Highlights of the Week

- Markets are responding less to the Fed’s rate cut and more to its liquidity posture, reinforcing that balance-sheet mechanics now matter as much as policy rates.

- The re-steepening yield curve, led by renewed pressure at the long end, reflects fiscal realities, rising investment demand, and limits on monetary control over long-term capital.

- Transportation stocks are sending a constructive signal that the goods economy is stabilizing beneath headline volatility.

- The labor market is loosening gradually, with cooling wage pressure and declining quits pointing to slower momentum, not collapse.

- AI-driven investment continues to support growth but is becoming increasingly intertwined with credit markets and balance-sheet risk.

- Geopolitical tensions and rising social stress are no longer exogenous risks; they are shaping confidence, behavior, and the macro backdrop.

- The expansion remains intact, but it is increasingly conditional—dependent on careful liquidity management, fiscal credibility, disciplined capital allocation, and the preservation of social and institutional stability. The economy is still moving forward, but the margin for error continues to narrow.

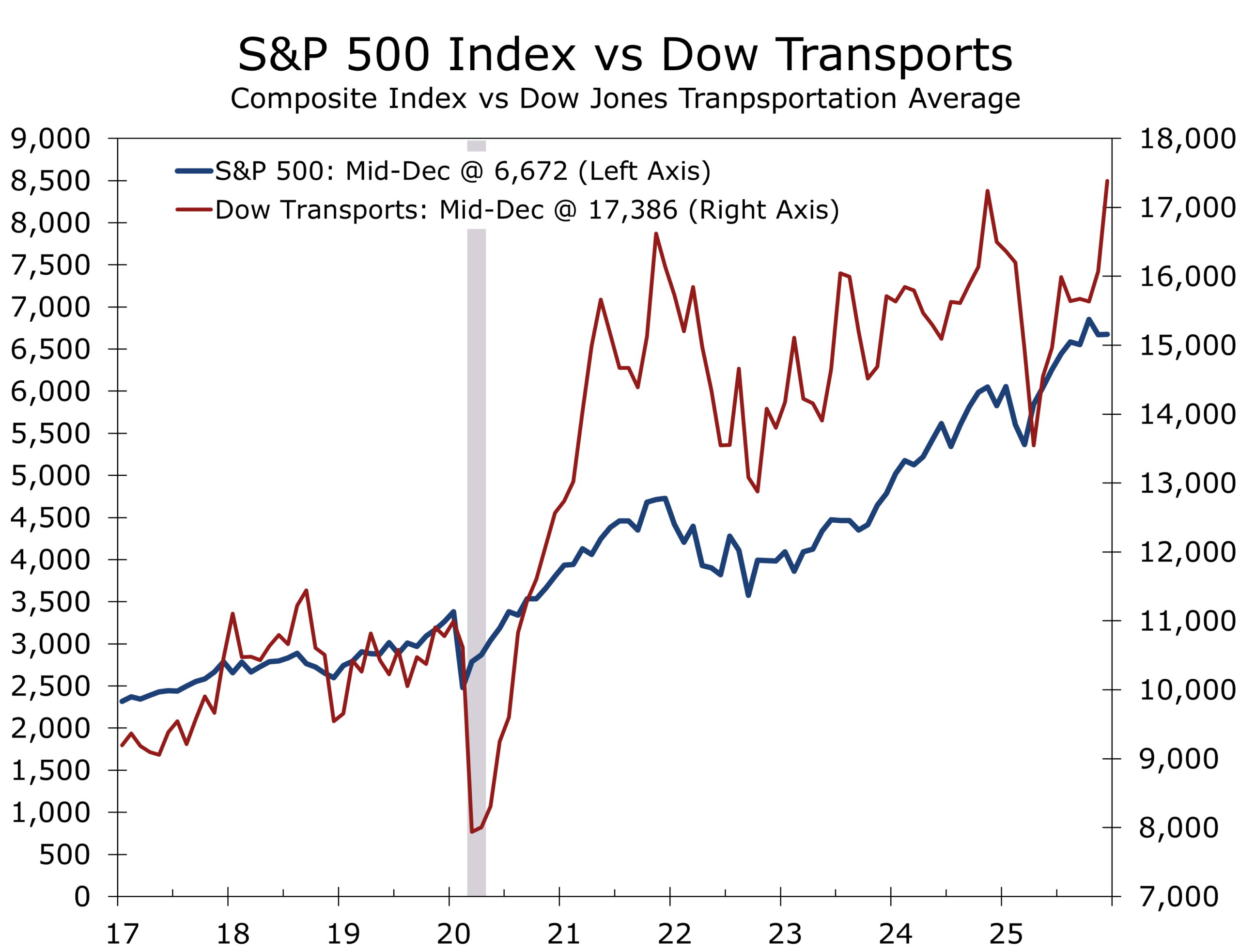

When the Transports Speak, It’s Worth Listening

While markets remain fixated on AI-heavy mega caps, one of the more constructive signals over the past week has come from a far more traditional corner of the tape: the transports.

Transportation stocks—railroads, trucking firms, and logistics providers—have outperformed the broader market. That matters because transports sit closest to real economic activity. They move raw materials, intermediate goods, and finished products. When they strengthen, it often reflects improving expectations for physical demand rather than multiple expansion or liquidity effects.

When transports lead, it’s usually the real economy—not sentiment—that’s turning.

Historically, transports tend to lead at inflection points. Their recent outperformance suggests the goods-producing side of the economy is finding its footing—possibly marking the end of the long-running freight recession. Inventories remain lean, freight volumes have stabilized, and consumer demand—while cooling—is not collapsing.

This is not a signal of reacceleration, nor a late-cycle blowoff. It fits a more nuanced macro narrative: a soft patch, not a hard stop. In a market dominated by intangibles and AI narratives, the steady bid under companies that move goods from Point A to Point B is a reminder that the real economy still anchors the cycle. Demand should firm more visibly this spring and summer as housing and other rate-sensitive sectors respond to lower borrowing costs.

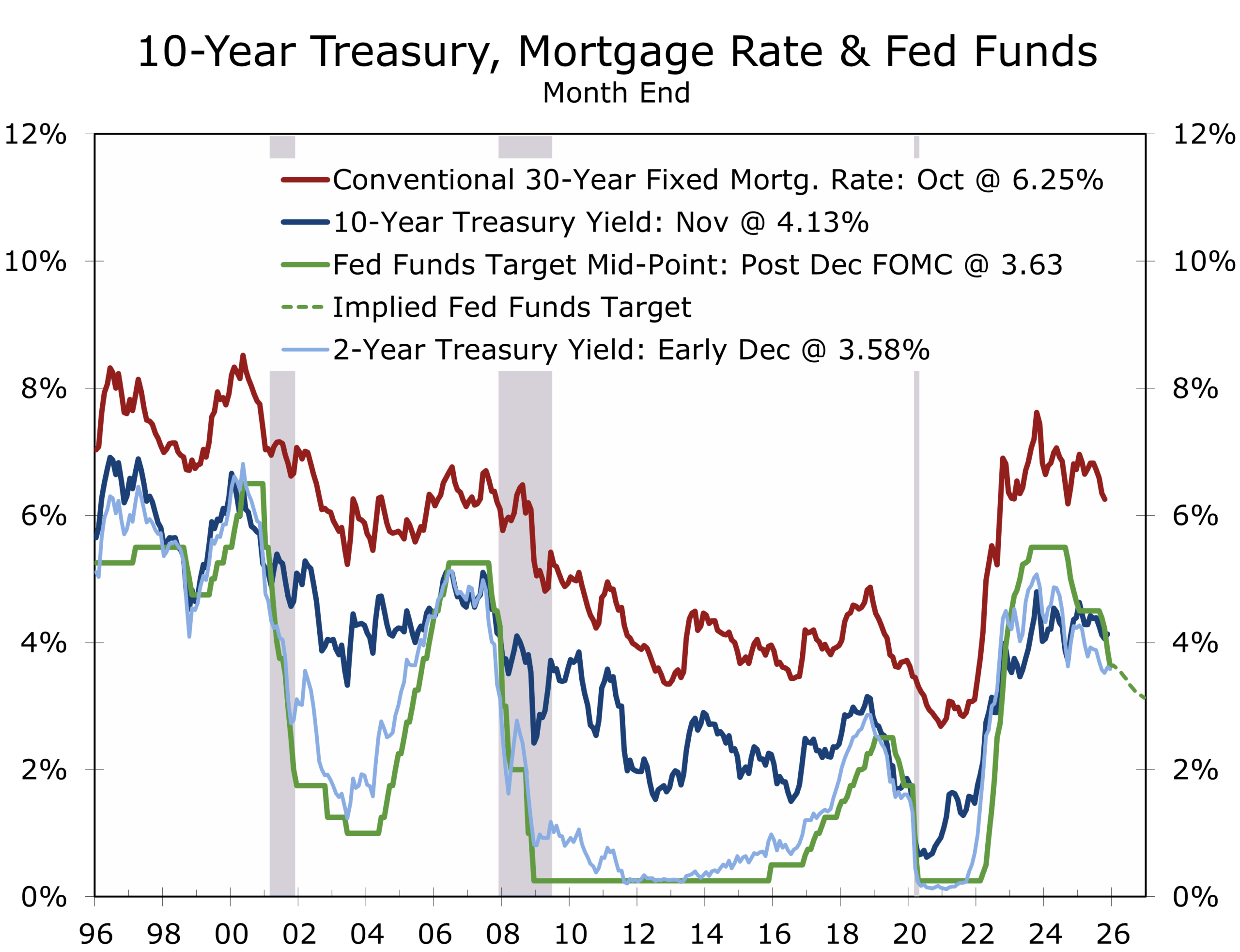

Rates, Fiscal Dominance, and Key Signals

The most revealing story in rates has not been the Fed’s decision to cut, but how markets reacted to how the Fed chose to ease. By moving cautiously, the Fed has preserved a progressively less tight—but still restrictive—policy stance. That approach has cooled inflation pressures without reigniting speculative excess. In that sense, policy has largely done its job.

The rate cut mattered less than how the Fed chose to ease.

The December move marked a subtle inflection.

By meeting day, the cut itself was expected. What mattered was pairing that cut with more aggressive-than-expected near-term Treasury-bill purchases. The modest balance sheet expansion was dubbed QE light by critics and described as reserve management by the Fed. The move was meaningful, which we interpret as an effort to avoid accidentally tipping the economy into recession with a temporary liquidity scare, is meaningful at the margin. Lower policy rates combined with balance-sheet expansion shifted market tone quickly and buoyed risk assets.

The yield curve responded accordingly. Short rates declined further, but long rates rose. The result was a steeper curve with a more uncomfortable message. The 10-Year Treasury had popped up to 4.20% earlier this month and then fell back under 4.10% and is not back up to around 4.18%.

The 30-year Treasury sent a clearer signal, with yields rising sharply in the days following the Fed’s announcement. The long bond is not trading CPI prints or FOMC rhetoric. It is trading duration risk, supply pressure, and long-run policy credibility.

Higher long rates reflect two beliefs gaining traction simultaneously: growth is likely to strengthen in 2026, and large fiscal deficits and heavy Treasury issuance are set to persist.

The bond market is drawing a distinction between the Fed’s influence over front-end financial conditions and its diminishing control over long-term borrowing costs.

This is fiscal dominance in practice—not a crisis of confidence, but a gradual shift in who sets the marginal price of long-term capital. The curve is not signaling recession, nor celebrating effortless growth. It is delivering a conditional verdict: the economy can move forward, but the cost of long-term capital is rising and the margin for policy error is thin.

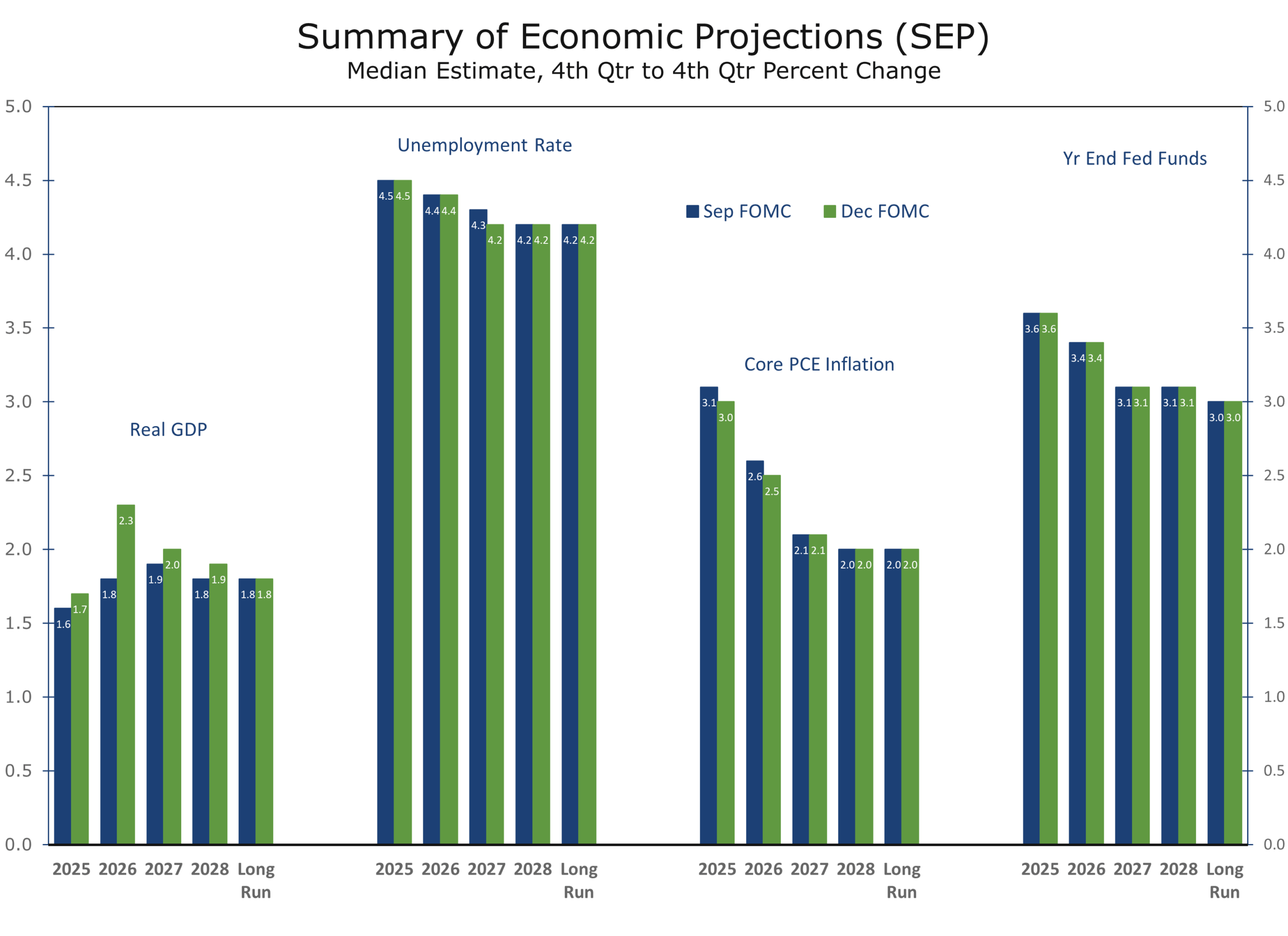

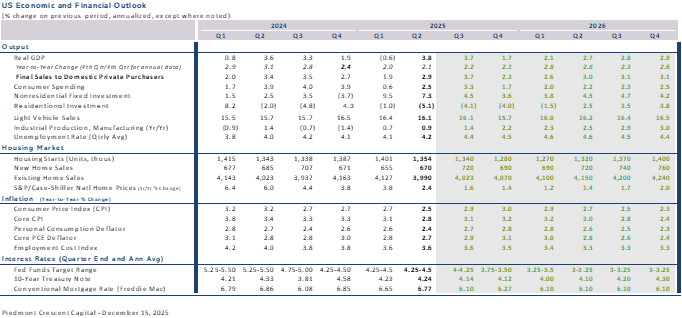

There is also a more fundamental driver behind higher long-term rates. The latest Summary of Economic Projections implies stronger private demand for funds in an increasingly investment-driven economy. The SEP lifted its 2026 GDP growth forecast by a half percentage point to 2.3% while maintaining expectations for decelerating inflation. Investment-led growth should boost productivity and ultimately lift the long-run neutral federal funds rate.

Recent Developments: Signals Beneath the Noise

Recent data reinforce a consistent theme: growth is slowing without stalling out. Small-business sentiment improved modestly. NFIB hiring intentions firmed, suggesting easing policy uncertainty and improved credit conditions may support incremental hiring in 2026. At the same time, inflation remains the top concern and pricing plans strengthened, suggesting that disinflation is uneven.

The labor market is loosening in an orderly way, shifting risk from inflation toward employment.

JOLTS added nuance. Job openings rose but layoffs edged higher. Quits are also off sharply. Job hopping is far less popular this past year and more workers are sending holiday cards to their supervisors this year.

Wage data sharpen that picture. The Q3 Employment Cost Index slowed to a pace consistent with the Fed’s inflation target once productivity is considered. Moreover, wages are rising faster for employees that remain in place than for job switchers. The bottom line is wage pressure is no longer the binding constraint for policymakers; the softening labor-market risk is.

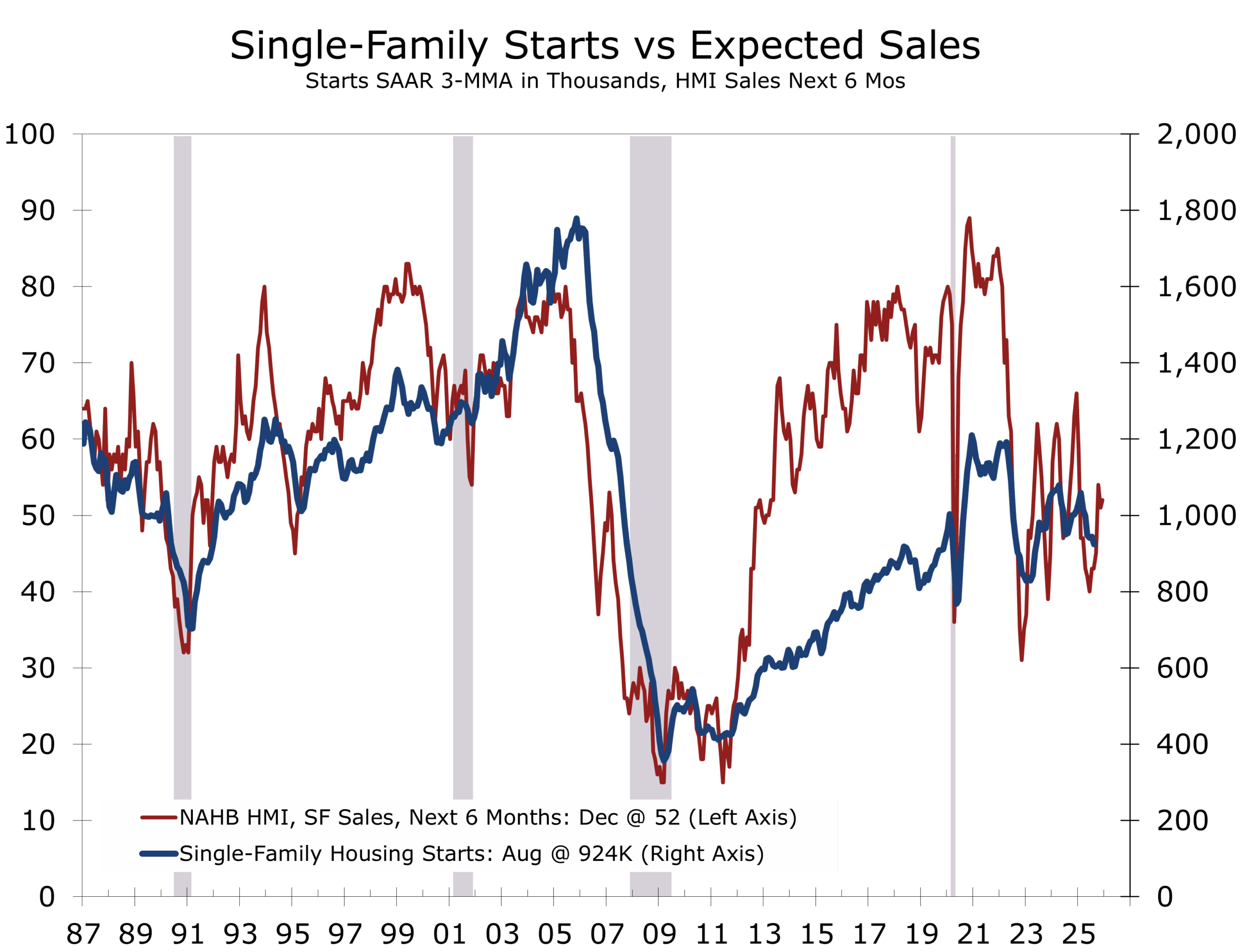

Housing remains soft but forward indicators are improving. Builders continue to rely on incentives to clear elevated inventories and expectations for sale six months ahead have strengthened—suggesting a stabilization in starts before a recovery.

A Dense Calendar at a Sensitive Moment

Monday’s releases set the tone

The Empire State Manufacturing Survey fell sharply into contraction. New orders and shipments weakened materially. Current price pressures eased, but expected prices received rose to their highest level since 2022. The six-month outlook improved notably. Current activity is soft; expectations remain resilient.

The NAHB Housing Market Index ticked higher. Current sales conditions remain subdued, but forward-looking components improved, reinforcing the view that housing is closer to a floor than a cliff.

Tuesday, December 16

The delayed October and November employment reports will be released together. Headline payroll growth should be modest, weighed down by federal displacement and early retirements. Private payrolls will offer a cleaner read on underlying momentum. The unemployment rate is expected to edge higher.

Thursday, December 18

Retail sales, flash PMIs, and CPI will round out the week, testing the Fed’s confidence that disinflation—particularly in shelter—continues into 2026. A heavy slate of Fed speakers will provide additional signal on how policymakers interpret a labor market that may already be near stall speed.

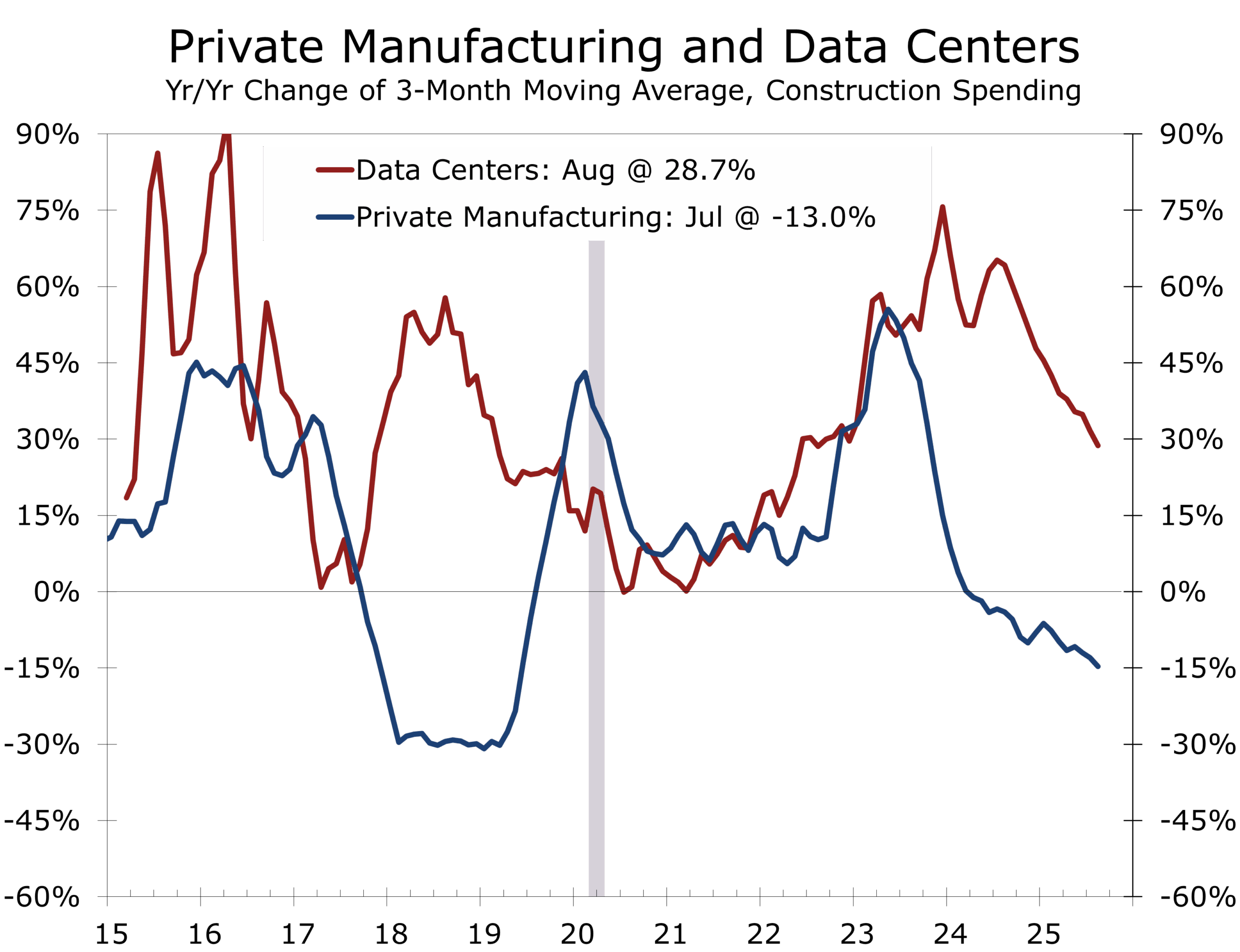

AI Investment: Growth Engine, Growing Side Effects

AI-related investment continues to do extraordinary work for the macro data. Data centers, semiconductors, power infrastructure, and AI-linked software now account for a disproportionate share of incremental business investment.

That concentration is precisely why scrutiny is rising.

AI investment is shifting from an equity narrative to a broader credit and liquidity story.

The concern is not AI’s transformative potential, but the circularity of the current build-out. Hyperscalers fund massive infrastructure projects, sell capacity across the ecosystem, capitalize internally developed software, and increasingly rely on debt structures predicated on sustained high utilization.

Investment shows up immediately in GDP. Productivity gains arrive later. Credit markets are taking note. AI has shifted from a pure equity story to a macro, credit, and liquidity story.

FOMC Statement & Powell Press Conference: We are looking for a hawkish quarter point cut, with three and possibly four dissents (one favoring a larger cut and two against any cut at all). Dissents mean less at this time, as a new Fed Chair will likely be announced ahead of the next FOMC meeting in January.

Geopolitics: Fragile Ceasefires, Shifting Lines

Geopolitical risk resurfaced over the weekend. Ceasefire frameworks in the Middle East were tested again, while developments in Ukraine suggest greater flexibility in pursuit of binding security guarantees. Markets have largely discounted geopolitical risk, but that complacency rests on the assumption that conflicts remain contained—an assumption that carries increasing weight as risk premiums thin.

Piedmont Perspective

Holiday Violence in a Connected World

Recent tragedies in Australia and at Brown University in Rhode Island are first and foremost moments of human loss. They occurred in spaces meant for celebration, learning, and community reflection, making their impact especially profound.

In recent years, violent attacks and unrest during the holiday season have become more frequent, particularly around large public gatherings tied to religious or cultural observance. From shootings and vehicle attacks in the United States to violent protests and security disruptions around Christmas markets in Europe, holidays have increasingly become moments when grievance, symbolism, and visibility converge.

While each incident is unique, many recent attacks and disruptions share a common thread. Grievances, often shaped or intensified by distant geopolitical conflicts, particularly in the Middle East, are increasingly being expressed locally. High-profile holidays and large public gatherings offer symbolism, visibility, and emotional resonance, making them vulnerable soft targets.

Holidays have always concentrated people, emotion, and symbolism. What has changed is the speed of transmission. Global conflicts are now experienced locally and emotionally in real time, amplified through fragmented information channels and absolutist framing. The fact that the FBI announced Monday that it disrupted a terror plot on the West Coast underscores both the persistence of these risks and the degree to which many threats never reach public view.

More troubling still, the language and moral framing of extremist narratives have increasingly bled into mainstream political discourse. While most participants, on the right and the left, reject violence outright, the normalization of absolutist, zero-sum framing lowers the threshold for radicalized individuals to act.

These dynamics matter economically. Social cohesion is a form of capital. When it erodes, confidence becomes fragile. Fragile confidence affects risk appetite, investment horizons, labor mobility, tourism, and, ultimately, growth.

What follows from this is not inevitability, but responsibility. Communities that fare best invest quietly in prevention by coordinating security around major gatherings, maintaining trusted local leadership, and sustaining institutions that identify isolation before grievance hardens into action. Preparedness also means having clear contingencies in place to respond quickly when tragedies occur, with the aim of saving lives and restoring order.

After a tragedy, the response matters. Collective mourning and visible, genuine support for victims and their families help restore confidence in shared spaces and prevent fear from becoming the lasting legacy. Just as importantly, these responses affirm that the overwhelming majority rejects violence, extremism, and the tactics of terror.

Empathy must come first. But resilience—social and economic alike—is sustained by the steady, often unseen work communities do before and after crisis. In that quiet resolve lies a critical source of stability, confidence, and long-term growth.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 15, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000