Trade, Tax Cuts & Trump’s Adventures

- The U.S. and China reached a limited trade pact focused on tariff rollbacks and increased access to tech products.

- Moody’s downgraded the U.S. credit rating to Aa1 from Aaa, citing structural fiscal risks and rising debt burdens.

- President Trump’s Middle East trip renewed the U.S.-Saudi strategic partnership, unlocking major IT and defense contracts and a flurry of deals with the UAE, Saudi Arabia, and Qatar.

- Russia’s war with Ukraine appears to be seeing some quiet progress toward a ceasefire, aided by Russia’s faltering economy and growing pressure from China.

- The CPI came in below expectations, while April retail sales were mixed. The tidal wave of tariff announcements slowed industrial production but the recent softening on tariffs has lifted global PMIs.

- Higher interest rates continued to undermine the housing sector. Weekly jobless claims remain mixed, while the early read on consumer sentiment came in weak amidst soaring inflation expectations.

- The tax package (Big Beautiful Bill) is shaping up to be modestly stimulative, while tariffs are expected to produce a drag on growth but modest uptick in government revenues.

Markets opened the week digesting a mix of economic data, trade diplomacy, and geopolitical news. Leading the headlines was a modest U.S.-China trade deal featuring targeted tariff rollbacks and eased restrictions on Chinese chipmakers, in exchange for expanded U.S. access to agriculture and industrial markets. Initial market optimism faded, however, amid lingering high tariffs and persistent uncertainty over summer supply chain disruptions.

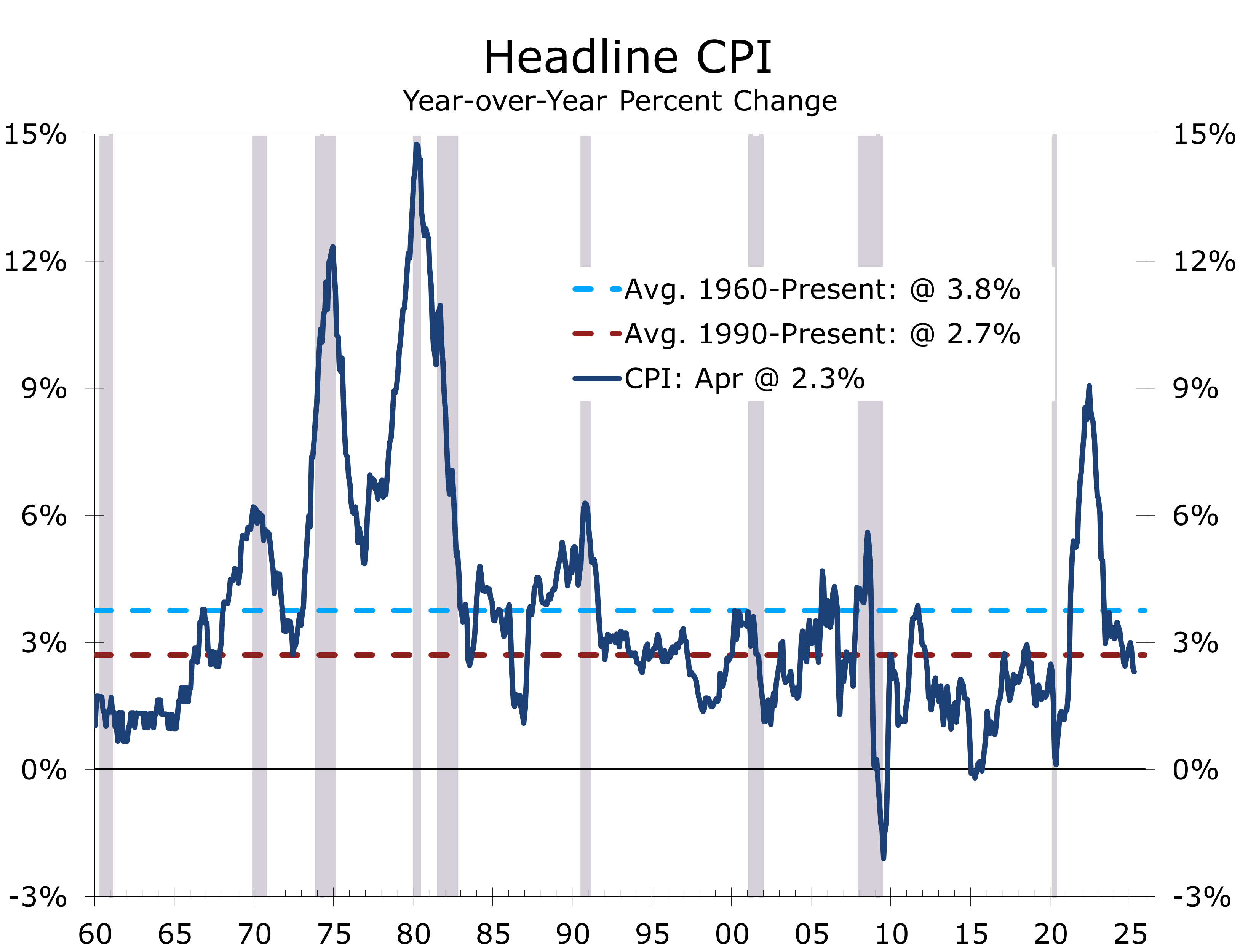

Markets digested a full week of economic data following the trade deal. The April CPI came in cooler than expected, with headline inflation up just 0.2%, bringing the year-over-year rate down to 2.3%. Core inflation held at 2.8%. Goods prices fell 0.2% year-to-year—mainly due to energy—while services stayed firm at 3.7%. Notably, core goods inflation turned positive at 0.1% y/y for the first time since early 2024, suggesting tariff-driven supply shocks may be building.

Tariffs have yet to boost measured inflation. The latest readings came in softer than expected.

Normally, softer CPI readings might nudge the Fed toward easing. However, with inflation expectations rising and supply-side frictions building, policymakers are unlikely to pivot soon.

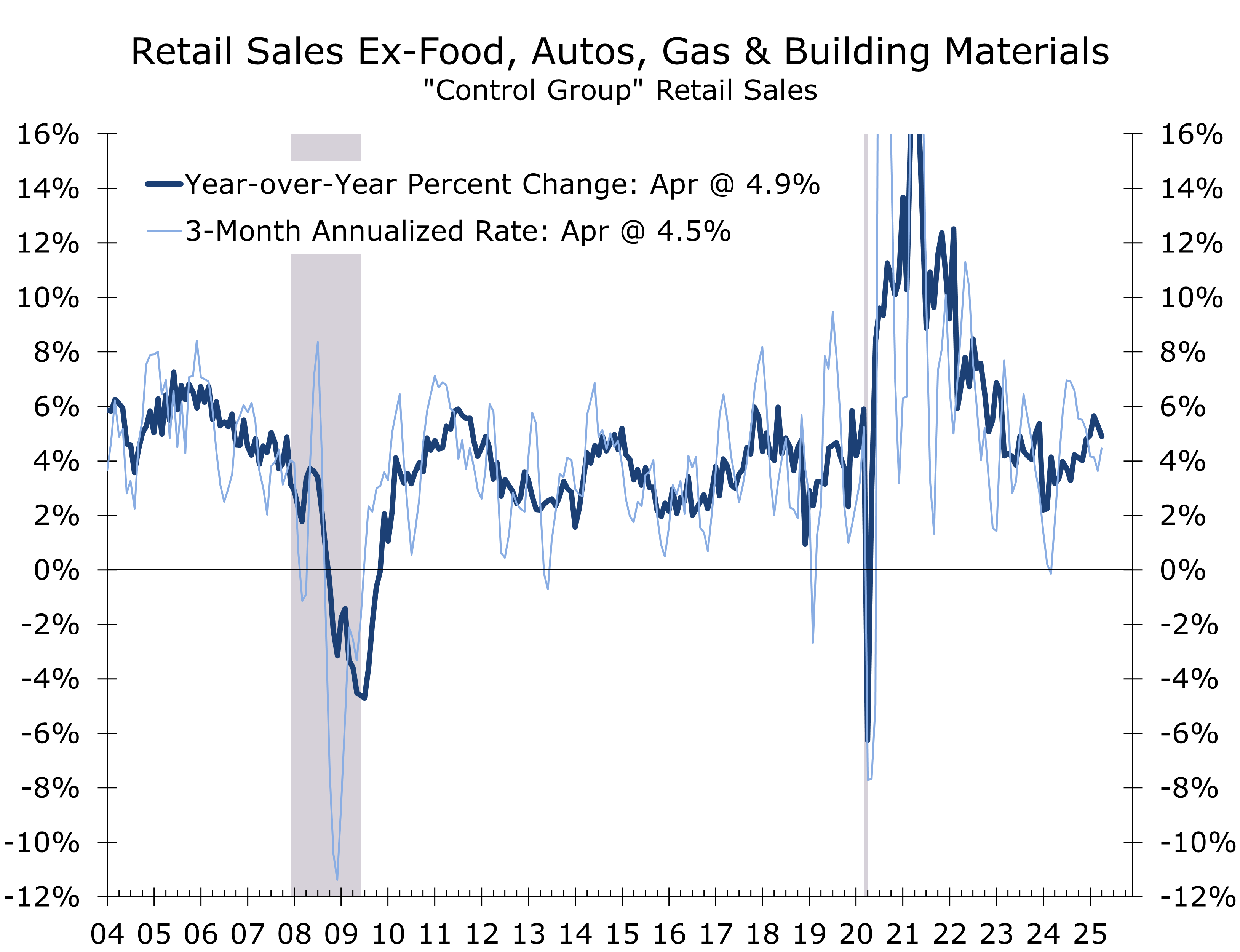

April retail sales pointed to deceleration, not collapse. Headline sales rose 0.1%, beating expectations but well off March’s revised 1.7% surge. Core sales also rose 0.1%, while the control group fell 0.2%, likely due to front-loaded spending in March—particularly autos—and a late Easter shift. Restaurant sales remained firm, countering weak consumer sentiment. On a three-month average basis, spending looks solid, and personal consumption is tracking stronger than expected, supporting our 2.4% upside Q2 GDP call.

Labor market resilience continues. Initial jobless claims edged down 2k to 227,000 for the week ending May 17, in line with expectations. Continuing claims rose 36,000 to 1.79 million—just above consensus—signaling that job seekers are having a harder time landing a new job. Meanwhile, the S&P Global U.S. Manufacturing PMI jumped 2.1 points to 52.3, the highest since 2022, with gains in output (50.7), new orders (53.3), and employment (49.6). Input and output prices surged to two-year highs, driven largely by tariff-related cost pressures. Business sentiment improved following the tariff rollback.

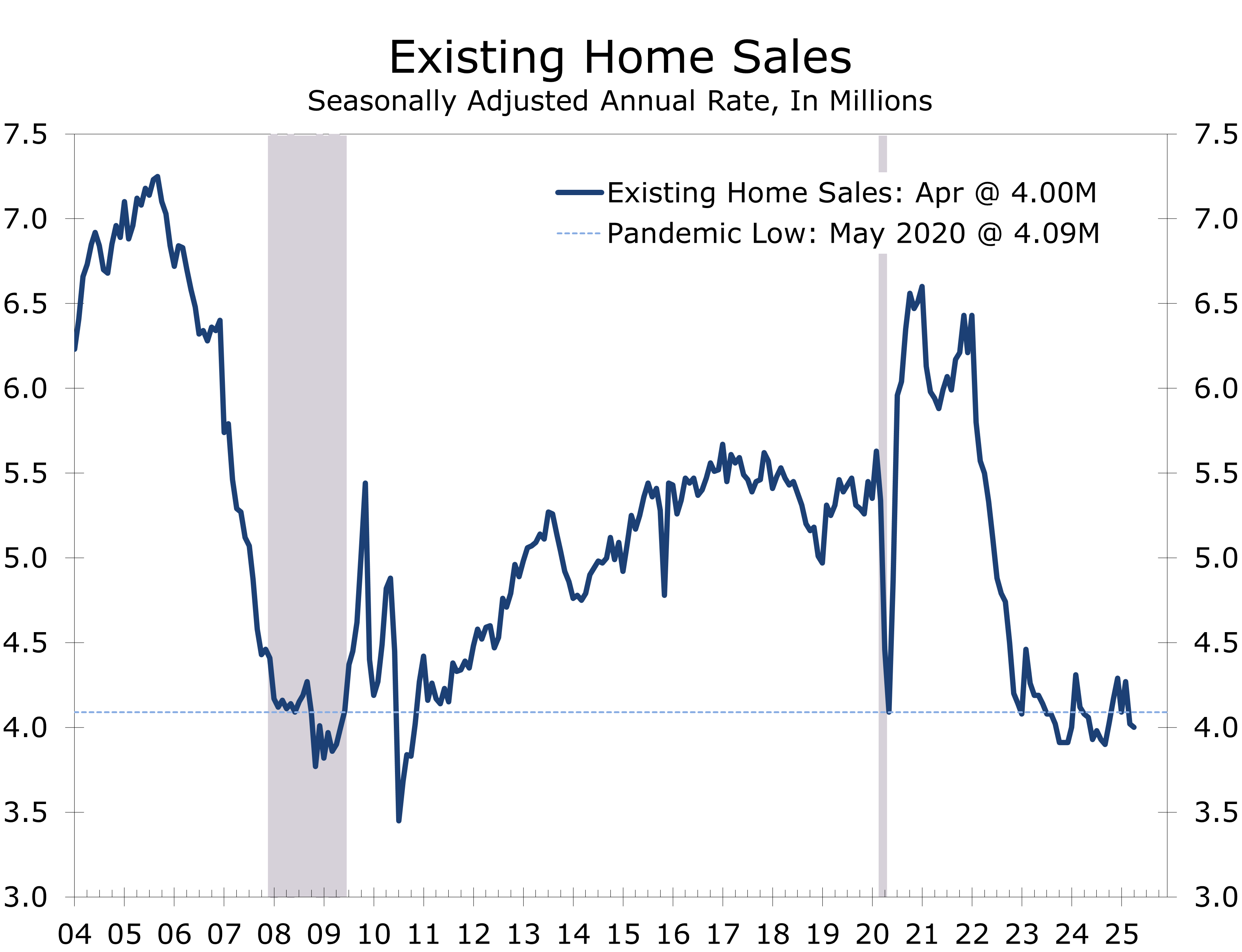

Existing home sales fell 0.5% in April to a 4-million-unit pace. Sales are down 2% year-to-year. Inventory rose 9% to 1.45 million units—the highest since September 2020—and up 21% year-to-year. The months rose to 4.4 months, the highest since May 2020.

While the housing market has needed more inventory, demand is clearly lacking. Homes sat on the market for an average of 29 days in April, up from 26 a year ago, suggesting slower turnover. Anecdotal evidence suggests prices cuts are becoming more common. The median price has slowed to just 1.8% year-to-year.

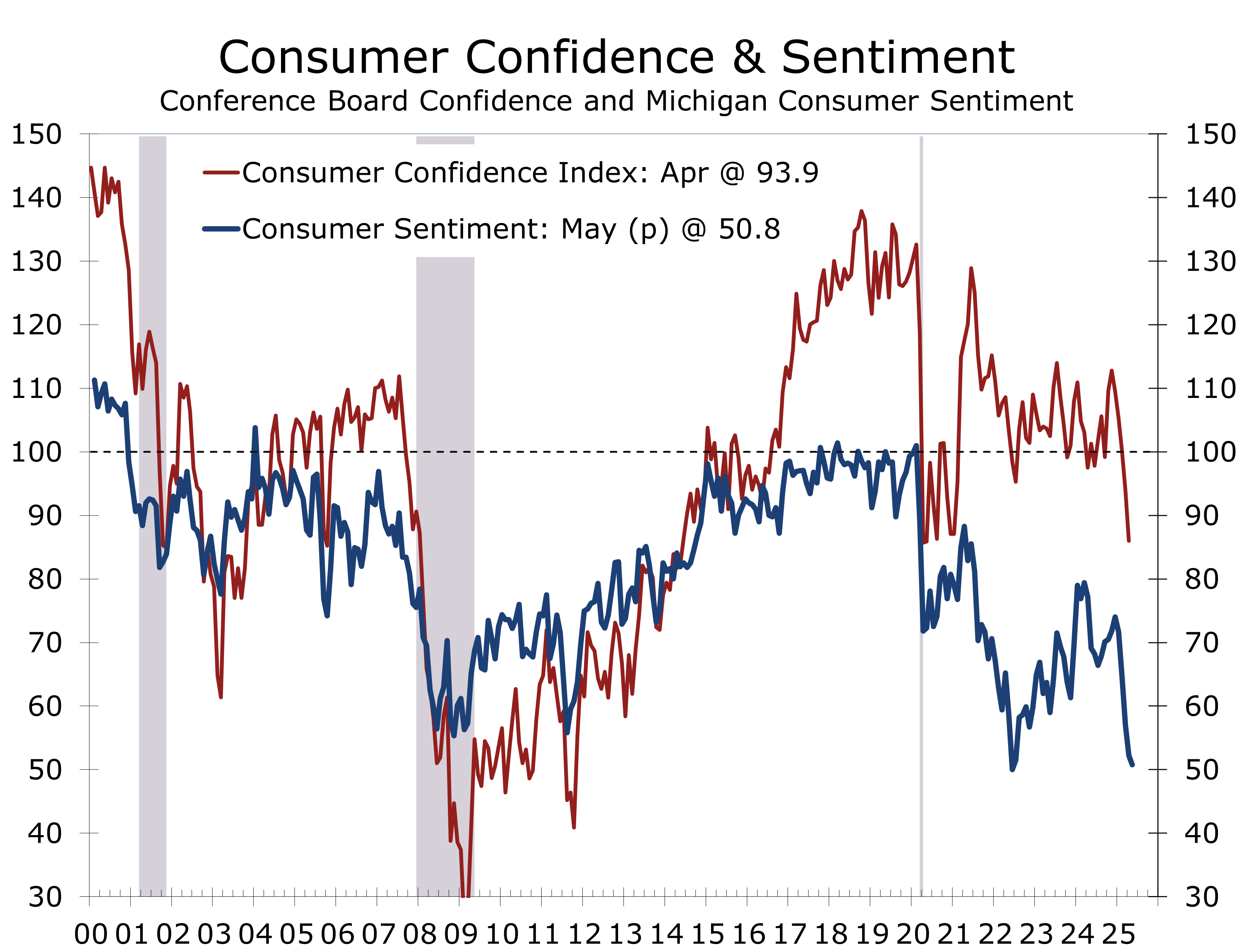

Earlier reports showed builder sentiment fell to a five-month low in May, and single-family starts declined 2.1% in April, pressured by high mortgage rates and construction costs. With the Fed intent on anchoring inflation expectations—especially after the University of Michigan’s May survey showed 1-year inflation expectations jumping to 7.3%—policy looks likely to stay tight even as growth momentum begins to wane.

Moody’s downgraded the U.S. sovereign rating to Aa1 from Aaa, citing decades of fiscal drift. Deficits could hit 9% of GDP by 2035, with debt soaring to 134% from 98% in 2024. Rising mandatory spending and interest costs—set to consume nearly a third of federal revenues by 2035—have eroded the ability to service debt, pushing the interest burden above that of other Aaa peers. Though markets shrugged, the downgrade warns that America’s fiscal credibility is unraveling. Moody’s stable outlook rests on the U.S. economy’s scale, institutional strength, and the dollar’s reserve status—but these pillars no longer fully offset fiscal deterioration. Tough decisions loom ahead.

Tax Cuts vs. Tariffs: A Lopsided Battle

Republicans advanced a reconciliation package with slightly larger tax cuts than expected. Deductions for tips and overtime were expanded, along with enhancements to the 2017 tax law—totaling about 0.2% of GDP. SALT deductibility was also broadened. For corporations, full expensing for domestic factory construction was reinstated, but cuts to green subsidies and offsetting tax hikes left net corporate relief smaller than anticipated.

The fiscal impulse—+0.1pp of GDP in Q4 2025 and +0.3pp in Q4 2026—is no match for Trump’s new tariffs, which will subtract 0.8pp and 0.5pp from GDP over the same period.

A modestly stimulative budget bill passed the House but will likely be tightened in the Senate.

Trump’s Global Pivot: Silicon Diplomacy

President Trump’s successful Middle East tour strengthen alliances and struck a number of new deals. The U.S.-Saudi reset includes a 411k bpd oil output increase in June, defense deals, and over $18 billion in tech and military contracts—Microsoft, Oracle, Palantir, Lockheed, and Raytheon among the winners.

Qatar followed with $4.2 billion in LNG, 5G, and semiconductor JVs. A U.S.-Qatar sovereign tech fund is in the works, positioning Doha as the Gulf’s digital hub.

Progress continued on expanding the Abraham Accords, with Saudi Arabia signaling interest contingent on U.S. defense guarantees, civilian nuclear cooperation, and a more active U.S. role in Palestinian peace efforts. A breakthrough remains possible.

On tour, Trump cast the region’s realignment as a bulwark against Iranian aggression and China’s digital expansion, pitching a “NATO for Networks” concept—tying together cybersecurity, missile defense, and data sovereignty. The pitch speaks to 21st-century threats in a multipolar digital battlefield.

Back home, with the “Big Beautiful Bill” squeaking through the House, Senate Republicans are eyeing changes to mitigate its impact on businesses and find more immediate savings.

Russia-Ukraine: Ceasefire Odds Rise as Costs Mount

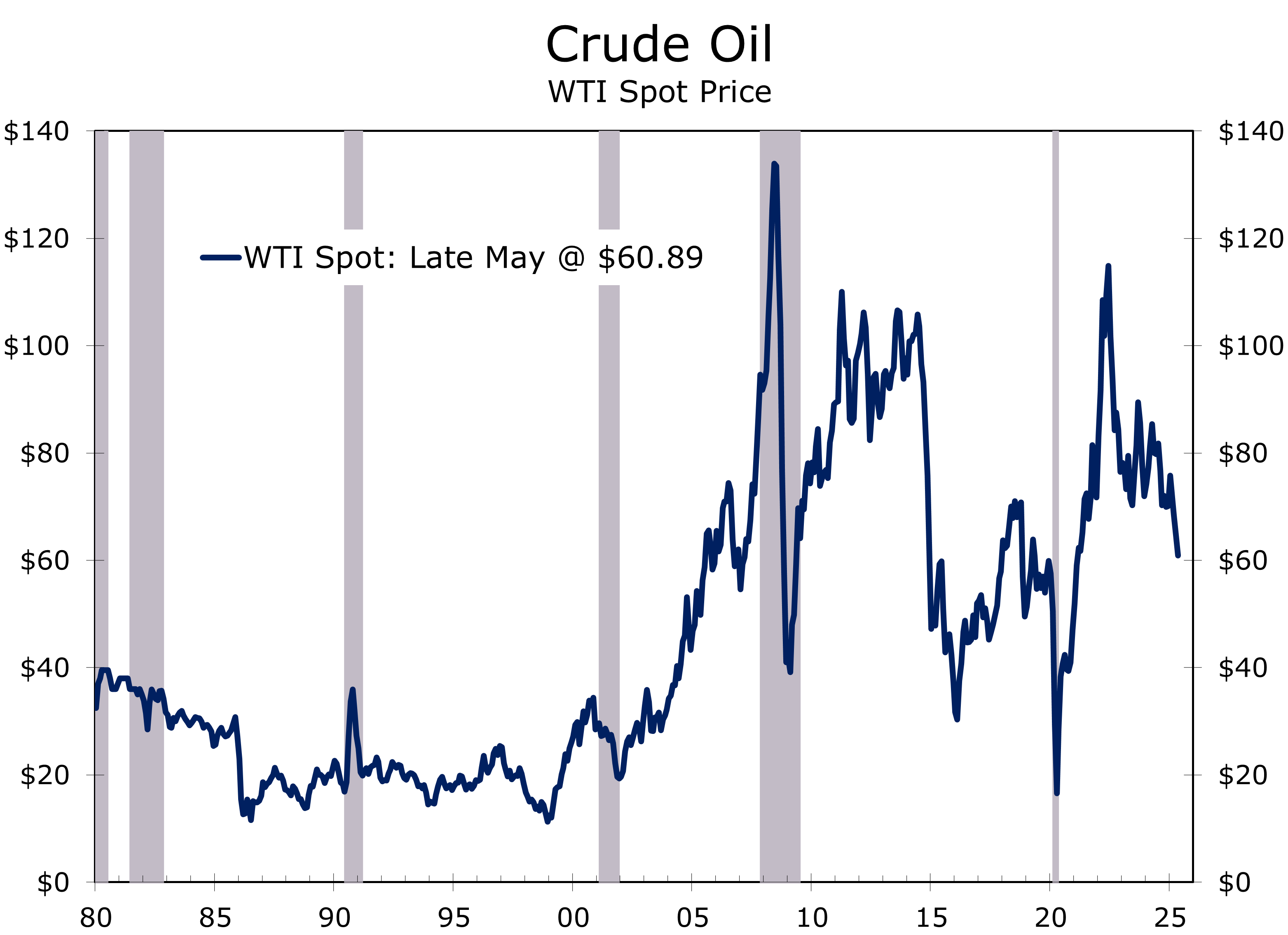

Russia’s war with Ukraine war has become a costly war of attrition. Russia’s economy is buckling—defense spending now outpaces oil and gas revenue, and Brent crude has slipped to $62/barrel. The National Wealth Fund has lost $67B since 2022, debt is nearing one-third of GDP, and interest rates are at 21%. Demographics are another threat: fertility is plunging, and the workforce is shrinking.

Despite widening deficits, Putin is betting on Western war fatigue. Ceasefire momentum may be building, but fresh sanctions could be required to bring Putin to the negotiating table and contain Kremlin ambitions.

China remains Russia’s economic lifeline but is playing hardball on energy and tech. For Moscow, a ceasefire could lock in territorial gains and stabilize the economy. For Trump, brokering one offers foreign policy clout, a potential market tailwind, and a way to lower NATO tensions.

The war has cost Russia $1.3 trillion, over 100,000 lives, and lasting economic damage. Quiet talks suggest Ukraine’s NATO bid is off the table, and neutrality is assumed. But some affiliation with Western Europe also seems inevitable. We had earlier pondered whether Ukraine could attain some sort of observer status within NATO, allowing for cross training with NATO members but no NATO bases on Ukrainian soil. That prospect seems more remote today. Even a formal peace remains distant, but a tactical ceasefire is increasingly likely.

Europe Pushes Back on Populism

Despite forecasts of a hard-right surge, Europe’s center held. Romania elected pro-European Nicușor Dan over nationalist George Simion. Portugal’s center-right outpaced the far right Chega party in parliamentary elections, which gained seats but not much clout. And Poland’s liberal candidate secured a run-off spot against his nationalist rival.

Europeans remain wary of populist instability. Trump’s low favorability and skepticism over U.S. reliability have reinforced centrism. Anti-immigrant rhetoric polls well across the continent, but hard nationalism still spooks mainstream voters.

Trade policy took a volatile turn: President Trump outlined a sweeping tariff overhaul targeting more than 150 countries earlier in the week, with formal notices expected soon. But markets were rattled Friday after he threatened a 25% tariff on imported iPhones unless Apple relocates production to the U.S. He also floated a 50% tariff on EU goods to break the logjam in trade talks. The White House moved quickly to calm markets, which remain cautiously positioned heading into the long weekend.

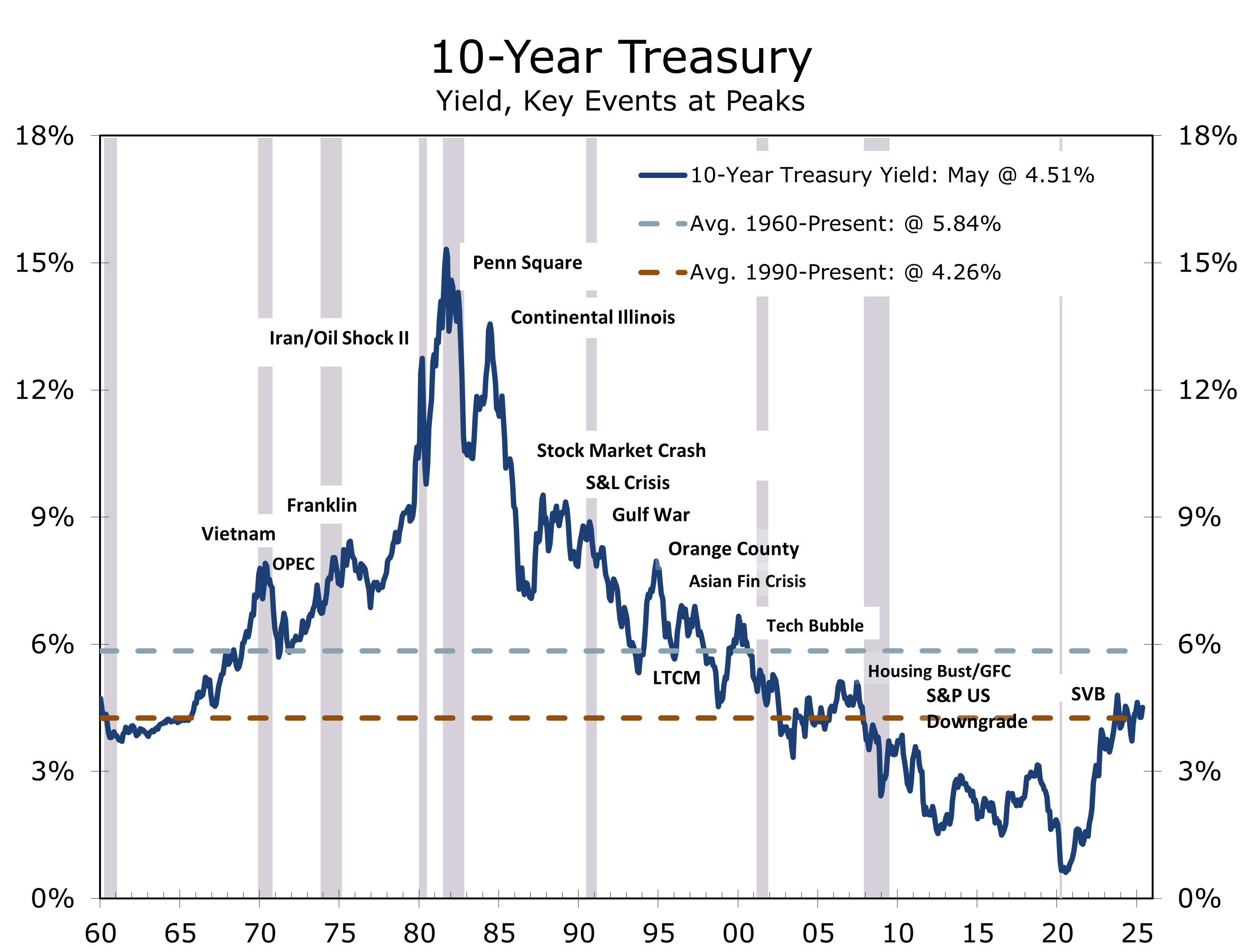

The 10-Year Treasury yield is ending the week just below its highs after a brief spike triggered by soft demand at Wednesday’s 20-Year bond auction—a less liquid, awkwardly placed maturity. In contrast, Thursday’s 10-Year TIPS auction was well received, helping stabilize yields.

Moody’s downgrade and the budget deal had only muted market impact, with investors positioned for worse. The more significant development may be structural: a surge in capital demand from emerging markets positioning as alternatives to China in global supply chains. Investor interest in EMs is now at its highest level since the early 1990s, and this shift could exert upward pressure on U.S. rates over time. We expect the 10-Year yield to trend higher and remain above its average for the past 35 years but well below its longer term average dating back to 1960, which was influenced by the runaway inflation of the late 1970s.

Looking Ahead

(Holiday-Shortened Week)

A full slate of data is due next week despite the Memorial Day holiday. Tuesday brings April Advance Durable Goods Orders and the May Consumer Confidence report. On Wednesday, the Fed will release minutes from the May FOMC meeting. Thursday follows with revised Q1 GDP, April Pending Home Sales, and weekly jobless claims. Friday rounds out the week with April Personal Income and Spending and the final University of Michigan Consumer Sentiment Index.

Key Variables to Watch:

- Core Capital Goods Orders: Watch for continued strength—these have remained resilient through trade headwinds.

- Sentiment Readings: Consumer Confidence and UMich sentiment should rebound from April’s drop, which reflected market turmoil following Trump’s “Liberation Day” tariff rhetoric.

- GDP Revision: Expect a modest upward revision in Q1 GDP, potentially to -0.1%.

- Consumer Spending: April Personal Consumption Expenditures could surprise to the upside. Unlike the Census Bureau’s retail sales, the BEA does not adjust for holiday calendar effects. We believe retail sales—particularly the control group—understated the underlying strength of consumer demand.

- Inflation Data: Core PCE deflator is likely to come in soft. Inflation expectations may ease slightly after their tariff-driven surge.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

May 23, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000