Inflation Rises Close to Expectations in July

- The headline CPI rose 0.2% in July, following a 0.1% drop the prior month.

- Shelter costs rose 0.4%, driving nearly 90% of July’s overall CPI increase.

- Residential rent rose 0.5% in July and is up a 24.5% from its pre-pandemic level.

- Energy prices were flat, with gasoline prices also unchanged for the month.

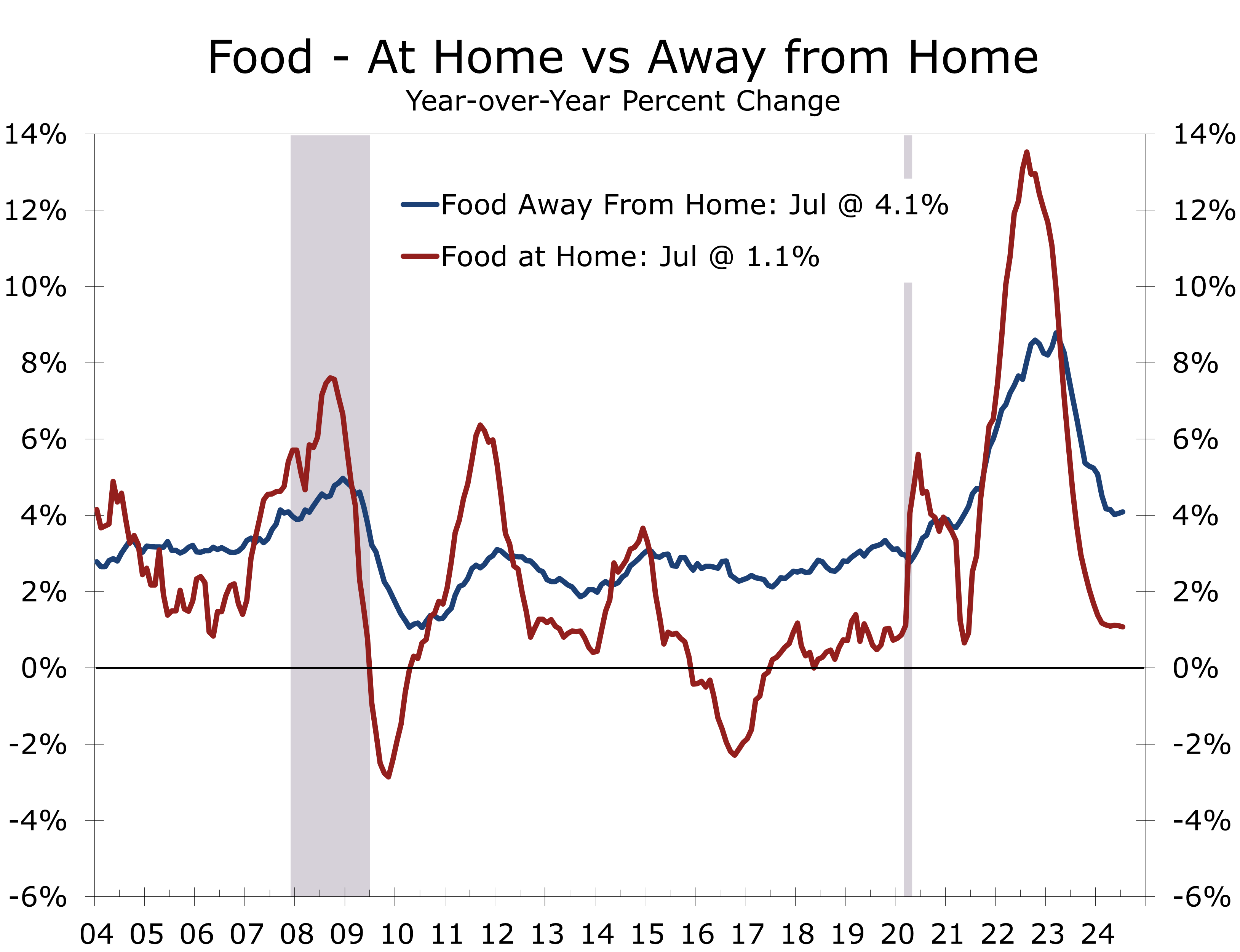

- Food prices rose 0.2%, the same as in June. Prices rose 0.1% at grocery stores, while prices for food away from home rose 0.4%.

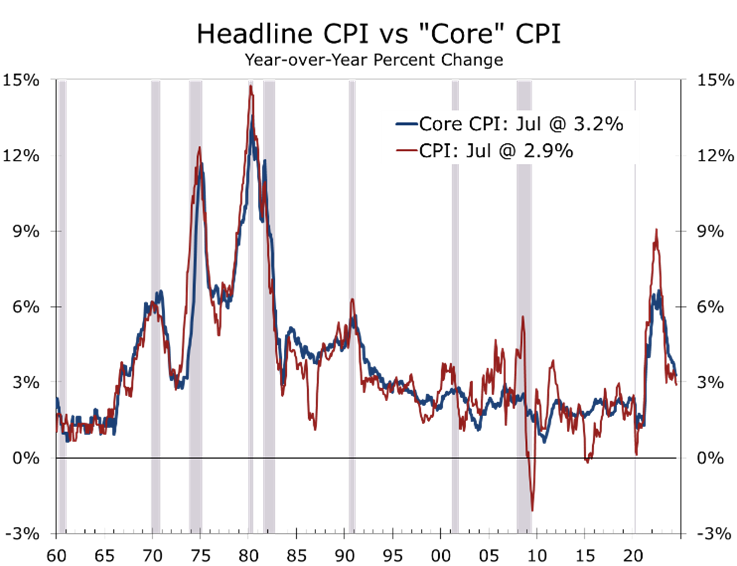

- On a year-to-year basis, the headline CPI fell to 2.9%, the smallest increase since March 2021, while the core rose 3.2%.

- Within the core CPI, transportation costs rose sharply, driven by higher insurances cost. Medical care costs declined slightly.

- Inflation is moderating as anticipated, supporting a potential rate cut in September. Markets remain divided on whether the Fed will begin its easing process with a quarter- or half-point cut, with the Jackson Hole conference offering some possible insights. The key determinant, however, will likely be whether the August jobs data refute or reinforce the message from the surprisingly weak July jobs data.

The Consumer Price Index (CPI) rose by 0.2% in July, following a rare 0.1% decline in June. This modest increase met market expectations, offering some relief after recent inflation data volatility. Over the past year, headline CPI climbed 2.9%, marking the smallest annual increase since March 2021. The core CPI, excluding food and energy, also saw a 0.2% uptick, pushing its annual rise to 3.2%.

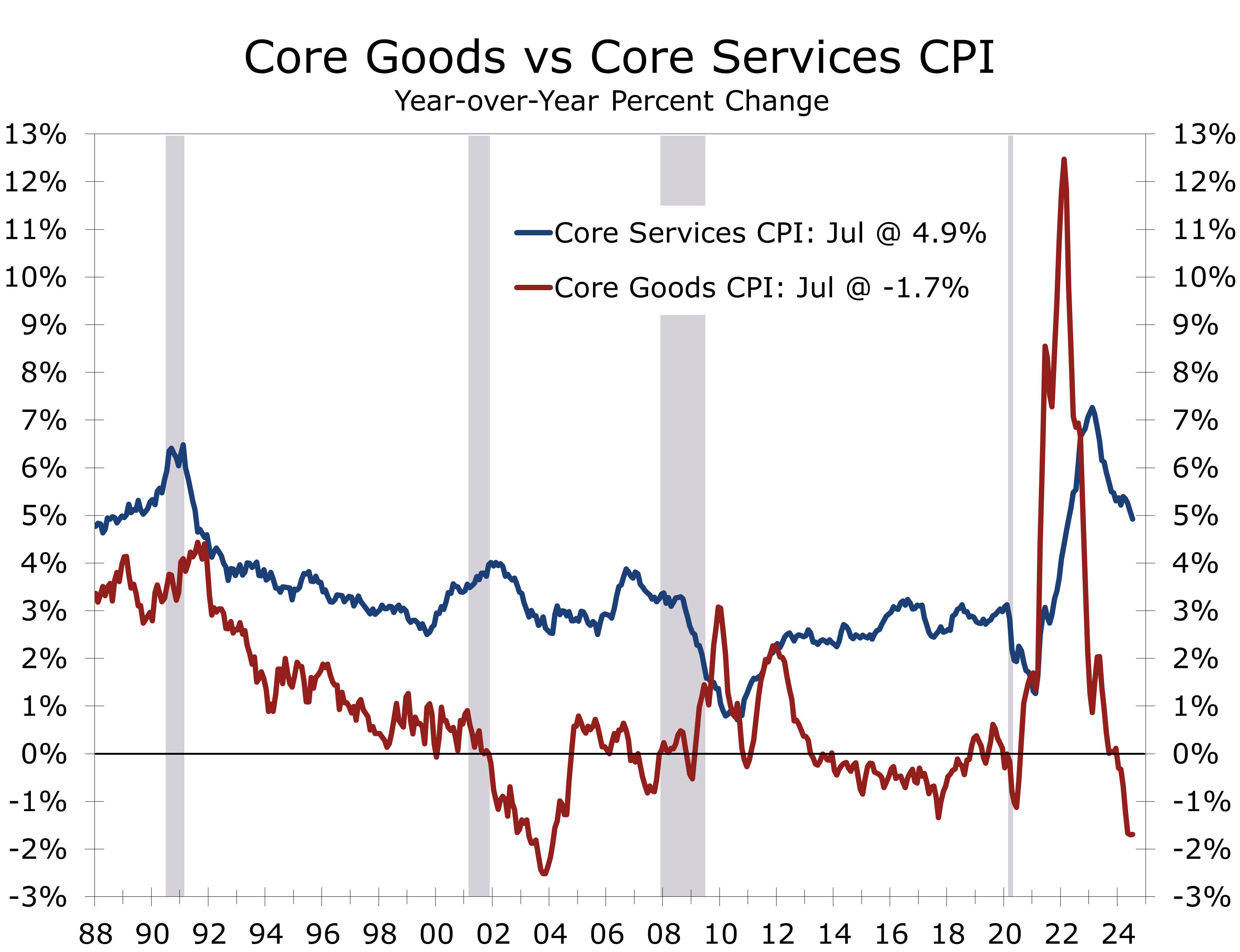

The underlying details of the report show the continuation of a number of important trends. Core goods prices fell 0.3% in July and are now down 1.9% year-to-year. Used car prices tumbled 2.3% in July, following a 1.5% drop the prior month and are now 10.9% lower than they were a year ago.

Inflation continues to moderate in line with expectations, setting the stage of lower rates.

Core services, including shelter, motor vehicle insurance, and medical care, rose 0.3% in July. Service prices continue to be driven higher by rising costs for shelter and transportation services, which both rose 0.4% in July. Prices for medical care services eased 0.3%, driven by a 1.1% decline in hospital services. Despite this, the overall medical care sector remain up 3.2% year-to-year and remains a significant contributor to overall inflation.

Shelter costs remain the biggest hurdle to bringing down inflation. Shelter costs remained stubbornly high in July, with the shelter index rising by 0.4%. This category accounted for nearly 90% of the overall CPI increase. The acceleration in shelter costs was broad-based, impacting tenant rents, owners’ equivalent rent, and lodging away from home. Residential rent, in particular, continues to prove uncomfortably persistent, rising 0.5% in July and climbing a cumulative 24.5% from its pre-pandemic level. High housing costs have likely kept renters in apartments longer, putting upward pressure on renewal rents.

Core services prices are proving resilient, largely due to persistent pressure on shelter costs.

Over the past year, core services are up 4.9%, with transportation services cost surging 8.8% and shelter climbing 5.1%. The persistent rise in core services prices, which are driven by both an overall shortage of housing, higher labor costs, and, in the case of insurance, some catch up from COVID-related price hikes, is a key variable the Federal Reserve continues to monitor closely. The unusual aspects of the post pandemic era have likely meant that the lags between changes in monetary policy and their impact on economic growth and inflation have changed, which is a subject certain to be discussed at the upcoming Jackson Hole monetary policy conference.

The energy index remained flat in July, following two consecutive months of decline. Gasoline prices were unchanged, while electricity and fuel oil posted modest gains. However, seasonal factors put downward pressure on the overall energy index in July. Looking ahead, these factors will reverse in August, potentially boosting the CPI and adding an element of uncertainty to what will be the final inflation reading before the September FOMC meeting.

Food prices rose by 0.2% in July, maintaining the pace seen in June. Grocery store prices rose 0.1% but the underlying data were mixed, with meats, poultry, fish, and eggs increasing, while cereals, bakery products, and dairy saw slight declines. The consistent rise in food prices underscores ongoing inflationary pressures within this category. Prices at restaurants rose 0.2% in July and are up 4.1% over the past year.

The Fed is likely satisfied with the latest CPI print. Our analysis of the CPI and PPI components hints at a downside surprise for the PCE deflator later this month, with the core PCE deflator rising only 0.1% after rounding down. Despite this, we maintain our forecast for just two quarter-point cuts this year, followed by 2 more in 2025.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

August 14, 2024

Mark Vitner, Chief Economist

Piedmont Crescent Capital

704-458-4000

mark.vitner@piedmontcrescentcapital.com