Lean Inventories Limit Sales in April

- Sales of existing homes fell 3.4% in April to a 4.28-million-unit annual rate. Sales have fallen in 14 of the past 15 months are down 23.2% over the past year.

- Sales of single-family homes fell 3.5% to a 3.85-million-unit pace, while sales of condominiums and co-ops fell 2.3% to a 430,000-unit pace.

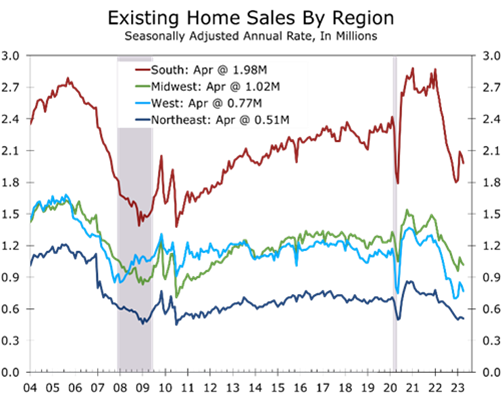

- Single-family sales fell in all four regions in April and are down most in the West.

- For-sale inventory rose 7.2% in April to 1.04 million units and is up 1% from a year ago but remains historically low.

- The median price of an existing home rose 3.6% in April to $388,000 (non- seasonally adjusted) but is down 1.7% from last April.

- Despite the drop, housing affordability remains stretched, with 25.4% of median household needed to make interest and principal payments on a median price home.

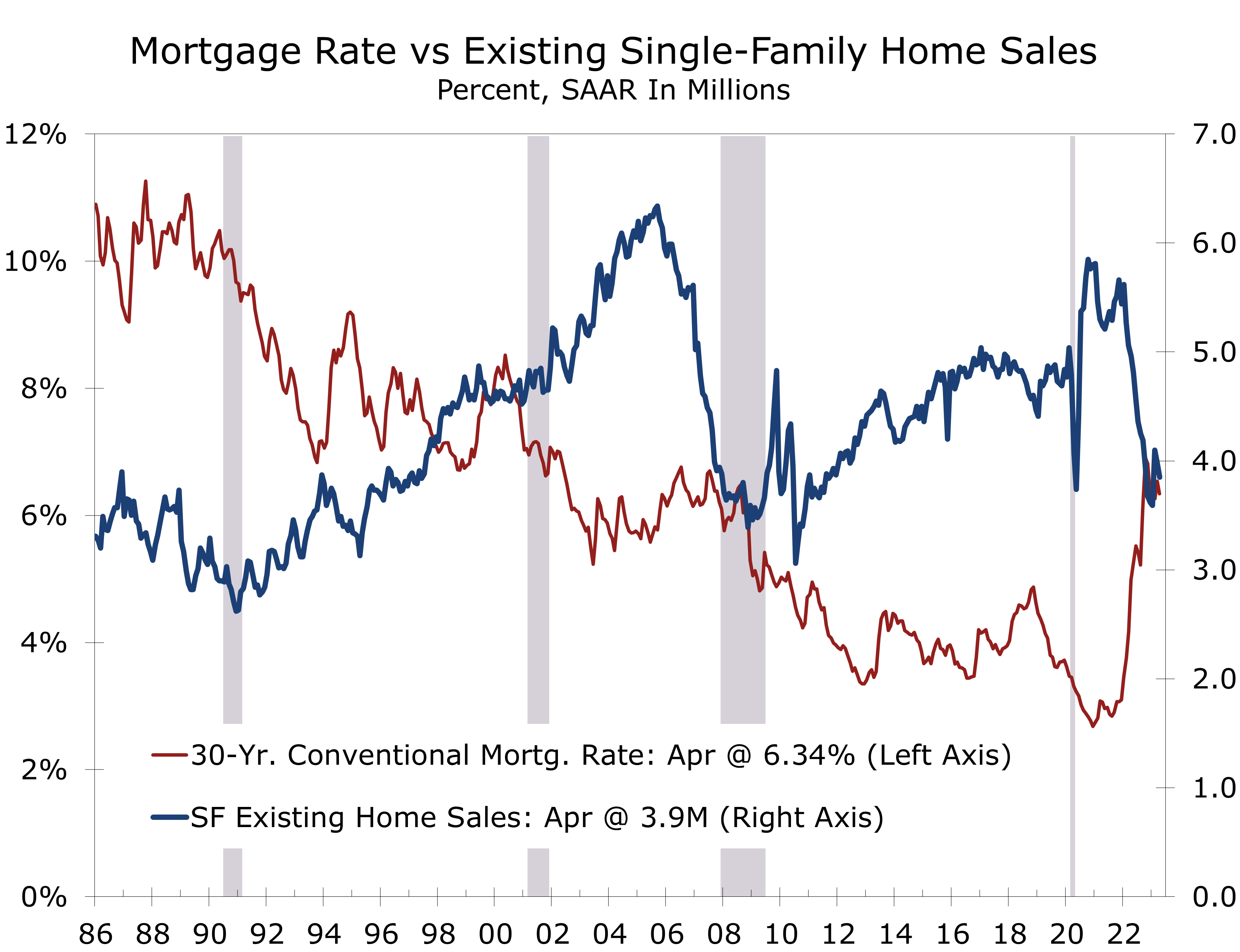

Existing home sales fell 3.4% in April to a 4.28-million-unit annual rate. March sales were also revised lower by 10,000 units to a 4.43-million-unit pace. Demand for homes is stronger than the headline figures suggest. Inventories of existing homes remain exceptionally lean for this time of year, frustrating many would-be buyers and likely boosting sales of new homes.

After spiking last fall, mortgage rates retreated late last year, which brought buyers back into the market in January. Existing sales, which are tallied at closing, jumped 13.8% in February, which is normally a seasonally slow time for sales. With sales picking up earlier than usual this year, sales rose less than usual this spring, resulting in seasonally adjusted declines in March and April. The bottom line is existing home sales have regained some of the strength they lost last fall. Some buyers priced out when mortgage rates surged to 7% last November likely came back into the market when rates fell back near 6%. Sales are still well below their year ago pace, and are unlikely to strengthen in a meaningful way this summer, as affordability is stretched, and inventories remain exceptionally lean.

Affordability remains stretched due to higher mortgage rates and the earlier spike in home prices.

Mortgage rates averaged 6.34% in April, close to their average for the past 35 years. Unfortunately, home prices soared following the pandemic, which made homes unaffordable for a large segment of the population. A home buyer purchasing a median priced home, with a 20% down payment, would need to devote 25.4% of median family income to interest and principal payments, or $1,929/month. The historic average is 19%, or $1,734/month.

Inventories of existing homes rose 7.2% in April to 1.04 million units, which is about 1% higher than they were one year ago. Inventories normally rise in the spring, however, and remain low by historic standards. At April’s sales pace, there is currently a 2.9-month supply of homes on the market, up from 2.6 months in March and 2.2 months in April 2022. The long-time historic norm had been 5 to 6 months but is now widely believed to be around 4 to 5 months.

Given so many homeowners currently have mortgages with fixed rates of 4% or less, the spike in mortgage rates this past year means fewer homeowners are likely to put their homes on the market this spring and summer, which will keep inventories lean and weigh on existing home sales. New listing are down sharply around the country.

The limited supply of homes for sale will support home prices, at least nationwide. After falling 13.2% on a non-seasonally adjusted basis from July 2022 through January 2023, the median price of an existing single-family home has risen in each of the past 3 months. The year-to-year change, however, has fallen to -2.1%, and will likely fall further in coming months as year-to-year comparisons become more difficult through July. Other home price measures, including the widely followed S&P/Case Shiller and Freddie Mac Home Price Index are already firming somewhat on sequential basis and remain up year-to-year.

Sales of single-family homes fell in all four regions of the country during April, tumbling 8.9% in the South and 8.2% in the West. Sales fell somewhat less in the Northeast and Midwest, declining 6.5% and 2.7% respectively.

Single-family home prices rose in all four regions in April on a non-seasonally adjusted basis. Over the past year, however, prices are down 8% in the West and are down 1% in the South. Prices are 2.3% higher year-to-year in the Northeast and up 1.8% in the Midwest. Prices have fallen the most in tech-driven markets, most notably the San Francisco Bay Area and Seattle.

Home prices have fallen the most in the West, with tech centers posting the largest drops.

Recent economic data has come in slightly stronger than expected and, with the turmoil in parts of the banking system seemingly settling down, we are beginning to hear more hawkish sentiment from the Fed. We continue to see a slightly better than even chance the Fed hikes rates again in June but doubt long-term rates will retest the highs hit before the banking problems surfaced back in February. Mortgage rates may firm a bit from current levels but will not likely retest the highs hit last November.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.