Highlights of the Week

- Venezuela stirred headlines and sentiment, but ample oil inventories and firm oil fundamentals kept energy prices contained, reinforcing confidence rather than caution.

- Oil and defense stocks rallied, reflecting the prospect of incremental gains to U.S. and Western oil firms, which alone have the expertise needed to boost Venezuelan production.

- Manufacturing is treading water. Production is edging forward modestly, while firms continue to trim labor and run unusually lean inventories as they wait for greater policy clarity.

- The quiet delay of furniture tariffs underscores a broader shift from tariff absolutism to tariff optionality. The switch is important for inflation dynamics, corporate margins, and Federal Reserve timing.

- Policymakers are threading a narrow path as growth stabilizes, inflation cools at the margin, and geopolitical risk rises without yet spilling meaningfully into the macro data.

- The week ahead is unlikely to alter the economy’s direction of travel, but it should clarify the story. Growth is decelerating toward trend, not stalling or rolling over.

Calibrated Power, Calibrated Policy

The first full trading week of 2026 offered a familiar lesson dressed in new clothes. Geopolitics can move markets, but fundamentals still write the longer chapters. The arrest of Venezuela’s Nicolás Maduro delivered an early risk-on jolt, pushing equities to record highs and briefly reviving talk of a supply-side oil shock. Yet crude prices barely flinched. Brent and WTI drifted lower, a reminder that global inventories, spare capacity, and demand elasticity still matter more than regime headlines. History rhymes here. Iraq in 2003 changed geopolitics overnight, but oil prices ultimately followed barrels, not banners.

Markets are rediscovering an old truth: geopolitics can move prices in the short run, but fundamentals will anchor them over time.

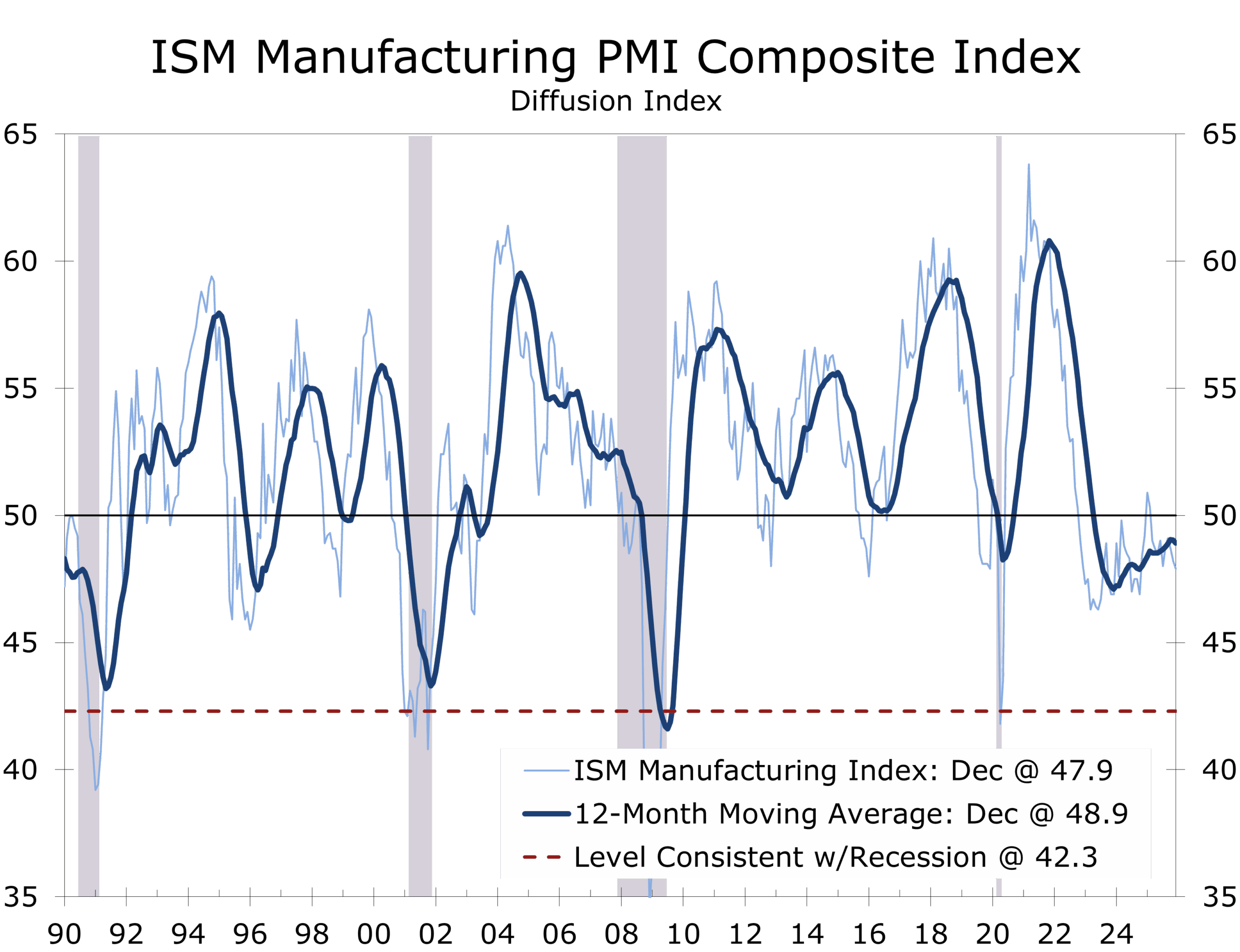

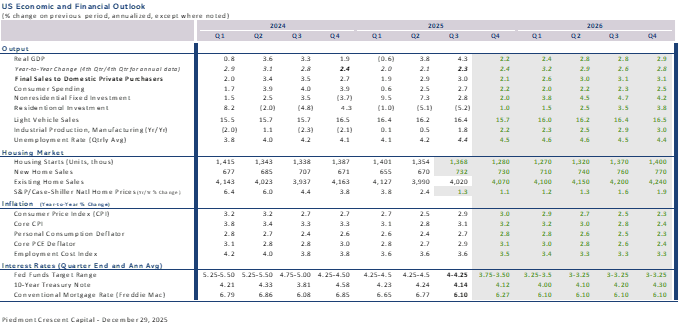

That same tension between narrative and reality showed up in Monday’s ISM Manufacturing report. The overall PMI fell 0.3 percentage points to 47.9 in December, marking the tenth consecutive month below the expansion threshold and the weakest reading of 2025.

Despite its long run in contraction territory, the weaker ISM index is not a signal of collapse. Instead, it is a picture of a factory sector treading water. Production is eking out modest gains, but manufacturers remain cautious—paring payrolls, preserving liquidity, and holding inventories at unusually lean levels. Capital spending continues, but selectively. Firms are not retreating so much as waiting.

What manufacturers are waiting for is clarity. Trade policy uncertainty and labor availability remain the binding constraints, not demand. On that front, the Trump Administration appears increasingly inclined to oblige. The policy posture emerging early in 2026 is consistent with our central calls for the year: that restoring affordability and momentum ahead of the midterm elections would require easing cost pressures rather than amplifying them. A lighter touch on tariffs and a more pragmatic approach to immigration both fit that playbook.

Manufacturing is not weak because demand has vanished, producers are overly cautious because policy clarity has.

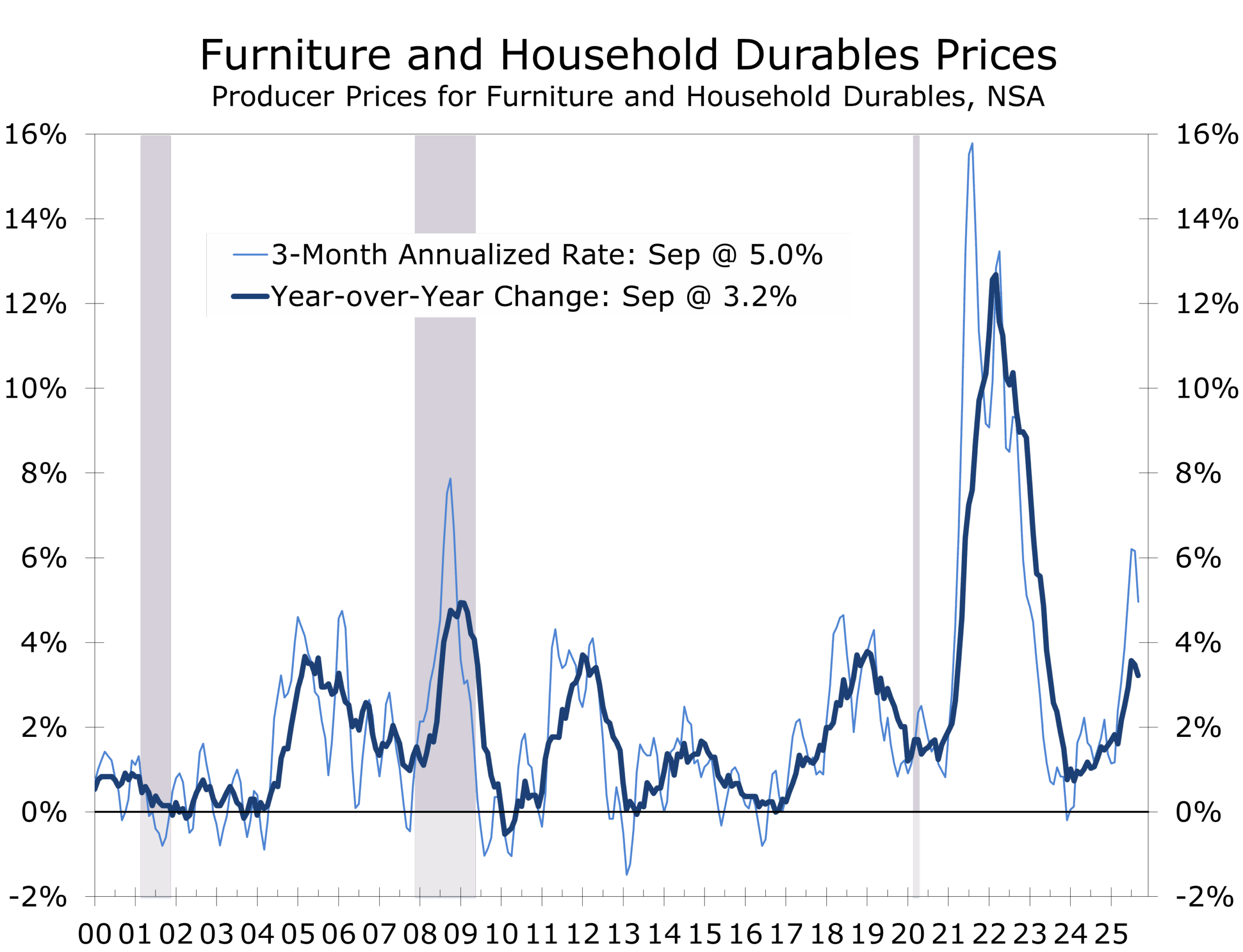

Against that backdrop, trade policy delivered one of the more telling signals of the week. The decision to delay scheduled tariff increases on upholstered furniture, kitchen cabinets, and vanities into 2027 is small in headline terms but meaningful in context. This was not a rollback. Existing tariffs remain in place. But it was a clear acknowledgment of inflation sensitivity and political timing. Furniture is a highly visible, price-elastic category. Allowing tariffs to ratchet higher would have fed directly into consumer prices at a moment when policymakers are trying to declare progress.

Markets understood the message. Home goods and furniture stocks rallied as near-term margin risk eased, and retailers gained a rare commodity in today’s environment: cost visibility. More broadly, the move reinforces a quiet but important evolution in trade strategy. Tariffs are being treated less like permanent fortifications and more like negotiating instruments with built-in off-ramps. That flexibility lowers near-term inflation risk and supports risk assets, even as it raises longer-term planning uncertainty for global supply chains.

Policy restraint is quietly doing some of the Fed’s work for it.

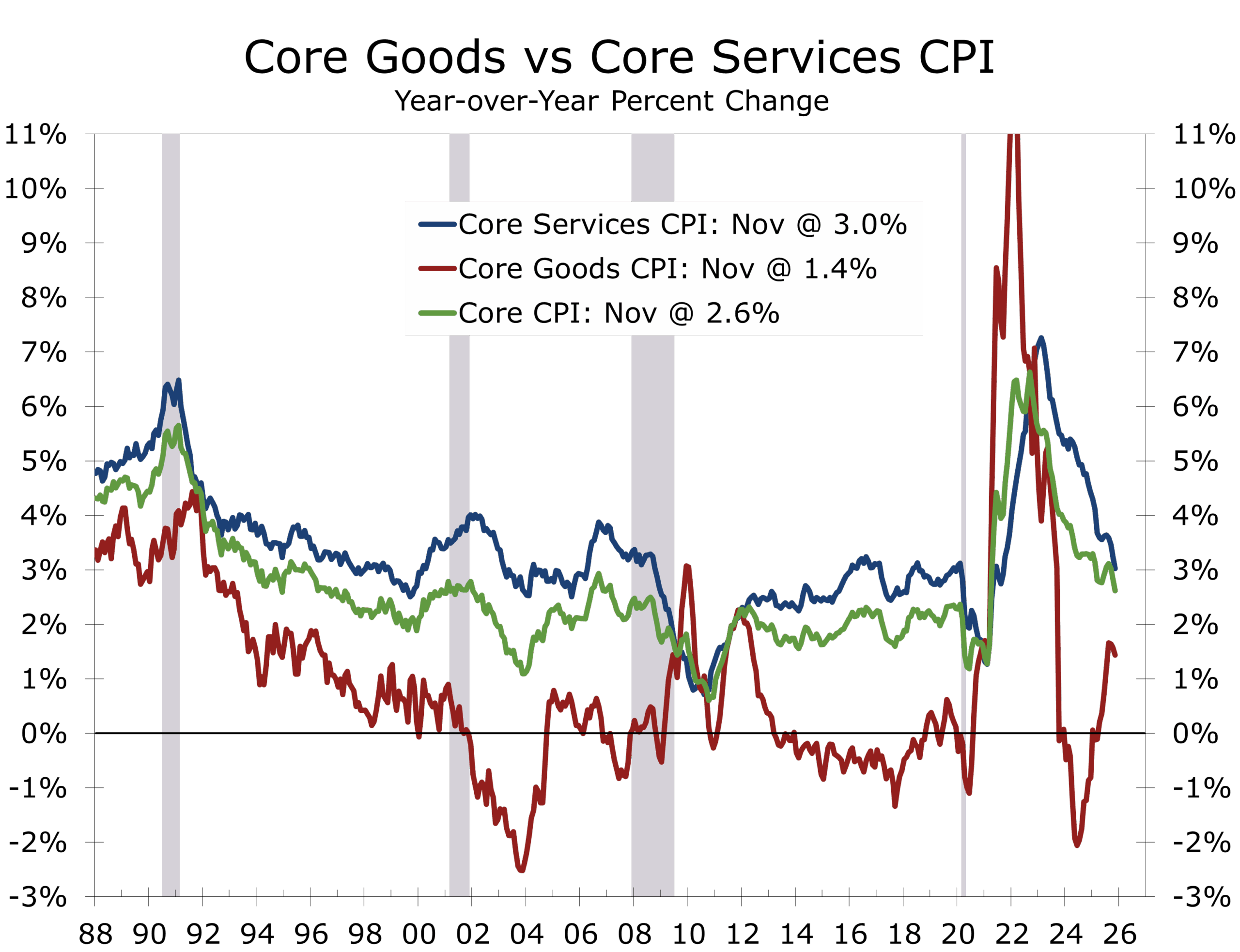

For the Federal Reserve, this matters at the margin. Goods disinflation has been one of the more reliable allies in the fight against inflation. A tariff escalation would have complicated that story just as services inflation shows signs of grinding lower rather than falling cleanly. By delaying the tariff hike, policymakers effectively removed one potential source of renewed price pressure from the 2026 outlook. It does not force the Fed’s hand, but it narrows the set of upside inflation risks the Committee must weigh as it debates the timing and pace of eventual rate cuts.

More broadly, the move reinforces a quiet but important evolution in trade strategy. Tariffs are being treated less like permanent fortifications and more like negotiating instruments with built-in off-ramps. That flexibility lowers near-term inflation risk and supports risk assets, even as it raises longer-term planning uncertainty for global supply chains.

Policy restraint is quietly doing some of the Fed’s work for it, reinforcing the disinflationary trend.

For the Federal Reserve, this matters at the margin. Goods disinflation has been one of the more reliable allies in the fight against inflation. A tariff escalation would have complicated that story just as services inflation shows signs of grinding lower rather than falling cleanly. By delaying the tariff hike, policymakers effectively removed one potential source of renewed price pressure from the 2026 outlook. It does not force the Fed’s hand, but it narrows the set of upside inflation risks the Committee must weigh as it debates the timing and pace of eventual rate cuts.

Geopolitically, the landscape remains unsettled but contained. Venezuela’s future oil contribution is likely measured in quarters, not weeks, and depends on capital, infrastructure, and sanctions mechanics as much as politics. We expect a modest uptick in oil output this year, somewhere around 300,000 additional barrels per day. Gains beyond that will require significant investment and time. What markets seem to be underestimating is U.S. energy know-how, specifically related to Venezuelan crude.

Russia’s war in Ukraine continues to evolve tactically rather than strategically, while China’s tightening grip on dual-use exports to Japan underscores how economic statecraft is becoming more precise, more targeted, and harder to model. None of this has yet bled meaningfully into U.S. macro data, but it continues to shape the risk distribution around the outlook.

The still-growing protests in Iran hold the most promise for the next major geopolitical upheaval. Change may also come sooner than expected in Cuba, but talk about Greenland is most likely a distraction. Unless Greenland becomes a base for Chinese and Russian asymmetric attacks on the U.S., there is no reason for Denmark or other NATO nations to be concerned about an unwanted military takeover by the U.S. Remember that President Trump is always negotiating. The repeated heightened rhetoric on Greenland may be designed to secure a more favorable arrangement with Greenland, such as a lease deal or a mineral rights deal. The U.S. already has the right to operate military bases in Greenland.

Early 2026 is shaping up as a period of calibrated power and calibrated policy. Growth is slower but steadier. Inflation is easing, but has not been vanquished. Manufacturing is waiting, not failing. Tariffs are no longer blunt instruments, and geopolitics is loud without yet being inflationary. The margin for error is thinner than it looks—but the runway remains open, for now.

2026 Top Calls

- Manufacturing treads water, then stabilizes. Production growth remains modest, inventories stay lean, and labor trimming continues into midyear, but conditions improve as policy uncertainty fades.

- Tariffs become more flexible, not more forceful. Expect selective delays, exemptions, and enforcement discretion aimed at containing inflation and protecting politically sensitive consumer categories.

- Immigration pragmatism returns quietly. Incremental easing helps stabilize labor supply, lower service-sector cost pressures, and support affordability without reopening broader political fights.

- The Fed cuts later and by a little less than markets once expected. With goods disinflation intact and services inflation grinding lower, the Fed gains time rather than urgency.

- Geopolitical risk stays elevated but contained. Markets price uncertainty, not disruption, favoring resilience over recession trades.

For a deeper discussion of our macro framework and policy outlook, see the December edition of The CAVU Compass, where these themes were first laid out in detail.

The Piedmont Perspective

The removal of Nicolás Maduro is more than a regime change. It is a stress test of a gray-zone alliance built on opacity, grievance politics, and sanctions arbitrage. For more than a decade, Caracas served as the Western Hemisphere hub of a loose alignment linking Russia, China, Iran, and Cuba. The glue was not ideology but utility: Venezuela offered geography, oil optionality, and permissive terrain for sanctions evasion; its partners provided capital, weapons, intelligence cooperation, and diplomatic cover.

That ecosystem extended beyond states. Venezuela became an enabling environment for Iran-aligned networks tied to Hezbollah and, indirectly, Hamas. Caracas did not direct militant operations, but it lowered coordination costs through diplomatic alignment, financial opacity, and limited physical safe haven. Permissive hubs matter: they reduce friction, extend reach, and complicate enforcement.

That model now looks fragile. Asymmetric coalitions tend to hold only while their hubs remain intact. Russia’s leverage in Venezuela was coercive and military, optimized for access rather than development. China’s engagement was financial and extractive, centered on oil-backed lending that insulated Beijing while hollowing out PDVSA. Iran focused on sanctions workarounds and logistics, using Venezuela as both testbed and rear area. With Caracas destabilized, the connective tissue frays. No partner can easily replicate Venezuela’s mix of proximity to U.S. markets, energy scale, and permissiveness elsewhere in the hemisphere.

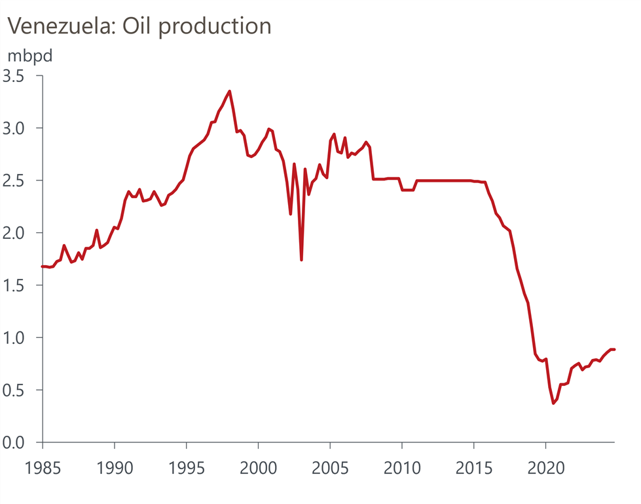

Markets initially priced these developments through energy, but expectations should remain disciplined. Venezuela holds roughly 303 billion barrels of proven reserves, yet production remains a fraction of late-1990s peaks above 3 million barrels per day. Recent output has hovered around 650,000–750,000 barrels per day, with exports discounted and routed through opaque channels, largely to China.

Venezuela is a geological superpower operating like a marginal producer. Years of underinvestment, infrastructure decay, sanctions frictions, and human-capital flight make supply restoration a medium-term project, not a cyclical shock. Even under a credible transition, gains would be incremental and capital-intensive, constrained by financing, diluent availability, and logistics. This is not an oil-shock story; it is an optionality story constrained by capital, infrastructure, and credibility.

The slope matters more than the headline. U.S. technology lowers break-evens before it lifts volumes.

Pundits are underestimating the U.S. technology advantage. Expertise in heavy-crude processing, enhanced recovery, project execution, and cost discipline can materially lower Venezuelan break-evens over time. The most plausible path is a modest rise in output in 2026—on the order of 300,000 barrels per day—followed by more durable gains contingent on political clarity and capital access.

An important regional tail risk has also diminished. The prospect of Venezuelan pressure on oil-rich Guyana has faded as Caracas destabilizes and its external backers turn defensive. That removes a non-trivial risk to one of the world’s fastest-growing new oil provinces and supports the view that recent events reduce upside volatility in energy markets rather than create a supply surge.

The more durable market impact runs through financial plumbing, not crude flows. Venezuela functioned as a settlement node for sanctioned trade, providing parallel payment rails, gold-for-energy exchanges, and opaque mechanisms. Removing that node raises transaction costs, lengthens settlement chains, and increases enforcement risk. It does not reverse reserve diversification, but it slows its velocity at the margin.

At the margin, this is modestly dollar-supportive. Reduced leakage reinforces the dollar’s role as the least-bad settlement option in a fragmented system. The effect is best read as a reduction in downside risk, not a new upside catalyst. By lowering the odds of energy-led inflation surprises and tightening financial plumbing, these shifts reduce the likelihood that the Federal Reserve is forced into a defensive policy response.

Risks remain. Cyber retaliation, proxy agitation, and short-term commodity volatility fit the playbook of a network under pressure. When opaque systems lose a hub, coordination degrades before adaptation sets in. Near term favors noise; medium term favors fragmentation and normalization.

Toppling the Maduro regime is no victory lap. It is a clearing of fog. The Americas regain strategic depth. Energy markets gain marginal optionality rather than abundance. And a coalition built on friction, provocation, and evasion finds itself, at least temporarily, short of all three.

The broader lesson extends beyond the hemisphere. Gray-zone power projection relies on permissive hubs combining geography, resources, and weak governance. When those hubs are disrupted, coordination tightens and strategic optionality narrows. For Beijing, the signal is less about oil than exposure. Sustaining external pressure campaigns, including around Taiwan, requires economic resilience, diplomatic bandwidth, and reliable logistics. Peripheral entanglements dilute focus and raise costs; patience, resilience, and allied cohesion remain the more durable sources of leverage.

Looking Ahead: Cooling, Not Contracting

The remainder of the week should reinforce a theme that is becoming clearer as 2026 begins. Manufacturing is treading water, and the broader U.S. economy is cooling following the outsize 4.3% real GDP growth in the third quarter. That deceleration, however, should not be mistaken for deterioration. Growth is likely converging toward its underlying trend, which is best approximated by private domestic final demand and has been growing at a 2.5% pace.

The key question now is not whether the economy is slowing, but what is doing the work underneath the hood. How much of that growth is being driven by capital deepening—investment in equipment, software, AI infrastructure, and productivity-enhancing technologies—and how much is still coming from labor inputs? That distinction will shape both the inflation outlook and the Federal Reserve’s tolerance for patience.

This week’s labor-market data will help clarify that balance. ADP and JOLTS should confirm continued cooling in labor demand rather than outright weakness. Job openings are expected to drift lower, consistent with firms trimming at the margin while remaining reluctant to shed workers aggressively. That pattern aligns with an economy leaning more on productivity than hiring to drive growth.

The ISM Services report later in the week will provide an important cross-check. Services activity remains expansionary, but employment components have been softening. A further easing would reinforce the view that labor is no longer the primary growth engine, even as demand holds up.

Friday’s employment report should anchor the week. Payroll growth is expected to remain positive but modest, with the unemployment rate holding near recent levels (possibly rising 0.1 percentage point at most) and wage growth contained. An outcome along those lines would be consistent with an economy growing near trend rather than above it, as the Q3 data showed. Economic growth is moderating but not slipping to stall speed or less.

From a policy perspective, this composition matters. Growth driven by capital deepening and productivity is inherently less inflationary than growth driven by rapid labor expansion. If the data continues to support that mix, the Federal Reserve gains time. The debate shifts from whether cuts are needed urgently to how confident policymakers can be that disinflation continues without requiring a material rise in unemployment.

The bottom line is the economy is slowing toward trend, not rolling over. Manufacturing is waiting, not faltering. And the durability of growth in 2026 will hinge less on how many jobs are added and more on how efficiently capital is deployed. Our forecast remains unchanged from where it has been since the last GDP release, with a slower pace in the near term and a stronger pace as the year progresses.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 6, 2026

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000