Relief Rally as Trade Tensions Ease

- U.S.–China Tariff Pause: A 90-day rollback sharply reduces U.S. tariffs from 145% to 30%, and China’s from 125% to 10%.

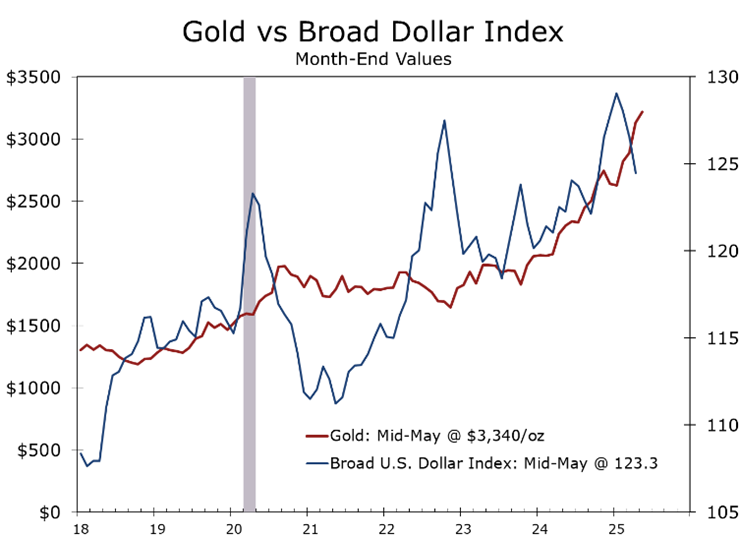

- Initial Market Response: Global equities surged, the dollar strengthened, oil prices rose, and gold fell as investors pivoted to risk assets.

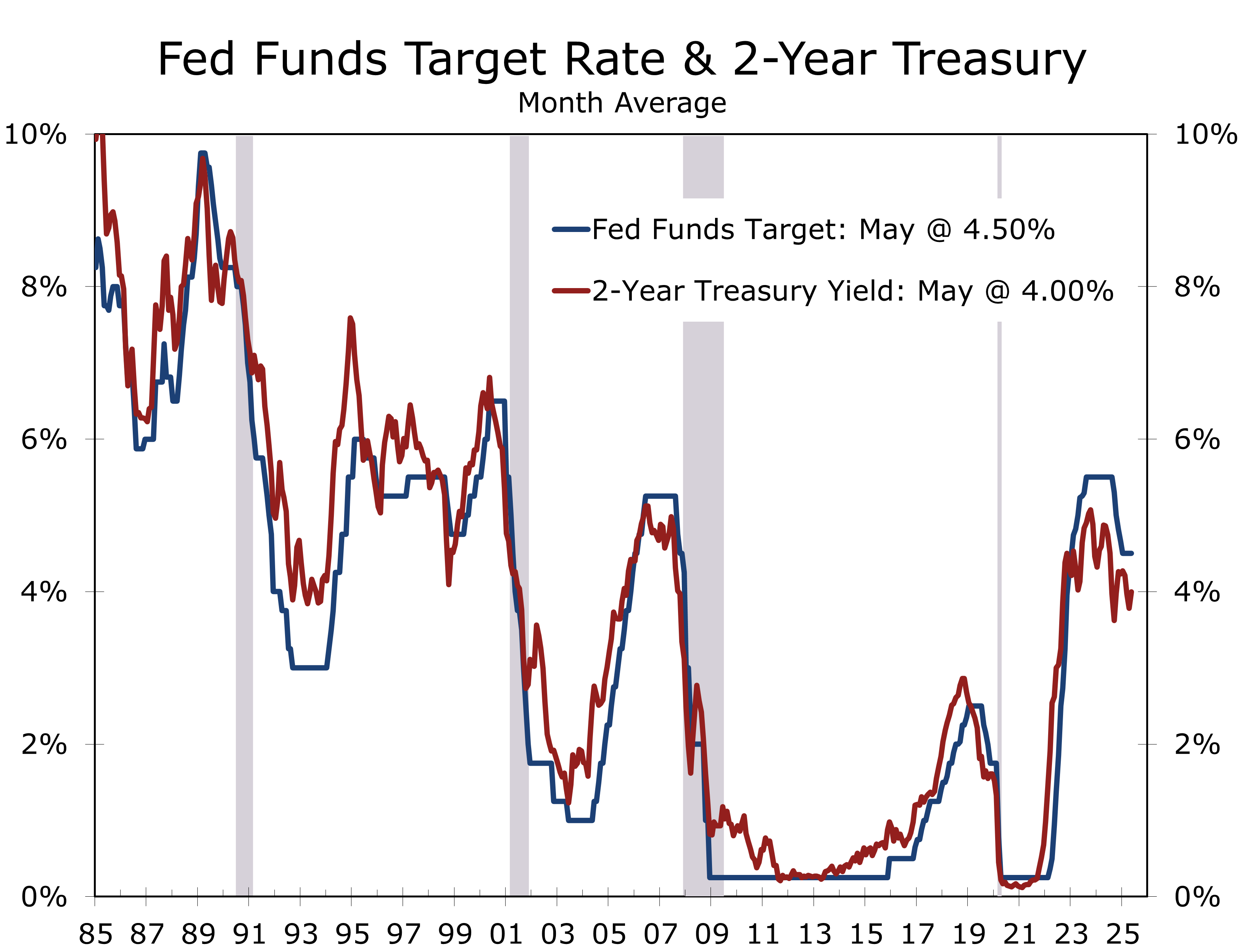

- May FOMC Meeting: The Fed held rates steady at 4.25%–4.50%, citing inflation uncertainty and labor market risks. Core PCE came in at 2.6% Year-over-Year.

- Geopolitical Risks: India-Pakistan conflict erupted over Kashmir, triggering one of the largest aerial engagements since WWII before a U.S.-brokered ceasefire.

- Data Watch: CPI, PPI, retail sales, Fed speeches, and consumer sentiment reports all due this week, with Tuesday’s CPI being the key report.

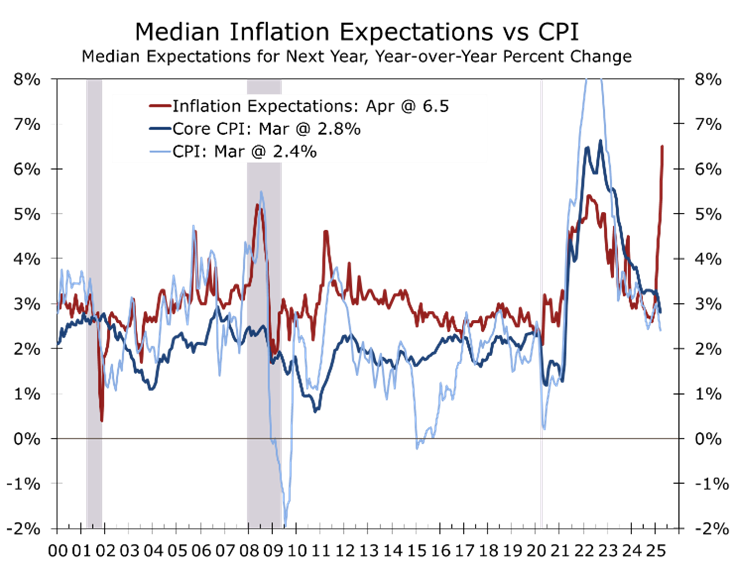

- Market participants will closely scrutinize this week’s CPI report and inflation expectations in the preliminary Univ of Michigan Consumer Sentiment survey for any sign inflation expectations are becoming unanchored.

The U.S. and China have agreed to a significant de-escalation in their trade war by implementing a 90-day pause on heightened tariffs. This agreement, emerging from this past weekend’s Geneva talks, sharply reduces tariffs from extreme levels—with the U.S. cutting tariffs on Chinese goods from 145% to 30%, and China reducing U.S. tariffs from 125% to 10%.

President Trump proclaimed the agreement a total reset—though it likely reflects more of a shift in mindset than a change in principle. The news spurred a surge in global stock markets, sent the dollar broadly higher, boosted oil prices, and reversed some of the recent spike in gold prices as investors shifted to riskier assets. While the immediate market reaction is positive, the agreement marks only a temporary rollback and does not address long-standing trade issues. Still, the two sides appear committed to working toward a more comprehensive deal. Following the latest developments, we slightly lowered our recession probability for this year from 45% to 40%.

This U.S.-China trade deal signals a willingness by China to work to address U.S. grievances.

At its May 6–7 meeting, the Federal Reserve maintained their federal funds rate target at 4.25% to 4.50%, continuing the pause initiated in January after 100 basis points of cuts between September and December 2024. The Fed’s policy statement reflected increased caution, citing persistent inflation pressures and growing risks to the labor market.

Chair Jerome Powell emphasized a data-dependent approach, noting the need for more time to wait and see if the recent soft economic data indicates a meaningful slowdown or is merely noise amid rapidly changing tariff pronouncements. Our read is that it is a little bit of both. Growth is slowing, but the noise around the Liberation Day tariff announcements greatly amplified growing economic anxieties among businesses and consumers. The latest inflation data shows core PCE up 2.6% year over year in March, still above target but trending downward. However, tariffs and related disruptions to trade are expected to lift the core PCE to at least 3% this year.

Trade talks overshadowed a major conflict between India and Pakistan.

While the markets were fixated on the trade talks, India launched air strikes against Pakistan on May 7 in retaliation for a terrorist attack in Pahalgam, Kashmir, that killed 28 civilians. The conflict intensified into one of the largest aerial engagements since World War II, involving over 100 fighter jets and missile exchanges.

A U.S.-brokered ceasefire was reached on May 10, but the situation remains fragile. The conflict underscores the risk posed by Pakistan’s harboring of terrorist groups and their occasional use of those groups to further geopolitical aims—comparable to Iran’s use of proxies like Hamas, Hezbollah and the Houthis. For markets, the de-escalation reduces immediate risk. The U.S. role in mediating the crisis also bolstered confidence in U.S. leadership, strengthening the dollar and pulling gold prices lower.

The temporary ceasefire in the U.S.–China trade conflict has delivered short-term relief to financial markets and granted the Federal Reserve additional breathing room. With no immediate need to adjust policy, the Fed can now take a “wait and see” approach as it assesses incoming economic data and evolving trade dynamics. That patience will be tested this week with a heavy slate of reports and Fed commentary.

Tuesday’s Consumer Price Index (CPI) report is expected to show a 0.3% increase for both headline and core measures. While inflationary pressures remain broad-based, a cooling in shelter inflation could help offset rising costs in auto and home insurance, as well as tariff-sensitive products. Used car prices are likely to fall this month, although recent increases in the Manheim Index suggest upward pressure may reemerge this spring or early summer. Year-over-year, core CPI is expected to hold at 2.8%, but this figure may creep higher in the months ahead.

Markets will also turn their attention to Wednesday’s remarks from Fed Governors Waller, Jefferson, and Daly—three voices with differing policy leanings. Their comments will be closely watched for signs of shifting tone or new forward guidance in light of the recent trade developments. Each brings a unique lens on how inflation, employment, and external shocks like tariffs should influence the Fed’s reaction function.

Thursday delivers a data deluge, headlined by the Producer Price Index (PPI), retail sales, initial jobless claims, and regional manufacturing surveys from the New York and Philadelphia Feds. The regional Fed surveys cover the period from late April through early May and might provide a better assessment of conditions, which worsened at the start of April, following the Liberation Day tariff announcements.

Chair Powell is also scheduled to speak. While Powell has not signaled any immediate changes to policy, he has warned that tariffs may eventually force the Fed into a difficult trade-off: prioritizing inflation fighting or job market support. His remarks will be parsed for any signs that this balance is beginning to shift.

Retail sales should be read in context. The late timing of Easter likely inflated March figures and could suppress April’s readings. The two months data should be averaged together to get a clearer view of the consumer’s trajectory. These figures are seasonally and calendar-adjusted, but distortions from holiday timing remain a persistent challenge.

Friday brings reports on housing starts, import prices, and consumer sentiment. Housing may show modest improvement from the disappointing March data. Inflation expectations will remain a key focus in the Consumer Sentiment data. If consumers believe prices will rise and adjust their behavior, expectations might become self-fulfilling. On the whole, sentiment is expected to bounce after a recent run of declines.

In short, while the tariff pause provides the Fed with a little more time to assess how much of the weakening in the soft data reflects actual changes in behavior. Our read is that consumers are still spending freely, and we see recession risk subsiding. Global leaders and the financial markets are also becoming more comfortable with the Trump Administration, which may temper some of the recent market volatility.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

May 12, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000