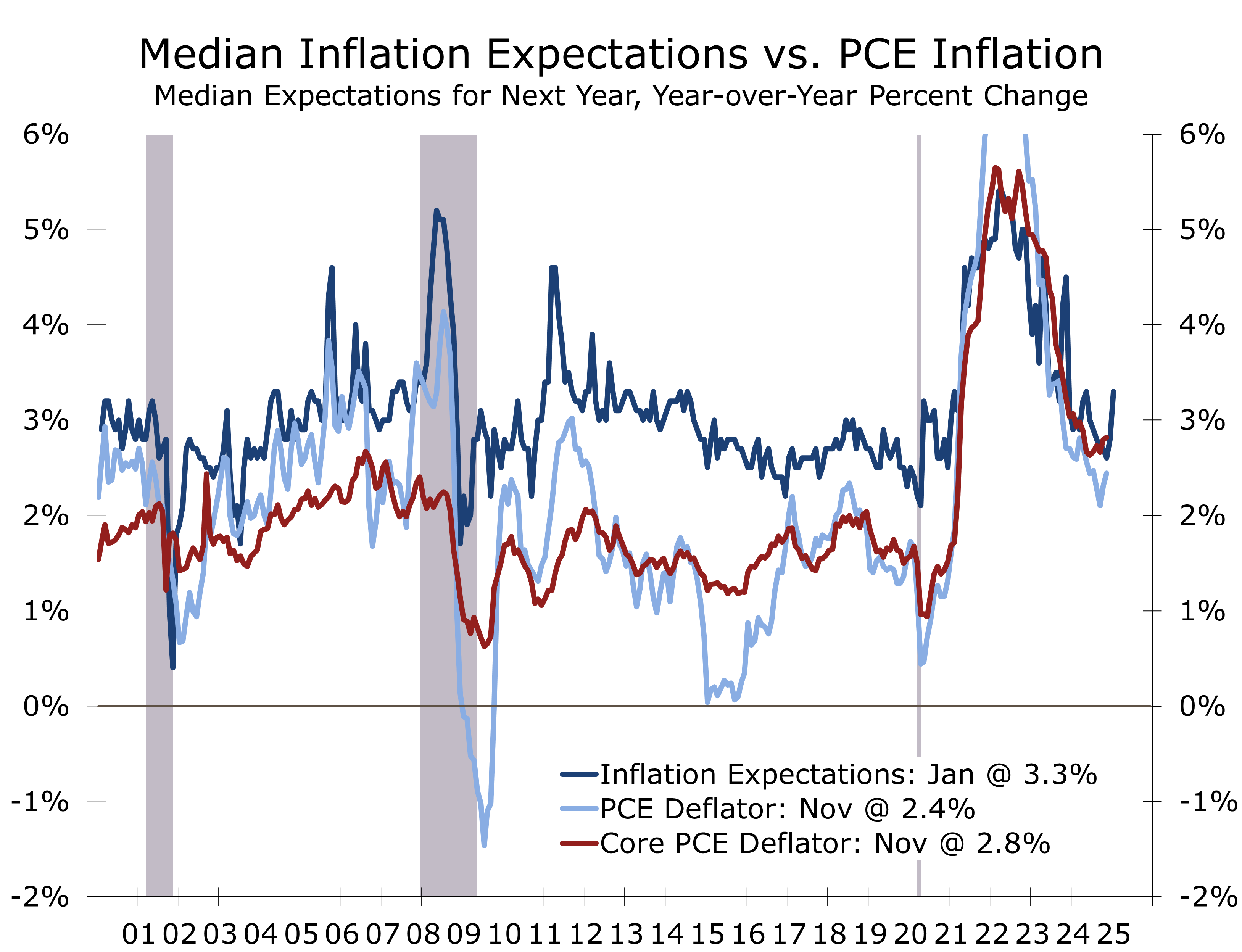

The divergence between the two indices highlights consumers’ growing worries about inflation and some trepidation about the incoming Trump administration, which promises to unleash significant changes. While earlier progress in slowing inflation had brought some relief, concerns about future price increases—exacerbated by uncertainty surrounding tariffs—dampened sentiment. Year-ahead inflation expectations surged to 3.3%, up from 2.8% in December, marking the highest level since May 2024. Long-term inflation expectations also increased, climbing 0.3 percentage points to 3.3%, the largest monthly increase since May 2021 and the highest level since June 2008.

While the surprisingly large jump in inflation expectations is unnerving, it is important to note that the preliminary Consumer Sentiment data, particularly the inflation components, are often misleading. The more comprehensive data reported at end of the month often reverse early-month swings in inflation expectations entirely. That said, there are ample reasons to believe the uptick in inflation expectations is more genuine than in the past. Progress on reducing inflation has stalled in recent months, and the Fed has acknowledged that the path back to its 2% inflation target is likely to be longer and more uneven than previously anticipated.

Heightened concern about inflation likely reflects recent price hikes at grocery stores, particularly for frequently purchased items such as eggs. The UMich notes that the rise in inflation concerns is evident across various demographic groups, with particularly strong increases among lower-income households and politically Independent-leaning individuals. Combined with added inflationary risks from tariffs, inflation expectations may remain elevated in the near term, giving the Federal Reserve further reason to remain cautious. The Fed places significant emphasis on keeping inflation expectations anchored and will work to discourage consumers from accelerating purchases to stay ahead of anticipated price increases.

Long-term interest rates have risen steadily since the Fed began reducing its federal funds rate target last September. Initially, the Fed’s half-point rate cut signaled a pivot toward supporting economic growth, even if it meant a longer timeline for achieving its 2% inflation target. While that approach seemed appropriate at the time, stronger employment data and slightly higher-than-expected inflation since the September meeting have complicated the narrative. To address this, the Fed revised its Summary of Economic Projections (SEP), clarifying that it would proceed cautiously with future rate cuts and likely refrain from lowering rates at the January FOMC meeting.

The climb in long-term interest rate accelerated following the stronger than expected employment report, rising to 4.78% – their highest level since November 2023. The yield curve has steepened, with the spread between the 10-Year and 2-Year Treasury widening to 39 basis points. Long-term rates are rising in other developed economies as well, most notably France, the U.K. and Japan, where they threaten to produce an even greater drag on these slower growth economies. The rise in long-term rates is primarily attributed to an increase in the term premium. This premium, which is the compensation investors require for the increased risk associated with holding longer-term bonds, reflects growing concerns about persistent inflation as well as the potential for future economic volatility.

The rise in long-term interest rates has disrupted the stock market rally, particularly for high-growth tech stocks with elevated or infinite price-to-earnings ratios, a trend that became evident when the 10-year Treasury yield surpassed 4.50%. While earnings season may provide temporary support, the Nasdaq—home to many high P/E stocks—will likely remain under pressure until the yield falls below 4.50%, which we expect by spring. Sharp increases in long-term rates typically slow economic activity, prompting rates to retreat.

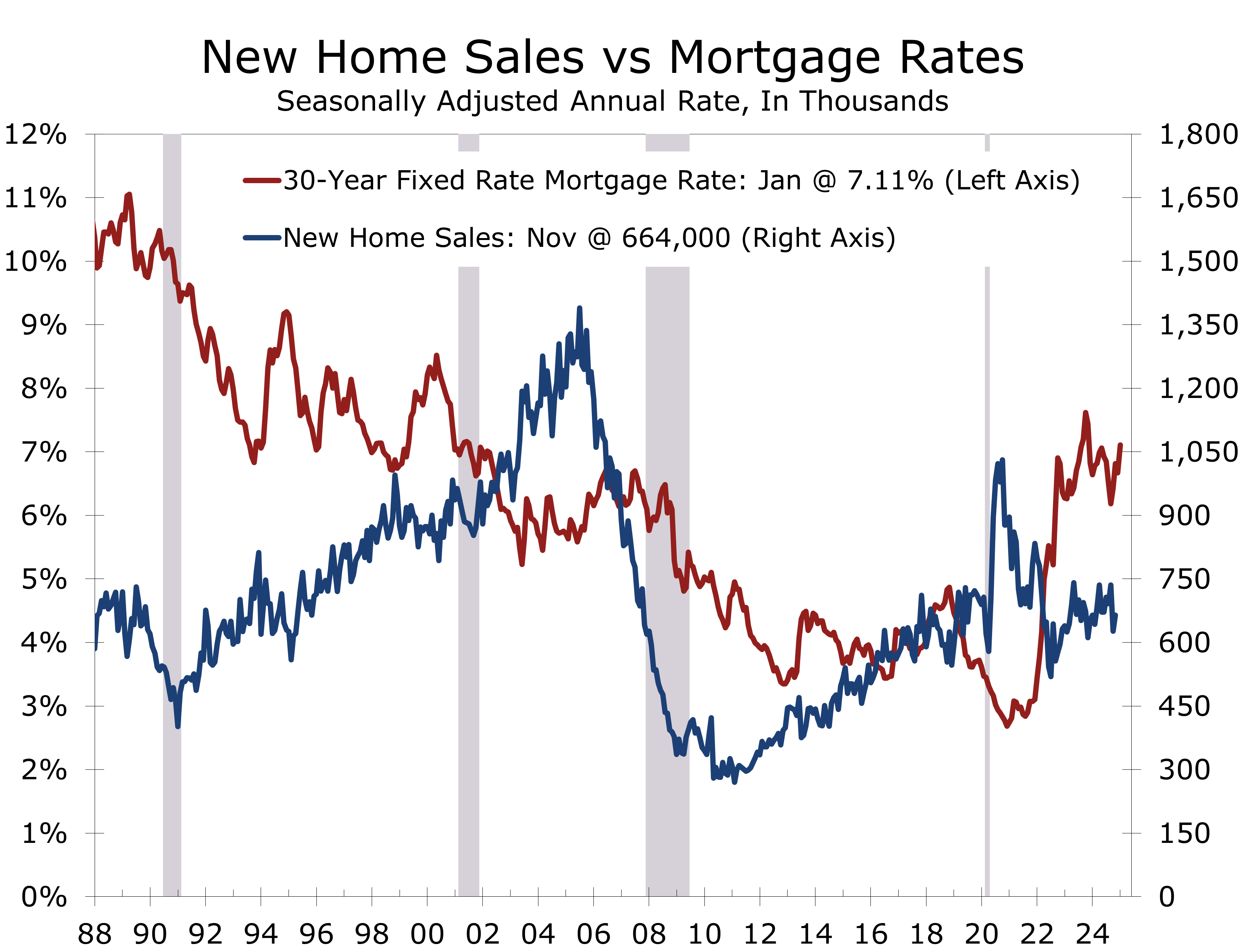

Higher interest rates are already significantly affecting the most rate-sensitive sector of the economy: housing. Mortgage rates above 7% have dampened demand, which was already constrained by limited inventory. However, new home inventories are rising, particularly in the South. The weakness in housing is reverberating throughout the economy, reducing demand for furniture, home furnishings, appliances, and other household-related services. We look for mortgage rates to pull back this spring as banks increase mortgage lending efforts.

The steady rise in long-term interest rates has become an early defining economic theme this year, driven by heightened uncertainty and rising term premiums. Much of this uncertainty stems from Donald Trump’s political return and his disruptive rhetoric, including post-election threats of steep tariffs on allies and competitors. His use of tariffs as leverage for trade, immigration, and security negotiations adds tension, particularly with global responses remaining unclear.

At the time of writing, there are credible reports promising negotiations involving the Biden Administration, Trump’s team, Hamas, and Israel to resolve the conflict and secure hostage releases. A successful resolution could enhance Trump’s credibility and pave the way for a Ukraine deal. However, any deal with Russia must include credible security guarantees—such as EU and NATO membership for Ukraine—to prevent future aggression. Weak agreements risk emboldening adversaries like China, Russia, Iran, and non-state actors.

Global conflicts are not the primary force behind rising bond yields. In the U.S., yields have climbed as the Fed prioritizes labor market support over a swift return to its 2% inflation target. A soft landing seems unlikely given ongoing fiscal stimulus from the IRA, CHIPS Act, and Infrastructure Bill. Rebuilding efforts in the South after this past fall’s hurricanes and in Southern California following the ongoing wildfires will further strain federal budgets, raising concerns about persistent deficits.

The prospect of new governments in Canada, the U.K., Germany, France, and Australia introduces additional global uncertainty. Policy changes in these nations are likely to mirror U.S. trends, as leaders aim to ensure workers receive a greater share of economic gains amid globalization and advancements in technologies like AI.

Long-term rates are settling into a new normal. Since 1990, the 10-year Treasury yield has averaged 4.26%, reflecting periods of quantitative easing and ultra-low rates, while the broader average since 1960 is 5.84%, influenced by past inflationary spikes. Policymakers are unlikely to repeat the mistakes of the 1970s, but rates are expected to stay within this range (4.26% to 5.84%) as long as inflation exceeds 2% and the economy maintains solid growth. Upside risks could materialize in 2025, driven by a surge in mergers and acquisitions alongside the Treasury’s need to refinance trillions in debt.

We have raised our estimate for fourth-quarter real GDP growth, reflecting stronger-than-expected economic data. Hiring accelerated in Q4, and holiday sales exceeded consensus estimates. However, higher interest rates continue to weigh on the economy, particularly in the already stretched housing market, where mortgage rates have climbed above 7%. Recent natural disasters, including Hurricane Helene in the Florida, Georgia and the Carolinas and wildfires in Southern California, will exacerbate housing pressures. Asheville, which already had one of the nation’s tightest housing markets, and Southern California are expected to see increased demand for residential rentals as displaced residents and firms seek housing. This rental pressure, especially in major markets like Los Angeles, presents another obstacle to the Fed achieving its 2% inflation target.

The disasters are also expected to dampen U.S. economic activity in the near term. Los Angeles County, home to 9.6 million people, and would rank as the 11th most populous state. Los Angeles accounts for 25% of California’s GDP and 3.5% of national GDP. Its $800 billion economy driven by high-value industries like aerospace, pharmaceuticals, IT, and entertainment, would rank as the 5th largest U.S. state by GDP, behind California, Texas, Florida and Illinois. While hurricanes and wildfires will weigh on growth in early 2025, rebuilding efforts are projected to boost economic activity in the second half of 2025 and into 2026.

We also anticipate the economy will gradually adapt to higher interest rates. The incoming Trump Administration will likely usher in a new wave of deregulation, make prior tax cuts permanent, and ease the state and local tax deduction cap. The creation of the Department of Government Efficiency (DOGE) is expected to achieve meaningful discretionary spending cuts over the next two years. These efforts, though limited without entitlement reform, may enable broader progress at addressing the budget deficit in later years.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice. Any forward-looking statements or forecasts are not guaranteed and are subject to change at any time. Information from external sources have not been verified but are generally considered reliable..