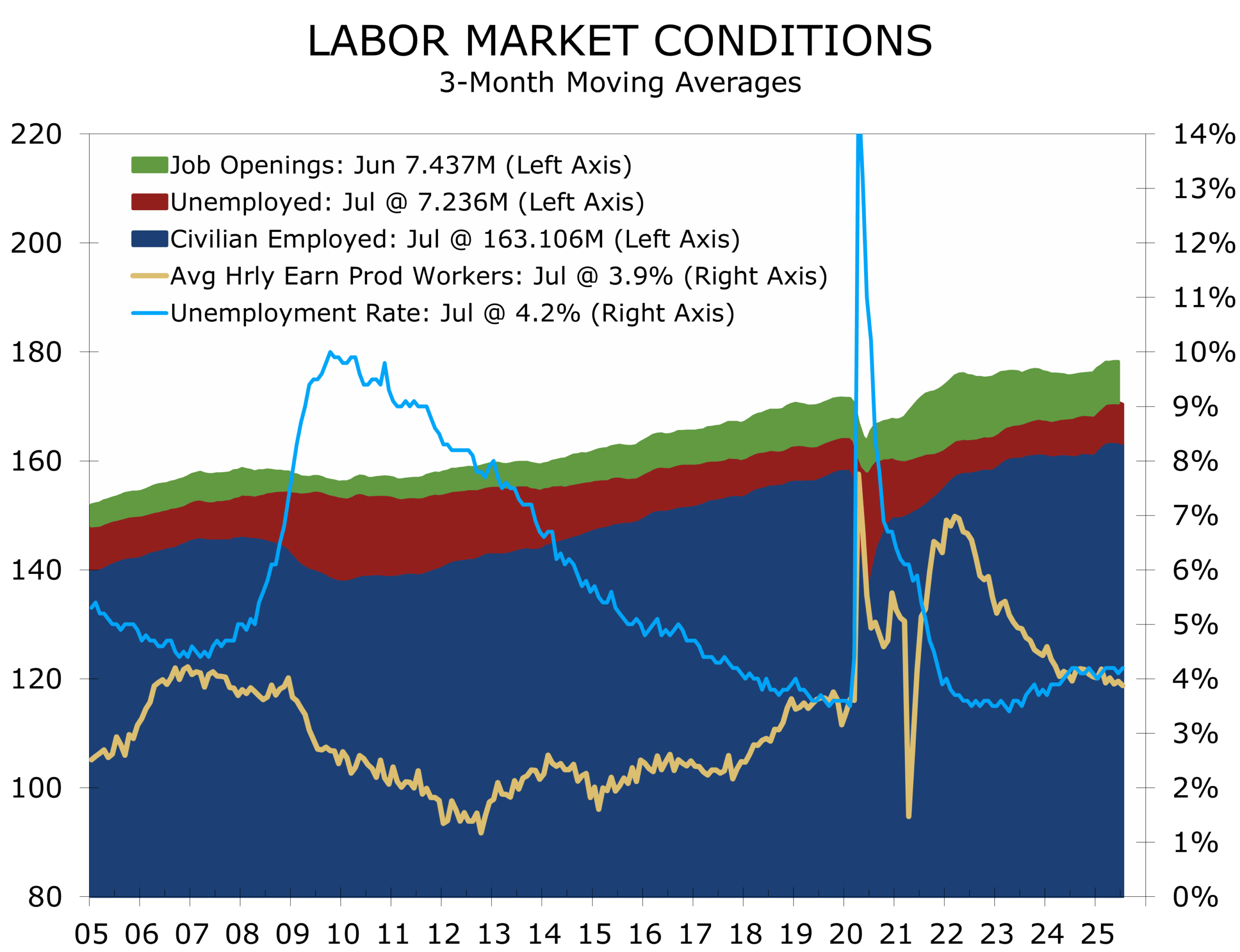

Unemployment is Also Deceivingly Low

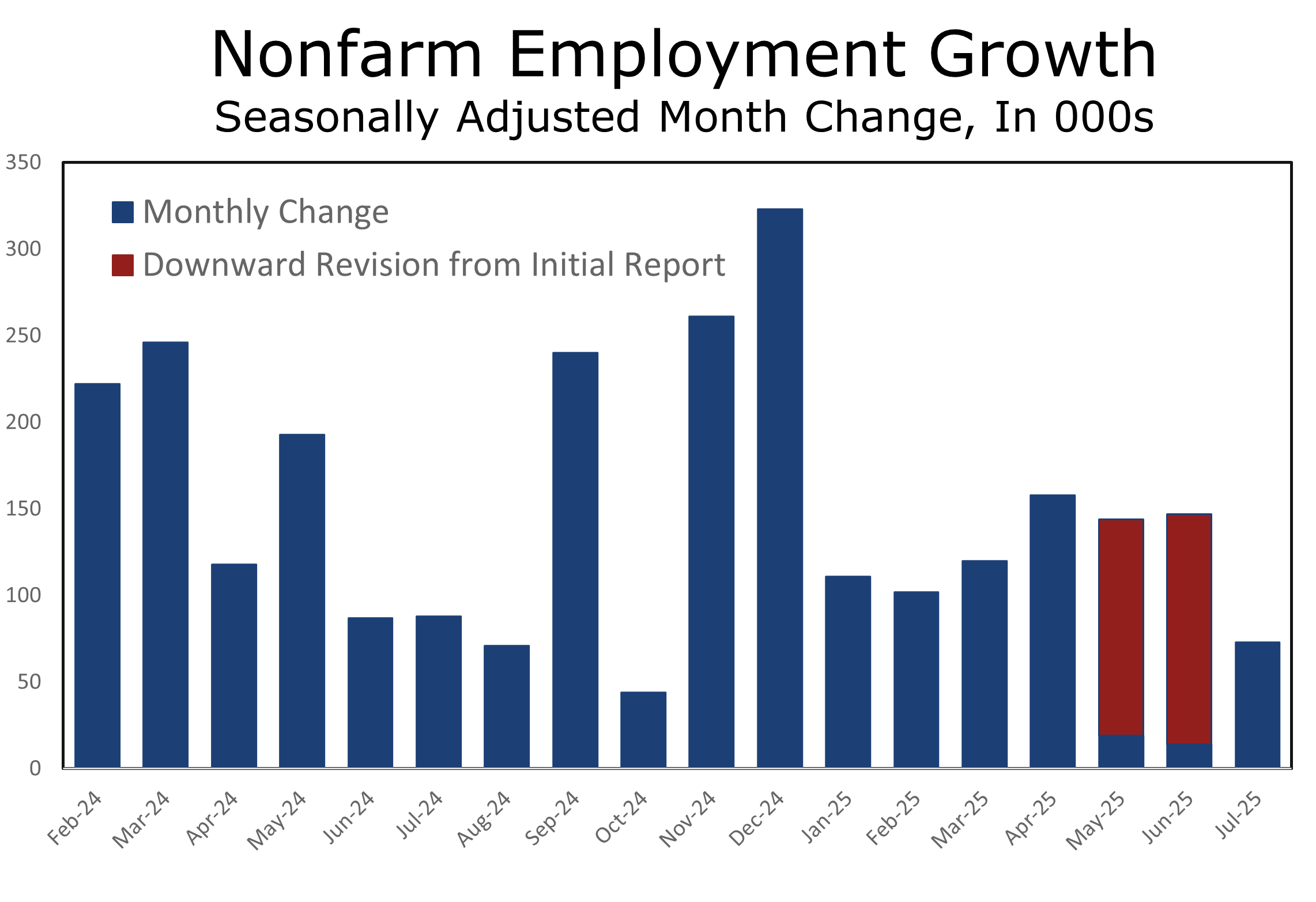

- Nonfarm payrolls rose just 73,000 in July, with steep downward revisions of 258,000 to May and June. The three-month average now stands at just 35,000.

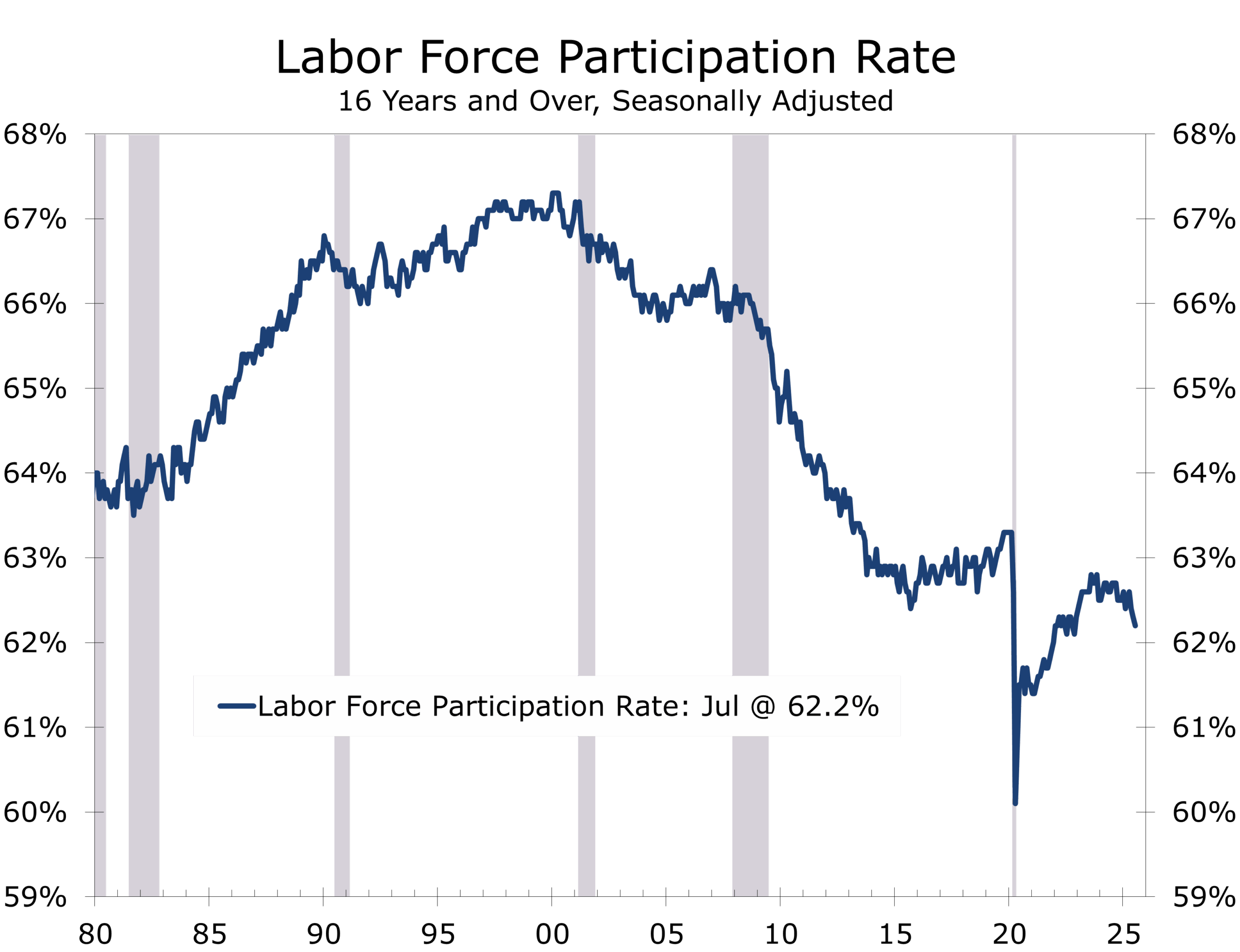

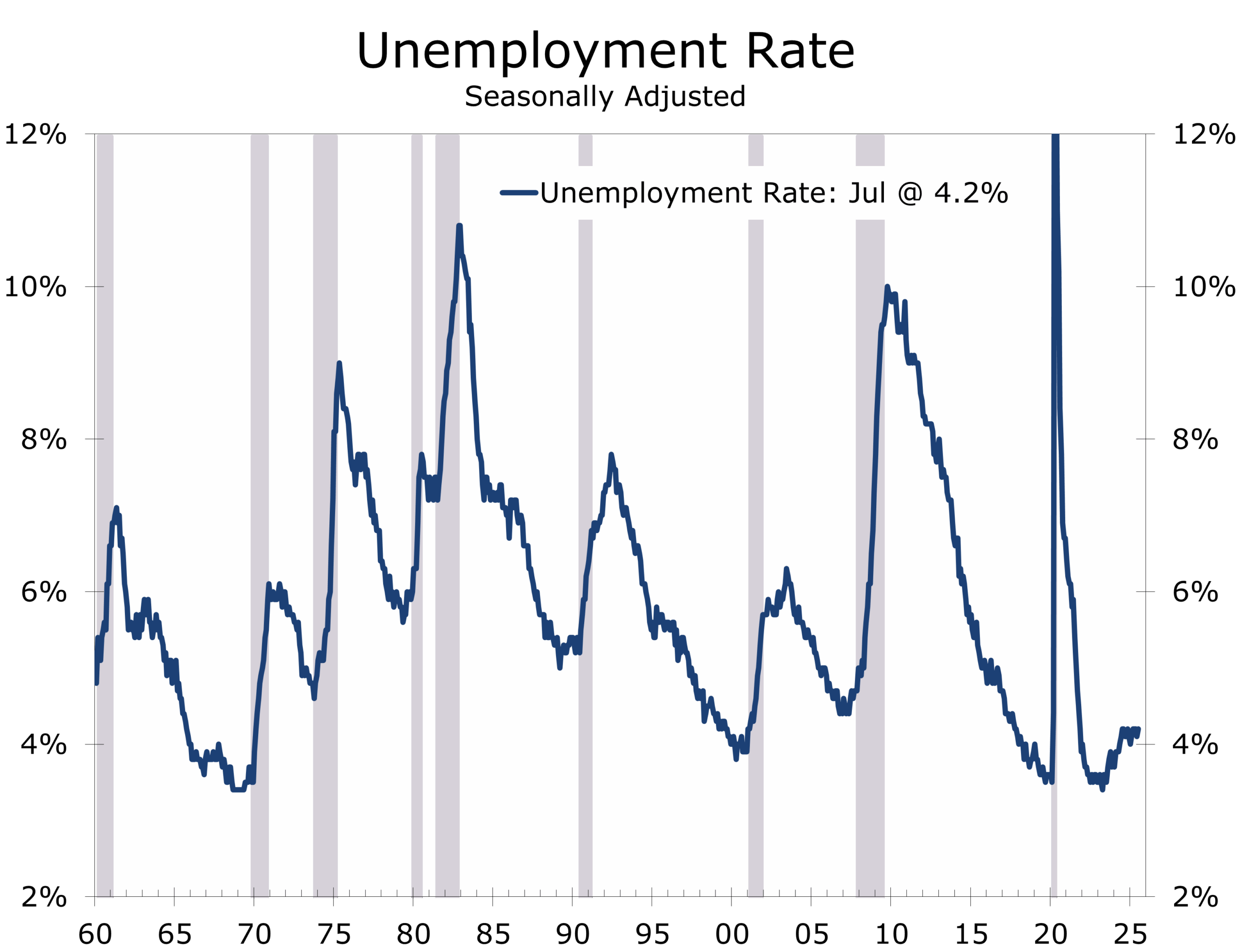

- The unemployment rate rose to 4.2%, but labor force participation fell to 62.2%, the lowest since the pandemic recovery.

- Long-term unemployment rose by 179K to 1.8 million, the highest since early 2022, and accounts for nearly 25% of unemployment

- Payroll gains were narrowly concentrated in health care (+55K) and social assistance (+18K). Most other sectors flat or declining.

- Federal government payrolls fell another 12K in July and are down 84K year-to-date.

- Household survey data showed a loss of 260,000 jobs, while the employment-population ratio slipped to 59.6%.

- Average hourly earnings rose 0.3% in July and are up 3.9% y/y. The workweek edged up to 34.3 hours, within its recent range.

- Tighter immigration enforcement and accelerating retirements have likely constrained labor supply, suppressing the unemployment rate. Adjusted for these trends, the jobless rate would likely currently be between 4.5% and 5%.

A Weak Report with Deceptively Stable Optics

The July employment report reveals a labor market losing altitude at an accelerating pace. Nonfarm payrolls rose a modest 73,000, but downward revisions to May and June erased 258,000 previously reported jobs. Over the past three months, job growth has averaged just 35,000—well below replacement level and consistent with recessionary conditions. When adjusted for likely overstatement in the establishment survey, the underlying trend may be close to flat.

Job gains were once again narrowly concentrated in health care (+55,000) and social assistance (+18,000). Construction, manufacturing, retail, professional services, and information were flat or negative. Federal employment fell by another 12,000 and is down 84,000 year-to-date. Private hiring breadth remained weak, with the total private diffusion index rising only slightly to 51.2 and the manufacturing index slipping to 43.8.

Job growth has become dangerously narrow, and unemployment appears understated.

Labor Force Shrinks, Long-Term Unemployment Rises

The unemployment rate rose slightly to 4.2%, but that low rate masks significant deterioration beneath the surface. Labor force participation slipped to 62.2%—the lowest since the pandemic recovery—while the employment-population ratio fell to 59.6%. These declines reflect both cyclical weaknesses, especially among younger workers, and structural pressures from tighter immigration and an aging workforce.

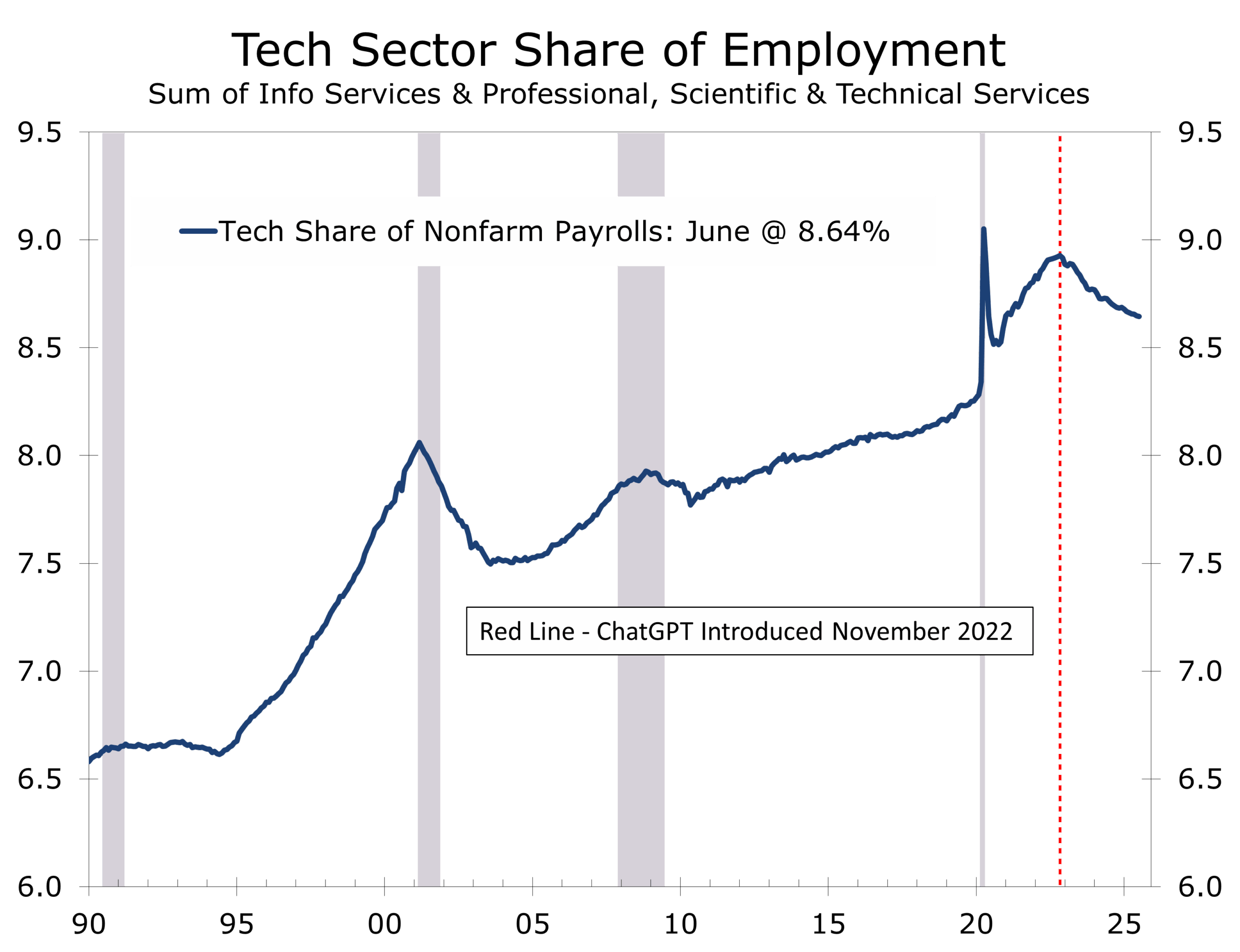

The household survey showed a net loss of 260,000 jobs in July. Long-term unemployment rose by 179,000 to 1.8 million—the highest since early 2022—and now accounts for nearly a quarter of the total unemployed, a troubling indicator historically tied to weakening labor demand and emerging AI-related displacement. Tech’s share of employment has declined since the launch of ChatGPT in November 2022. A narrow subset of tech-related roles we track within information and professional and technical services has now fallen for seven consecutive months, losing 12,300 jobs in July and 33,200 over the past three months.

AI disruption is quietly reshaping white-collar employment—and likely just getting started.

The True Unemployment Rate Is Likely Higher

The official 4.2% jobless rate is not fully reflecting labor market weakness. Structural constraints—particularly tighter immigration enforcement and accelerating Baby Boomer retirements—have limited labor force growth and artificially suppressed the headline unemployment rate. Economists estimate that absent these distortions, the true unemployment rate would be 4.5% or more.

As a result, job gains of just 35,000 a month were enough to stabilize the unemployment rate, whereas in prior years such a low print would have pushed it sharply higher. The decline in labor force participation confirms that the drop in joblessness is increasingly being driven by exits from the labor force, not hiring.

Tariffs and Uncertainty Continue to Weigh on Hiring

The drag from policy uncertainty is growing. President Trump’s latest tariffs—imposed just ahead of a August 1 deadline—have added a 35% duty on Canadian imports and expanded duties on dozens of trading partners. Businesses are reacting with hiring freezes and greater selectivity. Temporary help, retail, and tech services remain weak. The previously reported stability in the factory sector also looks suspect, with revised data showing a bit more weakness.

The Fed has the evidence to cut—waiting may turn the slowdown into a downturn.

A September Cut Might be Too Late

Downward revisions, rising long-term unemployment, flat household employment, and a declining participation rate all point to a labor market steadily losing steam. We estimate payrolls are overstated by about 50,000 jobs per month, suggesting employment may have actually declined in both May and June—back-to-back drops are rarely seen outside of recessions. The Fed now has sufficient data to justify a rate cut by September; the real question is whether waiting that long will prove too late. There was a time when the Fed would act decisively after a clearly weak jobs report. This may be one of those moments.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

August 1, 2025

Mark Vitner, Chief Economist

(704) 458-4000