Stagflation Fears Persist Despite Resilient Data

- U.S. labor market continued to show resilience in April, with employers adding 177,000 jobs. Soft undercurrents and downward revisions, however, continue to reinforce downside risks

- Q1 GDP fell at a -0.3% annualized pace, but distortions from frontloaded imports and inventories cloud the picture

- Eurozone inflation was firmer than expected but not enough to derail the ECB’s dovish path

- Oil remains under pressure as demand forecasts soften further, and the Saudis boost production while the rest of OPEC+ remains on the sidelines

- Romania swings right, Australia stays center-left in weekend elections and Canada moves slightly further to the left

Last week’s economic developments offered a clear reminder that the apparent resilience in the headlines likely masks fragility beneath the surface. April’s jobs report eased fears of an imminent downturn, with nonfarm payrolls rising by 177,000 and the unemployment rate holding at 4.2%. Downward revisions to prior months reduced the three-month average payroll gain to just 155,000, suggesting the labor market’s forward momentum is weakening.

Wage growth remains solid but is moderating, with average hourly earnings edging up 0.17% in April and up 3.8% year-over-year. The Employment Cost Index slowed to 3.6% in Q1, a trend consistent with the Fed’s inflation goal but one that suggests higher prices may more sharply erode real incomes and abruptly curb spending later this year.

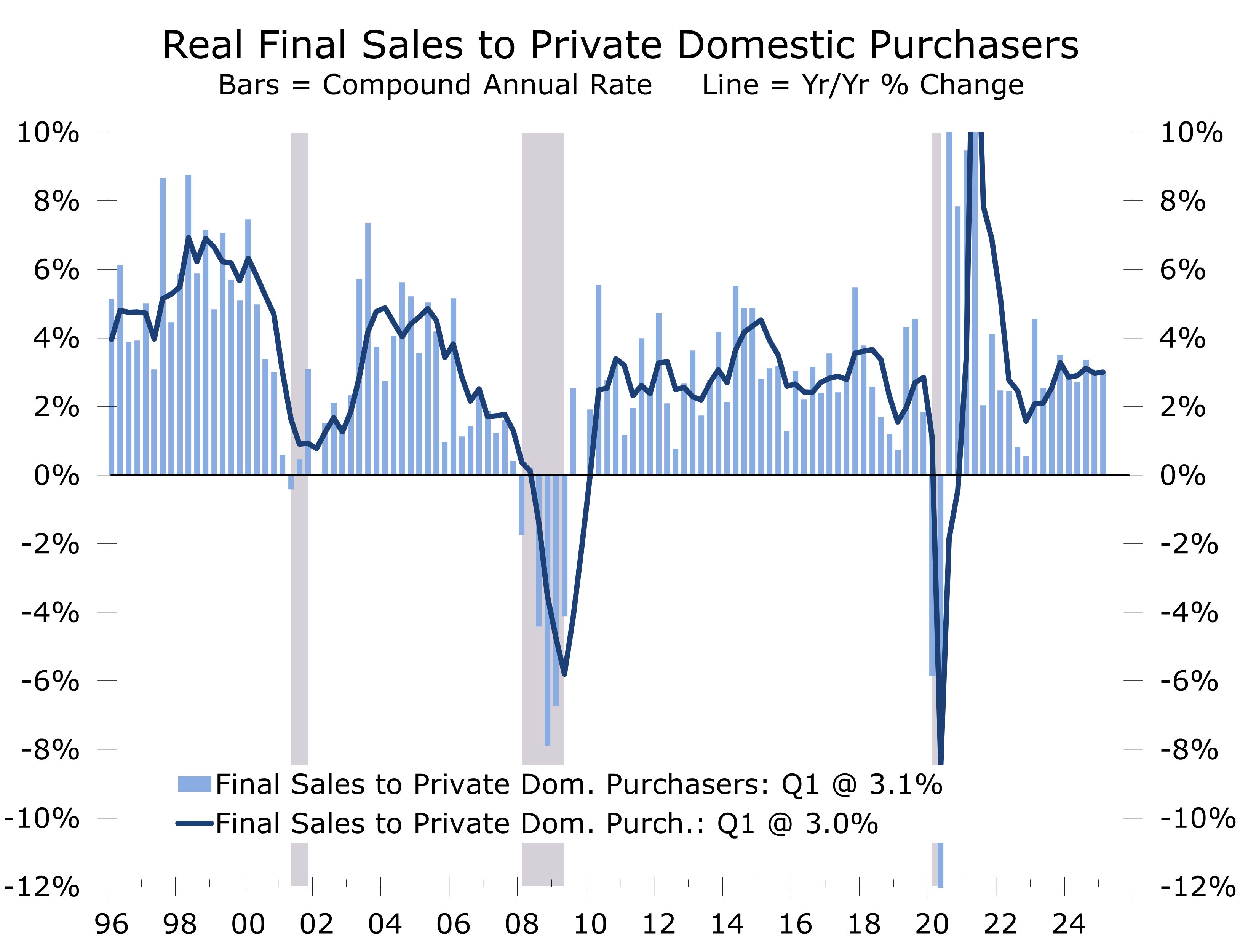

Real private domestic sales offer a clearer view of underlying economic momentum.

April’s soft labor report followed a negative Q1 GDP print, with real growth contracting at a -0.3% pace. While the headline decline raised recession concerns, the composition of growth was more nuanced. A modern-era record 4.8 percentage point drag from net exports—driven by a frontloading of imports ahead of tariff hikes—distorted the overall figure.

Real private final domestic demand, a better gauge of core momentum, rose 3.0% as business investment surged and consumer spending remained resilient despite weather-related disruptions and the unusually late Easter holiday and associated spring break travel. Equipment spending jumped 22.5%, including a historic 70% surge in information processing equipment tied to AI infrastructure, while residential investment added modestly to growth.

Our initial forecast is for Q2 real GDP to rebound to a 2.1% pace as trade-related distortions unwind and inventories normalize. Core demand is likely to cool, with real private final domestic demand slowing to around a 1.6% pace. Some of the strength in consumer spending and business investment was likely pulled forward, as consumers and businesses made big-ticket purchases and investments ahead of tariff increases. Our second-quarter outlook will be influenced by how much the Q1 data are revised. The slight contraction may be revised upward as more complete data on inventories becomes available, which would take away some of the Q2 bounce back.

The April ISM Manufacturing Index underscored the softening tone in U.S. data, falling to 48.7, with new export orders plunging to 43.1—levels reminiscent of the earlier Trump-era trade tensions. While supply chains remain intact, firms continue to cite tariffs and policy uncertainty as intensifying headwinds.

Personal consumption continues to moderate, and inflation is now being driven more by external shocks than overheating demand. In this environment, we expect the Fed to remain restrictive. While the Fed has downplayed surging consumer inflation expectations, their near-term significance might be greater, as consumers rush to purchase cars and other big-ticket items ahead of higher tariffs, pulling prices higher

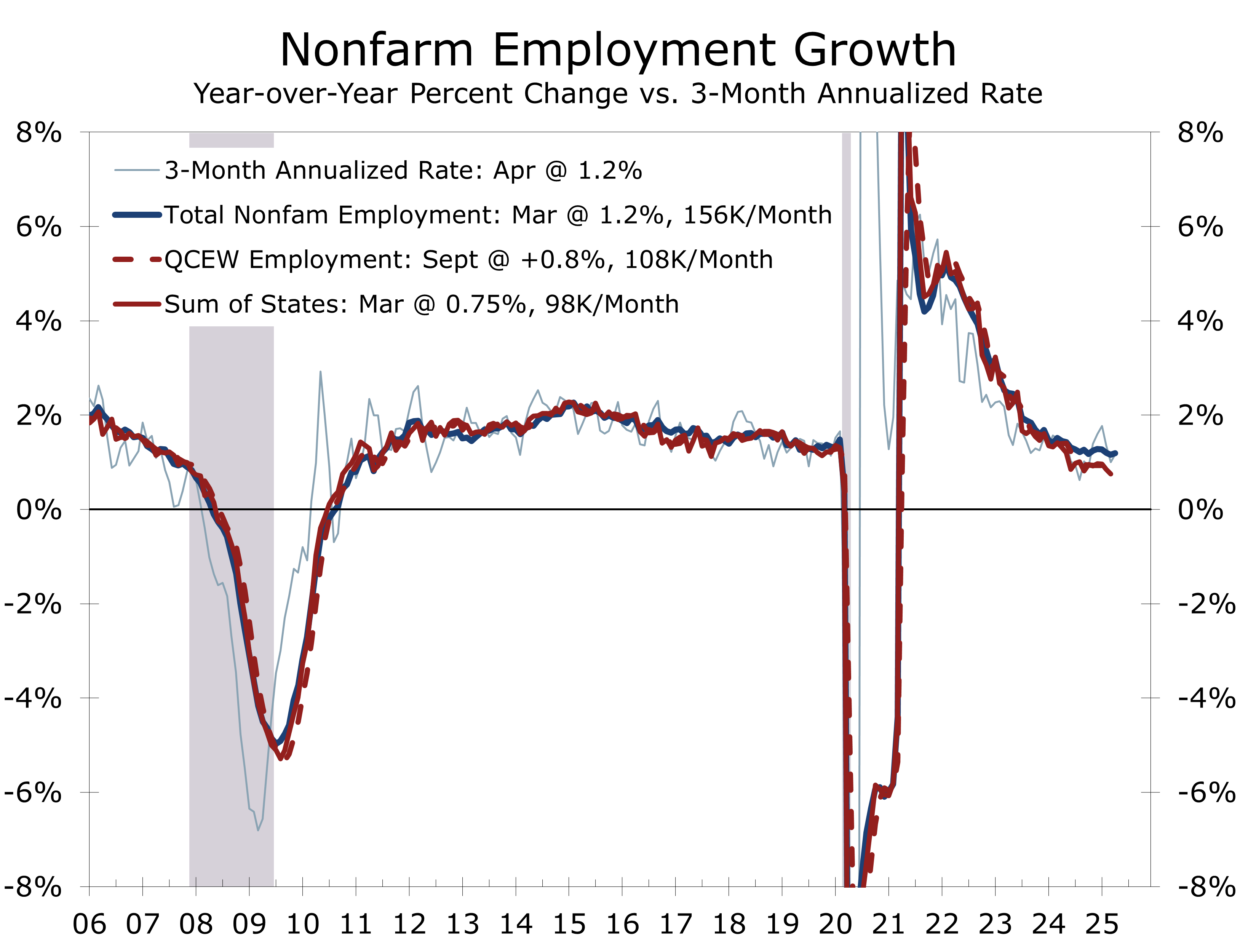

The May FOMC meeting is expected to be uneventful, with a relatively high bar for rate cuts. While Fed officials will keep a keen eye on the soft data, they are unlikely to act until there is some convincing follow-through to the hard data. We maintain a high degree of confidence that this will in fact occur, as we see the true underlying pace of job growth well below the recently published figures—around 100,000 jobs per month—and look for reported job growth to slow enough for the Fed to move forward with quarter-point cuts in July and September.

Our labor market view is reinforced by the recent dive in Consumer Confidence as well as the recent slide in job openings. State level job growth has also recently tracked the QCEW data, implying job growth is running at just under a 1% pace. Consumer surveys also back the notion that it is taking longer for displaced workers and labor force re-entrants to find new jobs.

Soft Eurozone, Diverging Japan

Internationally, the Eurozone’s inflation dynamics supported expectations for ECB rate cuts despite a modest uptick in core inflation to 2.7%. Temporary Easter-related pressures buoyed services prices, but wage growth remains soft. Flash Q1 GDP beat estimates at 0.4% quarter-over-quarter, though trade was the primary driver—a trend likely to reverse as U.S. import demand slows.

.

The Bank of Japan (BOJ) held its policy rate steady at 0.5% and sharply cut its growth forecasts for fiscal years 2025 and 2026, citing weakening exports and heightened uncertainty from U.S. tariffs. Despite these headwinds, Japan remains a G10 outlier: Tokyo’s core CPI accelerated to 3.4% year-over-year in April—its fastest pace in two years—driven by higher food prices and reduced energy subsidies.

The dollar’s weakness has moderated as tariffs are set to reshuffle the global trading system.

Foreign exchange markets remain volatile, reflecting divergent central bank paths and shifting capital flows. The dollar remains broadly supported by interest rate differentials and safe-haven demand, but recent softness in U.S. data has capped its upside. Meanwhile, the euro has struggled to gain traction despite the ECB’s slower pace of easing, and the Japanese yen remains under pressure amid persistent yield differentials—even as FX intervention risk rises. Currency misalignments could further complicate trade rebalancing, especially if U.S. tariffs drive renewed dollar strength and suppress exports.

Commodities, Equities, and the AI Boom

Commodity markets reflect a bearish overall tone. Brent crude remains under pressure from weakening global demand forecasts and rising supply concerns, with recent reports suggesting Saudi Arabia is preparing to ramp up production even as other OPEC+ members stand pat. This move has weighed on prices, which could soon test technical support near $50 per barrel. Lower oil prices could provide modest disinflationary relief in the near term, but they also reflect broader concerns about global growth and industrial demand, particularly from China and Europe.

In contrast, gold continues to benefit from geopolitical concerns, tariff-driven inflation, and safe-haven flows amid slowing global growth.

Equity markets rebounded the past couple of weeks and appear to be pricing in a soft landing. Valuations remain high by most traditional benchmarks, and we believe the markets remain vulnerable from continued volatility on the trade front and a sharper turn in the AI boom, as investment was apparently pulled forward at a faster-than-expected clip in the first quarter.

Geopolitical Spotlight: Romania, Australia, and Strategic Trade Realignments

Two elections over the weekend highlighted divergent political paths. In Romania, the pro-European National Liberal Party (PNL) won key local and European Parliament races, reinforcing NATO alignment and support for EU-backed energy and defense infrastructure. Meanwhile, in Australia, Prime Minister Anthony Albanese’s Labor government won a second term on a platform of cost-of-living relief and green investment, with policy continuity expected in trade and Indo-Pacific security partnerships.

In Canada, the re-election of a Liberal minority under Mark Carney last Monday has fueled expectations for a bilateral U.S.-Canada trade deal sooner rather than later. Reports suggest Canada could offer defense spending increases in exchange for tariff relief. Elsewhere, India continues to gain strategic momentum as a trade and supply chain alternative.

Looking Ahead

All eyes are on the Fed this week, with the FOMC expected to hold rates steady following April’s softer jobs report. The labor market remains firm enough for policymakers to keep the focus on inflation, which they still see as uncomfortably sticky.

Monday’s ISM services index surprised to the upside, rising 0.8pt to 51.6. Business activity slipped but gains in new orders and employment—alongside a jump in prices paid (+4.2pt to 65.1)—suggest tariff-related frontloading might be fueling near-term price pressures. Still ahead: the March trade deficit, consumer credit, Q1 productivity, and jobless claims—which have risen in recent weeks.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

May 5, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000