Highlights of the Week

- CPI and PPI came in lower than expected, reinforcing recent disinflation trends ahead of a tariff-driven bump.

- Upstream pricing shows limited tariff pass-through, though businesses are reporting otherwise and tariff revenue has surged.

- Small business optimism rebounded slightly but investment and hiring plans remain subdued amid policy uncertainty.

- Consumer sentiment rebounded in early June and inflation expectations fell.

- The labor market continues to show signs of softening, with jobless claims firming and continuing claims elevated.

- The U.S. and China tentatively reached a tentative deal to reduce tariffs and allow exports of critical materials; Israel struck Iran’s nuclear facilities—killing key military figures and drawing drone and missile retaliation.

- G-7 leaders to meet in Canada next week; geopolitical risk and energy security expected to dominate the agenda.

- Inflation trends and the volatile policy/geopolitical environment support the Fed’s pause. The labor market is cooling, however, and the balance of risks is shifting as inflation undershoots expectations. The Israel–Iran conflict has recalibrated global risks, with global growth likely to decelerate further.

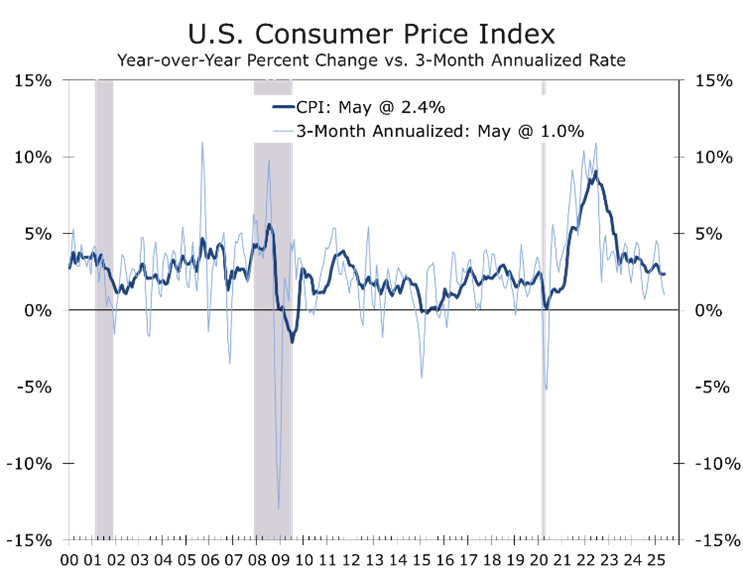

Inflation: Unexpectedly Cooling

May’s CPI and PPI prints once again surprised on the soft side—headline and core CPI rose +0.1% m/m; and the headline PPI matched that pace, with core goods prices declining. Businesses are apparently absorbing tariffs or deferring their impact by relying on previously source goods, especially in new motor vehicles and apparel. The core CPI has risen at just a 1.7% annualized pace over three months, while falling energy prices and smaller price hikes at the grocery store have held the overall CPI to just a 1% pace. This has allowed real wages to eke out modest gains, supporting consumer spending.

Tariffs are not proving to be as terrifying, as inflation continues to run below expectations.

Inflation fears appear overblown. While tariffs will eventually raise prices on select imports, they also reduce consumers’ discretionary spending power—limiting broader inflationary spillover. With roughly two-thirds of household spending concentrated in domestic services, any tariff-driven rise in goods prices is likely to be offset by disinflation in categories such as travel, dining, and recreation. The net effect is a dampened pass-through to overall inflation, opening the door for a rate cut.

Nearly every measure of inflation is moderating faster than expected, including measures of core services, which were problematic a year ago.

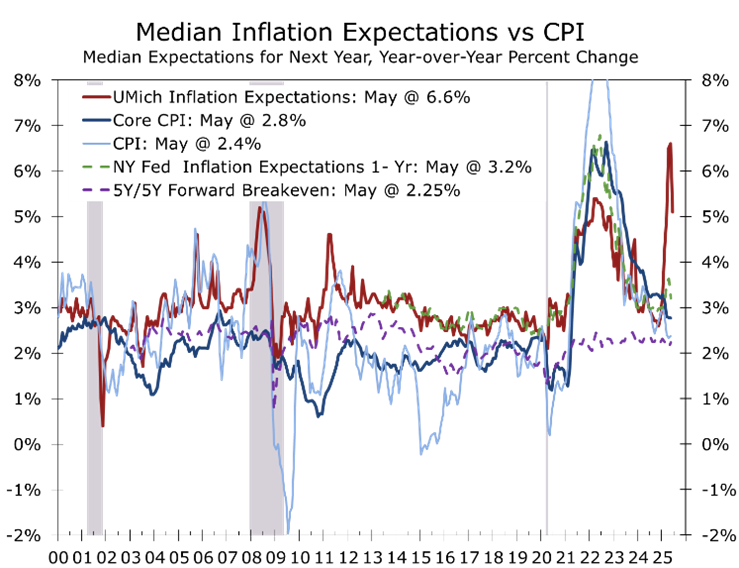

Consumer sentiment improved in early June, with the preliminary University of Michigan index rising to 60.5 from 52.2. The rebound, which broke a five-month downtrend, appears tied to the recent easing of U.S.–China tariff tensions, lower gasoline prices, easing grocery prices, and a resilient labor market.

All five of the survey’s components increased, with current conditions rising 4.8 points and expectations climbing 10.5. Encouragingly, the sentiment recovery was broad-based—cutting across income, geography, and political affiliation. The improvement in expectations is notable, as they are most closely tied to actual spending and had been severely depressed.

Consumer sentiment improved broadly in early June, while inflation expectations declined.

Year-ahead inflation expectations fell 1.5 percentage points to 5.1%, and long-run expectations edged lower to 4.1%, signaling some tentative improvement in inflation psychology. The retreat in expectations was overdue and came alongside equity market gains and another round of surprisingly benign inflation reports. The lack of a resurgence in inflation tied to tariffs reduces the risk that consumers will pull back spending preemptively. The data also preceded Israel’s attack on Iran’s nuclear facilities and defense infrastructure.

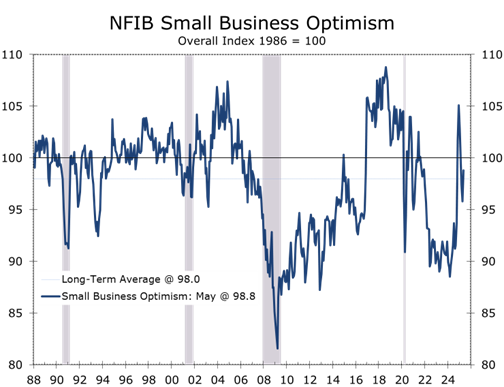

Business Sentiment: Cautious Stabilization

NFIB small business optimism rose to 98.8 in May—its first increase in six months—as sales expectations improved. Owners remain frustrated by the lack of progress on tax and regulatory relief and are struggling to absorb tariff-related cost increases. Capital spending plans are muted, with policy uncertainty delaying investment. Survey results align with ISM and factory orders data showing flat demand and persistently weak exports.

Labor Market: Cooling, Not Cracking

Initial jobless claims held at 248,000 for the week ending June 7, while the four-week average rose to 240,250—its highest since August 2023. Continued claims climbed to 1.956 million, the most since late 2021. While some of the increase may reflect seasonal transitions, the broader trend points to a softening labor market.

Federal employee claims remain below February highs, but signs of structural slack are emerging. The long-term unemployed share is rising, and surveys signal slower hiring amid tariff uncertainty. Layoffs remain low, yet job postings are down and reemployment is taking longer—pointing to growing friction. Still, conditions remain stable enough for the Fed to prioritize inflation control, though risks now tilt toward further labor market weakening.

Trade Outlook: Pause, Not Peace

The U.S.–China trade deal capped U.S. tariffs at 55%, China’s at 10%, and introduced a temporary rare-earth export agreement. The deal is tentative and allows companies to apply for a six-month license to purchase rare earths and magnets. While this removes some downside risk—a final settlement remains far off. GDP forecasts for 2025 have increased slightly. Our latest forecast, released Tuesday, calls for 3.8% growth in Q2, following by 1.4% growth in the second half of the year. For the year as a whole, we see real GDP rising 1.7% on a Q4/Q4 basis.

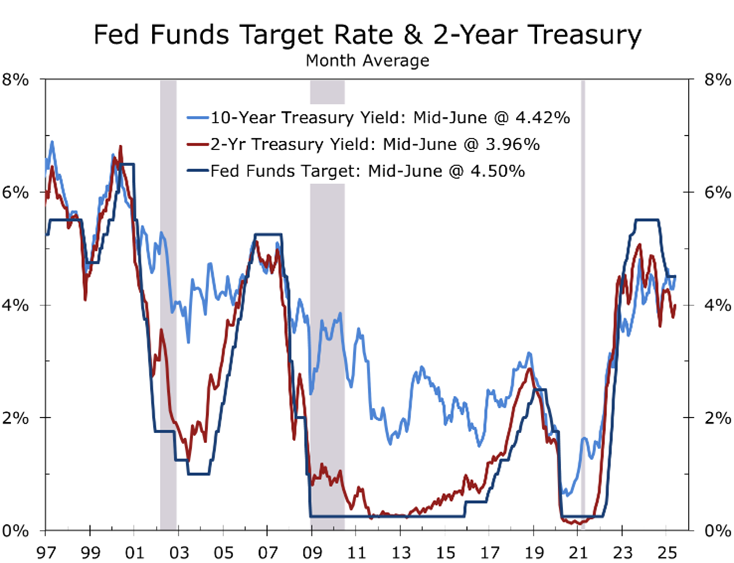

Recent Treasury auction data show mixed demand: the June 10-year note auction cleared at 4.45%, with soft indirect demand, pointing to market caution amid elevated supply. Meanwhile, the May Monthly Treasury Statement showed a $316 billion deficit—better than last year’s $347 billion—but fiscal year-to-date deficit widened 13.5% versus FY2024 thanks to a torrent of spending late last year and in early 2025. Rising entitlement costs, defense spending, and elevated interest payments remain structural headwinds.

Tariff revenue, now expected to contribute $2.5 trillion over the decade, provides some cushion and comes close to covering the CBO-project revenue loss from the GOP-led One Big Beautiful Bill’s tax cuts and spending hikes.

Geopolitical Risk: Rising Lion and Global Fallout

Israel launched a major military campaign—Operation Rising Lion—striking upwards of 100 Iranian nuclear and military sites, including Natanz and Isfahan. The strikes killed IRGC Commander Hossein Salami and senior commanders Mohammad Bagheri and Amir Ali Hajizadeh. Iran responded by launching 100 drones, which were largely intercepted by Israeli defenses.

New intelligence suggests the Israeli campaign included covert drone strikes, launched within Iran, on ballistic missile launchers and a decapitation operation targeting senior military leadership. Confirmed airstrikes included high-value targets such as the Natanz Enrichment Complex, Kermanshah underground missile storage, and key sites in Tehran and Esfahan. Much of Iran’s military leadership was eliminated in highly targeted strikes. Iran’s immediate response was muted—analysts believe Israel’s disruption of missile infrastructure and the deaths of key military leadership delayed a coordinated counterstrike. Iran has since launched missile barrages, most of which have been intercepted.

Iranian Supreme Leader Khamenei vowed retaliation but offered no specifics. Meanwhile, Tehran has suspended nuclear negotiations and may escalate its regional posture through proxies like the Houthis and Hezbollah. Israel apparently has free reign over Iranian skies and is openly refueling fighter bombers in clear daylight. Nuclear facilities are likely to be hit repeatedly in order to destroy the hardened bunkers they reside in. Israel has said the operation could last for up to two weeks and the objective is to eliminate the nuclear program—not set it back.

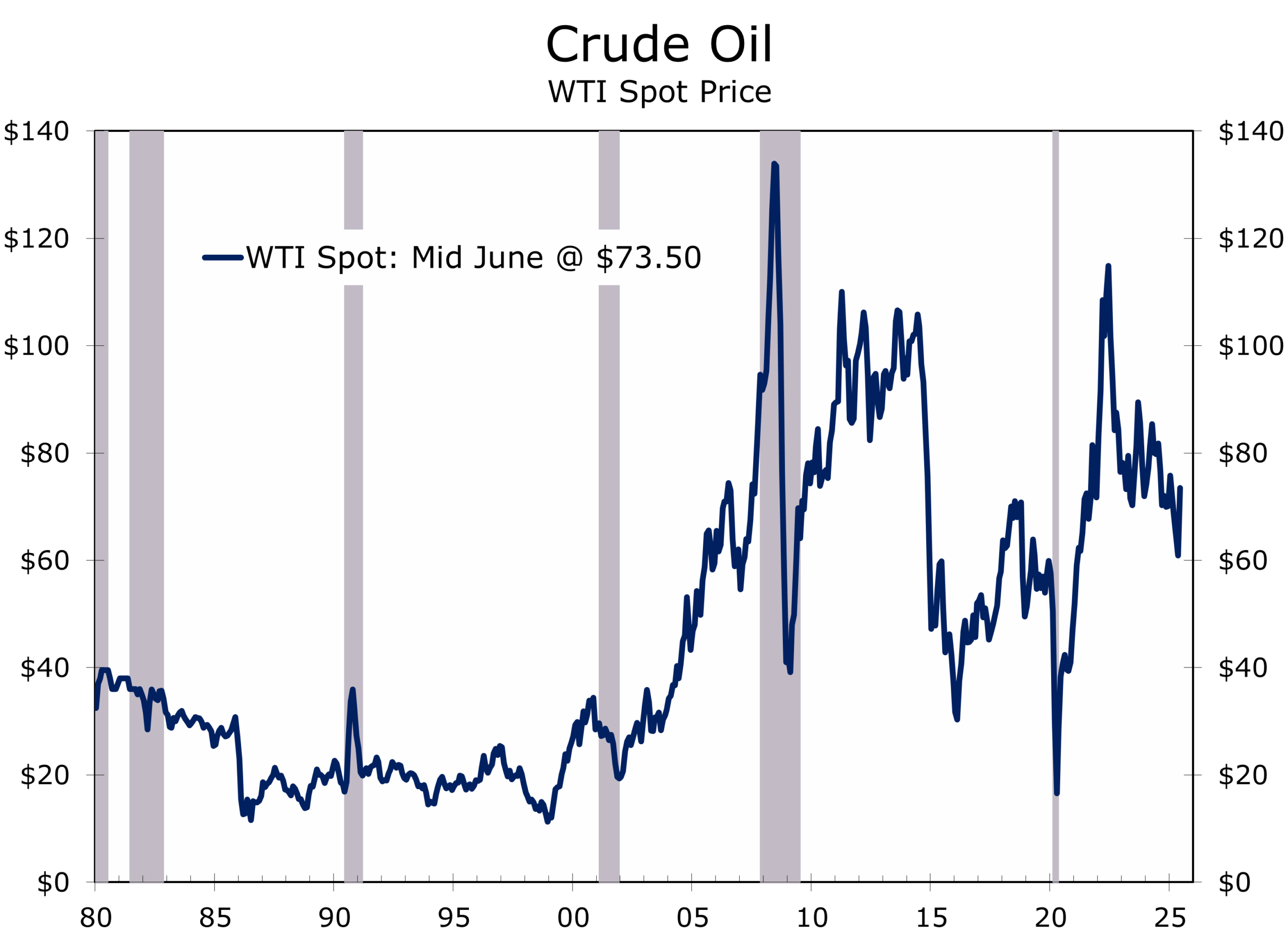

A frustrated and defeated Iran may lash out at its population, which was openly feeding information to Israel via the internet before Iranian authorities worked to shut down internet access. Iran might also strike neighboring oil facilities. Oil markets reacted with a 7–8% spike, and safe-haven demand surged for Treasuries and the dollar. Oil prices are still lower than they were a few months ago.

G-7 leaders, set to meet in Kananaskis, Alberta, Canada from June 15 to 17, 2025, are expected to confront a crowded agenda. Discussions will likely span artificial intelligence, global economic imbalances, defense partnerships, and regional stability—including the Israel–Iran conflict and support for Ukraine. The setting—a return to the Canadian Rockies where the 2002 summit was held—underscores the gravity of the moment. Hosted by Canadian Prime Minister Mark Carney, this 51st summit will also welcome key invitees including Ukraine’s President Zelenskyy, along with leaders from Australia, South Korea, India, Brazil, and Saudi Arabia. Coordination—or lack thereof—will shape market risk sentiment as the G-7 grapples with an increasingly fractured global order.

Recalibrating Risks

Inflation trends and the volatile policy environment support the Fed’s pause. The labor market is cooling, however, and the balance of risks is shifting as inflation repeatedly undershoots expectations and jobless claims edge higher. Tariff and tax uncertainty continue to weigh on investment and hiring.

The Israel–Iran conflict has recalibrated global risks. Treasuries, the dollar and gold are drawing safe-haven demand. The G-7 and FOMC meetings will serve as key diplomatic and economic inflection points to incorporate shifting geopolitical and economic risks. Israel has stated that it is planning a 14-Day operation to eliminate the Iranian nuclear program. Merely setting the program back would be a failure and increased global risks.

Markets will be watching for any shift in diplomatic posture toward Israel and Iran, as well as how the Fed recalibrates the inflationary risks from tariffs and higher energy prices against the disinflationary pressures of slowing growth.

Looking Ahead: Week of June 17, 2025

- FOMC Meeting (June 17–18): Expect the Fed to hold rates steady, but all eyes are on forward guidance and risk assessments. Market focus will be on Powell’s tone amid mixed macro data, slower inflation and elevated geopolitical risks.

- Retail Sales (May): Tuesday’s Retail Sales report will help further shape expectations for Q2 growth. Look for a rebound in discretionary purchases, which jumped in March ahead of tariffs and fell back in April.

- Housing Starts and Permits (May): Homebuilders face demand headwinds from rising insurance premiums and lingering affordability challenges. New home inventories have been rising, and builders have been cutting prices to spur sales. We expect another soft reading for both single- and multifamily starts.

- G-7 Summit (June 15–17, Kananaskis): Leaders from the G-7 and invited nations will tackle AI governance, support for Ukraine, Middle East volatility, global trade, and defense collaboration. Specific attention will be paid to China’s economic coercion, USMCA renewal prospects, and the economic governance gap between the G-7 and BRICS.

- Geopolitical Watch: Iran’s response to Israeli strikes—and whether proxies such as the Houthis or Hezbollah can coordinate retaliatory attacks—remains a key geopolitical risk. Any G-7 coordination on sanctions or diplomatic overtures could meaningfully shift global risks but not until Israel destroys much or all of Iran’s nuclear infrastructure.

- Treasury Refunding Outlook: Watch for potential updates on long-duration issuance plans and bond market reactions to persistent deficit concerns.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

June 13, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000