A Humbler Take of the Housing Rebound

-

- Housing starts fell 8% to a 1.434-million-unit pace in June. Sales for May were revised substantially lower, with most of the cut coming from multifamily starts.

- Permits fell less and show less volatility.

- Starts fell in all four regions, with the Midwest seeing an outsized 33.1% drop.

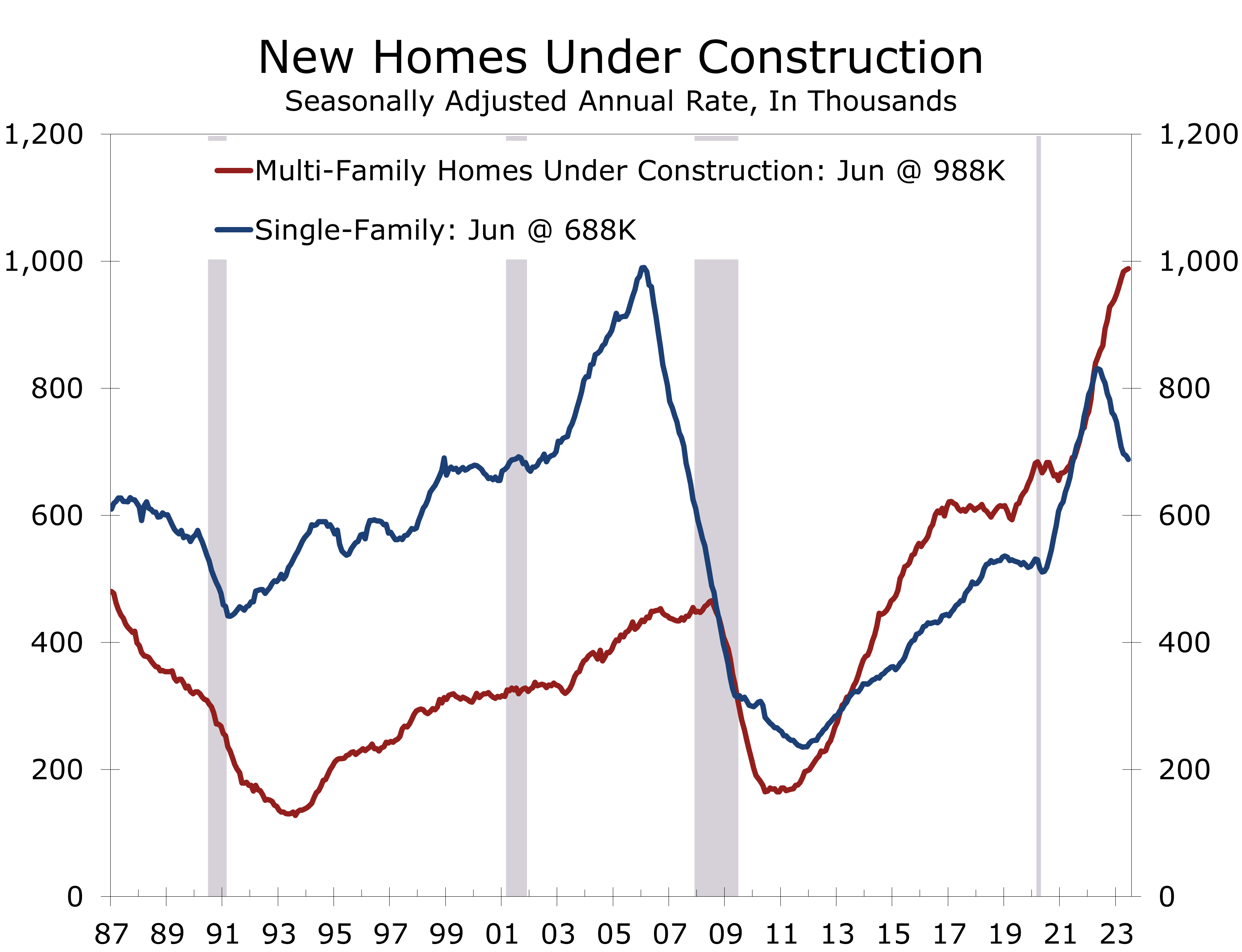

- Housing completions fell 3.3%, and the number of homes under construction edged 0.1% higher to 1.682 million units.

- Most of the backlog is large apartment projects, where cycle times have lengthened.

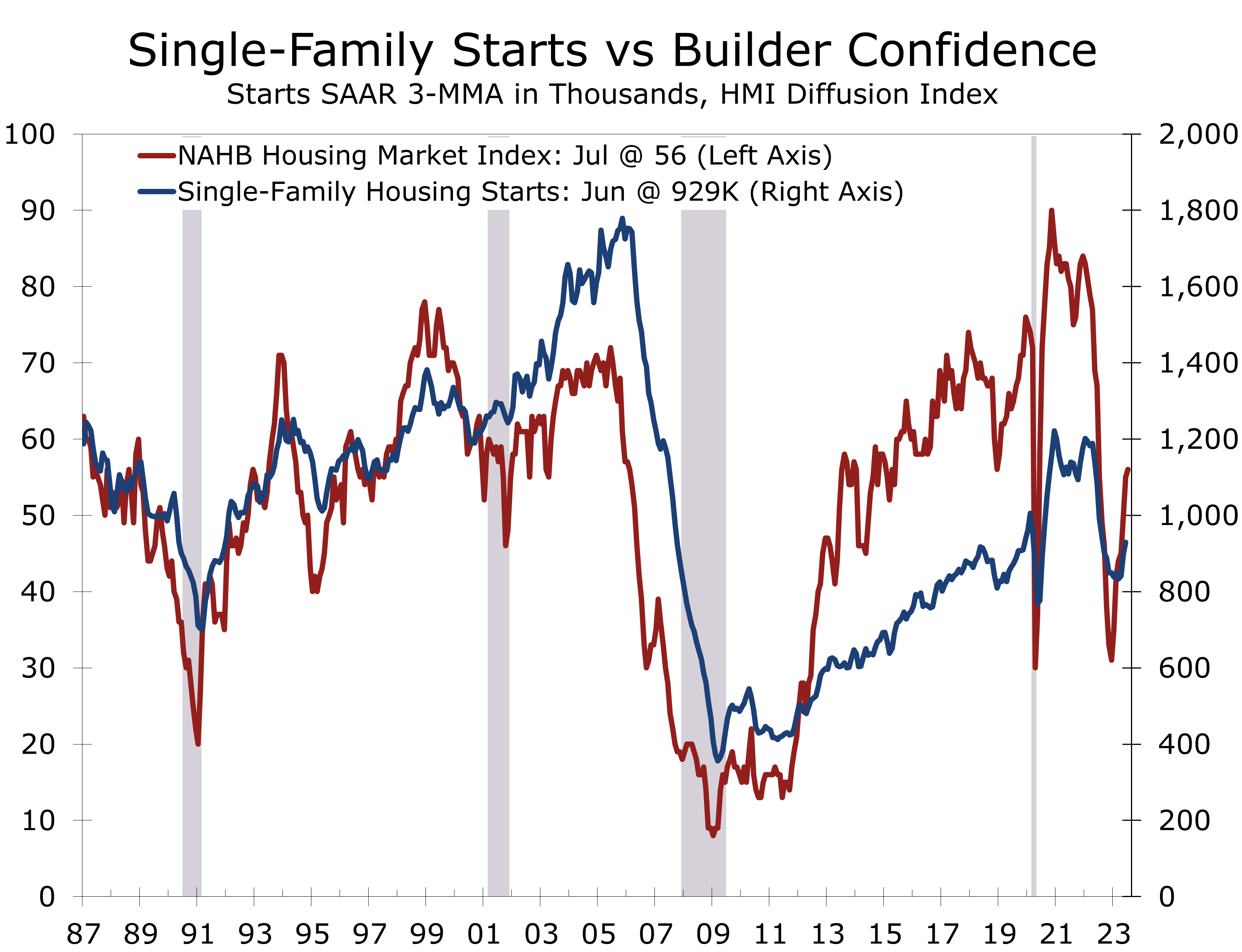

- Homebuilder confidence rose 1 point to 56 in July, marking the 7th straight month of improvement. Present sales rose 2 points to 62, while expected sales fell 2 points to 60.

- June’s data confirm home building cannot defy gravity. Higher mortgage rates and higher prices have severely reduced affordability. While the scarcity of existing homes is sending more buyers to new homes, fewer of those would-be buyers can afford to pay the higher premium for a new home.

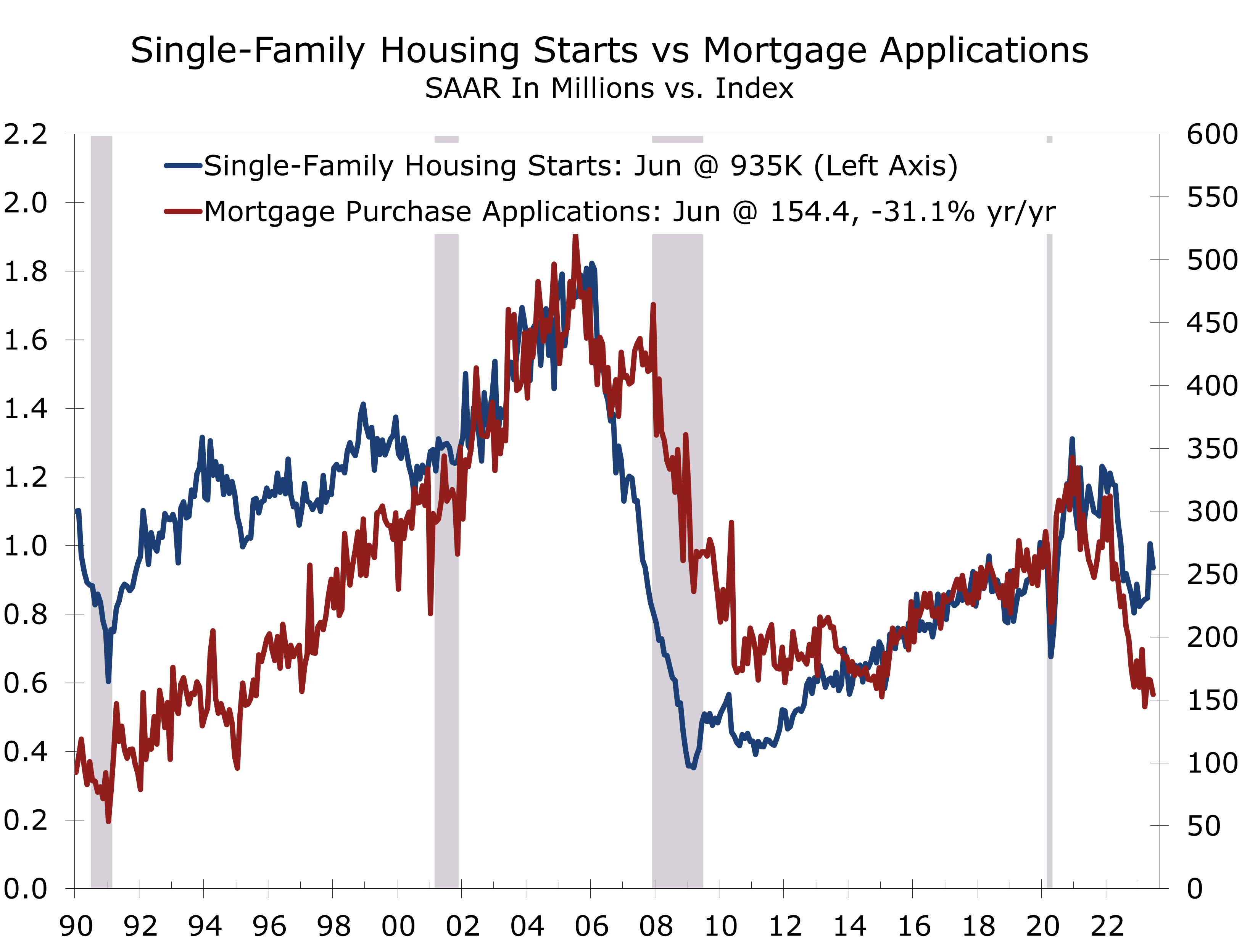

Housing starts fell 8% in June to 1.434-million-unit pace and the previously reported spike in starts for May was revised sharply lower. The June data provide a more realistic assessment of the housing market, which provided a modest upside surprise in the first half of this year. Demand for new homes has been bolstered by the lack of existing homes for sale.

Much has been made of the shift of buyers from existing homes to new homes. The influx of buyers has bolstered builder confidence and allowed them to scale back the aggressive incentives they were offering at the start of the year. Even with aggressive incentives, however, new homes are typically more expensive than existing homes, which means fewer would-be existing home buyers can afford to make the switch to a new home.

Affordability likely took a further hit in June, when mortgage rates rose past 7%. Higher mortgage rates are likely giving some builders pause. Single-family starts fell 7% in June to a still robust 935,000-unit pace.

Softening demand and tighter lending conditions are weighing on multifamily starts.

Multifamily projects accounted for most of June’s drop in housing starts and accounted for the bulk of the downward revision to the May data. Apartment developers are facing softening demand, slower rent growth and tightening lending conditions. The National Multifamily Housing Council quarterly survey noted that 57% of its respondents reported loosening conditions over the past 3 months. Debt and equity financing was also reported to be harder to secure.

The apartment market also faces an avalanche of new supply, mostly in larger markets. The length of time that it takes to complete apartment buildings has been elevated for quite some time. While shortages are responsible for much of the delay, a larger proportion of apartment projects in recent years have been in urban markets, where it is often more difficult to build. Projects have also been midrise or high-rise projects, which typically take longer to complete.

The backlog of apartment projects grew longer in June, with the number of units under construction rising 0.7% to 977,000 units. This marks the largest backlog for multifamily projects stretching all the way back to 1973. While that stat might raise the heartbeat of folks who remember past apartment busts, vacancy rates are considerably lower today than they were back then and housing in general is in short supply. The rub is much of the current backlog is in luxury and lifestyle units. Demand for those units may weaken later this year, as student loan payments resume.

Demand for luxury/lifestyle apartments will likely weaken as student payments resume.

The number of single-family homes under construction fell 0.9% in June to 688,000 units and has fallen 17% since last June. Higher short-term rates add to the sense of urgency to reduce work-in-process inventory.

The June data provide some much-needed improved perception of the state home building. Recent weeks have seen a rash of reports noting that housing had adjusted to higher interest rates. While that is true, housing starts have settled at a much lower level. Overall housing starts through the first six months of this year are down 15% from the first six months of 2022, with single-family starts through June running 21.1% below their year-ago pace. Starts of duplexes, triplexes and quadplexes are down by a similar amount. Starts of projects with 5 units or more are running just 2.1% below their year ago pace.

While single-family starts are down sharply for the first half of this year, they rose sequentially in the second quarter, averaging 929,000 units versus 834,000 in Q1, and will provide a slide boost to second quarter real GDP growth. Moreover, a larger share of home sales in May were for homes not yet started, so the recent pace may have some staying power.

The most recent NAHB/Wells Fargo Housing Market survey shows builders enjoying solid demand. The index rose 1 point to 56 in July and has risen every month this year. Confidence is being bolstered by stronger buyer traffic and less need to offer incentives.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.