Piedmont Crescent Capital | A View from the Piedmont

Islamabad Ends Without a Deal, Blockade Begins,

Iran Signals Willingness to Talk

The Prior Tail Risk Has Become the Base Case

Mark P. Vitner, Chief Economist · Piedmont Crescent Capital · April 14, 2026

Highlights of the Week

| Key Theme | This Week's Read |

|---|---|

| Inflation | March CPI surged 0.9% MoM (largest in 2 years); Core CPI 2.6%. March PPI: Final Demand +0.5% MoM, +4.0% YoY — hottest since Feb 2023. Goods prices jumped +1.6% MoM on energy. The energy shock is now feeding into the producer pipeline. |

| Consumer | U Mich Sentiment hit record low 47.6 (Apr prelim); 1-yr inflation expectations rose to 4.8%. NFIB Small Business Optimism fell 3.0 pts to 95.8 in March, below its 52-yr average for the first time since April 2025; Uncertainty Index spiked to 92. The NFIB cited the "dramatic spike in oil prices" as the primary driver. |

| Hormuz | U.S. naval blockade of all Iranian port traffic effective 10 a.m. ET April 13. Iran calls it "piracy" and warns no Persian Gulf port will be safe if Iranian ports are threatened. Oil initially surged back above $100/bbl. before retreating into the upper-$90s on reports of renewed back-channel contacts. |

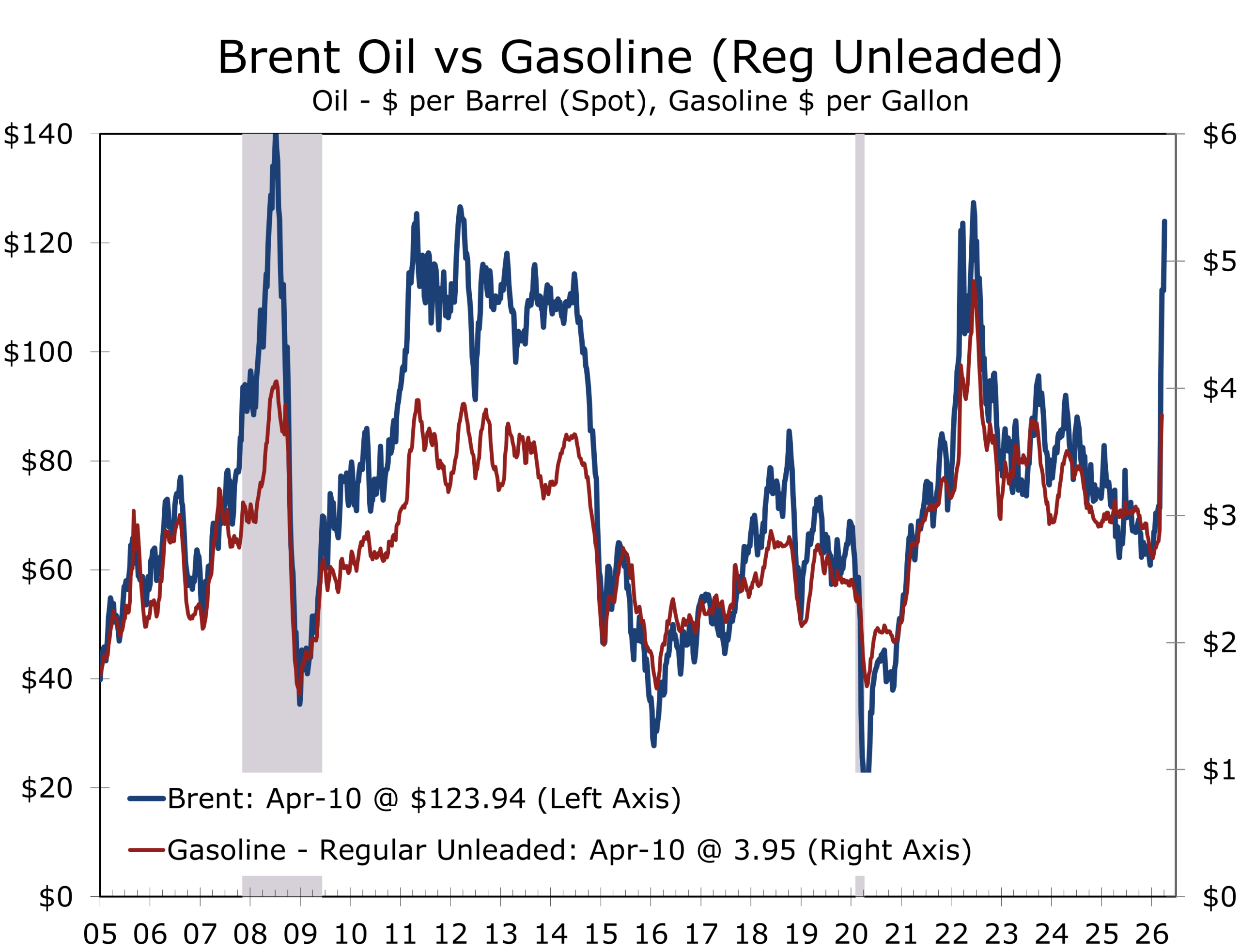

| Markets | The relief rally appeared to be over early Monday but reasserted itself by the close. WTI opened the week above $103 and Brent above $101 on the blockade announcement; hopes for a second round of talks have since pulled prices back toward last week's lows, with WTI at $95.73 and Brent at $97.89 Tuesday morning. |

| Diplomacy | Islamabad failed definitively on Sunday. Vance: Iran "chosen not to accept our terms." Nuclear disarmament and Hormuz control remained unbridged. Trump announced a naval blockade of all Iranian port traffic Sunday evening; CENTCOM confirmed it begins April 13 at 10 a.m. ET. U.S. also weighing resumption of limited military strikes. The two-week (through April 22nd) ceasefire status looked extremely uncertain at the start of the week but returned late Tuesday morning. |

| Fed/Policy | Fed is expected to hold rates steady. Inflation remains above target and energy costs pressures will persist. The central bank cannot look through an energy shock that is simultaneously squeezing household budgets and raising inflation expectations. The bar for hiking rates is exceptionally high, however, and a rate cut is unlikely while inflation expectations are rising. |

| Risk Signal | The naval blockade has moved from tail risk to operational reality. WTI and Brent both rose back above $100 to start the week but retreated sharply on word of quiet overtures from Iran. PCC revises its scenario framework: the former downside scenario (blockade/escalation) is now the base case. The ceasefire is in limbo. Iran's threat to retaliate against any Gulf port raises the stakes of every vessel movement. |

Market Snapshot

| Indicator | Level | Context |

|---|---|---|

| Brent Crude | $97.89 / bbl | Stabilized $95–$100; post-blockade range |

| WTI Crude | $95.73 / bbl | Mid-$90s; blockade-day spike partially retraced |

| 10-Yr Treasury | 4.30% | 4.30–4.35%; sticky inflation premium |

| 2-Yr Treasury | 3.82% | Curve +51 bps (2s10s) |

| National Avg Gasoline | $4.16 / gal | ↑ from $3.41 pre-war |

| National Avg Diesel | $5.67 / gal | ↑ sharply; record territory |

| Gold | ~$4,760 / oz | Safe-haven premium; clearest market signal |

| Fed Funds Target | 3.50–3.75% | On hold; no cut priced 2026 |

| UMich Sentiment | 47.6 | Record low (prelim. April) |

| 1-Yr Inflation Exp. | 4.8% | Highest since 2023 |

Sources: Reuters, WSJ, EIA, CME Group, University of Michigan. As of market open April 14, 2026.

“A truce is not the same as peace. A ceasefire stops the shooting. It does not restart the tankers.”

The Macro Backdrop: The Shock Is Gaining Traction

Two weeks ago, the economy appeared to have the forward momentum to outrun the energy shock. This week's data suggests otherwise. The transmission from higher energy prices is showing up, unevenly, in consumer prices, consumer sentiment, and behavior at the pump. The economy still has forward motion, but it is now more dependent on long-lived business fixed investment than it was a month ago.

March CPI was the week's pivotal release. Headline consumer prices surged 0.9% month over month, the largest gain in nearly two years, lifting the year-over-year rate to 3.3%. The composition, however, tells the most important story. Gasoline prices jumped 21.2% — the single largest monthly increase ever recorded for that series. The price of diesel fuel rose 30.8%. Together, energy accounted for nearly three-quarters of the entire monthly advance. Strip out energy (food prices were unchanged), and inflation rose just 0.2%, the same as it rose in February. Core CPI held at 2.6% year-over-year.

The composition of the release matters more than the headline itself. The first-round energy shock is now fully embedded in the March data, and the next question is whether the broader pass-through follows. Higher fuel costs raise transportation and logistics expenses, which feed into goods prices, services, and ultimately wages. We expect elevated fuel costs to work their way through the production channel over the next two to three months. Iran has every incentive to extend the conflict, knowing that pain at the pump will exert political pressure on President Trump.

Key Signal

This Is Not Yet a Generalized Inflation Breakout

Core CPI at 2.6% is stable and the energy shock has not yet propagated into wages or broad services — that remains the good news. But Tuesday's PPI data adds an important new layer: Final Demand PPI accelerated to +4.0% YoY, goods prices surged +1.6% MoM on energy, and the pipeline transmission from energy to wholesale costs is now confirmed. The next two CPI prints and the April PPI will determine whether this remains an energy-led squeeze or the beginning of a sustained breakout. We expect something in between — with near-term pressure concentrated in logistic-sensitive goods — but the bar for the Fed to look through this has risen materially.

The Consumer: From Sentiment to Behavior

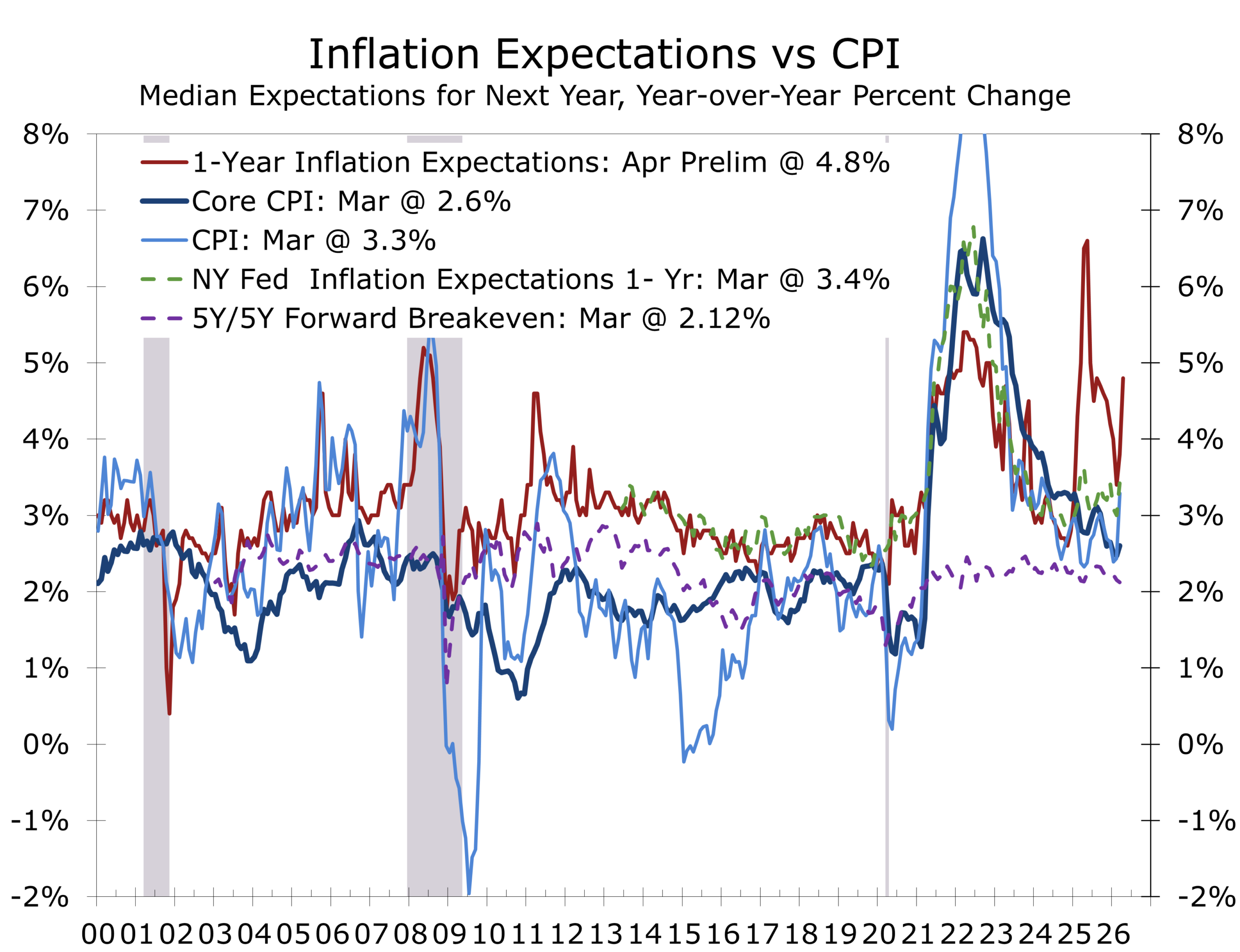

The consumer side of the economy deteriorated sharply this week, and in a way that matters more than a single data point normally would. The University of Michigan's preliminary April sentiment index fell to a record low of 47.6. One-year inflation expectations rose to 4.8%. Long-run expectations moved to 3.4%.

The long-run reading is the one to watch. Long-run inflation expectations are the anchor of the Fed's credibility framework, and the entire argument for looking through an energy-driven headline spike rests on households and businesses believing inflation will return to target. At 3.4%, that anchor is loosening. Consumer expectations for inflation have always run well ahead of financial market measures and the Fed's preferred gauges, such as the New York Fed's consumer survey, so a single reading is not itself a policy trigger. Even so, rate cuts are likely off the table while consumer inflation expectations are drifting higher.

More importantly, the deterioration is no longer confined to surveys. It is now visible in behavior. Drivers are cutting back as average gasoline prices reached $4.16 nationally and diesel hit $5.67. The estimated increase in consumer spending on gasoline and diesel has reached $10.4 billion; money that is no longer being spent on restaurants, entertainment, appliances, travel, or any of the categories that support service sector employment. This is the classic mechanism by which an oil shock converts from an inflation headline into a growth headwind.

The latest personal income and spending data showed the economy had a little less momentum ahead of the conflict. Nominal personal income fell 0.1% in February, largely reflecting sharp declines in personal dividend income ($39.7 billion) and government transfer receipts ($21.6 billion, led by lower Affordable Care Act-related social benefits). This was only partly offset by solid gains in compensation. Personal spending, which tends to more closely track wages and salaries, rose 0.5%, which still outpaced the 0.2% rise in wages and salaries. The saving rate slipped to 4.0%, leaving households little cushion.

Risk Factor

Inflation Expectations Are the Fed's Red Line — and They Are Moving

The Federal Reserve can look through a temporary energy-driven headline spike. It cannot look through deteriorating long-run inflation expectations. At 3.4%, the University of Michigan's long-run measure has not crossed the threshold that forces a policy response. Two more readings at or above current levels would restrict the Fed's ability to counteract the drag on spending. The Fed will have a hard time cutting interest rates while long-term inflation expectations are rising.

Key Data: PPI & NFIB (Released April 14)

Two key data releases this morning sharpen the economic picture. The March Producer Price Index came in softer than the headline feared but still alarming in its composition: Final Demand PPI rose +0.5% MoM (below consensus of +1.1%), but the 12-month rate accelerated to +4.0% YoY — the hottest reading since February 2023 and up sharply from February's +3.4%. Goods prices jumped +1.6% MoM, driven heavily by energy and gasoline, while services prices were flat. The message is clear: the energy shock is now feeding directly into wholesale costs and the producer pipeline, even as month-over-month momentum was somewhat softer than feared. Flat PPI services prices suggest margins are being squeezed initially, as higher energy prices reduce real incomes and make it more difficult for businesses to pass along their higher costs. April Core CPI read will reveal whether this pipeline pressure is accelerating into final consumer prices.

The NFIB Small Business Optimism Index for March fell 3.0 points to 95.8, slipping below its 52-year average of 98.0 for the first time since April 2025. The Uncertainty Index surged 4 points to 92, far above its long-term average of 68. Net profits dropped sharply (–11 points to net –25%). NFIB Chief Economist Bill Dunkelberg explicitly blamed the "dramatic spike in oil prices" for raising input costs, spooking business owners, and forcing price pass-throughs. Taken together, PPI and NFIB confirm that the energy shock has moved beyond the pump and is now embedded in wholesale price dynamics while visibly eroding Main Street confidence and margins. The economy is beginning to transition from an inflation shock to a growth headwind.

Geopolitics & Energy: A Ceasefire Is Not a Resolution

The relief rally built on ceasefire optimism has fully reversed. Markets were still pricing lower risk as late as Friday, with WTI at $95.73 and Brent at $97.89. That tone changed dramatically after 21 hours of direct talks in Islamabad collapsed on Sunday. The U.S. delegation — led by Vice President JD Vance, Steve Witkoff, and Jared Kushner — walked away without a deal. Iran's team, led by Parliament Speaker Mohammad Bagher Ghalibaf and Foreign Minister Abbas Araghchi, refused to surrender control of its nuclear enrichment program or cede leverage over the Strait of Hormuz. Tehran appears convinced that time is on its side and has internalized the pervasive "TACO" narrative circulating in social media and parts of the legacy press.

President Trump responded Sunday evening by announcing a naval blockade of all vessels entering or departing Iranian ports on the Arabian Gulf and Gulf of Oman. CENTCOM confirmed enforcement began April 13 at 10 a.m. ET. In the first 24 hours, no ships breached the blockade and six merchant vessels were directed to turn around. Oil prices immediately surged above $100 in early Asian trading Monday before partially retreating Tuesday to roughly $95–$98 as diplomatic signals resurfaced. President Trump stated that Iran had reached out seeking a deal, and a second round of talks in Pakistan is reportedly under active discussion.

Diplomatic channels remain open but narrow. Back-channel contacts have narrowed gaps on the nuclear file, though core differences persist: the U.S. proposed a 20-year suspension of all Iranian nuclear activity with strict verification; Iran countered with a 3-to-5-year halt. Ending Iran's nuclear ambitions and curbing its support for terrorist proxies remain non-negotiable for President Trump. The blockade is now operational, yet talks may resume as early as this week. Iran's next move remains the single most important variable for markets. The prior base case of a quick ceasefire extension has been overtaken by events.

The bond market's skepticism of last week's equity relief rally has been vindicated. The 10-year Treasury yield, which held steady near 4.30–4.35% through the ceasefire week, has now traded back down to 4.254%. Fixed income was pricing only a pause, not a resolution — and that caution looks increasingly prescient.

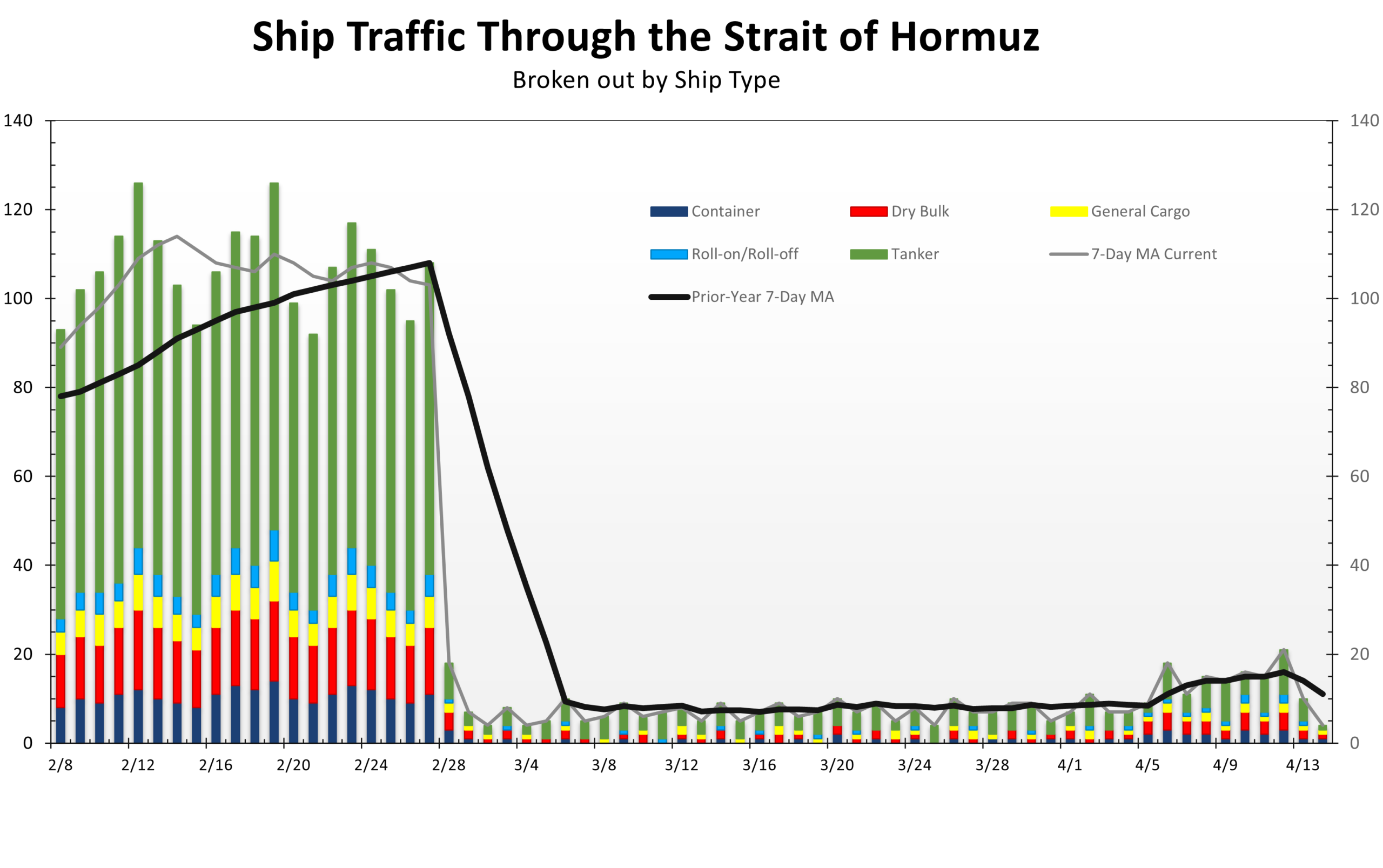

The Strait of Hormuz remains the central transmission channel to the real economy. Iran has effectively closed the waterway to nearly all foreign vessels since the war began on February 28, demanding control and fees for passage. The brief ceasefire produced only a trickle of commercial traffic (roughly 15 ships total versus a pre-war daily average of 138), with Iran charging $1–2 million tolls per vessel and conditioning passage on political relationships. The new U.S. blockade — targeting all maritime traffic to and from Iranian ports as well as any vessels paying Iranian tolls — adds a second layer of restriction. Tankers in the Persian Gulf have already begun diverting. Iran's military has warned that any threat to its port security will render "no port in the Persian Gulf and the Arabian Sea safe." This is an operational constraint in effect today, not rhetoric.

The standoff has prompted sharp downward revisions from multilateral institutions. The IMF has cut its global growth outlook and warned that sustained oil prices above $100 into 2027 would push the world economy to the brink of recession. The IEA has similarly slashed its forecasts for global oil supply and demand growth. IEA Executive Director Fatih Birol has warned that April could prove twice as difficult as March for global energy supplies, with diesel and jet-fuel shortages the most acute near-term risks in Asia and Europe. At the Semafor World Economy Summit, Birol described the Hormuz crisis as one that will "redraw the global energy map."

The Strategic Petroleum Reserve merits close attention. The U.S. executed a second SPR loan of 8.48 million barrels this week. The SPR now stands at 413.3 million barrels — its lowest level since the 1980s. Washington still has tools, but it does not have unlimited cushion.

Geopolitical Framework

The naval blockade — previously viewed as a 15–25% tail risk — is now an operational reality. Our revised probability distribution is as follows:

- 40% chance the blockade produces Iranian concessions within 10–15 days and talks resume before April 22;

- 40% probability the blockade holds, the ceasefire lapses on April 22, and hostilities resume at higher intensity (Iran remains convinced time is on its side);

- 20% tail risk of Iranian military retaliation against Gulf port infrastructure or U.S. naval assets, triggering full re-escalation.

The Islamabad outcome was a definitive breakdown, not a pause. Both sides exchanged written positions in the most intensive engagement between the two countries in 47 years. Vance left the U.S.'s "final and best offer" on the table; future offers will be less generous and may include demands for a permanent U.S. military presence on strategic islands in the Strait.

Markets & Financial Conditions: Relief, Not Resolution

The ceasefire-week equity rally was genuine in magnitude but has proven short-lived. As of Monday morning, markets are repricing the blockade reality: oil surged above $100 Monday before partially retracing to ~$96–98 Tuesday on Iran deal signals.

Today's energy shock differs structurally from the 1970s, thanks to a robust U.S. domestic production base, greater non-OPEC supply diversity, and a more aggressive SPR posture. None of those advantages ease the immediate supply arithmetic and impact on prices. The blockade has removed Iranian export volumes from global markets on top of the existing Hormuz transit disruptions, leaving open questions of how high oil prices go and how long they stay there.

The Federal Reserve remains firmly on hold. The FOMC had no analytical cover to cut rates even during last week's brief ceasefire window, with core CPI at 2.6% and inflation expectations drifting higher. With the naval blockade adding fresh supply pressure, rate cut discussion is off the table for the foreseeable future. Gold's resilience near $4,760 per ounce, with only modest give-back during the relief rally, is arguably the clearest signal in the market. A Columbia University energy analyst warned on Sunday that elevated oil prices are likely to persist through year-end 2026, regardless of how the conflict resolves, given the time required to reopen the strait, repair damaged infrastructure and rebuild depleted stockpiles.

Key Signal

Watch the Bond Market, Not the Equity Market, for the Definitive Signal

Equities are pricing the probability of a ceasefire, while the bond market is pricing inflation persistence. Until the 10-year Treasury yield moves meaningfully below 4.20%, on confirmed Hormuz normalization and easing energy prices, the financial conditions signal is tighter than the equity tape suggests. Corporate borrowers and CFOs should calibrate to the bond market's read rather than the equity market's relief.

CFO & Treasurer Corner: What This Means for Corporate Finance

| Focus Area | Action & Rationale |

|---|---|

| Funding & Liquidity | The fixed-rate issuance window has narrowed materially. With the naval blockade live and oil holding in the mid-$90s with upside risk, the 10-year Treasury is likely to reprice higher from 4.30%. Issuers who acted last week captured a window that may not reopen for months. Priorities now are drawing revolvers, building cash buffers, and reviewing covenant headroom against a scenario in which EBITDA weakens 20–30% in H2. Floating-rate borrowers are fully exposed and should model credit spread widening of 75–125 bps. For many treasury teams, the operative question is no longer whether to lock in rates but whether the market is still open. |

| Energy & Input Costs | Brent jumped back above $101 on the blockade announcement before retracing into the upper $90s (currently $97.89) on reports of renewed back-channel contacts. Much of the ceasefire-week pullback has been given back, and the window to hedge or pre-buy fuel and freight inputs has narrowed. Firms that did not act should revise stress-test assumptions upward and model 2026 cost scenarios at $115 and $140 Brent. Prices are likely to remain elevated through year-end 2026 regardless of resolution, given the time required to clear mines, repair infrastructure, and rebuild depleted inventories. The pre-buy and hedge window is closing; act now or model sustained pain. |

| Working Capital | Higher energy and freight costs are a slow-moving working capital squeeze. Transportation and warehousing absorbed the first wave, with consumer goods, industrials, and food producers next in line. Companies running just-in-time supply chains with thin inventory buffers face the greatest margin risk in Q2–Q3. Map exposures now and build cycle-time assumptions into cash flow models. |

| Consumer Demand | This week's Michigan Sentiment reading is not a soft data concern to be dismissed. At 47.6, it is at levels associated with genuine demand contraction, not merely caution. Consumers who are paying $4.16 at the pump and expecting 4.8% inflation a year from now do not increase discretionary spending, particularly middle and lower middle-income households, where budgets were already exceptionally tight. Revenue forecasts built on 2025 trajectory assumptions need to be revisited. One bit of caution, however: the UMich survey has been much lower than other measures and may be more reflective of persistent pressures on middle and lower-middle income households. Higher-end consumers appear to be holding up reasonably well. |

| Scenario Planning | Revise Q2 board scenario materials now, as the prior base case is obsolete. Ken Griffin of Citadel argued at the Semafor World Economy Summit that a 6–12 month Hormuz shutdown would make a global recession "inevitable," which is a reasonable way to calibrate the downside. Build three explicit scenarios: Blockade Succeeds (40% probability), with Iran conceding within 10–15 days, talks resuming, Brent $95–115, and consumer spending at 1.4–1.9%; Blockade Stalemates (40%), with the ceasefire expiring April 22, hostilities resuming, Brent $120–140, credit spreads +75–125 bps, and a contracting consumer; Full Escalation (20%), with Iranian military retaliation against Gulf ports or U.S. vessels, oil above $140, rising global recession risk, and the Fed in a nearly impossible bind. All three are live scenarios today and should be treated as such. |

Scenario Framework

| Scenario | Probability | Macro & Market Implications | Corporate Finance Action |

|---|---|---|---|

| Base Case | 40% | Blockade produces Iranian concessions within 10–15 days; back-channel contacts reopen talks before April 22. Ceasefire formally extended. Mine-clearing accelerates. Partial Hormuz commercial reopening by early May. Brent $100+ | Draw revolvers now. Fixed-rate issuance window narrowed; may reopen if blockade resolves quickly. Stress-test energy/freight at $115 Brent. Liquidity buffers are not optional. Prepare for demand contraction through Q2. |

| Downside | 40% | Blockade stalemates; Iran does not concede. Ceasefire expires April 22 without extension; hostilities resume. Both U.S. blockade and Iranian counter-restrictions remain simultaneously. Brent $120–140. Inflation re-accelerates past 4%; consumer spending in genuine contraction. Fed in impossible bind. Credit spreads +75–125 bps. This scenario has moved from 30% downside to co-equal with the base case. | Accelerate fixed-rate issuance ahead of wider spreads. Model demand destruction in revenue forecasts. Limit new floating-rate exposure. Review covenant headroom. |

| Tail Risk | 20% | Iranian military retaliation against U.S. naval assets or Gulf port infrastructure triggers full re-escalation. Iran's military has already warned that no Gulf port will be safe if Iranian ports are threatened. Oil $140+. Global recession risk rises sharply. Dollar surges; EM stress. Possible Chinese involvement following reported air-defense weapons delivery to Iran. Fed in impossible position: recession and 5%+ inflation simultaneously. | Maximize liquidity. Draw revolvers preemptively. Halt discretionary capex. Model severe demand contraction. Accelerate supply-chain diversification. |

Variables to Watch — In Order of Importance

| Variable | Why It Leads |

|---|---|

| 1. Iran's military response to the blockade (next 24–48 hours) | The blockade went live at 10 a.m. ET Monday. Iran's military has already warned that if Iranian ports are threatened, "no port in the Persian Gulf and the Arabian Sea will be safe." Whether Iran retaliates kinetically against U.S. naval assets or Gulf port infrastructure is the single most consequential variable in global markets right now. A kinetic response would mark the definitive end of the ceasefire and trigger the tail-risk scenario. Silence or a back-channel contact would signal Iran is reassessing. Critically, Iran's onshore oil storage fills to capacity within roughly 13 days of the blockade, after which fields must shut in — a process that carries long-run negative consequences for Iranian oil production. Iran has a finite window before the economic pain becomes irreversible. Watch CENTCOM statements, Gulf shipping advisories, and any signal from Tehran's oil ministry in real time. |

| 2. Retail gasoline and diesel prices | Where households and freight operators feel the war. The $10.4B per-week drag on consumer spending will not reverse until pump prices decline. Track AAA daily and GasBuddy regional data for a real-time assessment. |

| 3. 10-Year Treasury yield | The bond market's verdict on whether this is transitory. If the 10-year holds above 4.30% as oil falls, the market is telling you that the inflation risk is moving beyond energy. A move above 4.50% would signal a materially tighter financial conditions environment. The latest move, back down to 4.25%, suggests a near-term agreement would limit damage to the economy this year. |

| 4. University of Michigan inflation expectations | At 4.8% one-year expectations, we are approaching the threshold where the Fed's credibility becomes a greater question. The risk is that higher gasoline prices become embedded in wage demands. If expectations rise further in the next two readings, the policy calculus changes, with the Fed remaining on hold for longer being the most likely result. |

| 5. Islamabad negotiations (April 22 deadline) | The most consequential non-data variable on the calendar remains the next phase of the standoff: ceasefire extension, a broader framework agreement, or outright collapse. Each outcome carries a distinctly different macro signature. Markets should be prepared for any of the three. Iran will test President Trump's resolve, betting that domestic political pressure will eventually force him to cave. We believe the President sees no acceptable alternative to an outcome that permanently denies Iran both a path to a nuclear weapon and the ability — or desire — to threaten commercial shipping through the Strait of Hormuz or its regional neighbors, whether directly or via proxies. This remains a tall order. One notable development on Monday: Trump said the "right people" in Tehran had reached out seeking a deal. If that proves to be a genuine back-channel signal rather than a tactical ploy, the probability distribution would shift materially toward the base case. Watch for any announcement of a second meeting before April 22. |

Looking Ahead: Week of April 14

| Day | Release / Event | Why It Matters |

|---|---|---|

| Monday Apr 13 | Hormuz ship count update (EIA/Reuters) | Blockade entered its first full day. Oil surged above $100 in Asian trading before settling in the mid-to-high $90s as Trump signaled renewed back-channel contacts with Tehran. Enforcement was confirmed across the Gulf, with no Iranian kinetic response; U.S. equity markets absorbed the news with modest pressure and bond yields held 4.30–4.35%. Iran's first meaningful response will be the critical read, with credit spreads, the VIX, and the 10-year Treasury confirming which scenario is being priced. |

| Tuesday Apr 14 | PPI (March); NFIB Small Business Optimism (March) | PPI (March): Final Demand +0.5% MoM, +4.0% YoY — hottest since Feb 2023; goods +1.6% MoM on energy, services flat. Confirms energy-to-producer-pipeline transmission is live. NFIB Optimism fell to 95.8, below 52-yr average; Uncertainty Index hit 92. Empire State Mfg and Retail Sales (March) still to come; focus on the control group ex-autos, gas, and building materials. |

| Wednesday Apr 15 | Empire State Manufacturing (April); Retail Sales (March); Industrial Production (March); Beige Book | Retail Sales will show whether consumers have already begun pulling back on discretionary categories, with the control group (ex-autos, gas, and building materials) the cleanest read. Empire State gives an early April snapshot of factory conditions post-blockade. The Beige Book will offer the most textured view yet of how the energy shock is flowing through supply chains, labor costs, and corporate pricing. |

| Thursday Apr 16 | Initial Jobless Claims; Housing Starts (March); Philadelphia Fed | Claims above 220K would begin to crack the 'no-hire, no-fire' equilibrium. Housing starts will show whether rate sensitivity has been overtaken by sentiment deterioration. |

| Friday Apr 17 | Leading Indicators (March); Existing Home Sales (March) | Leading Indicators will offer an early read on whether the energy shock is pulling the broader cycle lower. Existing Home Sales will show how quickly the deterioration in sentiment is spreading to housing. Any Islamabad communiqué released over the weekend should be read carefully Monday morning. |

| April 22 | Ceasefire Expiration Deadline | Ceasefire expiration. Islamabad produced no deal and no scheduled follow-on, and the U.S. has left its final offer on the table. Iran's posture in the strait, in back-channels, and in its public statements between now and April 22 is the single most consequential variable for Q2 macro and markets. Positioning for each scenario should not wait until this date arrives. |

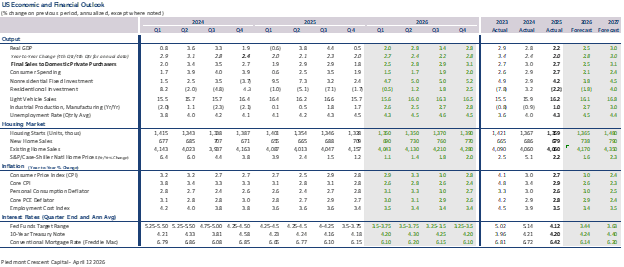

Piedmont Crescent Capital Economic Forecast

Concluding Thoughts

The prior read on CPI, Michigan sentiment, and the pump-price drain still stands. This morning's data has made each element harder to dismiss. March PPI accelerated to +4.0% year-over-year — the hottest print since February 2023 — with goods prices surging on energy even as the month-over-month headline came in slightly softer than feared. NFIB Small Business Optimism fell below its 52-year average for the first time since April 2025, and the NFIB chief economist pointed directly at the "dramatic spike in oil prices" for weakening confidence and forcing price pass-throughs. The energy shock is now showing up simultaneously in wholesale prices, Main Street margins, and small-business hiring intentions.

Diplomacy ran out of room relatively quickly in Islamabad as both sides tested one another's resolve. The picture on Tuesday was more encouraging than the blockade rhetoric might suggest. U.S.-Iran talks could resume as early as this week, even with the blockade in place, though both sides remain far apart on nuclear enrichment and Hormuz leverage. The blockade is imposing a steep daily cost on Iran's economy as onshore storage approaches capacity. Citadel's Ken Griffin has called a prolonged Hormuz shutdown a plausible path to global recession, though the drag would fall more heavily on the rest of the world than on the U.S. IEA Director Birol says the episode will "redraw the global energy map." Both views assume no negotiated resolution — which we believe is too pessimistic. The back-channel contacts reported this week leave room for an off-ramp, and the Iranian public has its own reasons to prefer a government that is not treated as a pariah.

The question that defined last week — whether back-channel contacts would produce a second round of talks before April 22 — has been replaced by a harder one: whether a naval blockade can extract the concessions that 21 hours of direct talks could not. The Strait of Hormuz remains the single most important indicator for global markets, though the relevant variable has shifted from the daily ship count to Iran's next move. Trump's suggestion on Monday that senior Iranian figures had reached out is worth watching closely. If that back-channel contact is genuine and produces a second meeting before April 22, our probability distribution shifts toward resolution. If it is merely a delaying tactic, the economic arithmetic of the blockade will force Iran's hand before much longer.

Variables to Watch (in order of immediacy)

- Iran's military response in the next 24–48 hours. This is the immediate escalation test. Tehran has already warned that no port in the Persian Gulf and the Arabian Sea will be safe if its own ports are threatened. Whether that warning turns kinetic will determine if we are in a coercive negotiation or a hot war.

- Any signal of Iranian flexibility via back channels before April 22. Vance has said diplomacy is not over, but the U.S. is now negotiating with a blockade rather than a proposal. Trump's claim that Iran's "right people" reached out — and U.S. confirmation that a second meeting is being discussed — is the most important signal of the day.

- Retail pump prices. The $10.4 billion weekly transfer from household budgets to fuel spending will not reverse until the Strait reopens. A Columbia University energy analyst warned Sunday that meaningful relief is unlikely before late 2026. Energy Secretary Wright echoed this at the Semafor World Economy Summit, saying prices will be "high and maybe even rising" until meaningful ship traffic resumes.

- Long Treasury yields. Watch whether the 10-year breaks above 4.50%. That would confirm the market has abandoned near-term easing hopes and is pricing persistent inflation into 2027.

- Chinese policy signals. Beijing buys the bulk of Iran's oil and has the most to gain from a negotiated resolution. Yet U.S. intelligence now suggests China may be preparing to supply air-defense weapons to Iran, adding a great-power dimension to the conflict.

Mark P. Vitner, Chief Economist, Piedmont Crescent Capital · Updated April 14, 2026

© 2026 Piedmont Crescent Capital. For informational purposes only.