Inflation Remains Well Short of Expectations

- Tariffs continue to dominate the economic discussion and remain the key driver of market volatility.

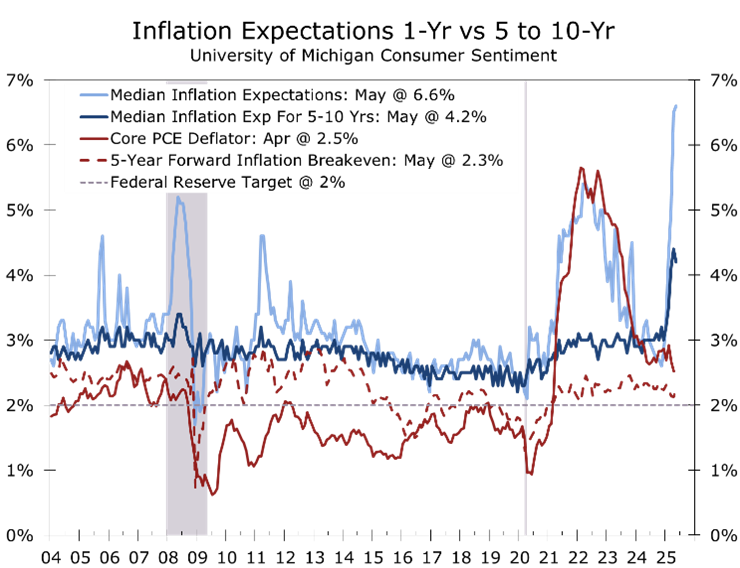

- Consumer surveys show sharply rising near-term inflation expectations, but data suggest more limited long-term inflation.

- Milton Friedman’s framework supports the idea that tariffs are not inflationary unless the Fed accommodates them.

- April PCE data showed muted inflation, with slowing consumption and a continued moderation in services prices.

- Treasury Secretary Bessant defends tariffs as targeted and non-inflationary; calls for offsetting tax cuts.

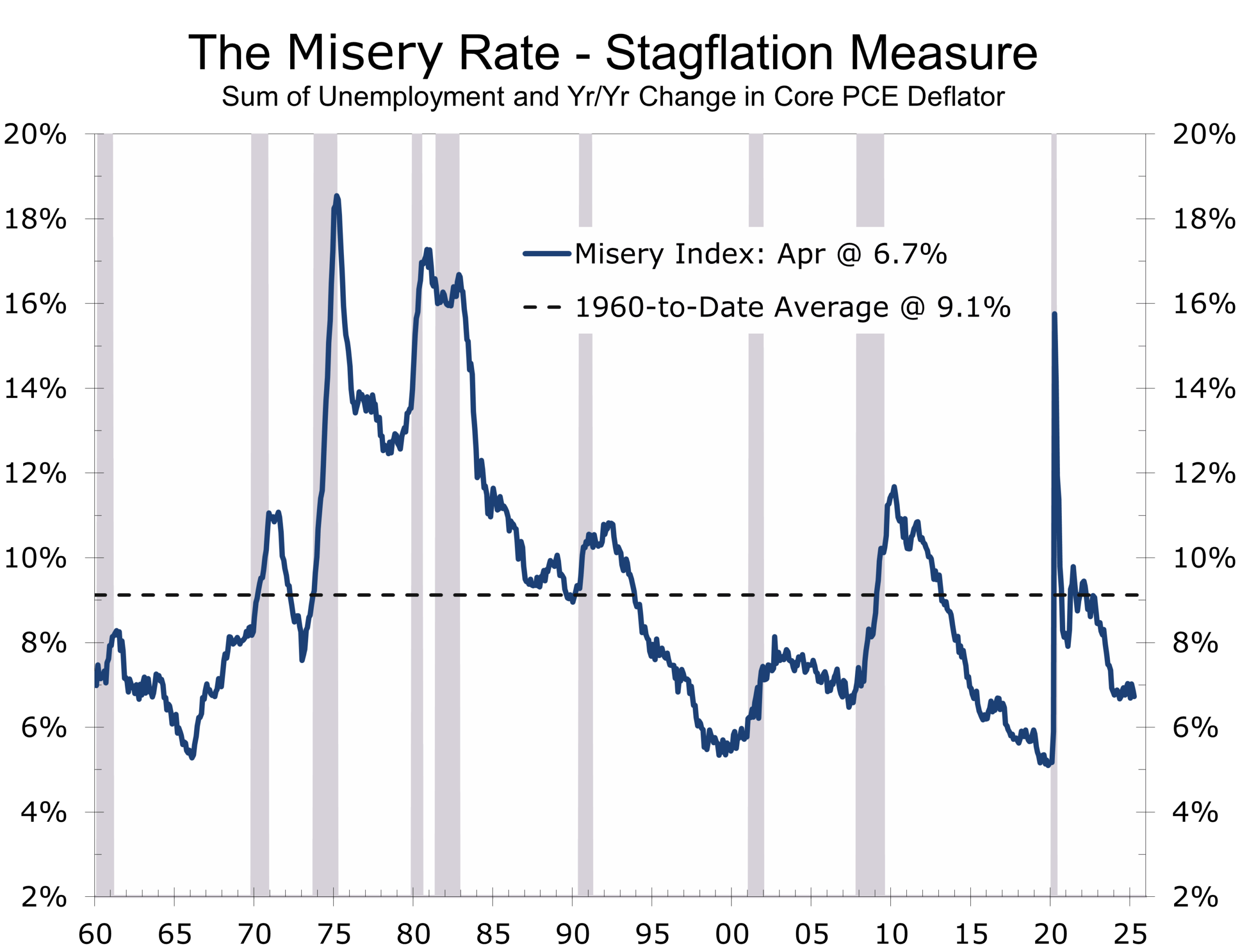

- Larry Summers warns of “stagflation-lite” and potential Fed policy missteps.

- Concerns over inflation expectations and supply chain risk are driving the Fed’s cautious stance.

- We expect the Fed to continue unwinding the tightening put in place from early 2022 to mid-2023 and look for two quarter point cuts during the second half of 2025, offsetting some of the drag tariffs have placed on an already slowing economy.

Tariffs and Inflation

Tariffs continue to dominate the economic discussion and remain a key driver of market volatility. One critical question persists: are tariffs inflationary or disinflationary? The most widely followed consumer surveys suggest Americans expect higher prices—both the University of Michigan’s Sentiment Index and the Conference Board’s Consumer Confidence Survey have registered upticks in inflation expectations. But as is typically the case with survey data, the deeper question is what tariffs actually do to inflation. As taxes on imports, they do not expand the money supply. Instead, they distort relative prices—altering the structure of spending more than fueling a rise in the overall price level.

The inflationary impact of tariffs is not as straightforward as it appears at first glance.

One of Milton Friedman’s most famous and defining axioms is that inflation is “always and everywhere a monetary phenomenon.” Within that framework, tariffs are not inflationary unless the Fed allows them to be—either by over-accommodating or by failing to distinguish between one-off price adjustments and persistent cost pressures. That logic underpins the Federal Reserve’s current pause. Despite slowing inflation and a modestly restrictive monetary policy, Chair Jerome Powell has signaled the Fed is not ready to cut interest rates further and will ‘wait and see’ how tariffs ripple through the data.

The latest inflation print supports that stance. The PCE deflator rose just 0.1% in April. Headline inflation eased to 2.1% year-over-year; core PCE slipped to 2.5%. Both are within striking distance of the Fed’s 2% target, particularly with the labor market near full employment. No broad acceleration is evident.

The underlying data are also supportive. Personal income rose 0.8%, driven by a 2.8% surge in transfer payments related to retroactive benefits under the Social Security Fairness Act. Wages and salaries—the core driver of consumer spending—climbed a solid 0.5%. Consumption increased just 0.2%, however, a sharp slowdown from March’s 0.7% gain. Notably, all of April’s increase came from services, reversing the prior month’s strength in goods. Durable goods outlays—particularly on autos and recreational equipment—feel after a March spike, as consumers appeared to front-load purchases ahead of tariff hikes. Since services account for roughly two-thirds of consumer spending, continued price restraint in this category would help limit broader inflation pressures.

The spending spree may have temporarily lifted goods prices and then reversed in April. Overall goods prices fell 0.1% in April, with grocery prices down 0.3% and gasoline prices edging slightly lower. Core goods prices eased as well, although some categories, including motor vehicles (+0.2%), furniture (+0.4%), and recreational goods and RVs (+1.5%) posted gains.

Service prices—largely insulated from import tariffs—rose just 0.1% in April after a 0.2% gain in March. Financial services prices tumbled 1.1%, reflecting the April equity selloff. Prices for recreational services fell 0.7%, driven by lower costs for sporting and cultural events. The closely watched “super core” index—which excludes housing and energy services—was flat in April. The slower pace in services inflation over the past two months may be an early signal of cooling demand in non-tradable sectors.

If consumers are spending more on tariffed imports, they have less to spend elsewhere.

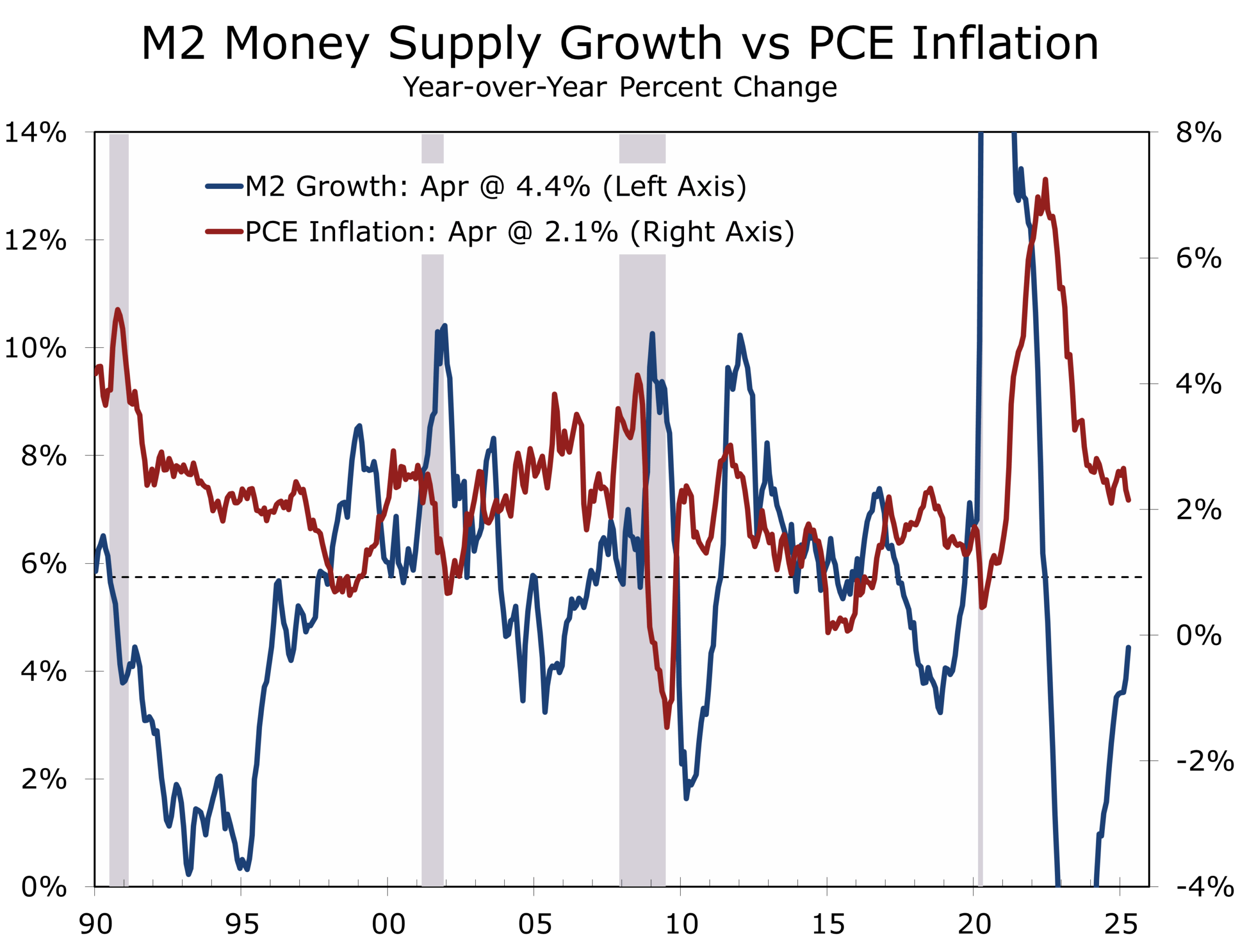

Tariffs raise prices on tradable goods and on goods and services reliant on imported components—they do not increase the money supply. If consumers are spending more on tariffed imports, they may have less to spend elsewhere—unless the Fed injects additional liquidity. This dynamic should limit inflation’s reach. The latest data show the M2 money supply has risen 4.4% over the past year, more than a percentage point below its 5.7% average pace since 1990.

The latest data strengthen the Trump administration’s argument that tariffs will not prove broadly inflationary. While that assessment may be optimistic, tariffs are likely to add less to inflation than consumers currently fear. We expect the economic data to bolster this point in coming months.

Treasury Secretary Scott Bessant appears prescient. He called the tariffs “surgical and necessary,” targeting strategic sectors like electric vehicles, solar panels, and steel. “These measures aren’t hitting staples,” he said on May 30. “We’re not seeing broad inflationary spillovers.” Bessant also suggested that tariff revenues could partially fund offsetting tax cuts. On Meet the Press, he remarked, “If taxes are inflationary, then cutting taxes is deflationary”—a deliberate effort to reframe tariffs not as inflationary fuel, but as a potential fiscal rebalancing tool.

Not all agree. Larry Summers, speaking with Bloomberg in May, warned that tariffs could lead to “stagflation-lite”—weaker growth paired with stickier prices in targeted sectors. He cautioned that mistaking sector-specific pressures for system-wide inflation could provoke a Fed policy error. Research from the Yale Budget Lab estimates that the 2025 tariff rounds—including the recent EU retaliation—could lift the PCE price level by 0.5 percentage points by year-end, relative to where it would otherwise be.

What would Milton Friedman say? Friedman staunchly opposed tariffs in nearly all forms. He would likely have argued that tariffs are primarily a tax that distorts market efficiency, with their inflationary or disinflationary impact depending on context. He would emphasize that tariffs raise the cost of imported goods, potentially increasing prices if domestic substitutes are pricier or supply chains are disrupted. However, he might also note that tariffs act as a tax by reducing consumer purchasing power, which could dampen demand and exert disinflationary pressure elsewhere. Friedman would likely stress that the net effect hinges on market dynamics and the economy’s underlying momentum

Treasury Secretary Scott Bessant appears prescient. He called the tariffs “surgical and necessary,” targeting strategic sectors like electric vehicles, solar panels, and steel. “These measures aren’t hitting staples,” he said on May 30. “We’re not seeing broad inflationary spillovers.” Bessant also suggested that tariff revenues could partially fund offsetting tax cuts. On Meet the Press, he remarked, “If taxes are inflationary, then cutting taxes is deflationary”—a deliberate effort to reframe tariffs not as inflationary fuel, but as a potential fiscal rebalancing tool.

Not all agree. Larry Summers, speaking with Bloomberg in May, warned that tariffs could lead to “stagflation-lite”—weaker growth paired with stickier prices in targeted sectors. He cautioned that mistaking sector-specific pressures for system-wide inflation could provoke a Fed policy error. Research from the Yale Budget Lab estimates that the 2025 tariff rounds—including the recent EU retaliation—could lift the PCE price level by 0.5 percentage points by year-end, relative to where it would otherwise be.

What would Milton Friedman say? Friedman staunchly opposed tariffs in nearly all forms. He would likely have argued that tariffs are primarily a tax that distorts market efficiency, with their inflationary or disinflationary impact depending on context. He would emphasize that tariffs raise the cost of imported goods, potentially increasing prices if domestic substitutes are pricier or supply chains are disrupted. However, he might also note that tariffs act as a tax by reducing consumer purchasing power, which could dampen demand and exert disinflationary pressure elsewhere. Friedman would likely stress that the net effect hinges on market dynamics and the economy’s underlying momentum.

Friedman would fundamentally oppose tariffs for their interference with free trade, predicting long-term inefficiencies—protected industries tend to be less creative and productive—over short-term price effects. This angle remains underappreciated in the current debate.

Tariffs threaten inflation by raising expectations and potentially disrupting supply chains.

Two key concerns are driving the Fed’s cautious ‘wait and see’ posture: the sensitivity of inflation expectations and the risk of renewed supply chain disruptions. While short-term expectations have spiked, long-term expectations remain mostly anchored. The Fed knows that if businesses and households begin to believe inflation is persistent, it could trigger wage demands and forward-pricing behavior—embedding inflation into economic decisions and pushing rates and volatility higher. Anchoring expectations is critical to maintaining monetary policy credibility.

Supply chain fragility is the other wildcard. Memories of post-pandemic logistics bottlenecks and component shortages are still fresh. With tariffs reinstated and global trade relations under pressure, the Fed is watching closely for signs of renewed stress. Powell and others have pointed to shipping costs, commodity volatility, and reshoring dynamics as potential inflation channels. Many economists in the “Team Transitory” camp still argue that the inflation surge that coincided with the reopening of the economy was driven more by pandemic-era supply snarls than by the 40% jump in M2 that followed the onset of the pandemic.

At its May meeting, the FOMC held rates steady at 4.25% to 4.50%. Minutes revealed most policymakers now see upside risks to inflation. Powell, in his post-meeting press conference, reiterated the Fed’s “wait-and-see” approach. “We can’t say which way this will shake out,” he said, citing the unusual supply-side nature of the risks. Dallas Fed President Lorie Logan noted that it “could take quite some time” before rate cuts are appropriate. New York Fed’s John Williams and Richmond’s Tom Barkin likewise emphasized the need for patience as tariff effects and global trade frictions evolve.

Markets are left parsing a complex signal. Tariffs may not be reigniting inflation as much as feared, but they’re clearly reshaping consumer behavior. The tax burden is real—even if it hasn’t fully registered in the indices. For the Fed, the challenge is distinguishing signal from noise. We still expect two rate cuts before year-end, with the first likely coming in September.

The key question now is whether short-term inflation fears begin seeping into long-term expectations. The University of Michigan’s survey shows a notable uptick, though it has become increasingly politicized. The Fed places more weight on market-based indicators—particularly the five-year forward breakeven. Absent a sustained rise in this measure, we expect the Fed to continue unwinding its 2022–2023 tightening cycle. They will need to proceed cautiously, however, because the noise surrounding the spike in consumer inflation expectations is highly visible and loud. Some reprieve will likely be needed before the Fed moves forward with what we expect to be two quarter point cuts in the federal funds rate, which should help offset the drag tariffs are having on an already slowing economy.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

June 2, 2025

Mark Vitner, Chief Economist

(704) 458-4000