THE CAVU COMPASS | Monthly macroeconomic insights and market commentary by CAVU Securities and Piedmont Crescent Capital

THE CAVU COMPASS

Monthly macroeconomic insights and market commentary provided by CAVU Securities and Piedmont Crescent Capital.

Mark P. Vitner, Chief Economist

Ceasefire at the Brink: IRGC Strikes Back, April 22 Deadline Looms

April 19, 2026

The IRGC Reversed Course. The April 22 Deadline Is Now the Only Thing That Matters.

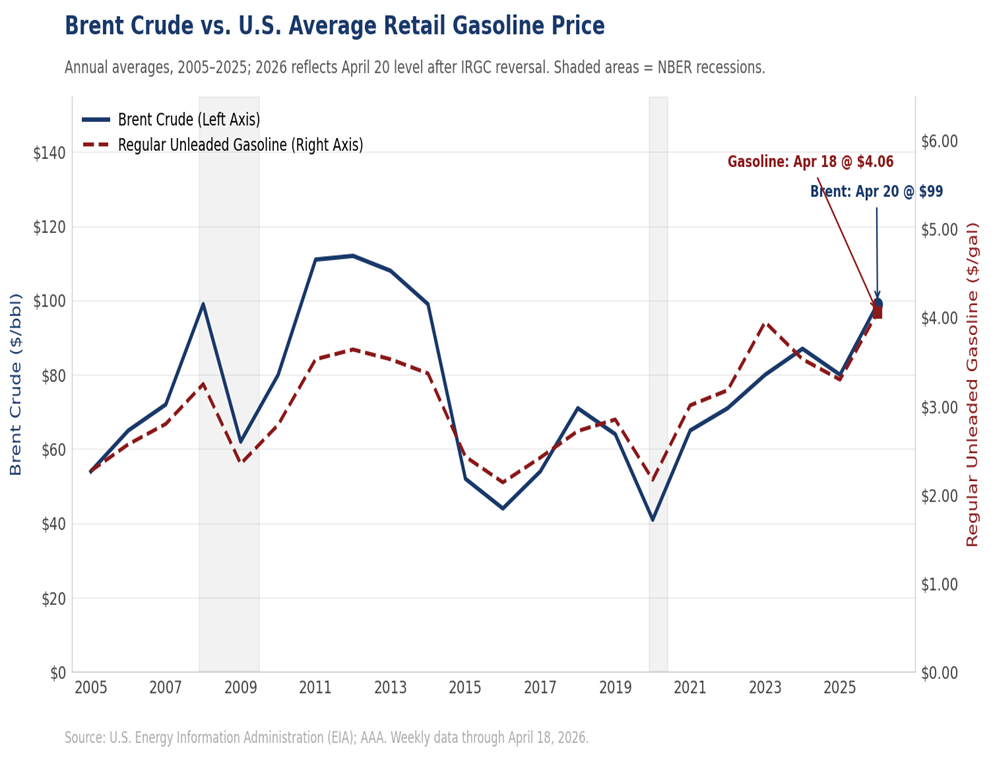

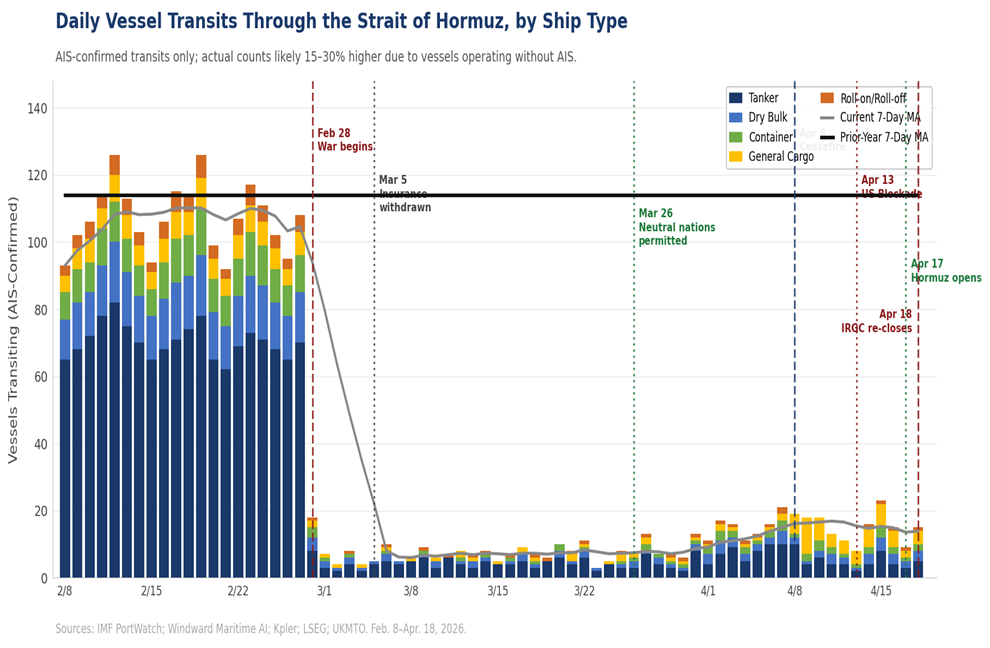

- The IRGC has reversed the Hormuz opening and attacked commercial shipping. Within hours of Iran's Friday declaration that the Strait was "completely open," the IRGC reversed course Saturday morning. Iranian gunboats fired on vessels attempting to transit — at least one tanker, the VLCC Sanmar Herald, was fired upon despite receiving prior clearance to pass. A U.S. defense official confirmed at least three IRGC attacks on commercial ships. The UKMTO reported two attacks. Brent crude surged back toward $99–100. The 24-hour window from Hormuz opening to Hormuz re-closure is the most dangerous sequence in the conflict since the April 8 ceasefire began.

- The U.S. port blockade remains in full force. President Trump, while welcoming Iran's Hormuz announcement, immediately posted on Truth Social that the naval blockade of Iranian ports "will remain in full force and effect as it pertains to Iran, only, until such time as our transaction with Iran is 100% complete." Negotiations "should go very quickly," he said. This is the correct posture: use Iran's concession as leverage to close a permanent deal, not a reason to stand down.

- This is a negotiating ploy, not a strategic reversal — but ploys have consequences. The IRGC's logic is reconstructable: Iran opened the Strait as a goodwill gesture tied to the Israel-Lebanon ceasefire; Washington immediately declared the port blockade would stay regardless; IRGC hardliners concluded Iran conceded too much and restored leverage by reversing. This is almost certainly tactical, not a decision to re-enter full hostilities. But Iranian gunboats have fired on commercial ships carrying prior clearance. That creates facts on the water that matter independently of intent.

- The April 22 ceasefire deadline is now the fulcrum. Pakistani mediators are working urgently on a second round of talks. Both sides have given "in principle" agreement to extend the ceasefire for at least two more weeks, per AP sources, but that signal predates the IRGC's Saturday reversal. Whether the extension holds now depends on whether Pezeshkian's civilian government or Vahidi's IRGC has the decisive voice in Tehran this week.

- The Fed is on hold, and it is not going to hike. FOMC minutes confirmed that almost all participants view current policy as well-positioned. With unemployment heading toward 4.6% and PCE toward 3.1%, the committee is not looking for reasons to tighten. We still see room for at least one quarter-point cut during the second half of the year, most likely in late summer, well ahead of the midterm elections.

- The global recession threshold is closer than the IMF is letting on. The IMF cut their 2026 global economic forecast to just 3.1%, just above the threshold that marks a global downturn. Many large forecasting shops have forecasts closer to 2.5%. Our own is slightly higher, at 2.8%. Our forecast for U.S. growth remains well above consensus.

- Housing has missed its spring season. NAHB homebuilder sentiment fell to 34 in April, lowest since September. Completed unsold inventory is back to Great Recession levels. Spring is typically the difference between a good year and a bad one in housing. This one is largely gone.

- Our scenario probabilities, revised for the IRGC reversal. Base Case (45%, down from 55%): ceasefire extension and second-round talks materialize; Brent stabilizes $85–$100. Downside (35%, up from 30%): ceasefire lapses April 22, Brent re-accelerates toward $115–$130, consumer spending enters genuine contraction. Tail Risk (20%, up from 15%): IRGC actions against U.S. naval assets trigger immediate U.S. military response; oil above $140; global recession risk surges.

Market Snapshot

| Indicator | Level | Context |

|---|---|---|

| Brent Crude | ~$97–100 / bbl | Surged back toward $100 after IRGC reversed Hormuz opening Saturday; erased most of Friday's relief |

| WTI Crude | ~$93–96 / bbl | Recovered most of Friday's decline after IRGC gunboat attacks Saturday; physical markets remain extremely tight |

| 10-Yr Treasury | 4.25–4.30% | Drifted down from 4.35% peak; bond market pricing limited near-term resolution |

| 2-Yr Treasury | ~3.82% | Curve +43–50 bps (2s10s); modest steepening on growth fears |

| Natl Avg Gasoline | $4.16 / gal | ↑ from $3.41 pre-war; $10.4B weekly drain on consumer budgets |

| Natl Avg Diesel | $5.67 / gal | ↑ sharply; record territory; freight cost surge is now embedded |

| Gold | ~$4,760 / oz | Safe-haven premium holds; clearest market signal of persistent risk |

| Fed Funds Target | 3.50–3.75% | On hold; PCC still sees room for one to two quarter-point cuts in the second half |

| UMich Sentiment | 47.6 (Apr prelim) | Record low; 1-yr inflation expectations 4.8%; long-run 3.4% |

| NAHB Sentiment | 34 (April) | Lowest since September; spring selling season effectively lost |

| Retail Sales (Mar) | Delayed to Apr 21 | Census Bureau delay; cleanest read on discretionary spending still pending |

| Industrial Production | −0.5% (Mar) | Third consecutive monthly decline; manufacturing down 0.1% |

| Initial Jobless Claims | 207–210k | Labor market holding; no sign yet of energy shock reaching payrolls |

| Empire State Mfg | Modestly negative | Early April snapshot; new orders and shipments declined |

| Philly Fed Mfg | 26.7 (April) | Surged well above expectations of 10.0; new orders and shipments hit multi-year highs; employment fell |

| S&P 500 | +4.8% for week | Risk-on surge on Hormuz news; Nasdaq +6.8%, DJIA +3.5%; all-time high intraday |

| Corp Bond Issuance | ~$100bn this week | Massive risk-on signal; banks led with BofA, JPM, Morgan Stanley each pricing $10bn deals |

"Iran's 'leadership' blinked on the Strait. The war is not over. But the arithmetic just shifted decisively in Washington's favor, which the IRGC does not like."

— Mark P. Vitner, Chief Economist, Piedmont Crescent Capital

The Consumer: From Sentiment to Behavior

March Retail Sales land April 21 — the day before the ceasefire expires — making the timing of this data release unusually consequential. We expect control group retail sales (ex-autos, gas, building materials) to rise +0.3%, driven by the generous 2025 tax refund season, with average refunds running more than 10% above year-ago levels. The headline figure will be misleadingly strong, perhaps +1.3% to +1.5%, because gasoline prices inflated the gas-station line item. The number to watch is the control group. A reading above +0.3% means the consumer was holding in March despite the energy shock; below +0.2% signals the energy drain was already overwhelming underlying spending before the IRGC reversal raised the risk of another oil price surge. Bank of America's internal card data for March showed per-household spending up 4.3% year-over-year, with discretionary categories ex-gas still growing at 3.6% YoY. April will be a harder test. Gasoline prices have fallen modestly in April, however, which may provide some modest relief to consumers' psyche and wallets. The cleanest measure of consumer health is hours away.

Consumers do not need to see a monthly spending report to know something has changed. They feel it at the pump. At $4.16 a gallon for gasoline and $5.67 for diesel, the $10.4 billion weekly income transfer from household budgets to the energy sector is large enough to matter in the aggregate. It does not cycle back into the consumer economy. It goes to refiners, producers, and governments. The personal saving rate was 4.0% heading into the conflict, well below the post-pandemic average. Middle- and lower-income households, who were already running lean, are most exposed.

Since peaking in early April, U.S. gasoline prices have fallen slightly. The national average climbed as high as $4.16 per gallon the week of April 9 — the highest level since August 2022 — before easing to $4.09 on April 16 and $4.06 as of April 18, according to AAA data. That represents a decline of roughly 7 to 10 cents from the recent high. Even so, the national average remains more than $1.00 higher than a month ago and roughly 30% above year-ago levels, keeping the energy shock's drag on real disposable income intact.

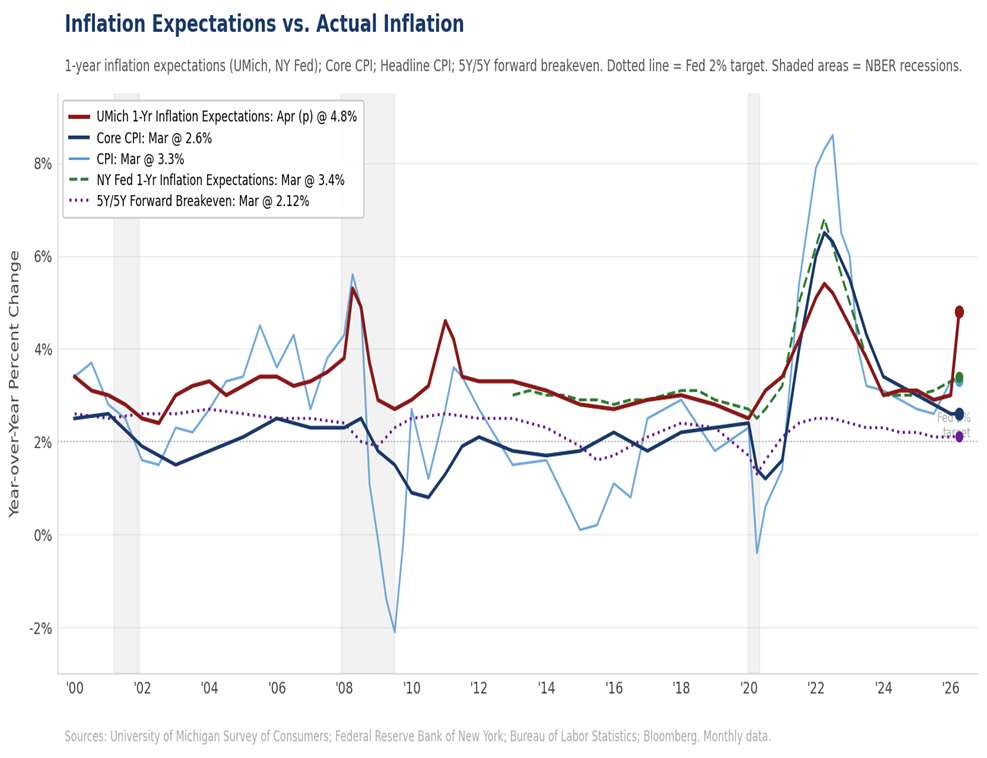

Higher gasoline prices are clearly weighing on consumer confidence. The University of Michigan preliminary April Consumer Sentiment reading of 47.6 is consistent with recent headlines from retailers, small business owners and homebuilders. One-year inflation expectations have jumped to 4.8%, the highest since 2023. Long-run expectations have moved to 3.4%, territory not seen since 2008. The Fed's entire justification for tolerating an energy-driven headline spike without tightening policy rests on the assumption that long-run expectations stay anchored near 2%. At 3.4%, that assumption is under genuine stress. That said, the Fed gives far more credence to more stable measures — the 5-year forward breakeven rate and the New York Fed consumer survey — both of which show medium- and long-term expectations remain anchored.

Risk Factor

The Savings Rate Cannot Absorb Another Month of This

The personal saving rate was 4.0% entering the conflict, well below the post-pandemic average. The roughly 40% jump in gasoline prices from pre-war levels has already begun to offset the benefit from sizable individual tax refunds flowing from last year's tax legislation. Within weeks, the pump-price drag will likely more than offset that tailwind. Without a meaningful retreat in energy prices, the path for consumer spending in Q2 leads to something worse than a slowdown.

The Beige Book: A Ground-Level Portrait of the Shock

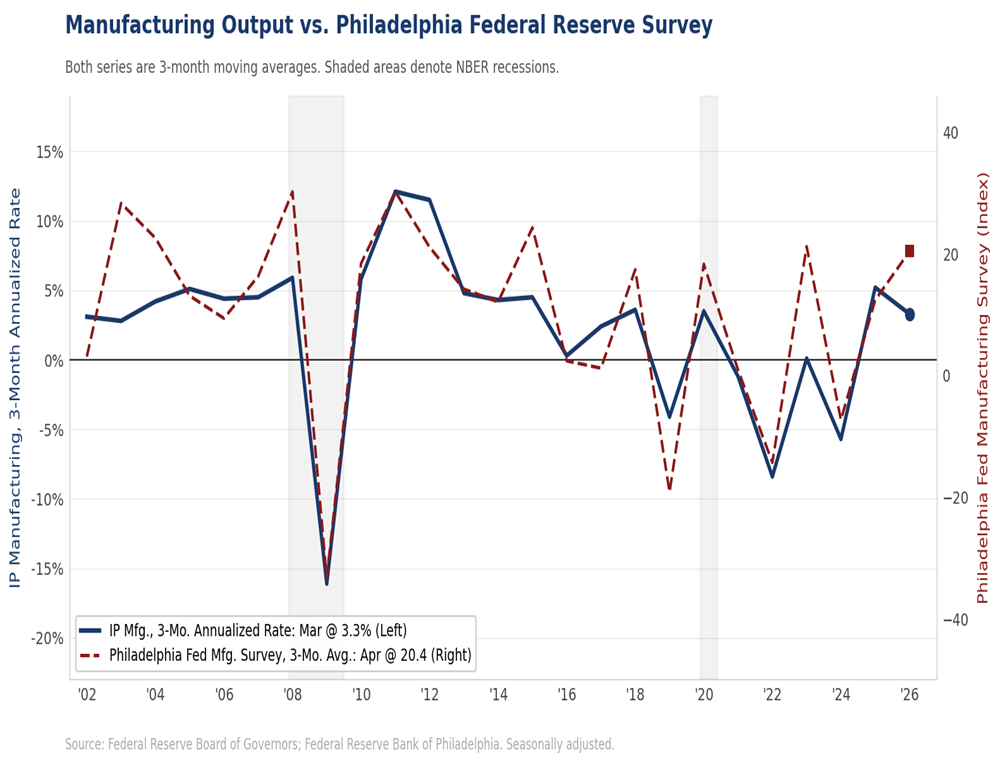

The Federal Reserve's April Beige Book, released Wednesday, April 15, described slight-to-moderate growth across most districts but with a wait-and-see posture that has become increasingly pronounced since the blockade took effect. All twelve districts reported the same basic pressures: energy and freight costs up, discretionary consumer spending softer, businesses pulling back on hiring and capital projects, and uncertainty rising. Against that backdrop, the Philly Fed manufacturing survey for April was a genuine positive surprise: the headline index surged to 26.7, well above the consensus of 10.0 and the prior reading of 18.1. New orders jumped 24 points to 33.0, and shipments rose nearly 12 points to 34.0 — both at their strongest readings since 2021 and 2022, respectively. Employment fell. The takeaway: production and orders are holding, but firms are not adding headcount, and the cost picture is worsening. Initial jobless claims fell 11,000 to 207,000 for the week ended April 11, consistent with our view that oil price shocks affect employment with a two-to-three quarter lag.

Transportation and logistics contacts in Dallas, Kansas City, and Chicago reported fuel surcharges near pre-pandemic highs. Food producers in Atlanta and Richmond flagged diesel and fertilizer as their primary cost pressures. Retailers in New York and Boston reported weaker foot traffic and softer card spending since the blockade. The breadth is the notable part. This is not a sector-specific problem or a regional one.

The Beige Book also documented an income split that is becoming more pronounced. Higher-income households in New York, San Francisco, and Boston continue to spend, supported by equity-market wealth effects. Middle- and lower-income households in Kansas City, Dallas, and Atlanta are pulling back. Gasoline prices consume a proportionally larger share of lower-income budgets, and those households had less savings to draw on at the outset.

Key Signal

The Bond Market Remains the Definitive Signal

Treasury yields fell 3 to 12 basis points through Friday on the Hormuz opening announcement, with the 10-year briefly breaking below 4.25% and the 2-year trading near 3.65 to 3.69%. Corporate issuance surged to approximately $100 billion for the week — the largest of the year — and spreads had tightened to pre-war levels. Then the IRGC reversed the Hormuz opening Saturday and Brent surged back toward $99–100. Watch the April 21 close: yields holding above 4.30% signal the bond market is pricing a ceasefire lapse. A fall back below 4.20% would signal the market believes a last-minute extension is coming. Until a deal is formally signed and the blockade visibly unwinding, financial conditions remain tighter than equities are pricing.

Breaking: Hormuz Declared Open — What It Means and What It Doesn't

The situation has moved sharply in the past 72 hours. Iran's Friday announcement that the Strait of Hormuz was "completely open" for commercial traffic produced a genuine, if brief, de-escalation. Markets priced it immediately: oil fell toward the high-$80s, equities surged, corporate spreads tightened to pre-war levels. More than a dozen commercial vessels actually transited — the most traffic since February 28. Then, early Saturday, the IRGC reversed course. Iran's joint military command declared that "control of the Strait of Hormuz has returned to its previous state." Iranian gunboats fired on at least one tanker that had received prior clearance to pass — the VLCC Sanmar Herald — and at least two additional attacks on commercial vessels were confirmed by both the UKMTO and a U.S. defense official. The 24-hour window from opening to re-closure is the most dangerous sequence in the conflict since the ceasefire began.

What the IRGC's reversal reveals about Iran's internal politics matters as much as the tactical situation it creates. Iran International has documented a widening rupture between President Pezeshkian's civilian government and IRGC hardliners. The Soufan Center has described the negotiating dynamic at Islamabad as reflecting a structural power struggle between Vahidi's IRGC hardliners and the more pragmatic officials aligned with Pezeshkian. Critically, the Stimson Center's Kaitlyn Hashem has documented how Israel's assassination campaign against IRGC leadership has had an ironic consequence: it elevated a generation of hardliners pulled from semi-retirement who are "more hardline, anti-U.S., and anti-Israel than those they replaced" and "less nimble in negotiating an end to the war." These are not pragmatists who got outmaneuvered — they are the hardliners themselves.

The IRGC's logic is straightforward: Iran opened the Strait Friday as a goodwill gesture tied to the Israel-Lebanon ceasefire. Washington immediately declared the port blockade would remain regardless. IRGC hardliners concluded the U.S. was banking the concession without offering anything in return — and reversed course to restore leverage. But 'almost certainly a negotiating ploy' and 'therefore risk-free' are not the same thing. Iranian gunboats have fired on tankers carrying prior clearance. A misjudgment, or a single incident involving an allied-nation vessel, could trigger a response that neither the IRGC's civilian handlers nor Washington's diplomats can contain in real time.

The U.S. port blockade, which CENTCOM says has completely halted Iran's seaborne trade and costs Tehran an estimated $400 million per day, remains fully in force. Iran has now conceded the central demand (Hormuz access) without getting what it wants in return. That puts Washington in a stronger position for the next round of talks. The port blockade, now in its seventh day, has completely shut off Iran's seaborne trade, which powers roughly 90% of its economy. Iran's onshore oil storage was already approaching saturation before Friday's Hormuz declaration. Iran had a closing window in which to act and opened the Strait Friday — then the IRGC reversed that decision within 24 hours, trading a genuine concession for a negotiating ploy.

The diplomatic picture as of Sunday, April 19: Pakistani mediators are working urgently. AP sources report both sides gave an 'in principle' agreement to extend the ceasefire for at least two weeks, though that signal predates Saturday's IRGC reversal. The nuclear impasse at Islamabad remains: the U.S. proposed a 20-year enrichment suspension; Iran countered with five years, which Washington rejected. Iran's economy, per Pezeshkian's own assessment on March 28, cannot withstand more than three to four weeks of current conditions without risk of collapse.

If the ceasefire lapses on April 22, Washington's response will be swift. Our assessment: the most likely military response scenario does not deepen the conflict into full-scale war. It does push oil back above $110, widen credit spreads 75 to 125 basis points, and set back any ceasefire extension by at least two weeks. We expect Brent crude to average around $100 per barrel through the middle of this year, with a potential peak near $120 should the April 22 ceasefire expire. For the United States, we see only a 0.5 percentage point addition to headline inflation and a roughly 0.5 percentage point subtraction from GDP growth. U.S. growth remains capital-driven, powered by the ongoing AI buildout, Boeing's ramp-up in aerospace assemblies, the GLP-1 pharmaceutical and life-sciences boom, elevated defense spending, and continued reshoring activity. These structural tailwinds leave the U.S. better insulated than Europe or Asia.

Geopolitical Framework

| Scenario | Probability | Macro & Market Implications | Corporate Finance Action |

|---|---|---|---|

| Base Case | 45% ↓ from 55% | Framework agreement before or shortly after April 22. Mine-clearing begins under IMO coordination. Ceasefire formally extended. Brent falls toward $75–$95 as supply-risk premium compresses. Consumer spending stabilizes in Q2, recovers in H2. Economic damage from the seven-week shock is real but bounded. | If a deal closes quickly, the fixed-rate issuance window reopens. Monitor Brent: a sustained move below $85 changes the cost-of-capital calculus materially. Hold liquidity buffers in place until a formal agreement is signed. Do not unwind hedges. |

| Downside | 35% ↑ from 30% | Ceasefire lapses April 22 with no extension. IRGC hardliners retain control. Hormuz remains effectively closed. Brent re-accelerates toward $115–$130. Consumer spending enters genuine contraction. Fed policy becomes nearly impossible to calibrate. Credit spreads +75–125 bps. | Accelerate fixed-rate issuance ahead of wider spreads. Model demand destruction in revenue forecasts. Limit new floating-rate exposure. Review covenant headroom urgently. |

| Tail Risk | 20% ↑ from 15% | Iranian military retaliation against U.S. naval assets or Gulf port infrastructure. Oil $140+. Global recession risk surges. Dollar surges; EM stress. Possible Chinese air-defense weapons delivery to Iran adds great-power dimension. Fed caught between 5%+ inflation and recession. | Maximize liquidity immediately. Draw revolvers preemptively. Halt discretionary capex. Model severe demand contraction. Accelerate supply-chain diversification away from Gulf-dependent inputs. |

Inflation & Monetary Policy: A Stagflationary Bind

The March CPI and PPI together confirm that the energy shock is now embedded in the producer pipeline, not merely at the consumer level. Final Demand PPI rose 4.0% year-over-year, the hottest reading since February 2023. Goods prices jumped 1.6% month-over-month on energy; services prices were flat. Margins are being squeezed, not prices being passed through broadly. Small businesses are absorbing the cost hit rather than raising prices, which is exactly what the NFIB data shows: net profits dropped 11 points in March, and NFIB Chief Economist Bill Dunkelberg pointed directly at the oil price spike as the cause.

March CPI rose 0.9% for the month, with the 3.3% year-over-year reading driven almost entirely by the 21.2% surge in gasoline prices. Our year-end 2026 headline PCE forecast of 3.1% and core PCE forecast of 2.5% reflect the pass-through of energy costs into goods prices and, eventually, services. We expect PCE to peak near 3.5% year-over-year in April before energy base effects begin pulling it lower in the second half. Consumer inflation expectations have moved sharply across multiple surveys: UMich 1-year expectations rose to 4.8%, the New York Fed survey moved up 0.4 points to 3.4%, and the Conference Board survey rose 0.7 points to 6.2%. Our view is that the unemployment channel wins: the demand destruction from sustained energy prices is more likely to force the Fed's hand than the inflation pass-through.

Gasoline prices have declined modestly since peaking in early April, which may slow or even partially reverse the rise in inflation expectations. The impact on the April CPI could be even more dramatic, as gasoline prices typically rise in April as driving increases for springtime activities.

PCC's view has not changed. The Fed will not hike. The current shock is narrower than 2021 to 2022, the labor market is in better balance, and the funds rate already sits 50 to 75 basis points above the FOMC's own median neutral estimate. We continue to see room for one or two quarter-point cuts in the second half of the year, most likely beginning in late summer, with a possible second cut after the midterm elections. The Senate Banking Committee holds a confirmation hearing for Kevin Warsh next week, which may provide early signals on the next Fed Chair's views on monetary policy and central bank independence. The more consequential test of Fed independence is the ongoing Supreme Court case over the White House's attempt to remove Governor Lisa Cook.

Key Signal

This Is Not Yet a Generalized Inflation Breakout

Core CPI at 2.6% and flat PPI services prices tell us the energy shock has not yet run into wages or broad services costs. Small businesses are absorbing the hit through lower margins. Second-round inflation effects should be smaller than in 2022, given looser labor markets and more financially stretched lower-income households. The April CPI release will be the next meaningful test. If core clears 2.8% year-over-year, the argument for rate cuts this year becomes very hard to sustain.

Housing & Capital Investment: War Casualties in the Spring Season

The NAHB homebuilder sentiment index fell four points to 34 in April, its lowest reading since September and well below the consensus of 37. Every component was down: current sales, expected sales six months out, and buyer traffic. Builders cited higher energy-related material costs (diesel especially), higher mortgage rates, and buyers who are simply not showing up. The share offering incentives fell from 64% to 60%. Margins are already too thin for builders to give anything more away.

The Census Bureau's housing data lag the conflict by six to eight weeks. Housing starts for February and March will be released April 29; new home sales on May 5. Spring accounts for a disproportionate share of annual builder volume. This spring is largely gone. Completed but unsold inventory, which had been rising steadily since mid-2025, was at its highest level since the post-financial crisis period as of January. It will go higher.

Capital investment is the most bifurcated sector in the economy right now. AI-linked infrastructure, semiconductor manufacturing, aerospace, defense-tech, and advanced manufacturing reshoring are holding up well. On the other side, projects tied to supply-chain normalization are being staged and delayed, particularly those dependent on Gulf commodity inputs: nitrogen fertilizer, sulfur, and naphtha. AI investment alone is likely to contribute close to half a percentage point to U.S. GDP growth this year, providing a meaningful structural offset to the energy drag.

The Global Picture: Downgrade Cascade

The global growth outlook has deteriorated sharply. Our own forecast puts world GDP growth at roughly 2.8% for 2026 on a dollar-weighted basis. The U.S. at 2.5% (2.7% Q4/Q4 basis) is well above consensus; the Eurozone and UK are tracking closer to 0.7% and 0.3%, respectively. The IMF has already cut Germany's 2026 growth outlook to 0.8% and the Eurozone to 1.1%. The Gulf Cooperation Council faces a GDP contraction of roughly 8% relative to the pre-war baseline. The only economies avoiding meaningful downgrades are China, India, and a narrow group of commodity exporters.

The Eurozone faces a particularly acute version of the same stagflationary squeeze. Eurozone headline CPI was revised up to 2.55% year-over-year in March, with core at 2.29%. A notable development in Europe this week: Hungary's opposition Tisza party won a decisive parliamentary victory, ending Viktor Orbán's 16-year rule. The change in government is immediately positive for EU-Hungary relations and potentially unlocks the vetoed 90 billion euro loan to Ukraine.

China's direct exposure to the Hormuz disruption is limited. Roughly half of its crude oil imports transit the Strait, but coal accounts for about 60% of China's primary energy consumption and is sourced almost entirely domestically. Oil through Hormuz represents only about 5% of total Chinese energy consumption. The indirect risks — weaker global demand for Chinese exports, tighter financial conditions, and the possibility that Chinese air-defense weapons deliveries to Iran prove accurate — are more significant. That last development would give the conflict a great-power dimension that Beijing has so far avoided.

CFO & Treasurer Corner: The Action Checklist

| Focus Area | Action & Rationale |

|---|---|

| Funding & Liquidity | The window for advantaged fixed-rate issuance is closed. The 10-year at 4.25% to 4.30% is likely to reprice toward 4.50% if the blockade stalemates or the April 22 ceasefire lapses without extension. Draw revolvers now. Build cash buffers against a scenario where EBITDA weakens 20% to 30% in the second half. Floating-rate borrowers should model credit spread widening of 75 to 125 basis points. For many CFOs, the question has shifted — it is no longer whether to lock in rates, but whether the market will still be open at acceptable spreads by May. |

| Energy & Input Costs | The pre-buy and hedge window for Q2 is gone. Firms that did not act during the ceasefire week missed the best entry. The priority now is revising stress-test assumptions and modeling 2026 cost scenarios at $115 and $140 Brent. Prices are likely to stay elevated through year-end regardless of how the conflict resolves. Clearing mines, repairing infrastructure, and rebuilding inventories takes time regardless of when a ceasefire takes hold. |

| Working Capital | Higher energy and freight costs are working their way through supply chains in waves. Transportation and warehousing have taken the first hit. Consumer goods manufacturers, food producers, and light industrials are next. Companies with just-in-time supply chains and thin inventory buffers are most exposed in Q2 and Q3. Map those exposures now, lengthen your cycle-time assumptions, and get the cost impact into Q2 cash flow models before the next board meeting. |

| Consumer Demand | Industrial production declined sharply in March. The Beige Book shows discretionary spending softening across most districts. UMich sentiment is at 47.6, a level historically associated with spending contraction. Revenue forecasts built on 2025's trajectory need to be revised to reflect the lagged impact of higher fuel costs. The one mitigant: higher-income consumers, supported by equity-market wealth, are still spending. Firms with concentrated higher-income exposure in luxury goods, premium travel, and financial services are better insulated than mass-market peers. |

| Scenario Planning | Build three explicit scenarios aligned with our probability framework: Base Case — Deal or Extension (45%), Downside — Ceasefire Lapses (35%), Tail Risk — Full Escalation (20%). For the downside, use Ken Griffin's framing from the Semafor Summit: a 6 to 12 month Hormuz shutdown makes global recession inevitable. All three are live today and even if an agreement is reached, normalization of energy markets and supply chains will take time. |

Variables to Watch

| Variable | Why It Leads |

|---|---|

| 1. IRGC attacks — is the ceasefire survivable? | The IRGC reversed Iran's Friday opening within 24 hours and fired on tankers. Watch three signals: (1) whether IRGC gunboat activity ceases in the next 24–48 hours; (2) whether a second round of talks is confirmed before April 22; (3) whether any attack touches a U.S. asset (Tail Risk activation). Our view is the IRGC is trying to strengthen their current weak hand going into the 'final' negotiations. |

| 2. March Retail Sales (April 21, 8:30am ET) | Headline will be inflated by gasoline prices — possibly +1.3% to +1.5% MoM. Focus on the control group (ex-autos, gas, building materials). We project +0.3%, driven by the tax refund tailwind. Above +0.3% means the consumer was holding in March; below +0.2% signals genuine contraction already underway. BofA card data for March showed spending per household +4.3% YoY, with ex-gas still +3.6% YoY. |

| 3. Retail pump prices | The $10.4 billion weekly transfer from household budgets to fuel costs will not reverse until the Strait reopens. Track AAA daily and GasBuddy regional data, which has fallen 7 to 10 cents from its peak. A national average below $4.00/gal on gasoline is the first genuine consumer relief signal, and remaining there requires oil to fall durably below $85/bbl. |

| 4. April CPI (May release) | The April print will be the first to capture a full month of post-blockade gasoline prices. We expect headline PCE to peak near 3.5% year-over-year in April before energy base effects pull it lower. The key number is core CPI. A move above 2.8% year-over-year signals the energy shock is propagating into services and broad goods prices, making rate cuts this year very difficult to sustain. |

| 5. 10-Year Treasury yield | At 4.25% to 4.30%, the bond market is pricing a diplomatic pause. A move above 4.50% signals the market has given up on near-term easing. A decisive move below 4.20% tells you growth fears are overtaking inflation concerns. Our base case has the 10-Year averaging 4.25%. |

| 6. UMich long-run inflation expectations | At 3.4%, the long-run anchor is loosening but not broken. Two more readings at this level would narrow the Fed's room to support growth without triggering a credibility question. The Fed is unlikely to cut interest rates when UMich long-term inflation expectations are rising. |

Piedmont Crescent Capital Economic Forecast

| % change unless noted | 2024 Actual | 2025 Actual | 2026 Forecast | 2027 Forecast | 2028 Forecast |

|---|---|---|---|---|---|

| Output | |||||

| Real GDP | 2.8% | 2.1% | 2.5% | 3.0% | 2.8% |

| Consumer Spending | 2.9% | 2.6% | 2.0% | 1.9% | 2.4% |

| Business Fixed Inv. | 2.9% | 4.1% | 3.8% | 4.5% | 4.0% |

| Residential Inv. | 3.2% | −2.1% | −1.8% | 4.0% | 3.5% |

| Housing Market | |||||

| Housing Starts (000s) | 1,371 | 1,357 | 1,365 | 1,480 | 1,460 |

| New Home Sales (000s) | 685 | 679 | 738 | 790 | 820 |

| Existing Home Sales (000s) | 4,067 | 4,076 | 4,160 | 4,350 | 4,480 |

| Inflation (Year-over-Year) | |||||

| CPI | 2.9% | 2.7% | 3.0% | 2.4% | 2.2% |

| Core CPI | 3.2% | 2.6% | 2.6% | 2.3% | 2.2% |

| PCE Deflator | 2.6% | 2.6% | 3.0% | 2.5% | 2.0% |

| Core PCE Deflator | 3.0% | 2.8% | 2.9% | 2.4% | 2.0% |

| Labor Market | |||||

| Unemployment Rate (%) | 4.1% | 4.3% | 4.6% | 4.4% | 4.2% |

| Nonfarm Payrolls (000s/mo) | 122 | 10 | 40–70 | 60–90 | 90–120 |

| Interest Rates (End of Period) | |||||

| Fed Funds Target (EOP) | 4.25–4.50% | 2.75–3.00% | 3.00–3.25% | 3.25–3.50% | 3.50–3.75% |

| 10-Year Treasury (EOP) | 4.58% | 4.18% | 4.20% | 4.20% | 4.10% |

| Conv. Mortgage Rate | 6.72% | 6.42% | 6.25% | 6.10% | 5.90% |

Strategic Takeaway

The situation as of Sunday, April 19 is materially more dangerous than it was 72 hours ago. Iran opened the Strait of Hormuz on Friday — a genuine strategic concession that markets priced immediately and correctly. Then the IRGC reversed course within 24 hours, fired on commercial shipping, and declared the Strait back under its previous control. The brief opening was real; more than a dozen vessels transited. The reversal is equally real, and it reveals something important: the IRGC hardliners, not President Pezeshkian's civilian government, hold decisive authority over Iran's military posture. Stimson Center analyst Kaitlyn Hashem has documented how Israel's assassination campaign against IRGC commanders elevated a generation of hardliners pulled from semi-retirement who are more hardline and less nimble than those they replaced. These are not pragmatists constrained by hawks. They are the hardliners.

The economic damage from the seven-week shock is real and already embedded. The factory sector saw industrial production decline in March, though output still rose solidly for the first quarter as a whole. The April Beige Book shows a wait-and-see posture on hiring and capital spending across all twelve Fed districts ahead of the ceasefire deadline. Housing has missed its spring selling season, causing us to reduce our second half GDP forecast. Oil price shocks of this magnitude tend to weigh most heavily on business investment and hours worked with a lag of two to three quarters, meaning the employment and capex consequences of the past seven weeks will not be fully visible in the data until Q3 and Q4. Even if a ceasefire is signed this week, that damage does not reverse.

We are revising our probability distribution back toward the pre-Friday balance. The Base Case falls from 55% to 45% — not because a deal is impossible, but because the IRGC's reversal has made it harder to achieve before April 22 and raised the cost of failure if the deadline lapses. The Downside rises from 30% to 35%, and the Tail Risk rises from 15% to 20%, reflecting the IRGC's demonstrated willingness to attack commercial shipping. A ceasefire extension remains possible — AP sources report both sides gave an in-principle agreement before Saturday's reversal — but that agreement is now under stress. The April 22 deadline is the fulcrum.

Five indicators will tell you which scenario is materializing. First: whether IRGC gunboat activity ceases in the next 24 to 48 hours — a stand-down signals the hardliners made their point and are prepared to let diplomacy run. Second: whether Pakistani mediators confirm a second round of talks before April 22. Third: March Retail Sales on April 21 — watch the control group; above +0.3% means the consumer was holding in March. Fourth: where Brent oil closes on April 21 — above $105 means the market is pricing a lapse; below $95 means the market expects an extension. Fifth: any signal from Washington of flexibility on the port blockade as leverage to empower Iran's civilian government.

Mark P. Vitner, Chief Economist, Piedmont Crescent Capital · Updated April 19, 2026

Questions? Email: CompassReport@cavusecurities.com

© 2026 CAVU Securities, LLC

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation, offer, or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice. Any forward-looking statements or forecasts are not guaranteed and are subject to change at any time. Information from external sources has not been verified but is generally considered reliable.