Highlights of the Week

- Post-shutdown data confirm an economy that is still expanding but doing so at a noticeably slower pace—fully consistent with our latest CAVU Compass.

- Labor markets continue to soften quietly: Challenger layoff announcements have risen, continuing claims are edging higher, and consumers are increasingly strained by affordability rather than job insecurity.

- Companies are accelerating economic-development announcements as they adapt to rapid tariff adjustments and a more interventionist policy environment.

- Oil and broader commodity prices eased this week as reports surfaced of a potential U.S.–Russia–Ukraine peace framework, reducing the geopolitical risk premium.

- With a slew of projects nearing completion, the coming global LNG supply wave presents a structural disinflation force that will shape energy pricing into 2026.

- Geopolitical risks—including Gaza and Lebanon, the potential Saudi normalization, and possible regime change in Venezuela—remain elevated, even as markets trade with surprising calm.

- The narrative tension developed in the CAVU Compass and extended in our Piedmont Perspective—between official progress and lived experience—continues to define the moment in both the U.S. and globally.

A Clearer View of a Cooling Economy

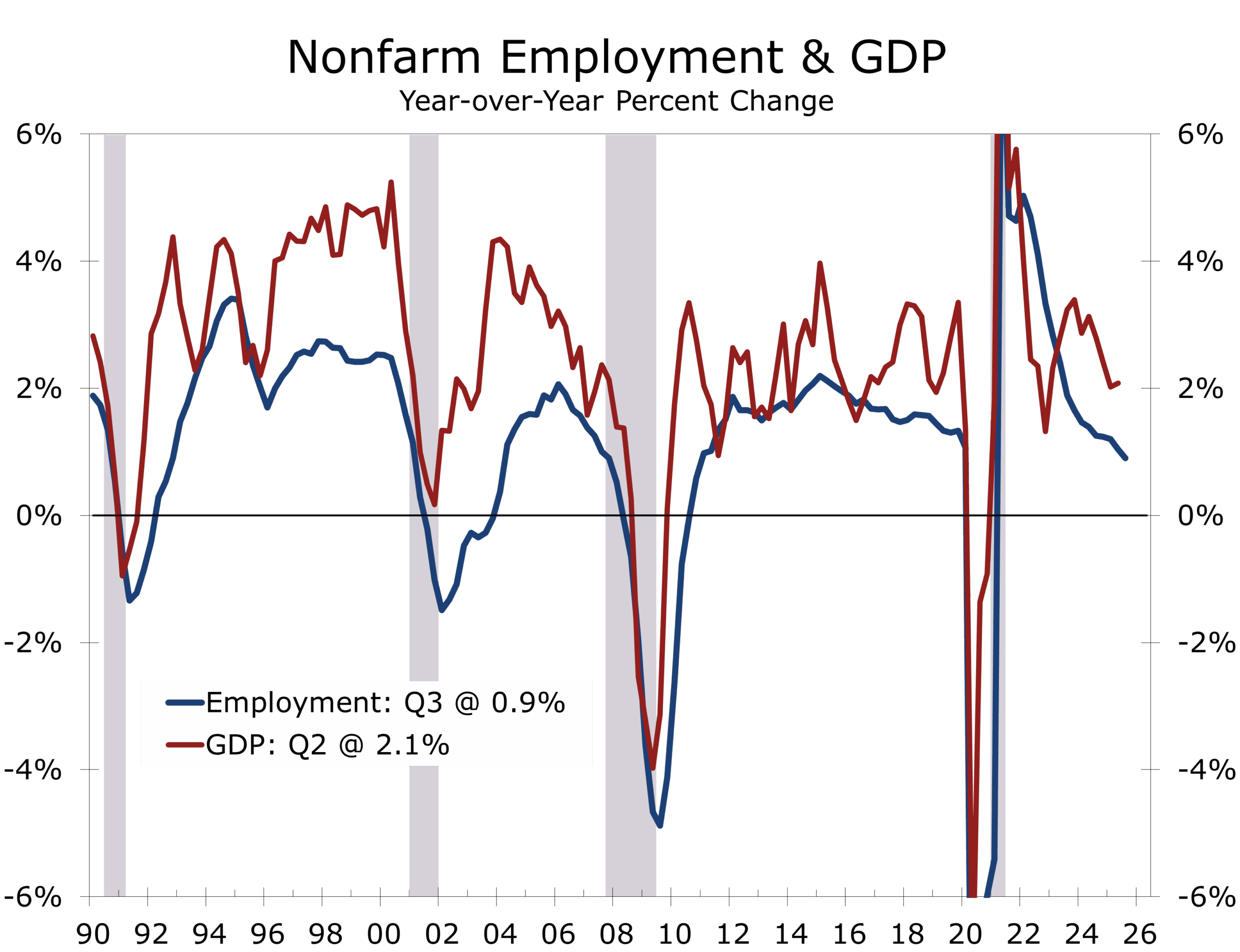

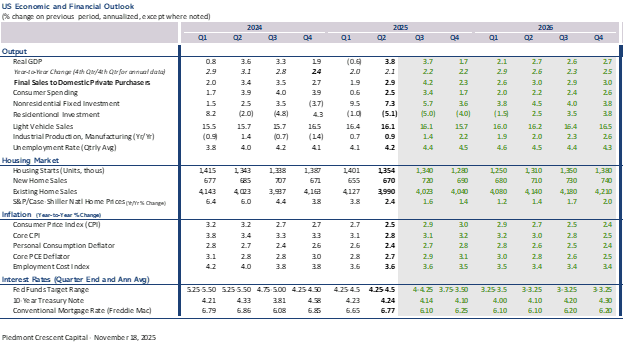

The past week provided a clearer window into the post-shutdown macro environment, and the data that emerged fit neatly within the framework laid out in the latest CAVU Compass. The economy continues to expand, but its pace has become more deliberate and uneven. Third-quarter GDP still appears stronger than initially expected, supported by a narrower trade deficit and firmer construction activity. Yet the underlying rhythm of domestic demand is clearly more moderate than the headline suggests. As the flow of data normalizes, the picture that emerges is not of an economy accelerating into late 2025 but of one easing gradually onto a slower trajectory.

Following a surprisingly strong Q3, growth remains positive but is no longer accelerating.

Growth remains positive but is no longer accelerating

Labor market developments continue to warrant close attention. Headline payroll gains in September were firmer on the surface, but the downward revisions to August and the softening three-month average are more revealing. Initial jobless claims remain low, but continuing claims have risen steadily—an early sign that job seekers are taking longer to reattach to the workforce

The more consequential development came via the Challenger job-cut announcements, which have now begun to rise after months of relative stability. These are not broad-based layoffs, but targeted reductions across a widening set of industries, signaling a shift from hiring freezes toward more active cost control.

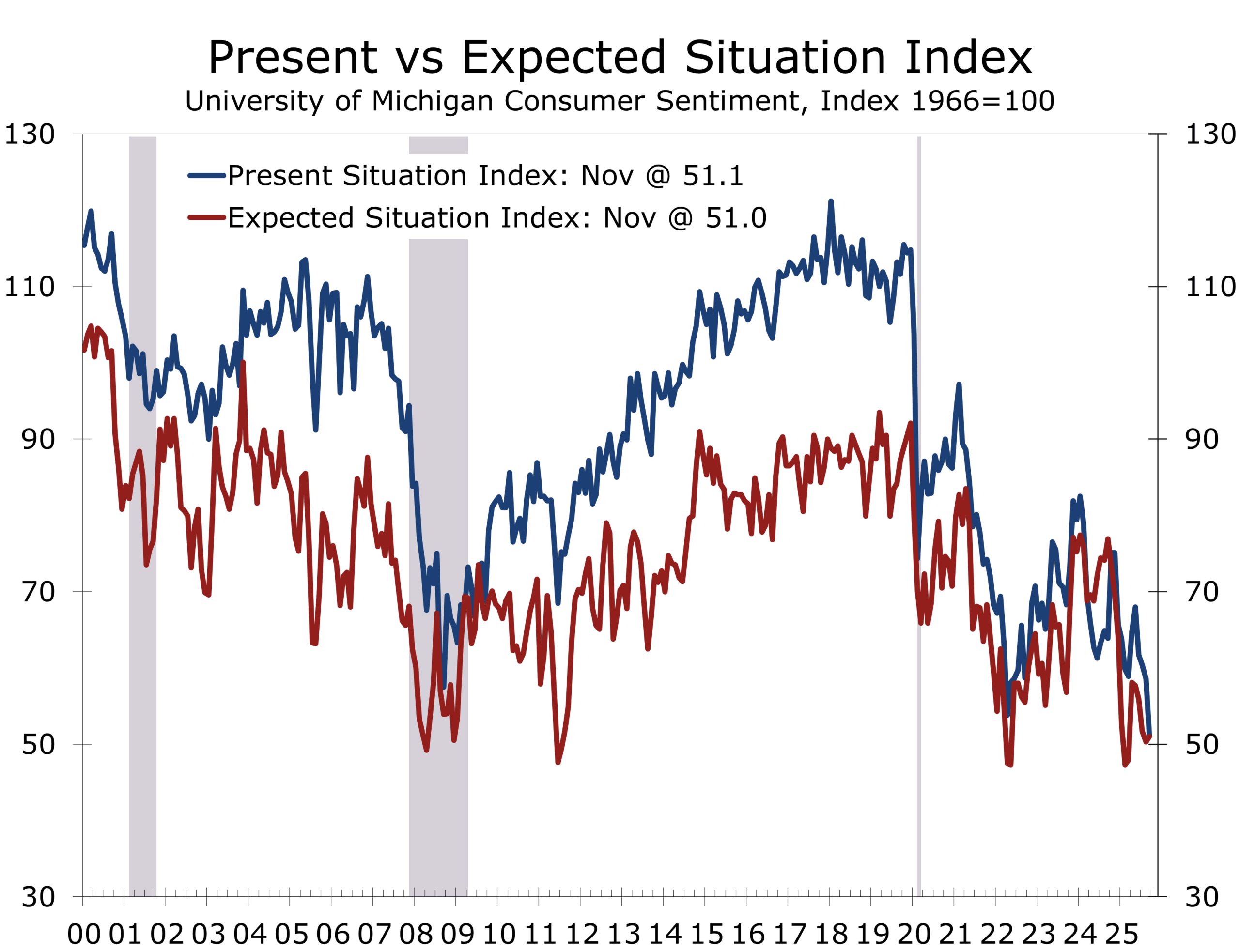

Consumers, meanwhile, remain under pressure. The final University of Michigan Sentiment Index slipped again, reinforcing a theme that has persisted all year: the dominant source of household stress is not fear of unemployment but the cost of living. Elevated rent, insurance, mortgage payments, and utilities continue to weigh on household budgets even as inflation recedes. This gap—between the employer’s view of labor costs and the household’s view of affordability—remains one of the defining tensions of this cycle.

Persistent affordability challenges and a soft job market for recent college graduates is driving anxiety.

The latest Consumer Sentiment data show consumers generally feel more pessimistic about their current financial situation, with buying conditions for durable goods falling to their worst level in more than 40 years, even as year-ahead and long-run inflation expectations eased for a third straight month. Sentiment declined across all income groups, but remains most depressed among lower-income households, reflecting the growing bifurcation of the American consumer.

Monetary policy sits squarely in this middle ground. The October FOMC minutes underscored a divided Committee heading into the December meeting, with members split between the need for additional insurance cuts and the risk of moving too quickly in the absence of fresh official data. Shutdown-delayed payroll and inflation releases mean the Federal Reserve is flying with only partial visibility.

With official economic data still playing catch-up, the Fed will likely err on the side of caution and cut rates at their December FOMC meeting

Market pricing already reflects a multi-quarter sequence of slow, measured rate cuts. The modestly positive slope of the yield curve aligns with this expectation: the curve is not pricing recession, but neither is it pricing acceleration. Rather, it reflects an economy in controlled deceleration with a central bank intent on maintaining credibility.

The curve is modestly positive—and telling a very different story from a year ago

Energy and commodities introduced a notable shift in tone this week. Oil prices eased as reports suggested a potential peace framework between Russia and Ukraine, reducing one of the most important geopolitical risk premia embedded in global commodity markets. Even tentative negotiations can influence pricing when the conflict has disrupted energy flows, shipping routes, and insurance costs for nearly four years. If the diplomatic signals materialize into a more durable arrangement, the corresponding easing in supply risk could prove meaningful for oil, natural gas, wheat, and industrial inputs.

In a major switch, geopolitics appear set to pull prices lower, rather than push them higher

This development comes atop the largest LNG supply wave in history, which is set to expand global energy capacity through the second half of the decade. Together, these forces create a more stable and potentially more disinflationary energy environment going into 2026 that will be more favorable to energy-intensive industry and energy-import dependent economies.

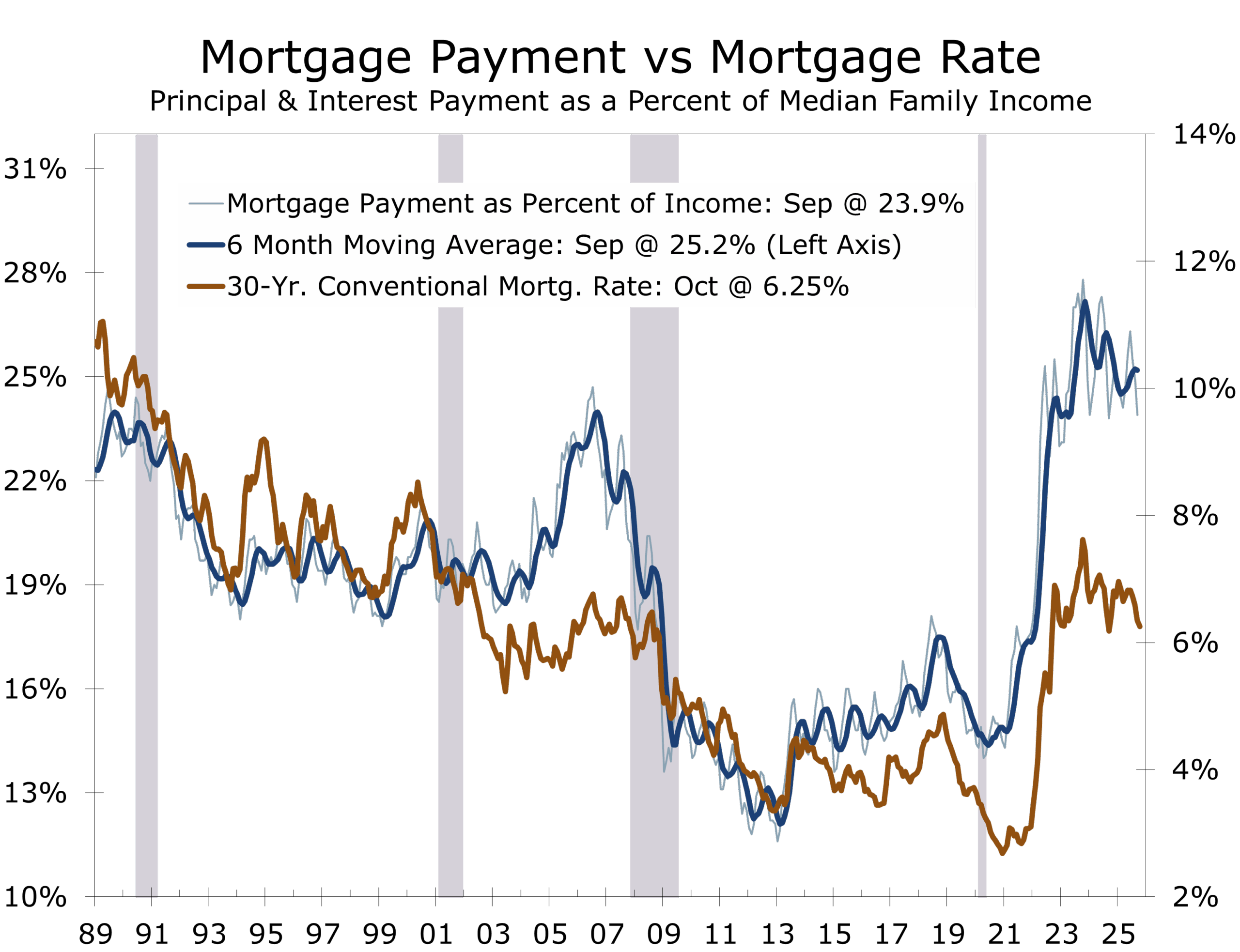

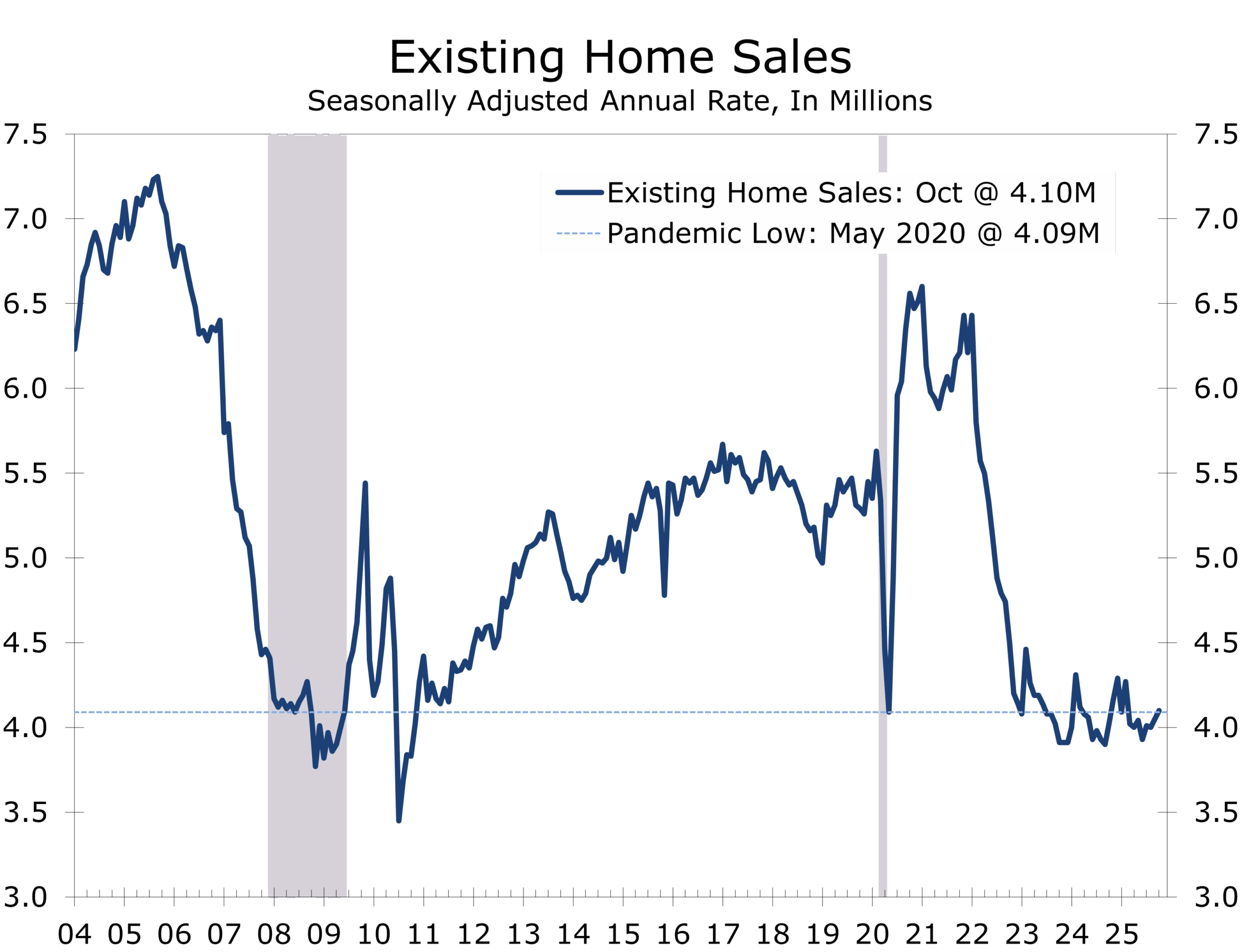

Housing has shown signs of stabilization rather than recovery. Existing home sales have drifted higher, mortgage rates have eased modestly, and builder sentiment has improved. Builders continue to rely on incentives and selective price adjustments, but inventories are better balanced and construction spending has leveled off. Affordability remains the principal obstacle, and it will likely remain so until borrowing costs decline further or wage growth firms.

Housing affordability remains stretched, which is keeping a low ceiling on home sales.

Overall, we see the economy entering a short 6–8 month lull, with growth averaging roughly 2% through spring. This softer patch should also ease some of the pressure that has built up on household budgets over the past two years. That pause should help recharge household balance sheets as grocery prices, fuel, and rents ease further.

Housing is already seeing a bounce, albeit off low levers, as builder discounts and rising existing-home inventories begin to restore affordability. With sales picking up, we expect inventories to normalize over the next few months, giving way to improving starts in the second half of 2026. Stronger home sales will also support demand for furniture, appliances, and other home-related goods.

Geopolitical risks remain present across multiple theaters. The UN-backed Gaza stabilization proposal continues to face significant obstacles, while intermittent escalation along the Israel–Hezbollah border remains a concern. Saudi Arabia’s normalization conditions—security guarantees, nuclear cooperation, and progress on the Palestinian track—signal long-term strategic alignment but short-term caution. The U.S. naval buildup near Venezuela suggests heightened tension even if financial markets have yet to price it in.

Risk repricing remains one headline away amid a flurry of major new developments.

The overarching narrative continues to evolve into the tension we highlighted in our Piedmont Perspective. Official data suggest a cycle that is slowing but intact. Markets see a credible path toward easing, and corporate investment signals cautious forward momentum. Yet for many households, the lived experience of the economy feels materially different from the aggregates. The divide echoes the contrast between The Wizard of Oz—optimistic, institutionally confident—and Wicked, which interrogates unequal realities and curated narratives.

Navigating the Cycle: A CFO’s Playbook

For finance executives, this environment argues for maintaining liquidity buffers, extending maturities selectively, and preserving optionality as the Federal Reserve navigates a shallow easing cycle. The modestly positive yield curve supports favorable laddering strategies. Softening sentiment and rising Challenger cuts suggest a cautious consumer in early 2026, reinforcing the need for disciplined working-capital management.

At the same time, firms with marketing scale and brand reach are capturing disproportionate wallet share. McDonald’s and Walmart continue widening their advantage through value-driven messaging, while Lowe’s is separating from peers in a slowing home-improvement market. This “marketing-heft dividend” underscores the value of brand investment, loyalty platforms, and customer analytics in an affordability-constrained environment. Treasury desks should also monitor commodity developments closely—particularly the Ukraine peace discussions—which are already influencing oil and grain curves.

Piedmont Perspective

We take pride in continuously analyzing every dimension of life—business, culture, sports, and geopolitics—through the lens of economics. This week, we turn our focus to the release of Wicked for Good, the second installment of the Wicked film series, inspired by the acclaimed Broadway production and early works.

Emerald Cities and Economic Narratives

Economic narratives have always carried political weight. Few cultural touchstones illuminate that better than The Wizard of Oz and its modern counter-story, Wicked. They share the same fictional landscape but reflect very different American moods—and they mirror the questions resurfacing today amid rising debts, monetary uncertainty, and geopolitical recalibration.

Baum’s 1900 novel emerged from a nation still defining itself after the Spanish-American War, the closing of the frontier, and the growing pains of an industrial republic. The fiercest policy conflict of the era revolved around money—specifically whether the country should maintain the gold standard or adopt a bimetallic system. Populists championed Free Silver as a way to ease deflation and reduce debt burdens; William Jennings Bryan’s “Cross of Gold” speech cast the stakes in moral—and unmistakably populist—terms. “You shall not crucify mankind upon a cross of gold,” he warned, arguing that monetary policy was not merely an economic mechanism but the fulcrum upon which fairness, opportunity, and national identity turned.

Baum encoded this debate into Oz with deliberate precision. Dorothy’s silver shoes (made ruby by Hollywood) walking the yellow-brick road depicted the competing visions of monetary orthodoxy. The Wicked Witch of the East symbolized eastern industrial-financial power; the Wicked Witch of the West represented western monopolies and the harsh economic realities of the frontier. The Good Witches stood in for reform movements challenging these regional forces. And the Wizard—charismatic, theatrical, ultimately exposed—embodied political and economic elites whose authority depended more on spectacle than insight.

Baum’s deeper argument was democratic: the Scarecrow, Tin Man, and Lion demonstrate that clear thinking, hard work, heart, and courage often reside in ordinary citizens rather than in the technocrats behind the curtain. The people of Oz represented the American public—farmers, workers, and small merchants navigating the real economy.

The 1939 Technicolor film softened the populist edge but preserved the essential message: institutions can be flawed, authority can be illusory, and resilience often comes from within. It was optimism forged in scarcity and anxiety, but optimism nonetheless.

A century later, Wicked turns that optimism inward and interrogates it. The America of Maguire’s novel had lived through Watergate, the Cold War’s end, globalization, and rising mistrust of institutions. In this retelling, the Wizard is not a harmless showman but an architect of narrative control. “Wickedness” becomes a label attached to dissent. And Elphaba—the so-called Wicked Witch—embodies the truth-tellers: whistleblowers, reformers, independent analysts, journalists, and skeptics who expose uncomfortable facts and disrupt carefully managed narratives. Her crime is not malevolence but refusing to participate in the institutional fiction.

Stories shape markets as much as actual data.

This prism aligns Wicked with a broad set of contemporary political forces—populist movements on the left and the right; anti-corruption and transparency advocates; civil-liberty and privacy groups; anti-monopoly coalitions; critics of surveillance and state secrecy; and reformers who warn that narrative control is now a central tool of political power. They share a common belief: the official story is not the whole story.

That contrast—Baum’s confidence in citizen agency versus Maguire’s skepticism toward institutional motives—resonates sharply today. The economy is wrestling with record debts, widening fiscal imbalances, uneven mobility, and renewed debates over the nature of money. Polarization now functions as a currency of its own, and the powers that be—across both political camps—deploy it to shape narratives, mobilize supporters, and pressure institutions.

The echoes of silver-vs-gold appear in arguments over digital currencies, Federal Reserve independence, and whether the United States can sustain monetary primacy amid geopolitical fragmentation. The public is once again asking Baum’s essential questions: How durable is the system? Do the experts truly know what they’re doing? And what happens when confidence in the narrative begins to crack?

Both Oz stories converge on a single lesson: power rests on controlling the narrative. Baum argued that ordinary Americans possessed more agency than they knew. Wicked warns that institutions can—and often do—shape stories to protect their own fragility. Today’s monetary debate—deficits, the dollar’s role, digital alternatives—sits squarely between those worldviews.

In every era, there is always someone behind the curtain.

Those navigating the cycle can follow the yellow-brick road, but—as Baum implied—they should never lose sight of whoever is pulling the strings behind the curtain.

The Week Ahead: November 24-28

Next week will bring a full set of economic releases, as the government agencies continue to catch up from the government shutdown.

Tuesday, November 24

Will bring reports on September Retal Sales, as well as the September Case-Shiller Home Price Indices. We will also get the Business Inventories for August, Pending Home Sales for October and the November Consumer Confidence Index. The retail sales data and Consumer Confidence data will likely garner the most attention, as they will provide insight into how much momentum the economy had at the end of the quarter and a look into consumers’ minds just ahead of the holiday shopping season. We look for a solid increase in retail sales and a modest dip in Consumer Confidence, reflecting the growing number of layoff announcements.

Wednesday, November 25

We will get our first look at third quarter real GDP. We are projecting 3.7% growth for the quarter but this past week’s trade data, which showed a narrower goods deficit, raises the risk of an upside surprise. The Commerce Department will also report personal income and consumer spending, which will also provide some updated price information.

A Stronger GDP report may fan fears that the Fed will take a pass at cutting rates in December. We do not think they will. What little data we have for the fourth quarter suggests the economy lost considerable momentum and that the drag was accelerating just before the government shutdown ended. The call on the field is a quarter point cut. The Fed will need to see overwhelming evidence to overturn that call.

Thursday, November 26

Thanksgiving Day!

Friday, November 27

The Chicago PMI for November is on the only variable on deck. The report may show some modest improvement. The markets will also likely be on the lookout for early signs of the strength of retail sales at the official start of the holiday shopping season, paying close attention to real time tracking measure and credit card data.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

November 21, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000