Solid Job Growth Will Keep the Fed on Hold

- Nonfarm payrolls rose 143,000 in January, with the unemployment rate dipping to 4.0% – the lowest since May 2024.

- Job growth is concentrated in health care, retail trade, and government sectors, which accounted for 93% of overall job gains.

- Revised data shows 620,000 fewer jobs added through 2024 than previously reported, which was now worse than expected and should keep the Fed on hold.

- The lower unemployment rate reflects a further tightening in labor market conditions, with a slowdown in immigration ahead of the presidential election likely contributing to the trend.

- Average hourly earnings rose by 4.2% year-over-year, reinforcing concerns about wage-driven inflation and caution from the Fed.

- The January employment report suggests the labor market can handle prolonged higher interest rates. While January job growth was weaker than expected, upward revisions to prior months raised the three-month average to 237,000 per month. Annual benchmark revisions were in line with expectations, removing the need for a more immediate rate cut.

Nonfarm payrolls increased by 143,000 in January, while the unemployment rate fell to 4.0%. Job gains remain heavily concentrated in health care, social assistance, retail trade, and government, which together accounted for 93% of total job growth. Employment at motor vehicle assembly plants, temporary staffing firms, and in the mining and energy extraction sectors declined slightly.

The annual benchmark revisions show 620,000 fewer nonfarm jobs were created through the end of 2024 than previously reported, aligning closely with our estimate. This downward revision likely diminishes the urgency for the Federal Reserve to cut interest rates.

Annual benchmark revisions were no worse than expected, leaving the Fed on hold.

January’s decline in the unemployment rate reflects a tightening labor market. This year’s population adjustment was unusually large due to a spike in immigration. Had the new population figures been applied to earlier data, the unemployment rate would have fallen by 0.2 percentage points, to 3.9%.

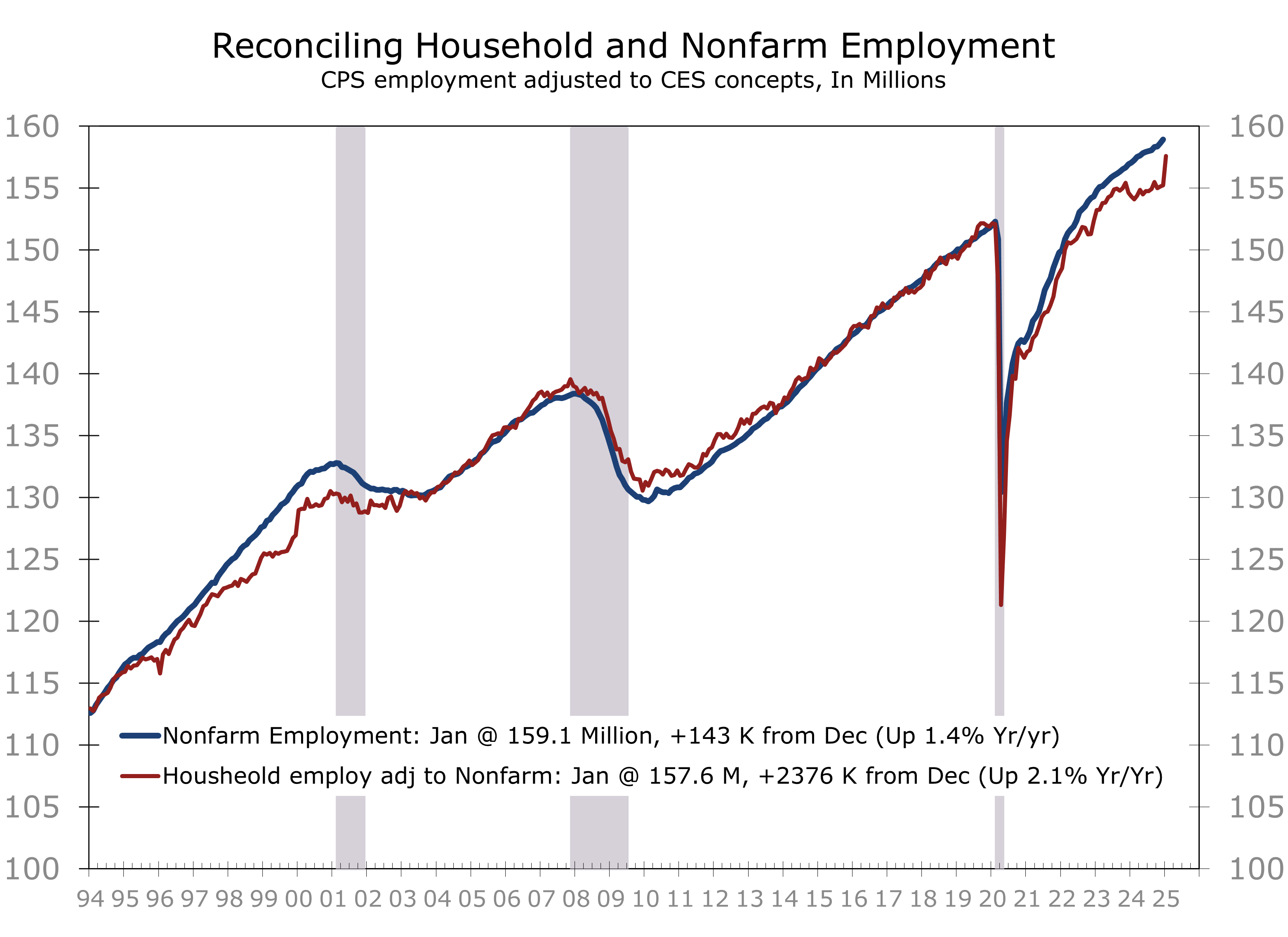

The annual adjustments also helped close what had been an unusually wide gap between nonfarm payrolls (CES) and the BLS-adjusted civilian employment series (CPS). The gap ended the year with adjusted civilian employment 4.3 million jobs below nonfarm payrolls but narrowed to just 1.46 million fewer in January.

While job growth moderated in December, it remains solid, averaging 237,000 per month over the past three months and 176,000 per month over the past year. With the unemployment rate at 4% and rising inflation expectations, the Fed will likely remain on hold.

Overall job growth is moderating and the breadth of industries adding jobs is narrowing.

While job growth remains solid, the pace of growth is moderating, and the breadth of industries adding staff is narrowing. Health care, retail, and government jobs dominated job growth this past year, and that trend continued into January. Health care added 44,000 positions, driven by gains in hospitals (+14,000), nursing facilities (+13,000), and home health care services (+11,000). Retail trade added 34,000 jobs, led by general merchandise retailers (+31,000). Government employment rose by 32,000.

The January jobs data signals that the labor market can withstand higher short-term interest rates for an extended period. While job growth in January was weaker than expected, upward revisions to prior months lifted the three-month average to 237,000 per month, and the annual benchmark revisions were no worse than expected. The Fed would have needed to see a significant downward revision to the benchmark data to justify a more immediate rate cut.

The unemployment rate fell to 4.0%, the lowest since May 2024, highlighting the tight labor market. January’s data, including annual population updates, suggests that a slowdown in immigration—particularly ahead of the presidential election—is further tightening labor conditions.

The unemployment rate edged higher and household employment data remain weak.

Average hourly earnings rose 4.2% year-over-year, partly due to a later survey period capturing a greater proportion of annual wage increases. Combined with rising inflation expectations, this raises concerns about wage-driven inflation, prompting the Fed to take a cautious approach. With solid job growth continuing, the Fed can afford to wait for more data before further easing its previous tightening.

The annual revisions and population adjustments provide clarity on labor market strength. Most employment measures are now in sync, offering a clearer view of labor market conditions. While we continue to monitor the narrowing breadth of job gains, the labor market remains tight and maintains strong momentum.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

February 7, 2025

Mark Vitner, Chief Economist

(704) 458-4000

mark.vitner@piedmontcrescentcapital.com