Retail Sales Hit a Flat Spot…

- Retail sales rose 0.2%, softer than expectations and essentially flat given the Census Bureau’s ±0.4% confidence interval.

- August’s +0.6% gain was unrevised, preserving a strong summer handoff.

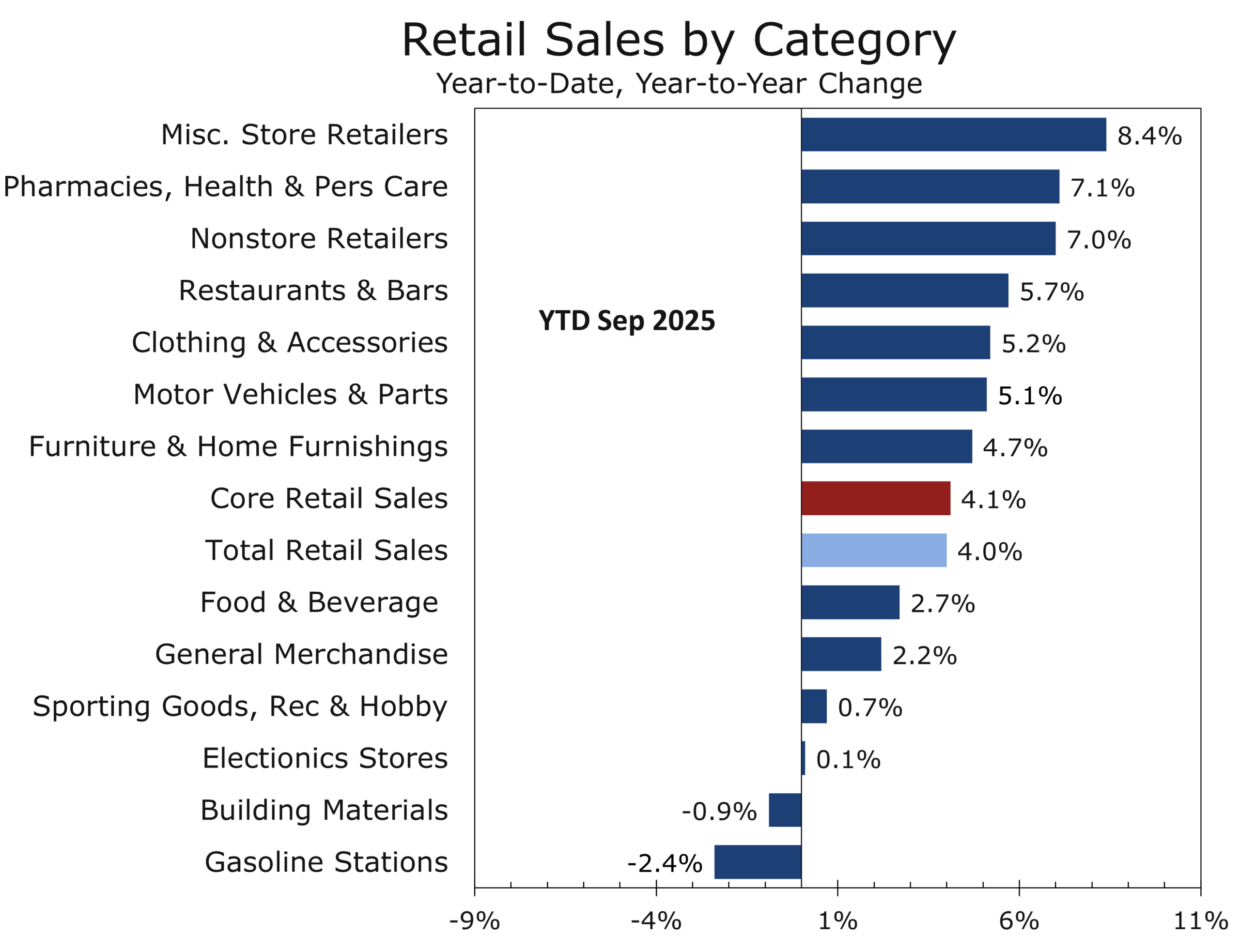

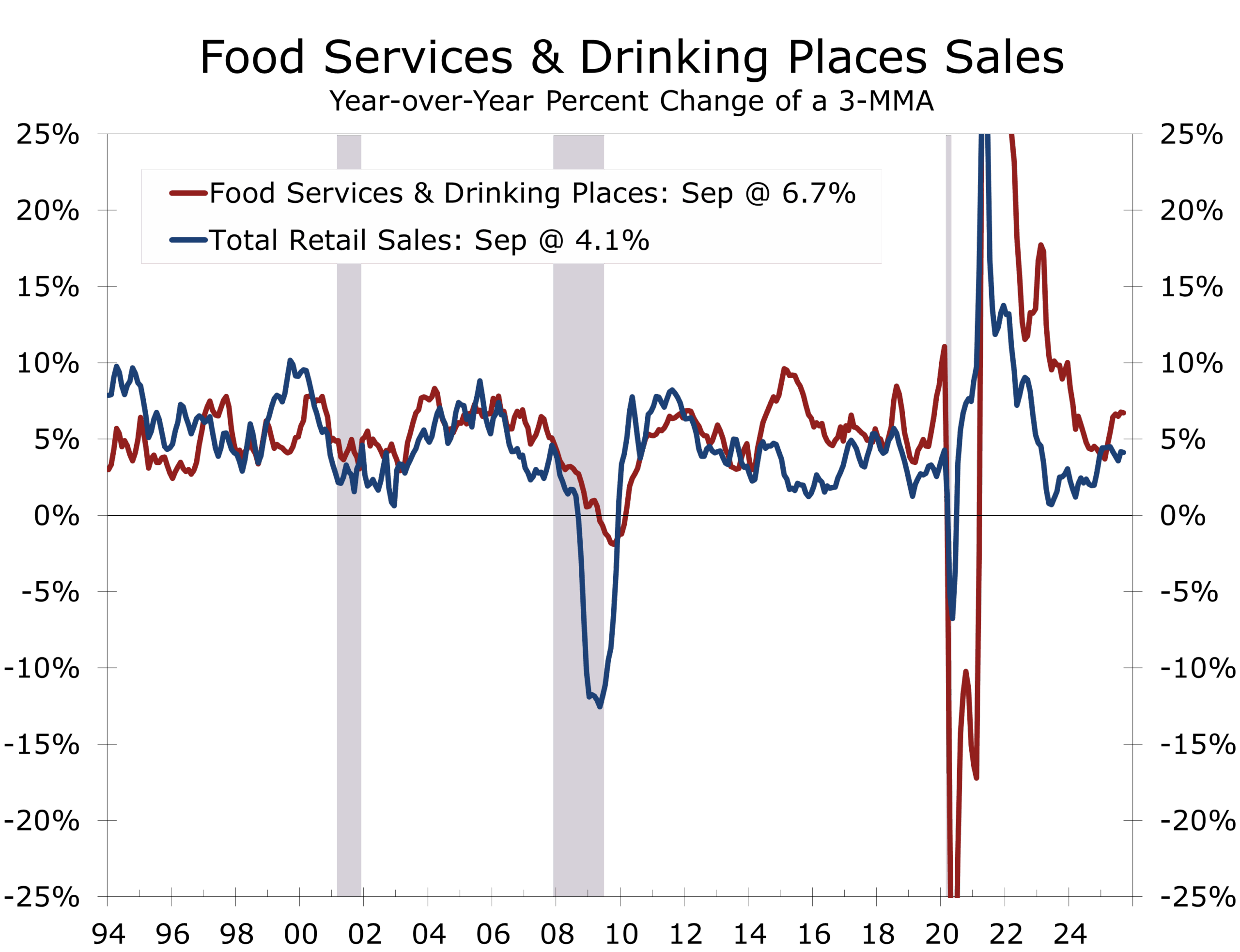

- Year-over-year sales increased 4.3%, led by nonstore retail (+6.0%) and food services (+6.7%).

- September’s sectoral shifts showed goods categories cooling while service-oriented and necessity-driven categories strengthened.

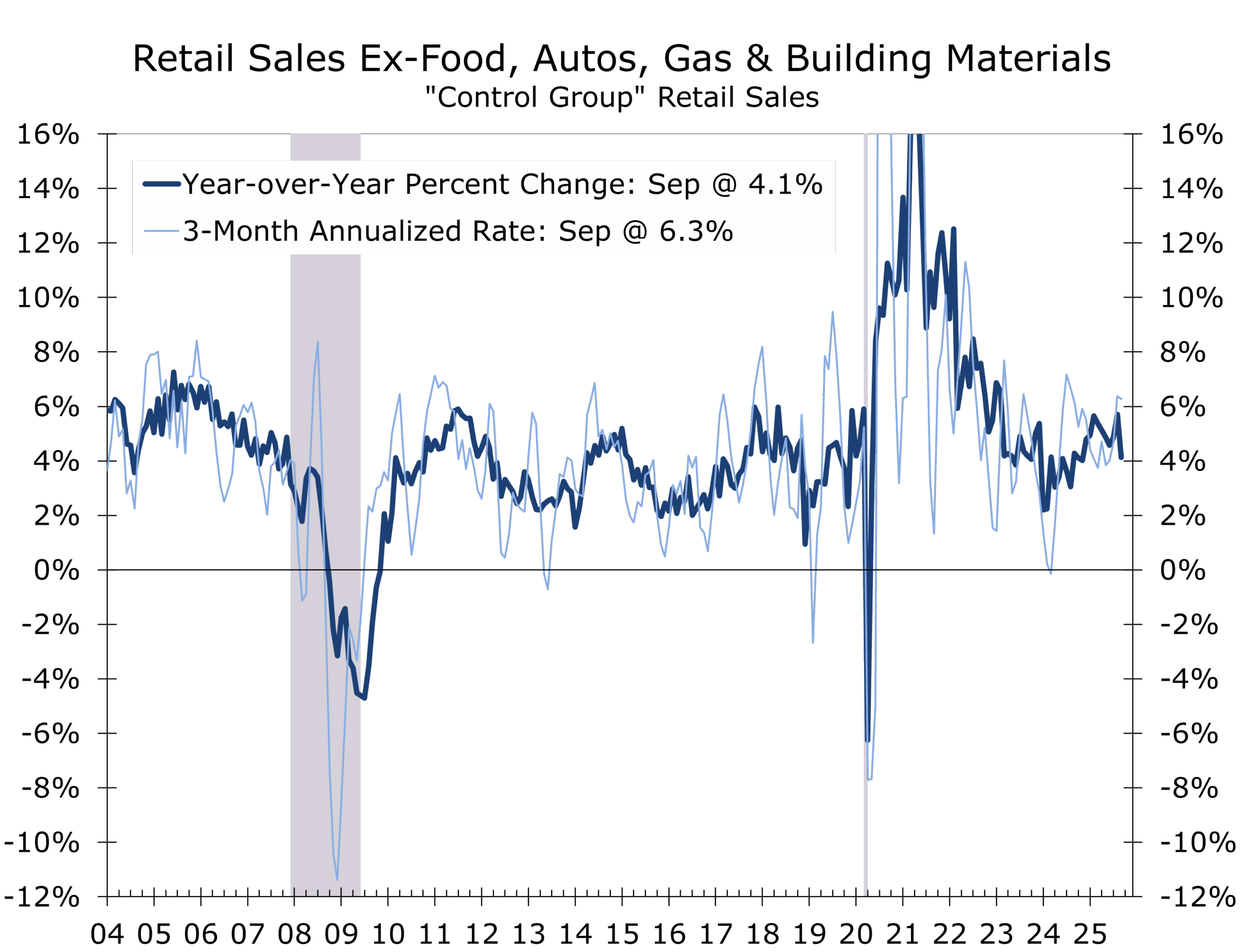

- Control-group sales fell 0.1%, but still rose 6.1% annual rate during Q3

- The unwind of summer EV-driven auto demand began earlier than expected. The EV tax credit expired at the end of September, suggesting supply constraints or early pull-forward effects were behind the drop.

- Nonstore sales’ 0.7% decline may stem partly from seasonal adjustment issues tied to unusually large August online promotions that seasonal factors failed to fully capture.

- The K-shaped consumer remains firmly in place: high-income households continue to spend, while middle- and lower-income households face rising costs for key necessities, weaker job fundamentals and tighter credit.

- Slower retail momentum adds fuel to the growing calls for a December rate cut, particularly as a cooling labor market is now clearly exerting pressure on discretionary categories.

- Despite September’s softness, holiday spending remains on track for its strongest growth since 2021, supported by wealth effects and high-income resilience. We are looking are looking for holiday retail sales to rise 4.5% this year

…As Momentum Rolls into Services

U.S. retail sales rose 0.2% in September, undershooting expectations and marking a meaningful slowdown after a stronger summer. The gain sits entirely inside the Census Bureau’s ±0.4% confidence interval, effectively yielding a flat print.

The report—delayed by the 43-day federal shutdown—follows July and August strength that was amplified by a rush to purchase electric vehicles ahead of the expiring federal tax credit. Curiously, motor vehicle sales softened 0.3% in September even though the credit expired at month-end, suggesting that the strongest models were depleted ahead of the deadline and that the pull-forward was more front-loaded than usual.

September’s soft headline gain masks a shift away from goods to steadier service spending.

The defining feature of September’s report is the sectoral rotation that is becoming more pronounced as the cycle matures. Goods categories that surged earlier in Q3 softened across the board: electronics (–0.5%), clothing (–0.7%), sporting goods (–2.5%), and nonstore retail (–0.7%). Yet all remain positive year-over-year, indicating that part of the decline reflects payback for prior strength rather than an outright deterioration. The weakness in nonstore sales was likely amplified by residual seasonality created when a wider group of online retailers aligned their promotions with Amazon’s expanded Prime Day—an effect not yet fully reflected in seasonal-adjustment factors.

In contrast, service-oriented and necessity-based categories showed ongoing strength. Food services (restaurants and bars) rose 0.7%, health & personal care 1.1%, and miscellaneous retailers 2.9%. Gasoline station sales rose 2.0%, though they remain negative on a year-over-year basis due to lower fuel prices. This rotation away from discretionary goods and toward services and necessities mirrors classic late-cycle behavior, with households becoming more selective but still engaged.

Momentum indicators reinforce this shift, with most retail categories posting softer readings in September. Nonstore retail shows the same pattern: weak sequential momentum despite a 6.0% year-over-year gain. Food services continues to be the most dependable pillar of the consumer, maintaining three-month momentum near 6.2% and 6.7% year-over-year growth.

Control-group softness adds mild downside risk to early Q4 GDP tracking

The weakness in control-group sales, which fell 0.1%, introduces nuance without changing the underlying Q3 story. Core retail sales, which provide a good approximation of the goods portion of personal consumption expenditure, rose at a 6.3% annual rate during the third quarter.

.

Personal spending is tracking a 0.4% nominal gain for the month and a real increase of close to 0.2%, consistent with real consumer spending rising at around a 3.2% annualized in Q3. That aligns closely with our own Q3 real GDP tracking at 3.7%.

Slowing retail momentum increases pressure on the Fed to consider a December rate cut

The larger question now is how sharply spending slows in Q4. The answer increasingly hinges on the labor market. Unemployment has risen to 4.4%, the highest in four years, and hiring has become narrower and more uneven across industries. These dynamics are now showing up in September’s discretionary categories. More broadly, they strengthen the argument—already building in markets—that the Fed should consider an insurance cut in December. While Fed officials have centered their concerns on the labor market, the September retail data show that a cooling job market is clearly pressuring spending at the margin. The marginal deceleration visible in goods categories dovetails with market volatility, softer sentiment, and the increasingly bifurcated consumer landscape.

September’s weaker motor vehicle sales suggest they pullback in October will be less than had been expected. We are looking for real consumer spending to slow to a 1.7% annualized rate in Q4. That said, underlying demand heading into the holiday season remains healthier than September’s headline number suggests. High-frequency indicators continue to look solid, and strong household wealth gains—especially among older and higher-income households—are expected to support a 4.5% year-to-year rise in holiday-related spending this year.

Spending at restaurants and bars remains a notable bright spot, with sales up 6.7% year-over-year, reinforcing that higher-income households are still spending freely on discretionary services even as goods categories cool. This strength, however, masks a widening performance gap across the industry. Many chains, particularly those marketing to middle income households, have reported sluggish traffic and tightening margins, squeezed by higher food and labor costs that remain difficult to fully pass through. Larger national brands—with established marketing platforms, stronger digital engagement, and the scale to offer targeted value—are outperforming smaller operators. September’s results fit this pattern: demand at the upper end remains healthy, but the pressure on operating margins underscores how uneven and income-dependent service-sector momentum has become at this stage of the cycle.

Overall, the September retail sales report points to normalization rather than deterioration: a resilient but increasingly selective consumer navigating a cooling labor market, shifting incentives, and tighter financial conditions. Momentum is easing, the ceiling is lower, and the floor—while still firm—is clearly thinning as the cycle matures. The government will release its full estimate of Q3 GDP on December 23. September’s figures set the tone for Q4 and remain consistent with our early call for a slowdown toward the 1.7% range.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

November 25, 2025

Mark Vitner, Chief Economist

(704) 458-4000