Highlights of the Week

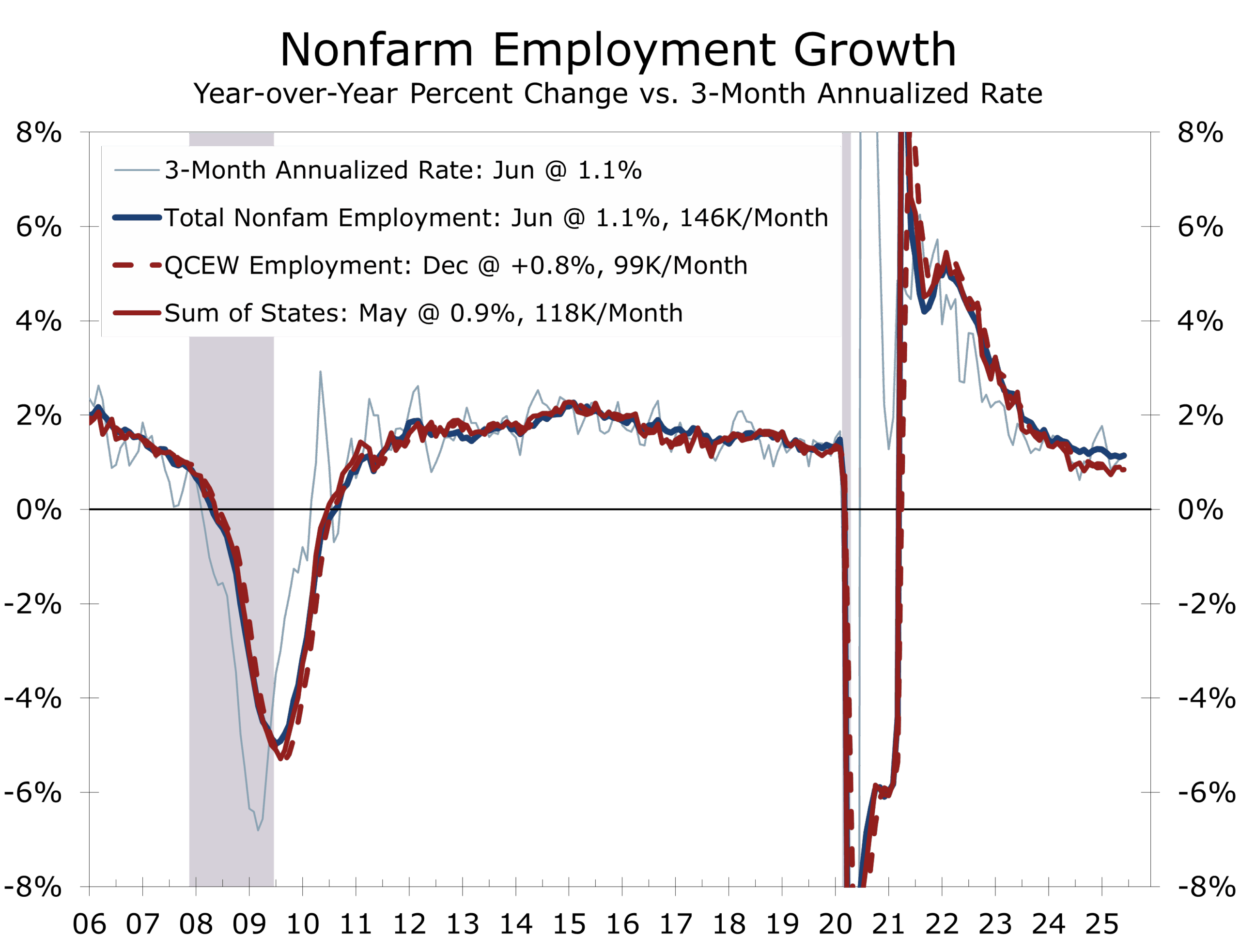

- June’s employment report showed modest headline growth, but hiring remains narrowly based and the most recent QCEW data points to a weakening labor market.

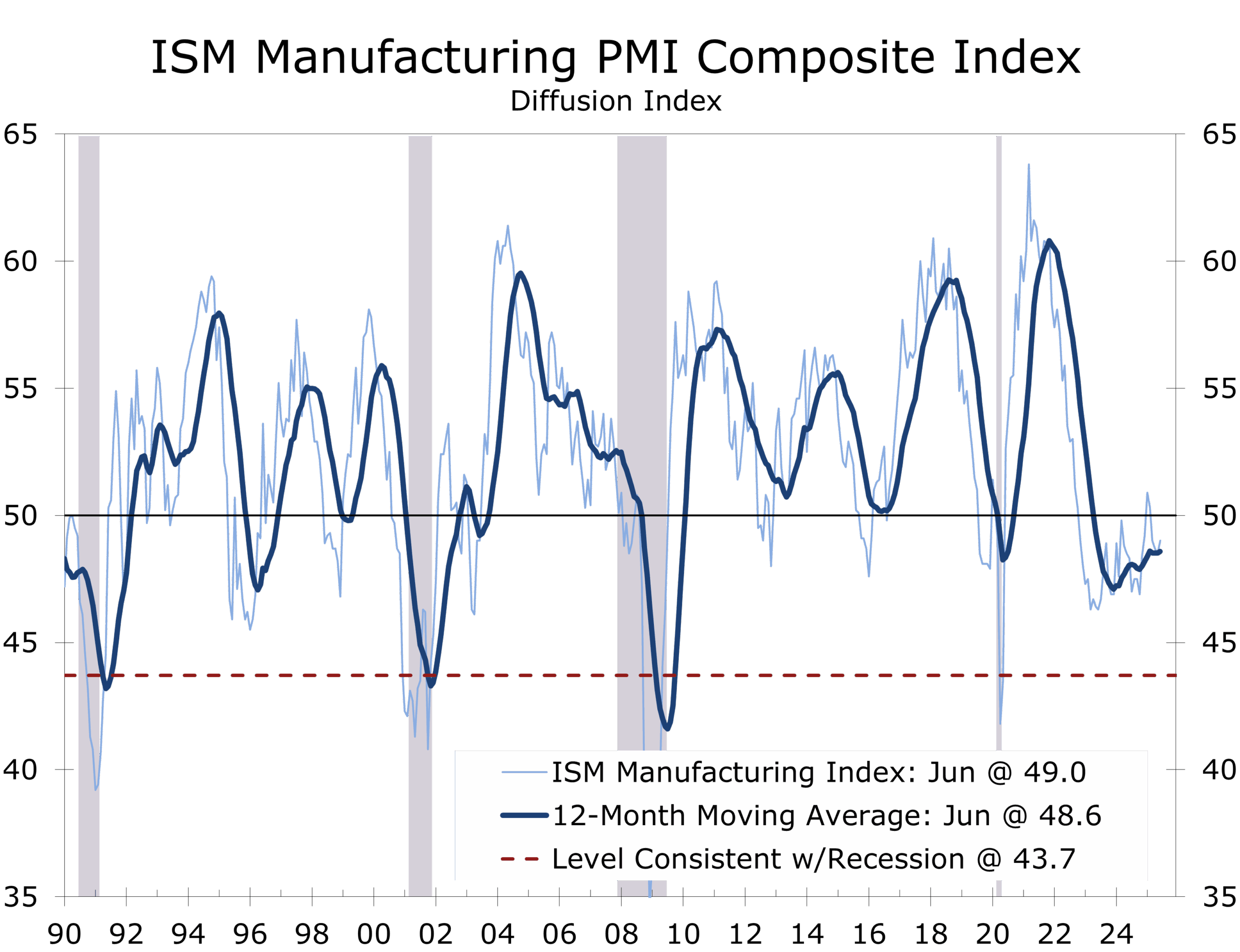

- ISM data confirmed the economy continues to grow modestly, with inflation pressures slightly easing.

- Construction spending continues to decline, with private residential and nonresidential investment both under pressure.

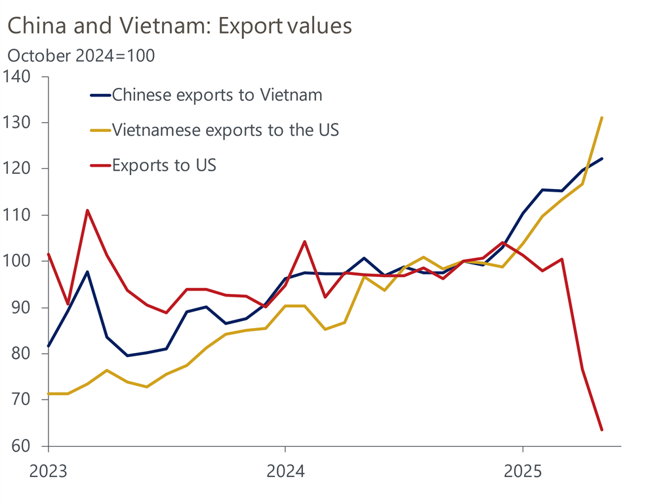

- The U.S. secured a tariff deal with Vietnam and moved closer to triggering tariff hikes on nations outside U.S. trade pacts.

- President Trump signed the “Big Beautiful Bill” into law, extending the 2017 tax cuts and prolonging massive budget deficits, fanning fears over fiscal dominance.

- Zohran Mamdani’s New York Democratic victory signals growing economic angst.

- The Texas Hill Country floods exposed breakdowns in local emergency preparedness, not federal weather forecasting programs.

- Uncertainty and volatility have pulled back considerably since the April 2nd Liberation Day announcements. While trade deals have been slow to materialize, the economy has likely passed the peak tariff impact. The Fed is also closer to cutting interest rates and the decision at the July FOMC meeting will likely be a closer call than currently thought.

Labor Market: Cracks Beneath the Surface

June’s nonfarm payrolls rose by 147,000, with modest upward revisions to April and May. The unemployment rate edged down to 4.1%, but the internals tell a different story. Hiring was concentrated in healthcare, education, and government. Employers have added an average of 150,000 jobs a month for the past three months, with most of that gain coming from healthcare, leisure and hospitality, and state and local government. Separately, the ADP employment measure reported a loss of 33,000 private-sector jobs during June, its first decline in 27 months—driven by a 47,000 drop at firms with fewer than 50 employees.

Even the slower growing nonfarm payroll numbers likely overstate job growth. As we’ve noted repeatedly, the QCEW data, which reflect a count of jobs from unemployment insurance tax rolls, suggest job gains have likely been overstated by around 900,000 jobs. We will get updated data through March 2025 (which is the preliminary source material used for the annual revisions) on September 9, three weeks ahead of the September FOMC Meeting. Another variable to watch is federal employment, which fell again in June and is down 69,000 since January. More declines are likely as retirements pick up, allowing attrition to further reduces staff levels.

The May JOLTS report showed job openings rising to 7.77 million, but 80% of the gain came from accommodation and food services—likely a seasonal blip or possibly a response to tightening immigration enforcement. Hiring dipped, layoffs remain low and the quits rate remains subdued. With the unemployment rate at 4.1%, it’s hard to argue the labor market is unbalanced—but momentum is clearly fading, as seen in the narrowing breadth of job gains, rising level of continuing claims and dwindling share of consumers stating that jobs are plentiful.

Slowing immigration is weighing on labor force growth and restraining the unemployment rate.

ISM: Stabilization Without Strength

The ISM Services index edged back into expansion at 50.8, while ISM Manufacturing remained just barely in contraction at 49.0. New orders softened to 46.4, while employment fell further to 45.0, with manufacturers trimming staff to cut costs amid margin compression from rising input costs, tepid final demand and tariff-related uncertainty. Production ticked up, but new order backlogs fell, and hiring remains on hold.

The ISM indices are consistent with slower economic growth but not a recession. The Manufacturing Index would need to dip below 43.7 to be consistent with a downturn. Still, the soft recent readings are another sign the economy is losing momentum.

Housing and Nonresidential Construction Weaken

Construction spending declined for the ninth straight month in May. Residential investment is now tracking an 7% annualized decline for Q2, driven by weakness in single-family construction and hesitancy among potential homebuyers. Nonresidential structures are also faltering, with business investment in structures on track to decline at a 5.5% pace in Q2. Data center construction is a bright spot, but factory and power structure investment is retreating, particularly for plants requiring foreign-produced machinery. The tax bill’s levy on China-linked solar and wind projects may further depress green infrastructure spending.

Trade and Tariffs: Trump’s Revenue Engine

President Trump announced a tariff agreement with Vietnam, reducing U.S. duties from 46% to 20% in exchange for duty-free access for American exports. Goods transshipped through Vietnam—primarily from China—will face a 40% tariff. This follows earlier bilateral deals with China and the U.K.

Vietnam maintains the third largest trade deficit with the U.S. and has become an important destination for manufacturing operations moving out of China due to trade or costs concerns, particularly for shoes, furniture and consumer electronics The 40% tariff goods routed through Vietnam is likely a signal of where Chinese tariffs are ultimately headed, particularly for transshipped products, regardless of which country they are routed through.

Fiscal Dominance and the Dollar

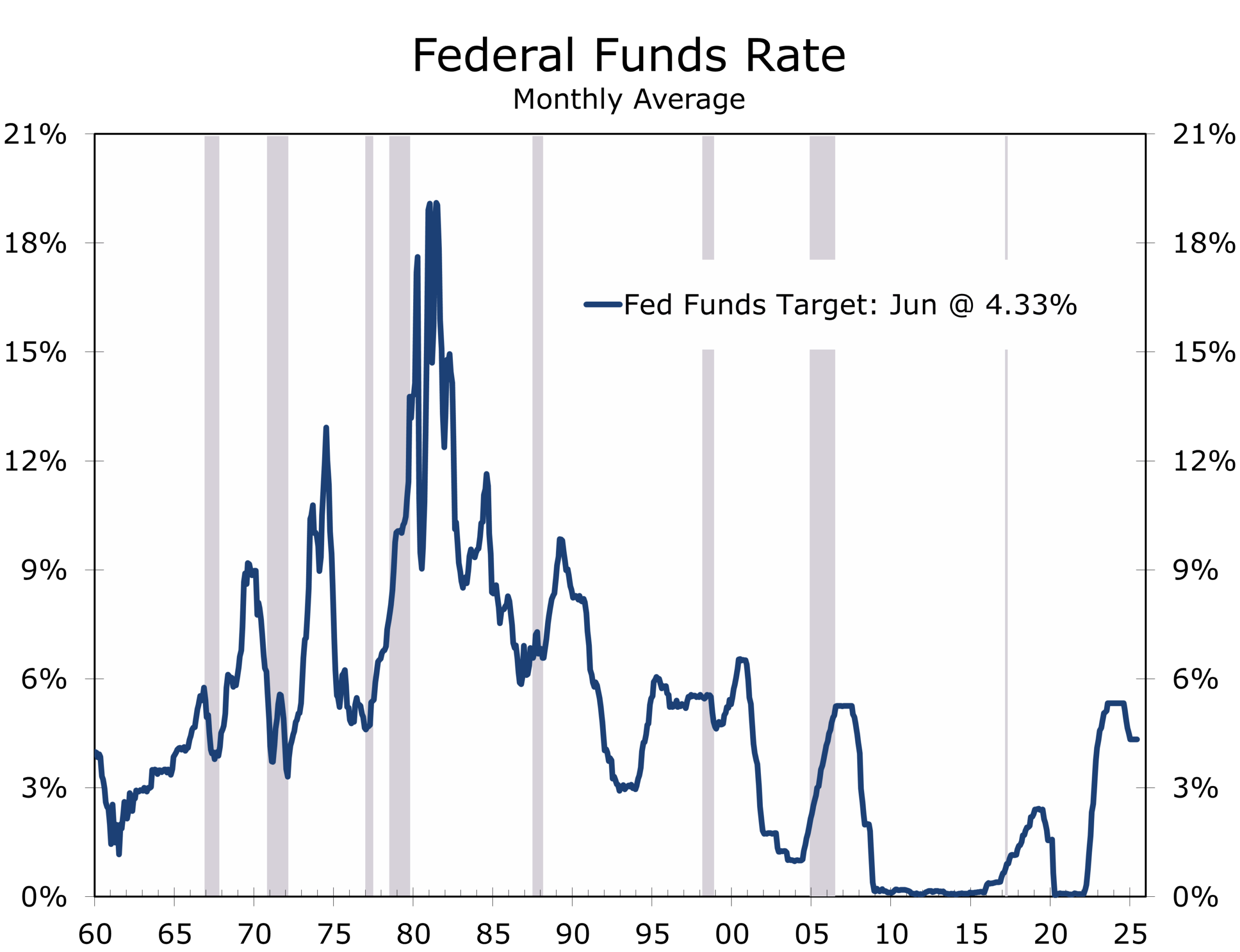

President Trump signed the expanded “One Big Beautiful Bill” into law, potentially increasing annual deficits to $3.3 trillion annually by 2035. The package relies on optimistic scoring and a Treasury pivot to short-term debt issuance. We feel the CBO is underestimating the positive impacts from the budget bill but still see extremely large deficits for as far as the eye can see. Trump is openly pressuring the Fed to lower rates to contain borrowing costs—a potential shift toward fiscal dominance.

Trump continues to pressure Powell to cut rates to spur growth and lower financing cost.

“Fiscal dominance” refers to a regime in which the central bank subordinates monetary policy to fiscal needs, effectively monetizing debt to keep government borrowing costs manageable. It’s not just about buying bonds—it is about the Fed losing the ability to fight inflation independently, cornered by the size of the deficit and rising interest payments.

We are not there yet, but the risks are no longer merely theoretical. The newly signed spending bill adds to an already unsustainable fiscal trajectory, and markets are questioning how long the Fed can keep monetary and fiscal policy in separate lanes. The weakness in the dollar, strength in gold and crypto are all warning signs about the unsustainability of fiscal policy.

Still, today’s Fed is far more independent than in the past—and far less likely to monetize debt outright. The greater risk may be the opposite: that the Fed will delay rate cuts simply to avoid the appearance of political capitulation. That would be a policy error. Inflation is clearly easing, PCE is near 2%, inflation expectations remain anchored or are becoming more so, and the real economy is slowing. Employment growth is narrowing, housing is stagnant, and business investment is losing steam.

In that context, the Fed should cut rates by 75 basis points, starting at the July FOMC meeting. September is more likely—but every delay increases the risk of overtightening into a slowdown already unfolding both above and beneath the surface.

The 1970s taught us what happens when monetary policy caves to political pressure. But that era also reminds us how quickly confidence-driven mistakes can become structural ones—especially when the Fed hesitates at the wrong moment.

Despite surging deficits, bond yields have been volatile, and the dollar has dropped nearly 11% year-to-date. Treasury auctions this week will once again test market demand amid growing concerns about foreign participation.

Mamdani and the Message from New York

Zohran Mamdani’s Democratic primary win in New York highlights rising discontent with establishment economic policy. Mamdani’s socialist platform has drawn comparisons to 1970s India, while his foreign policy stances have drawn criticism for anti-Israel and antisemitic rhetoric. Still, his rise reflects a deeper concern: the economy no longer works for many Americans. The share of national income going to wages has been declining for decades, a trend exacerbated by the rise of China and the erosion of U.S. manufacturing employment.

Both the far right and far left are gaining traction by focusing on pocketbook issues long ignored by the political center—even if many of their proposed solutions are economically incoherent or politically untenable. The underlying sentiment, however, is not to be dismissed: frustration with inequality, affordability, and economic insecurity is driving a new wave of political realignment. The two major political parties should focus on finding practical and meaningful solutions.

Israel: Escalation Avoided, Fragile Progress Continues

President Trump’s Monday meeting with Israeli Prime Minister Benjamin Netanyahu comes as the region shifts from confrontation to cautious diplomacy. A 60-day pause in Gaza fighting is underway, and indirect ceasefire talks between Israel and Hamas have resumed. Iran, weakened by Israel’s systematic destruction of its proxy network and then highly effective U.S. and Israeli airstrikes against its air defenses and nuclear infrastructure, has signaled openness to restarting nuclear negotiations, and the White House has opened quiet channels with Syria’s new government.

Trump hopes to leverage these developments into a broader diplomatic breakthrough—including an expanded Abraham Accords framework. Beyond Saudi Arabia, the administration is exploring the possibility of drawing in Syria and even Lebanon. While politically complex, such moves represent the most ambitious extension of the accords to date.

Meanwhile, an unprecedented initiative in Hebron could test a bottom-up model of Israeli-Palestinian diplomacy. Sheikh Wadee’ al-Jaabari and four other leading tribal figures have signed a letter recognizing Israel as a Jewish state and proposing the formation of an independent Emirate of Hebron. Their plan calls for joining the Abraham Accords, establishing a joint economic zone, and replacing the Oslo-era Palestinian Authority with clan-based leadership grounded in local legitimacy.

The initiative pledges “zero tolerance” for terrorism and outlines a phased labor partnership with Israel. It has been quietly supported by Economy Minister Nir Barkat and has drawn attention from both U.S. and Saudi officials. With the backing of clan leaders representing over 500,000 Hebron-area residents, the proposal could serve as a test case for a decentralized, pragmatic approach to governance. While the sheikhs’ plan represents a sharp departure from the stagnant Oslo framework, its success will depend on both political will and regional coordination.

A broader Middle East peace deal would have substantial carry through to other parts of the globe and would be a positive for global financial markets and U.S. leadership. Russia and China have used the Middle East conflict to tie the U.S. up and weaken support throughout developing countries. Without this wedge, more progress will be possible elsewhere.

Volatility Retreats, But Uncertainty Lingers

Despite economic crosscurrents, global business and financial markets do not appear overly anxious. Business sentiment surveys show muted concern, and the market-implied probability of severe outcomes (like a U.S. recession or a 20% drop in equities) has declined. Implied volatility in currency markets has also fallen, providing some stability following a long slide in the value of the dollar. Treasury yields have also fallen back off their recent highs, despite heightened concerns about persistent large budget deficits. Expectations for Fed rate cuts have also increased, with the markets currently pricing in between 3 and 4 quarter point cuts by the middle of next year, with kickoff coming in September.

Looking Ahead: Week of July 8–12

- NFIB Small Business Optimism (Tuesday, July 8): We are looking for a modest rise in the NFIB index, as easing geopolitical pressures and recent financial market stability boost expectations.

- Tariff Deadline (Wednesday, July 9): President Trump is expected to send ‘letters’ to countries without finalized deals. Watch for additional announcements on BRICS-aligned penalties.

- FOMC Minutes (Wednesday, July 9): Look for confirmation of the Fed’s cautious tone and insight into members’ views on tariffs and labor slack.

- Jobless Claims (Thursday, July 10): Jobless claims remain exceptionally low going into a seasonally volatile period for claims that could see initial claims move lower. Continued claims, however, continue to trend higher, reflecting a tougher market for job seekers.

- Treasury Auctions: 3-, 10-, and 30-year bond sales may test market tolerance for ballooning debt.

Final Thought: A Delicate Balance

Markets may be rallying, but the fundamentals are drifting. Hiring is slowing, margins are compressed, the Fed remains boxed in, and global trade rebalancing is still underway. Yet geopolitical risks have eased—at least temporarily—and fiscal stimulus is flowing. The second half of 2025 will be a test of execution. The pieces are now coming into place such that a modest, well-timed interest rate cut could set the stage for a resurgence in growth next year. Policymakers must stay disciplined until the inflation threat fully recedes.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

July 8, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000