Highlights of the Week

- The Beige Book confirms softer labor demand, more cautious consumers and producers, and still-resilient capital spending that continues to justify lower rates.

- Investment momentum remains the cycle’s backbone, led by AI infrastructure, aerospace, energy and industrial buildouts.

- Early holiday shopping began with heavy foot traffic but lighter spending per person, suggesting a mixed and highly value-conscious start to the season.

- ADP’s latest high-frequency data show a four-week average loss of private-sector jobs, raising concerns about a faster cooling labor market.

- Russia–Ukraine enters a dangerous winter phase with diminishing diplomatic traction, raising spillovers for Europe, energy and the U.S.–China strategic calculus.

- A new international investment initiative signals a pivot toward “diplomatic deal-making,” turning global capital flows into geopolitical tools.

- Markets remain hypersensitive to incremental data as traders balance falling inflation against uncertainty about how quickly the Fed can ease.

A Market Searching for Confirmation

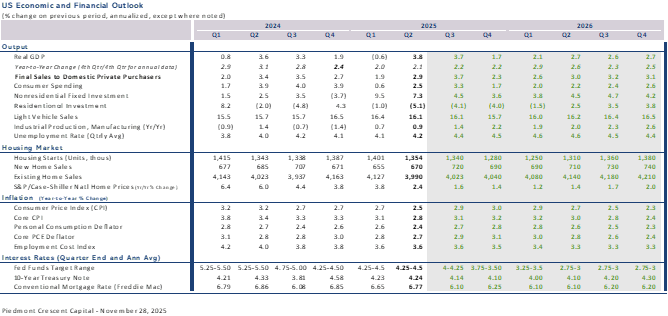

Financial markets spent the week parsing signals in an environment where the broad story is already understood. Inflation is cooling. The labor market is losing momentum. The Fed is preparing to cut, while remaining cautious about moving too quickly or signaling that it is adopting a more aggressive path. Treasury yields drifted lower following a steady run of dovish remarks from Fed officials. Equities maintained a measured upward bias.

Investors seek confirmation rather than direction. Data continue arriving in fragments—cooler in some places, firmer in others—yielding a narrative that is neither recessionary nor exuberant, but transitional to a lower trajectory. The economy continues to be driven by capital spending, innovation and productivity while households and employers step back from the confidence they carried earlier in the year.

A market in transition: cooling inflation, cooling labor, and investors waiting for proof.

Private data broadly reinforce this more cautious backdrop, with hiring and consumer sentiment slipping further. Anecdotal evidence from the Beige Book and from retail earnings calls echoes the same themes: caution at the register, a sharper tilt toward value, and a resilient core that is carrying more of the load.

The Beige Book’s Quiet Signal: Softer Labor, Cautious Consumers, Capital Still in Command

The Fed’s latest Beige Book strengthened the case for lower rates by underscoring a cooling labor market and a more guarded consumer. Districts reported slower hiring plans, easing wage pressures, and early indications that workers feel less invulnerable than they did in the spring. Retailers and manufacturers noted lighter traffic, thinner order books, and a noticeably defensive posture heading into year-end.

The Beige Book shows a labor market that is cooling, not cracking.

The path forward is not as simple as the data suggests. While the case for easing is convincing, lower rates would almost certainly invigorate financial markets and intensify capital spending—risking a renewed bout of asset inflation at a moment when the Fed is trying to guide the economy toward a softer glide path rather than an upswing in speculative momentum.

Capital investment remains the economy’s stabilizing force. Long-cycle projects—most notably AI infrastructure, energy systems, aerospace, and industrial equipment—continue to provide ballast as other sectors cool. A shift to lower financing costs would likely accelerate this capital-intensive expansion, though potentially at labor’s expense.

A Kansas City contact remarked that it is “a great time to get a tattoo,” because top artists once booked months ahead suddenly have availability. Workers likely feel a little more self-conscious and less secure about the job market. That is certainly what the data show. Consumer confidence is breaking lower and consumers are becoming increasingly selective.

A Mixed Start to the Holiday Shopping Season

Early retailer feedback and high-frequency trackers suggest the holiday season got off to a strong start on Friday and Saturday. Retailers described crowded stores and active browsing, but conversions were uneven and heavily reliant on promotions. While sales came in at the high end of expectations, shoppers leaned into discounts, prioritized essentials and shied away from expensive discretionary purchases.

This year’s holiday shopping season is defined by large crowds and a discerning consumer.

The tone is value-oriented and price-sensitive. Yet retailers are said to be going into the relatively short traditional holiday shopping season with fewer promotions. This unusual discipline will likely prove short-live and we look for promotions to increase, which will boost volume but compress margins.

The shift mirrors the Beige Book message: the consumer is still engaged but increasingly cautious. The economy is no longer consumer-led; momentum has shifted toward investment and productivity.

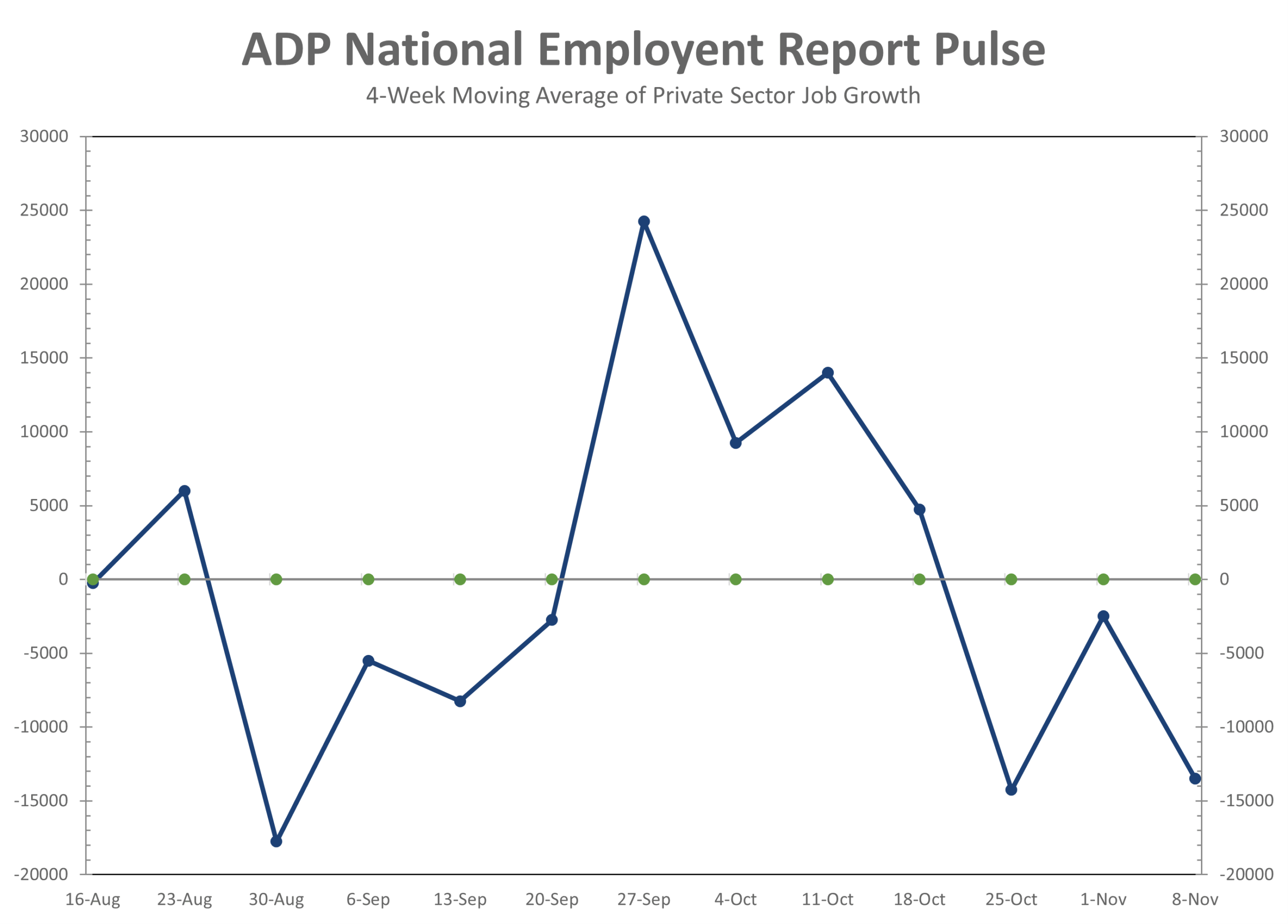

ADP Labor Data: A Clear Warning Signal

ADP’s latest NER Pulse report shows that private-sector employers shed an average of 13,500 jobs per week over the four weeks ending November 8. This four-week moving average is the weakest stretch in many months and suggests that labor-market softening is accelerating beneath the surface.

The contraction was broad-based across goods and services. The decline carries heightened significance given the Fed’s comfort with the ADP series and the lack of fresh BLS data ahead of the December meeting. For investors and policymakers, this is the clearest early-warning signal yet that labor-market cooling may be further along than widely acknowledged.

The government shutdown exerted a larger than expected drag on the economy.

Government Shutdown Ended Just in Time

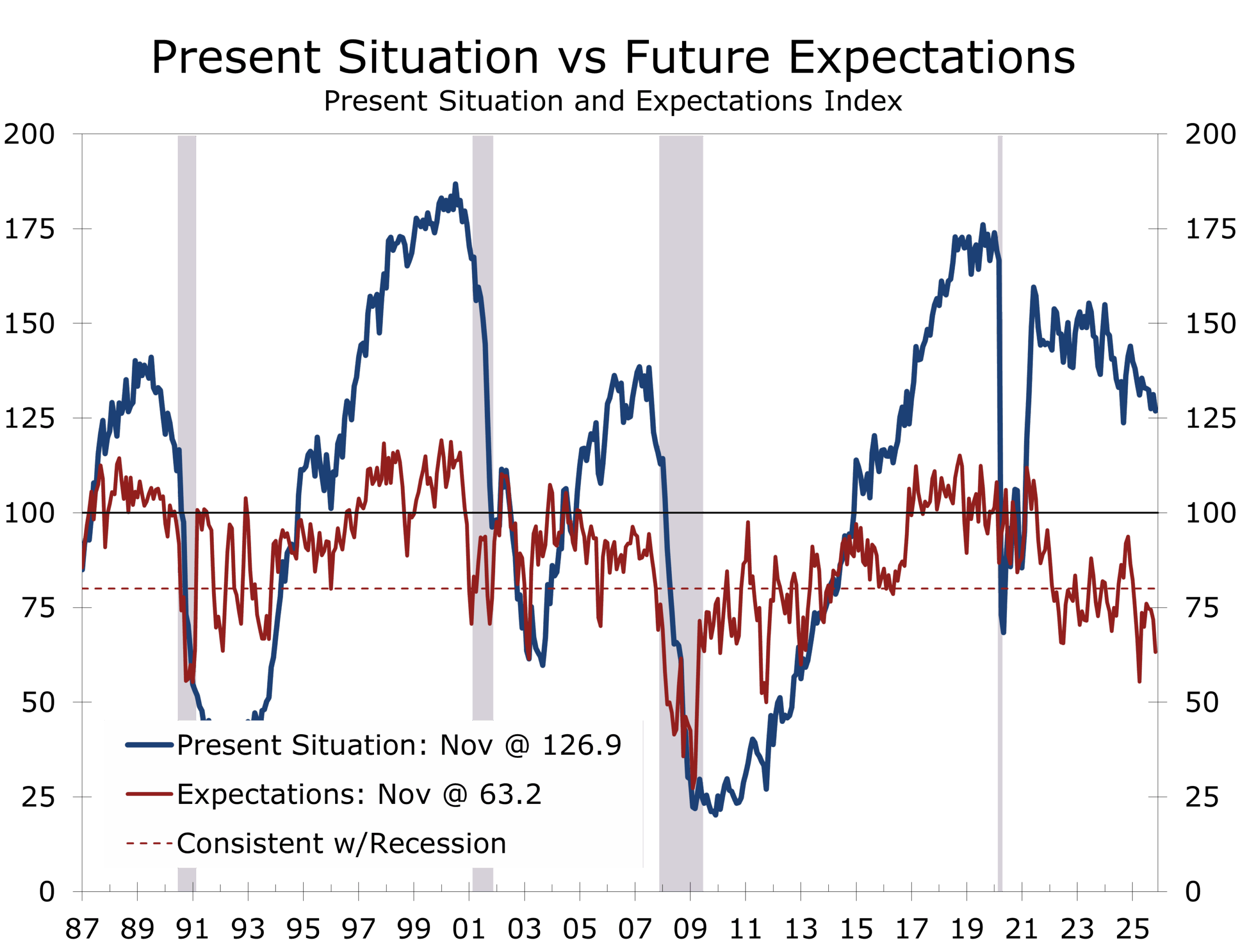

Consumer confidence fell to 88.7, its weakest reading since April. The 43-day federal shutdown, increased layoff announcements, equity volatility, and persistent concerns over inflation dominated write-in responses. The Expectations Index fell to 63.2, its tenth straight month below the recession-signaling threshold of 80.

Sentiment deteriorated across all major demographic and political groups. Big-ticket buying plans slipped, and service-spending intentions weakened. Spending grew solidly in Q3 but now looks more guarded.

Spending ended Q3 on a weak note, with retail sales rising just 0.2% in September—essentially flat in real terms. Goods categories weakened broadly (electronics, nonstore retail, sporting goods, apparel), while spending in food services (restaurants and bars) rose 0.7%, personal care (+1.1%) and miscellaneous retailers (+2.9%) provided stability.

Control-group sales fell 0.1%, reflecting shifting consumer preferences. The “K-shaped” profile persists. Higher-income households continue to spend mostly on services and experiences, while middle- and lower-income households increasingly ration discretionary purchases. This split extends to restaurant dining as well, with fast food and limited service chains seeing slower sales and diminished pricing power, but sales and prices both rising at full service restaurants, particularly at the upper end.

Housing affordability remains stretched, which is keeping a low ceiling on home sales.

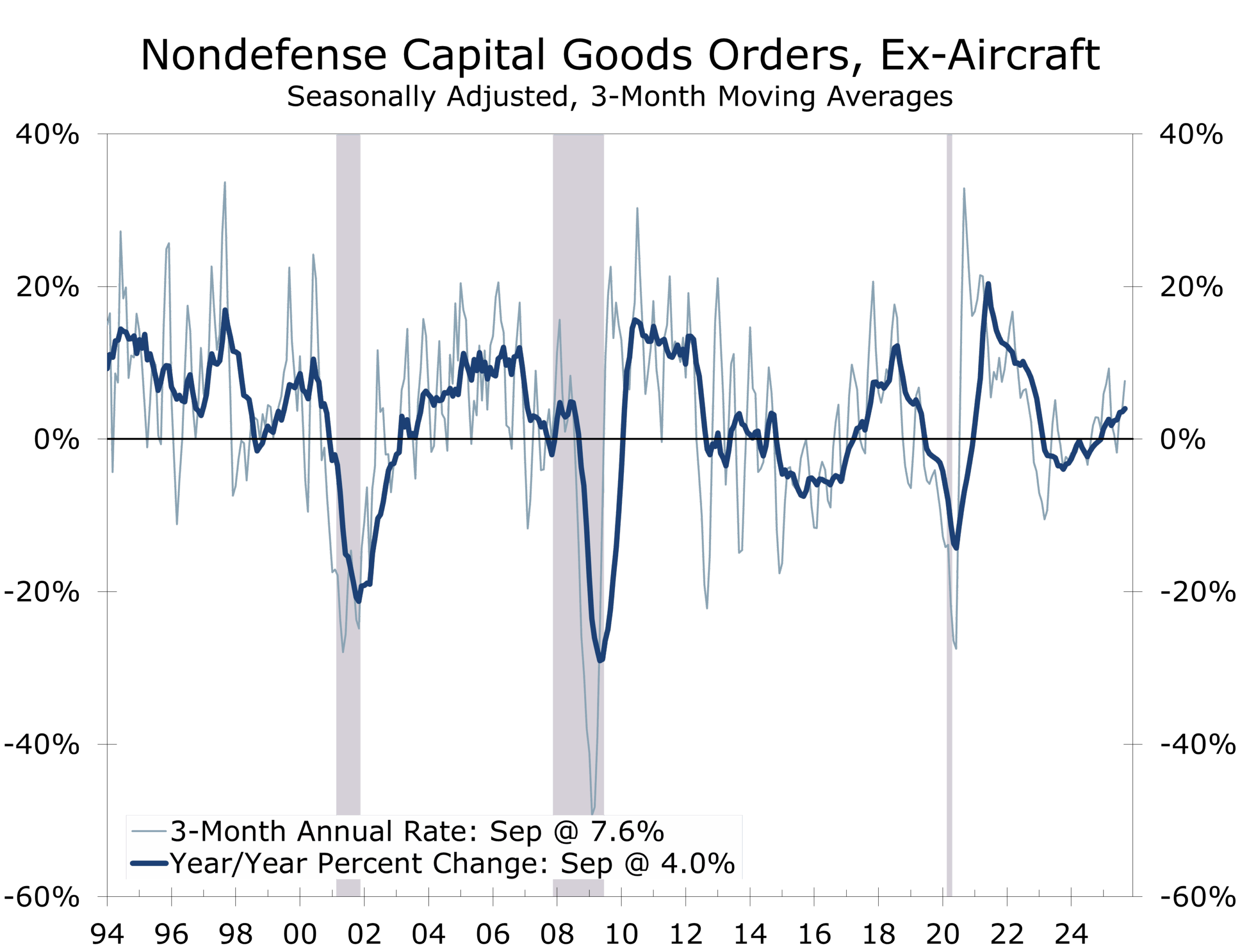

AI-Led Capex Continues, but Shipments Slow

Durable goods orders rose 0.5%, supported by a second consecutive 0.9% increase in core orders. Strength remains concentrated in AI-adjacent categories such as information-processing and electrical equipment. But shipments slowed sharply, pushing Q3 equipment investment growth down to 3.1% from 8.5% in Q2. The slowdown caused many forecasters to trim their Q3 GDP estimates.

Corporations continue to benefit from wide margins and low credit spreads. Now, with interest rates falling and expected to remain lower in 2026, we expect the recent strength to broaden beyond AI. Productivity enhancing investment is likely to be pursued by producers of consumer goods, with reshoring efforts becoming more apparent.

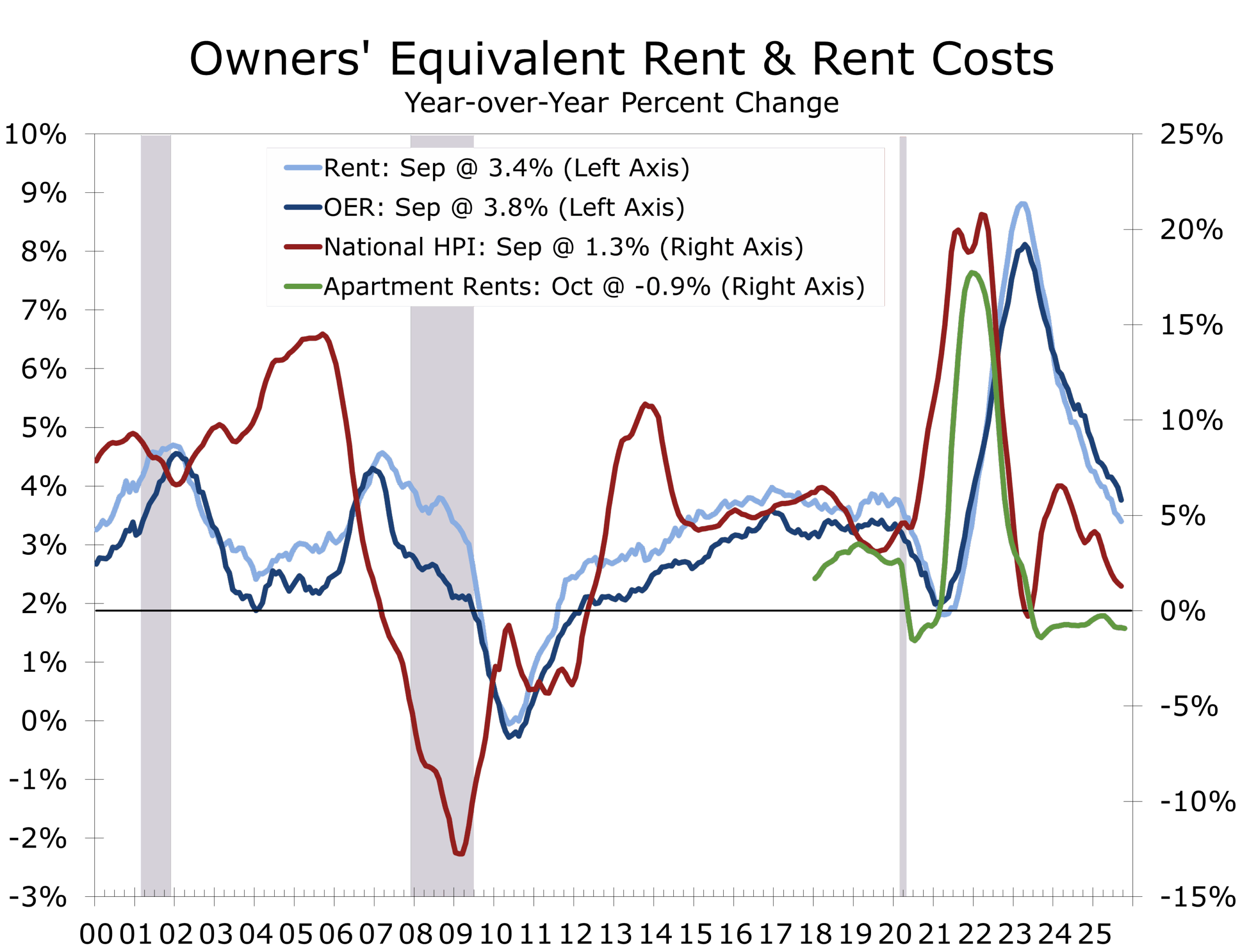

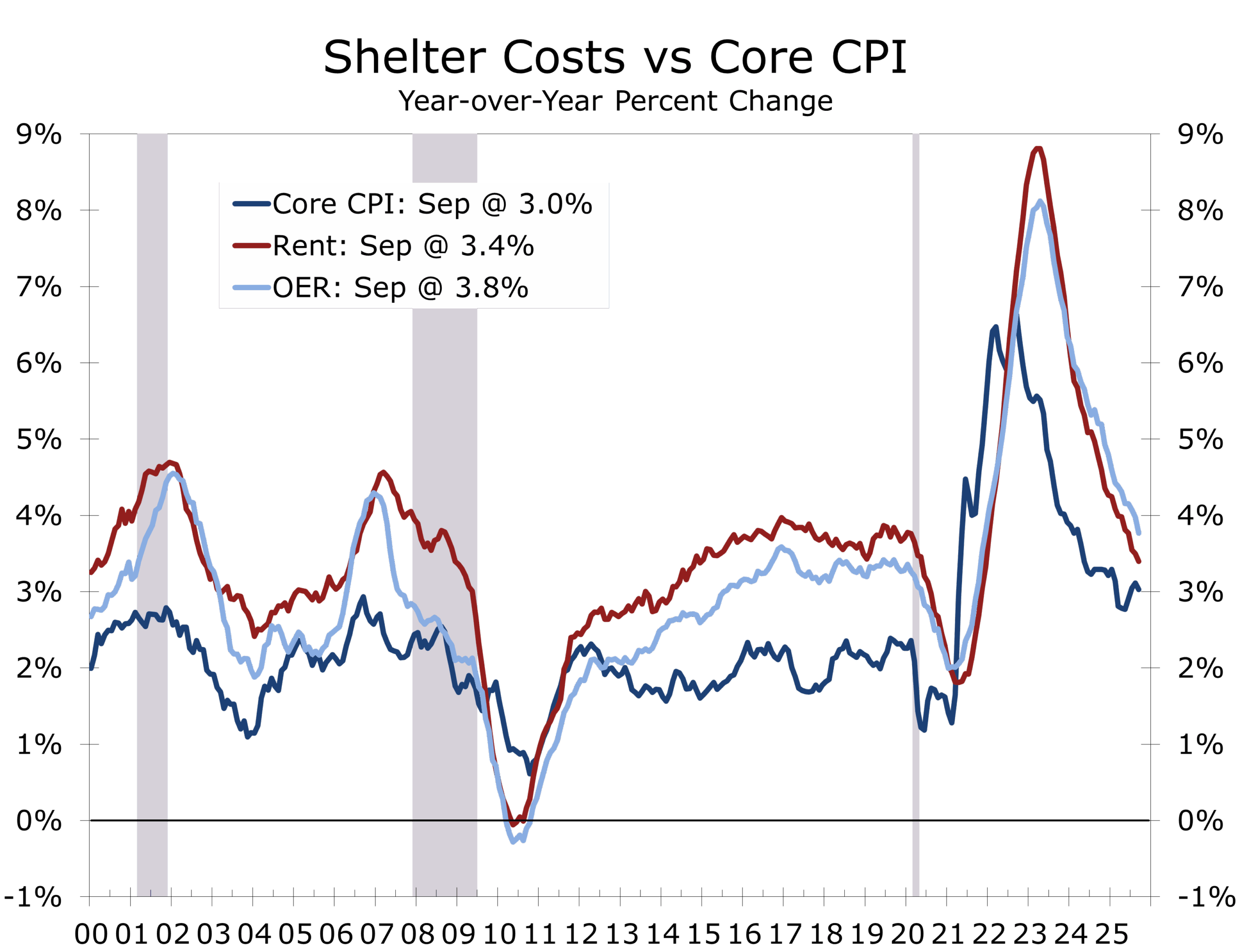

Home Prices: Broad Cooling and Shelter Disinflation

National home prices rose just 1.3% over the past year and fell 0.3% month over month in September. All 20 major metros posted monthly price declines (NSA), with Tampa (-4.1% y/y), Phoenix, Dallas and Miami leading the downturn.

Residential rents tend to follow home prices, which means core inflation is headed lower.

Home price growth is expected to fall below 1% before rebounding in mid-2026 as rates decline. The cooling points to shelter inflation decelerating toward 3% by year-end 2026, a key disinflationary tailwind for the coming year. Shelter accounts for just over 44% of the core CPI, so that deceleration should become readily apparent and help bring headline and core inflation back in line with the Fed’s long-run goal.

PPI: Energy-Driven Rebound, Core Remains Mild

Producer prices rose 0.3% in September as a rebound in wholesale gasoline prices and higher beef prices lifted the headline. Final demand goods advanced 0.9%, the largest gain since February. About 60% of the increase came from gasoline, which surged 11.8%. Energy overall rose 3.5%, food increased 1.1%, and goods excluding food and energy edged up 0.2%. Beef and meats strengthened, along with residential electric power and motor vehicles, while fresh vegetables and nonferrous ores declined.

Final demand services were flat, as a 0.2% drop in retailer and wholesaler margins offset firmer readings in transportation and warehousing (+0.8%) and a modest uptick in services less trade and transportation. Airline fares jumped 4.0%, while margins for machinery and equipment wholesaling fell 3.5%, and portfolio management fees declined 1.2%.

Taken together with the earlier reported CPI, the data imply inflation remain relatively contained in September. The overall PCE deflator likely rose 0.3%, while the core likely rose 0.2%

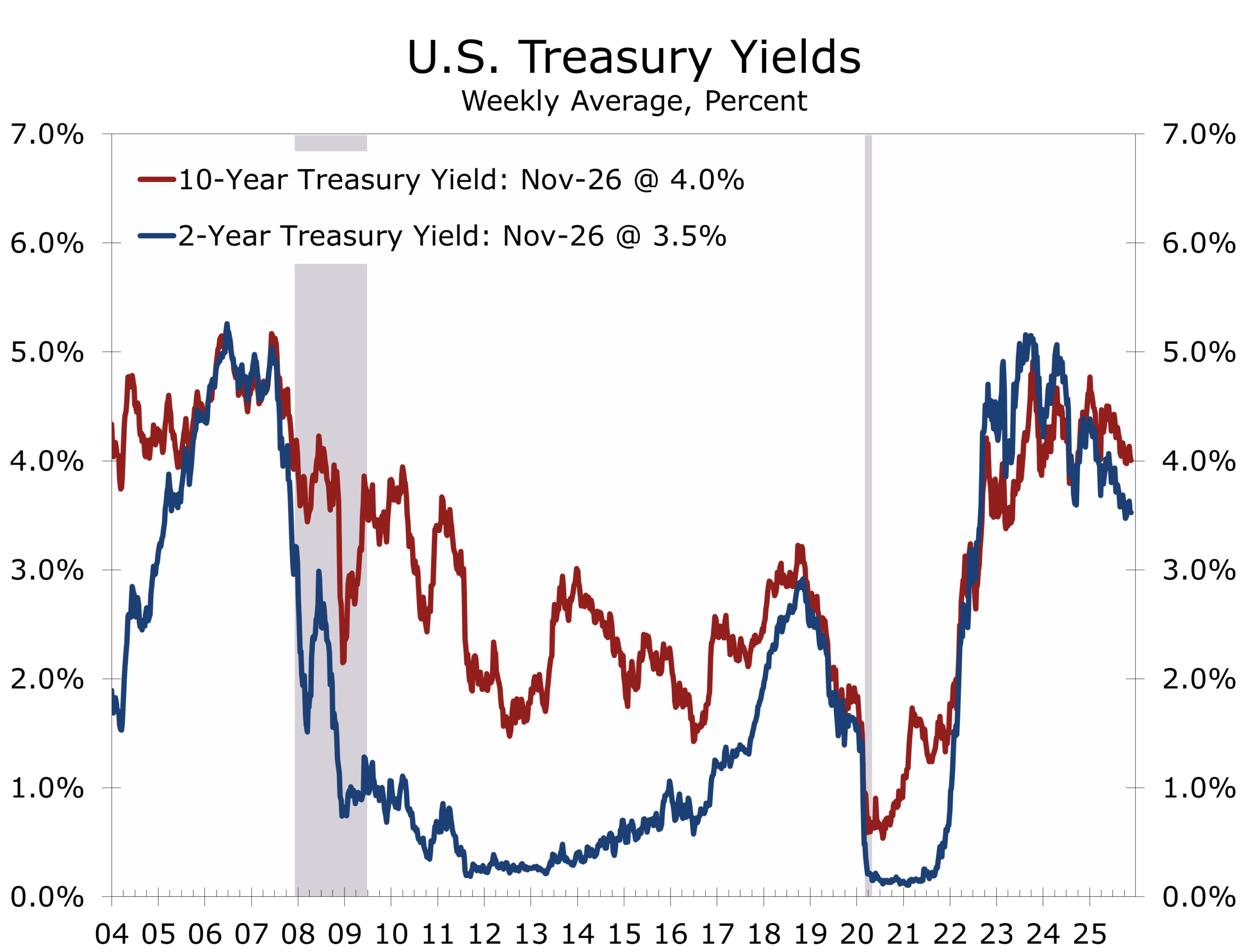

Fixed Income: Lower Yields, Higher Cut Odds

Treasury yields ended the week 7–9 basis points lower as markets priced in a higher probability of a December rate cut following dovish signals from New York Fed President Williams. Mortgage-backed securities widened on expectations of increased volatility, and primary dealer Treasury holdings climbed to a record $604 billion, highlighting strong demand for duration in a thin-data environment. For funding managers, the message is clear: fixed-income markets remain range-bound heading into the FOMC meeting and a compressed holiday issuance calendar, but positioning is shifting toward rate-cut readiness. Funding conditions are stable, liquidity remains ample, and the window for opportunistic terming-out of debt is still open, although it may narrow quickly once the Fed’s path becomes clearer.

A Winter of Attrition and Narrowing Diplomacy

This winter is shaping up to be one of higher military tempo and shrinking diplomatic opportunity. Ukraine continues to ration artillery and drones, leaning on asymmetric strikes and localized counter-offensives, while Russia presses along multiple fronts and employs increasingly sophisticated Iranian-style drone swarms. President Trump had repeated stated his desire for a peace deal by Thanksgiving and is now probably striving for Christmas or yearend. A poorly structured settlement, however, would risk setting a precedent that could haunt Europe, the United States, and Asia for years to come.

America’s geopolitical bandwidth is fully subscribed, as risks are increasingly intertwined.

Europe’s energy position is stronger than it was in 2022, but its political cushion is notably weaker. Fiscal strains, demographic pressures, and rising populism are chipping away at cohesion. For the United States, the stakes run through two major channels. First, China’s Taiwan calculus: Beijing is studying Ukraine closely as a sandbox for sanctions resistance, supply-chain rerouting, and attrition warfare. Japan is watching with equal urgency. Second, Middle East stability: regional tensions from Syria to the Gulf continue to simmer, with Israel repeatedly disrupting rearmament efforts by Hezbollah and Hamas.

Piedmont Perspective

“Societies fray gradually, not suddenly.” — Tolstoy

The tragic shooting of two National Guard troops in Washington this week is a reminder of how thin the seams of American public life have become. These were young Americans serving in the capital, far from any battlefield, yet caught in the undertow of a society that feels more strained and brittle than it did only a few years ago.

Tolstoy’s A Confession offers an unsettling parallel. Writing in 1882, he warned of a “corrosion of spirit,” a gradual loss of meaning and connection that takes hold as trust erodes. Societies rarely break in a single dramatic moment. They often come apart slowly, thread by thread, as small tears go unattended and the bonds that once held communities together weaken through neglect, fatigue, or indifference.

The erosion of societal norms rarely announces itself. It begins subtly through frayed trust, rising cynicism, and quiet withdrawals from community long before it becomes visible in headlines or data.

The pressures visible today follow that pattern. Economic strains linger even as the broader economy shows resilience. Institutional missteps and political volatility have fed a deeper sense of skepticism. Inequality continues to shape how people experience opportunity and stability. On top of this sits an information environment built for speed and outrage. Social media, partisan echo chambers, and parts of the press often reward provocation over clarity. This dynamic does not cause violence by itself, but it increases isolation, weakens judgment, and makes the cracks in society more difficult to repair.

None of this reduces individual responsibility or simplifies the complexity of a single act. It does, however, form the context in which too many people now struggle with belonging, purpose, and confidence in their institutions. The sense of drift is widespread across demographic, regional, and political lines.

Tolstoy did not write to encourage despair. His goal was to highlight the need for repair and renewal. Resilience comes from the basic ties that make a society work: trust built in small interactions, communities that extend beyond politics, institutions that act transparently and with restraint, and citizens who view themselves as stewards of the wider republic rather than spectators to it.

Resilience is rebuilt the same way it frays: gradually. Small acts of trust, service, and accountability reverse the drift.

A quieter point sits underneath all of this, and it carries economic relevance. Markets may focus on inflation prints, labor data, and the next move from the Federal Reserve, but confidence does not exist in a vacuum. A society that feels strained or disconnected becomes more sensitive to shocks and more reactive to uncertainty. The same “erosion of norms” that weakens civic life also shows up in survey data, consumer behavior, and risk appetite. This past week’s declines in confidence and more selective holiday spending fit that pattern.

As we sift through the latest economic signals, it is worth remembering that the country’s real strength has never been measured only in GDP releases, employment reports or by the shape of the yield-curve. It comes from the people who show up each day. It comes from workers and soldiers, first responders and teachers, public servants and small-business owners, as well as families and communities that create the quiet foundation of civic life.

We honor the two Guardsmen, one who lost her life and one who continues to fight for his, by remembering that our institutions endure because free citizens build them, protect them, and hold them accountable. That commitment to a free society remains the quiet engine of American resilience. It is not the businesses or institutions themselves that define our strength, but rather our capacity to create, renew, and reinvent them. At a time when the headlines lean toward division, it is this shared responsibility that gives the country its greatest advantage and helps steady the broader economy when uncertainty rises.

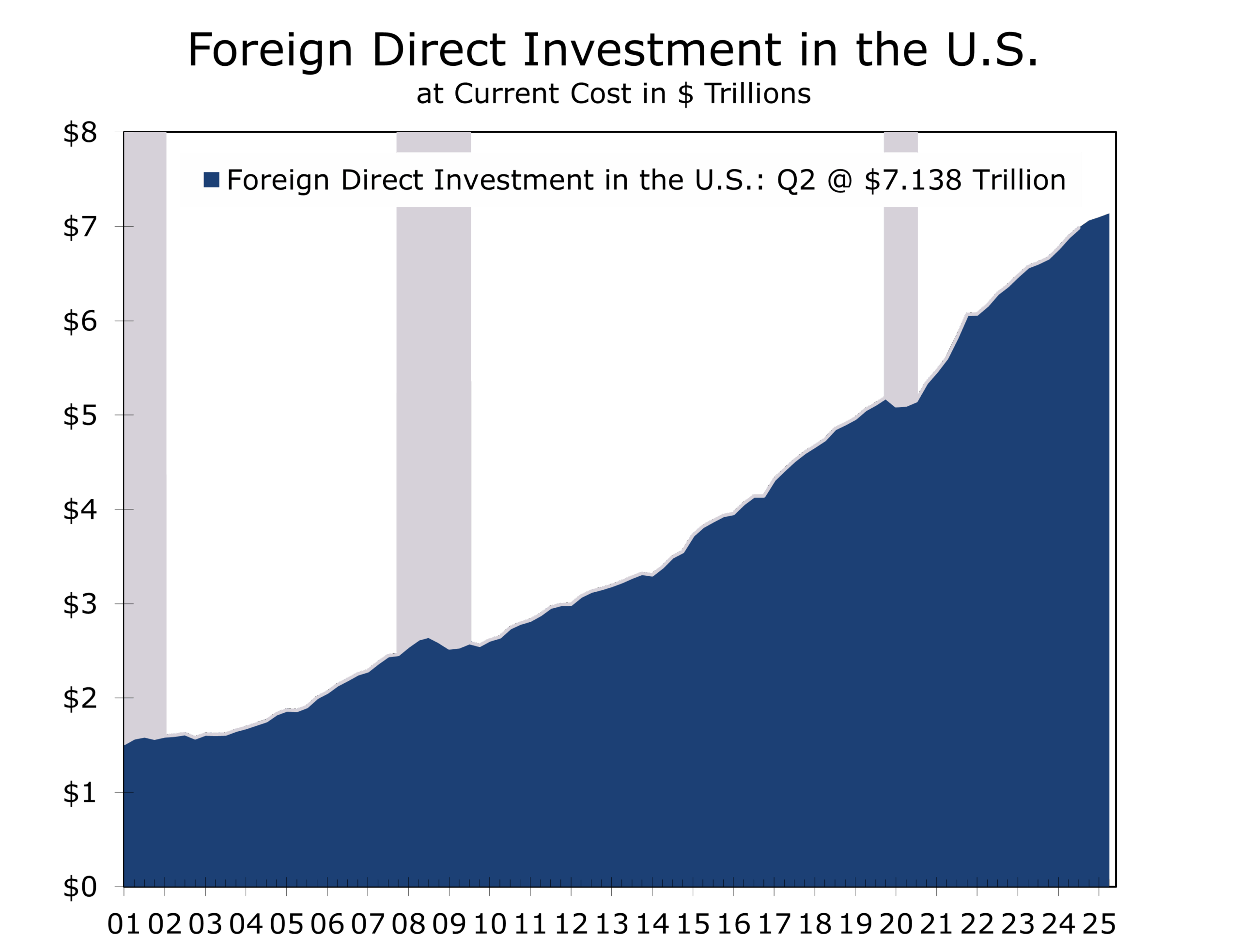

Foreign Direct Investment: Capital as Diplomacy

The Trump administration’s new international investment framework signals a pivot from tariff-centric confrontation toward a more deal-driven form of economic statecraft. The emerging strategy treats access to U.S. capital, corporate partnerships, and investment guarantees as tools of geopolitical influence—leveraging balance sheets where sanctions and tariffs have begun to hit diminishing return.

Recent Bloomberg analysis notes that while headline pledges of a $20-trillion investment boom are materially overstated, identifiable commitments still run into the multi-trillion range and concentrate heavily in advanced technologies, energy systems, and strategic manufacturing. Bloomberg’s more conservative analysis puts the total at closer to $7 trillion, which is still a hefty sum.

A multi-trillion dollar investment push creates upside risk for U.S. capex and long-run growth.

A sustained wave of cross-border projects—even at the lower, independently verified scale—would carry real macroeconomic weight. In a world reshaped by reshoring, friend-shoring, and supply-chain redundancy, expanded U.S. investment from abroad would reinforce the capital-led expansion already underway. Sectors such as AI infrastructure, semiconductors, energy platforms, defense technology, and advanced logistics anchor the current cycle; additional international activity would deepen order books for U.S. suppliers and add upside risk to near-term capex and GDP.

Context matters. The entire stock of foreign direct investment already in the United States stands at roughly $7.1 trillion, at current costs, while U.S. direct investment abroad totals about $6.8 trillion. Even a modest, sustained increase in direct investment flows, well below Trump’s touted figures, would still be large relative to the existing base and could meaningfully support long-run potential GDP. If the Bloomberg analysis is accurate, then $7 trillion in additional foreign direct investment would roughly double the stock of facilities currently in place. To borrow a phrase from president Trump, that would be ‘huge’. The initiative’s emphasis on advanced manufacturing, data-driven systems, and modern energy would also reinforce productivity, raise global demand for U.S. goods and services, and extend the reindustrialization impulse that has defined this cycle.

There are trade-offs. Politically influenced investment flows tend to be lumpy, with project timing and approval tied to negotiations rather than purely economic returns. That increases volatility and makes the growth path more corridor-shaped than smooth. But the broader takeaway is clear: cross-border capital is becoming a strategic asset. Its deployment will be more dynamic and less predictable—but also rich with opportunity for the sectors aligned with the administration’s priorities.

Drifting Toward Easing, Still Waiting for Data

Equities closed the week with a modest gain, helped by a modest decline in Treasury yields and slightly tighter credit spreads. The S&P 500 and Dow ended the month in positive territory, while the Nasdaq slipped fractionally. With no employment report ahead of the FOMC meeting, markets are trading on inference rather than evidence, waiting for data that either validates the soft-landing narrative or complicates it.

With Santa leading the rally, the markets are waiting for confirmation, not direction.

The Fed’s runway for easing remains visible but narrow. A December cut now appears highly likely, yet visibility beyond that is hazy at best. We anticipate clarity on Powell’s successor by yearend, with Kevin Hassett emerging as the leading candidate. Powell, for his part, seems intent on leaving room for his successor to navigate what may become a more complicated early-2025 policy landscape.

The Week Ahead: December 1-5

We continue to wait for federal agencies to catch up with the economic data. Private data continue to offer the best intel of current economic conditions.

Monday, December 1

Look for credit card data and other private high frequency data for an assessment on Black Friday and opening weekend holiday retail sales.

We will also get a couple of readings on the manufacturing sector, with S&P final PMI at 9:45 and ISM Manufacturing Index at 10:00 am. The ISM Manufacturing Index has been stuck at just under 50 but well north of the 43.7 level that is typically consistent with recession. The more leading indicators have recently been hinting at some reacceleration, but it is likely too soon to see that in this report.

Jerome Powell will provide remarks before joining a panel on George P. Shultz and his economic policy contributions at the Hoover Institution at 8:00 pm.

Tuesday, December 2

Michelle Bowman, as Fed Vice Chair for Supervision, is scheduled to testify before the U.S. House Committee on Financial Services.

We will also get data on U.S. light vehicle sales and reports on sales for Cyber Monday.

Wednesday, December 3

We will get the latest update on ADP employment for November. The October report posted an increase of 42,000 private-sector jobs. We are also scheduled to receive reports on import prices, as well as the final S&P Services PMI and the ISM Services Index. The latter will be closely scrutinized for updates on employment and prices.

Thursday, November 26

We will receive weekly first-time unemployment claims and are also scheduled to receive October merchandise trade data.

Friday, November 27

We will close the week with a look at September personal income and spending, as well as inflation data. Personal income is expected to rise 0.4%, while consumer spending should rise 0.2%, or essentially flat after inflation. Services outlays are a bit of wildcard.

We will also get preliminary University of Michigan Consumer Sentiment and Consumer Credit use data for the month of October late Friday afternoon.

An Economy Tilting Toward Capital and Resilience

A consistent pattern emerges across the Beige Book, durable-goods orders, home prices, labor data and capital spending: the U.S. economy is gradually shifting toward a capital-led, innovation-driven expansion. AI infrastructure, industrial construction, aerospace, energy systems, logistics and defense technology are becoming the structural supports of the cycle.

The investment boom is being supported by wide corporate margins, strong order books, reshoring initiatives and a growing pipeline of public and private projects. This shift toward capital deepening and productivity-enhancing investment gives the economy a sturdier foundation than headlines often suggest.

The outlook is not without risk, but also not without promise. Consumers remain under pressure. Labor markets are cooling. The inflation fever has broken but has not fully subsided. Even so, an investment-centric expansion can support stronger long-run growth, greater supply-chain resilience and a healthier balance between consumption and production.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

November 30, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000