Economic Uncertainty in 2025: Trade, Jobs, and Growth

- Concerns over President Trump’s various tariff initiatives and efforts to reduced government spending have led to heightened uncertainty, which has weighed on consumer and business confidence. This has led businesses to increase imports, postpone investments, and reduce hiring, ultimately resulting in significantly lower forecast for GDP growth this year.

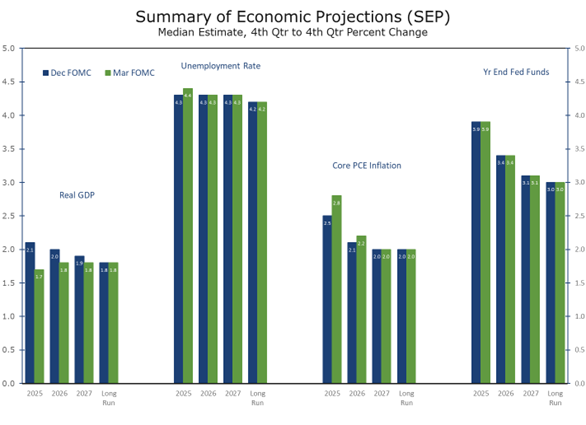

- The Federal Reserve’s initial assessment of President Trump’s tariff increases indicates that core PCE inflation is projected to rise 3.0% in 2025, a 0.5 percentage points faster than their previous forecast. Simultaneously, the median GDP growth estimate for 2025 was lowered by 0.4 percentage points to 1.7%. Chair Powell also made note of heightened uncertainty apparent in the economy today, and implied that the Fed would proceed cautiously.

- While increased inflation and decreased GDP growth forecasts have raised stagflation concerns, these worries are likely premature, as both inflation and unemployment remain historically low. We define stagflation and provide some benchmarks that provide some context to assess this threat. We also examine the risks of recession by various measures.

- Tighter U.S. immigration policy has significantly reduced net immigration into the U.S., which is weighing on labor force and employment growth. Industries that are expected to be most impacted include leisure and hospitality, construction, healthcare and agriculture. Overall job growth is expected to slow in coming months, reflecting the smaller contribution from immigrants and reduced hiring by the federal government.

- Geopolitical risks remain high and will continue to influence the outlook. Progress on a ceasefire between Russia and Ukraine has been modest but remains promising. Israel has halted aid into the Gaza strip, renewed air attacks on Hamas and moved troops back into Gaza. The U.S. has also increased attacks on the Houthi’s and is moving two carrier groups to the area. One key near-term risk is that Israel moves to destroy Iran’s nuclear weapons facilities, which might lead to some disruptions in oil supplies from the Middle East and higher global oil prices. Tariffs remain the dominant geopolitical concern, with hopes rising for a lighter touch on reciprocal tariffs.

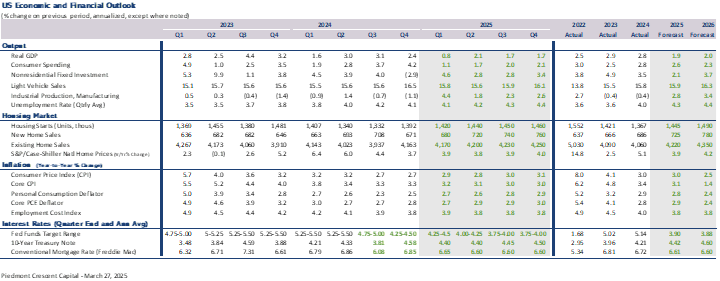

- We are now looking for real GDP to grow at just a 0.8% pace in the first quarter and just 1.9% for 2025 as a whole, on a calendar year basis. On a fourth quarter to fourth-quarter basis, our 2025 forecast is slightly below the Fed’s, at just 1.6%. Job growth is expected to weaken notably over the next few months, which we believe will open the door for two quarter-point rate cuts this summer, and possibly a third this fall.

The March Federal Open Market Committee (FOMC) meeting reaffirmed the Federal Reserve’s cautious, data-dependent approach, holding the federal funds rate steady at 4.25%-4.5% while slowing the pace of quantitative tightening (QT). The Fed also announced the runoff of maturing Treasury securities will decline from $25 billion to $5 billion per month, while mortgage-backed securities runoff remains at $35 billion. This adjustment reflects the Fed’s intent to maintain ample liquidity while navigating evolving economic risks. With growth moderating and inflation proving more persistent, the FOMC remains comfortable waiting to assess the full impact of recent and upcoming policy shifts before making further adjustments.

The Fed’s updated Summary of Economic Projections (SEP) suggests a more stagflationary outlook. The 2025 GDP growth forecast was downgraded to 1.7% from 2.1%, while core PCE inflation expectations rose to 2.8% from 2.5%. Despite the median dot plot continuing to signal two 25-basis-point rate cuts in 2025, a growing number of FOMC participants now see fewer cuts, with eight members expecting less than 50 basis points of easing. Chairman Powell acknowledged the rise in short-term inflation expectations, particularly in response to tariffs, but emphasized that a hawkish pivot would require a broader and sustained unanchoring of long-term inflation expectations. While the University of Michigan’s measure of long-term inflation expectations has increased, Powell downplayed its significance, noting that other indicators remain stable.

Financial markets responded positively to the Fed’s measured approach, with the 10-year Treasury yield initially declining by 10 basis points and equities rallying. The financial market’s improved post-meeting tone has carried over, even amidst continued volatility on various tariff proposals. The decision to slow QT is expected to provide additional support to the economy, particularly by keeping long-term yields in check, which may offer relief to the housing market as it enters the spring selling season.

The Fed may be underestimating labor market risks, as hiring trends point to a weakening job market. QCEW data suggests employment growth through last September was overstated by about 550,000 jobs. If payrolls decline further and unemployment exceeds 4.4%, the Fed might be forced into more aggressive rate cuts. However, persistent inflation—especially from tariffs—may constrain policy flexibility and delay easing until late this year or even 2026. While some compare the Fed’s updated outlook to the 1970s stagflation, those fears seem overstated. Even with slower growth, unemployment is expected to peak at 4.5%, and inflation should remain below 3%, both close to the Fed’s long-run objectives and far from the crisis levels of that earlier era.

We continue to believe that full-fledged stagflation is unlikely. For stagflation to take hold, inflation would need to rise at least one percentage point above the Fed’s 2% target and either persist or show signs of further acceleration, while unemployment would have to rise a full percentage point above the Fed’s full-employment threshold of 4.3% and remain elevated or continue increasing. This sets the minimum stagflation threshold at 8.3%. Current conditions are still well below that level, with inflation at 2.8% and unemployment at 4.1%, which is still below the full-employment threshold. Additionally, solid productivity growth is helping contain inflationary pressures and preventing a wage-price spiral.

The Misery Index, which combines inflation and unemployment, provides a useful gauge of stagflation risk. At 6.9%, it is still well below the 8.3% threshold. Even with our forecast of unemployment rising to 4.4% and core PCE inflation reaching 3.0% by year-end, the Misery Index would only rise to 7.4%. By contrast, during the stagflationary periods of the 1970s and early 1980s, the Misery Index routinely exceeded the high teens due to exceptionally loose monetary policy and major demographic shifts, particularly the influx of baby boomers and women into the workforce. Today’s inflationary pressures stem from more temporary factors—tariffs, supply chain disruptions, and fading pandemic stimulus.

If stagflation risks were to rise, the Fed would face a difficult choice: tighten monetary policy aggressively to control inflation at the cost of higher unemployment and a potential recession or tolerate higher inflation at the risk of unanchoring inflation expectations. Historical precedent favors decisive action, implying higher interest rates. If the Fed were to allow inflation to persist, the eventual costs of bringing it back down would likely be higher. Fortunately, today’s environment is different. Inflation expectations remain well-anchored, and the Fed’s measured approach to rate cuts reflects its strategy to balance inflation risks with risks to the labor market.

Given current conditions, we expect the Fed to maintain policy flexibility—responding as needed to prevent a temporary rise in inflation from becoming entrenched while standing ready to ease if labor market conditions deteriorate. This underpins the Fed’s pause in lowering interest rates. The next move is still more likely to be a rate cut rather than a hike, but the timing has become less certain, with financial markets still expecting two quarter-point cuts this year, albeit with less conviction than before.

Retail sales experienced a significant decline in January, with the headline figure contracting by 0.9% alongside a broad-based pullback across key categories. While adverse weather and seasonal adjustment factors played a role in the reduction, the widespread weakness indicates a softer start to Q1 consumer spending. A major contributing factor was the downturn in auto sales, while discretionary categories—such as sporting goods, furniture, and building materials—witnessed the steepest declines. Additionally, non-store retail sales, primarily online, decreased, prompting questions about whether weather alone was responsible for January’s weakness.

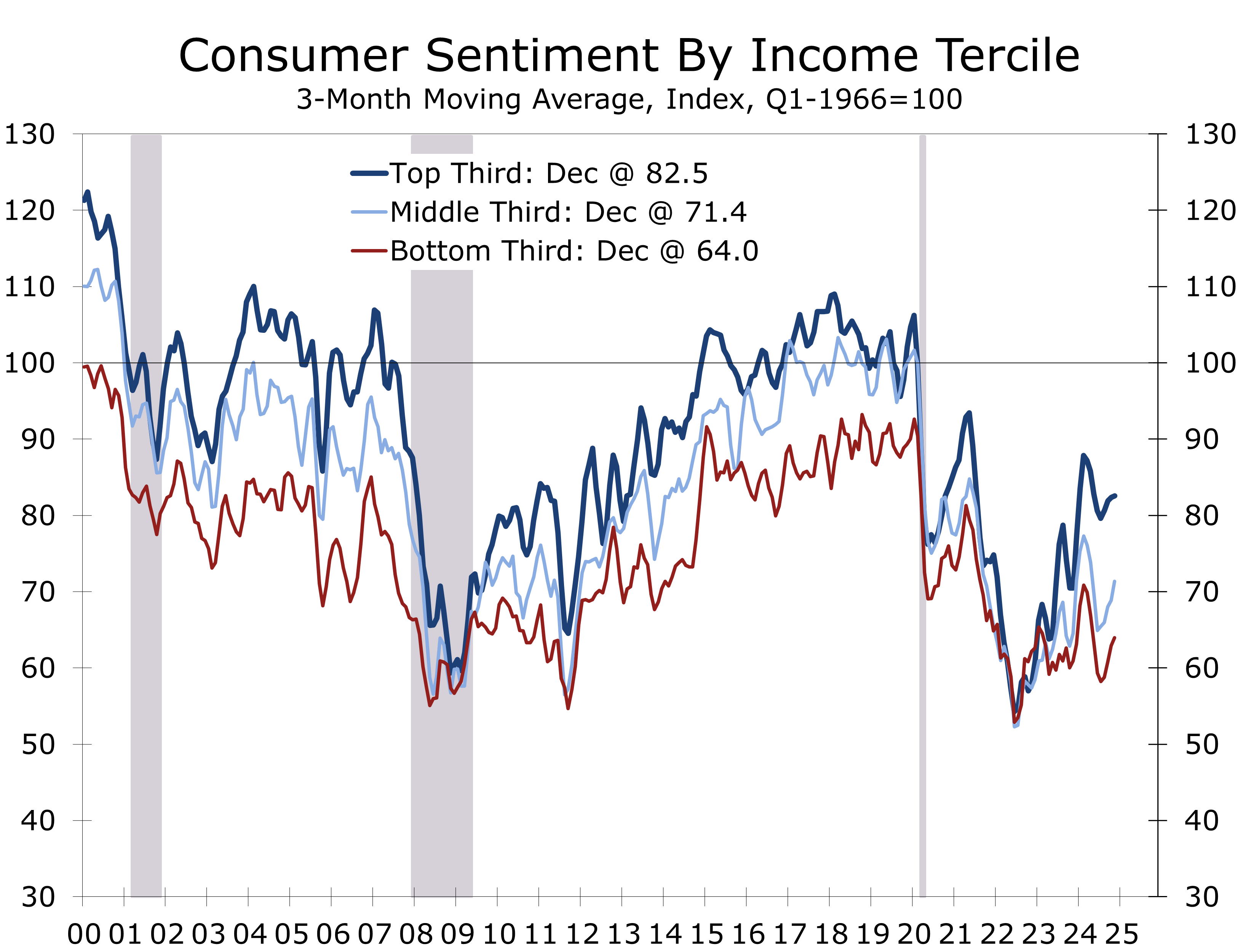

Consumer sentiment has continued to deteriorate in early February, reflecting increasing policy uncertainty. With excess savings largely exhausted, current spending relies more on employment and income growth. Elevated grocery prices and rising insurance costs are likely significant contributors to the decline in sentiment. Consumers’ assessment of current conditions has dropped 6.4 points since December to 68.7, while expectations for future economic conditions—which have a closer link to actual spending—have fallen by 6.0 points to 67.3.

The University of Michigan’s consumer sentiment survey highlights particular weakness among lower-income households. Sentiment for the lowest income tercile has decreased to 64, matching the levels seen during the depths of the Global Financial Crisis. Middle-income households are only slightly more optimistic, with sentiment at 71.3. These figures suggest that economic uncertainty and rising costs are disproportionately affecting consumers with tighter budgets, posing a potential obstacle to discretionary spending.

Despite these concerns, underlying fundamentals support consumer spending in 2025. The unemployment rate remains low at 4%, and weekly jobless claims are near historic lows. Wage growth is robust, and household balance sheets—along with slightly lower interest rates compared to a year ago—should provide some support. Low-rate financing incentives are expected to sustain light vehicle sales and big-ticket spending.

However, financial strength is not evenly distributed across income groups. Rising costs for necessities are disproportionately impacting lower- and middle-income households, putting pressure on discretionary spending. Given these dynamics, we have slightly reduced our estimate for Q1 consumer spending and continue to anticipate a below-consensus gain of just under a 2% annual rate.

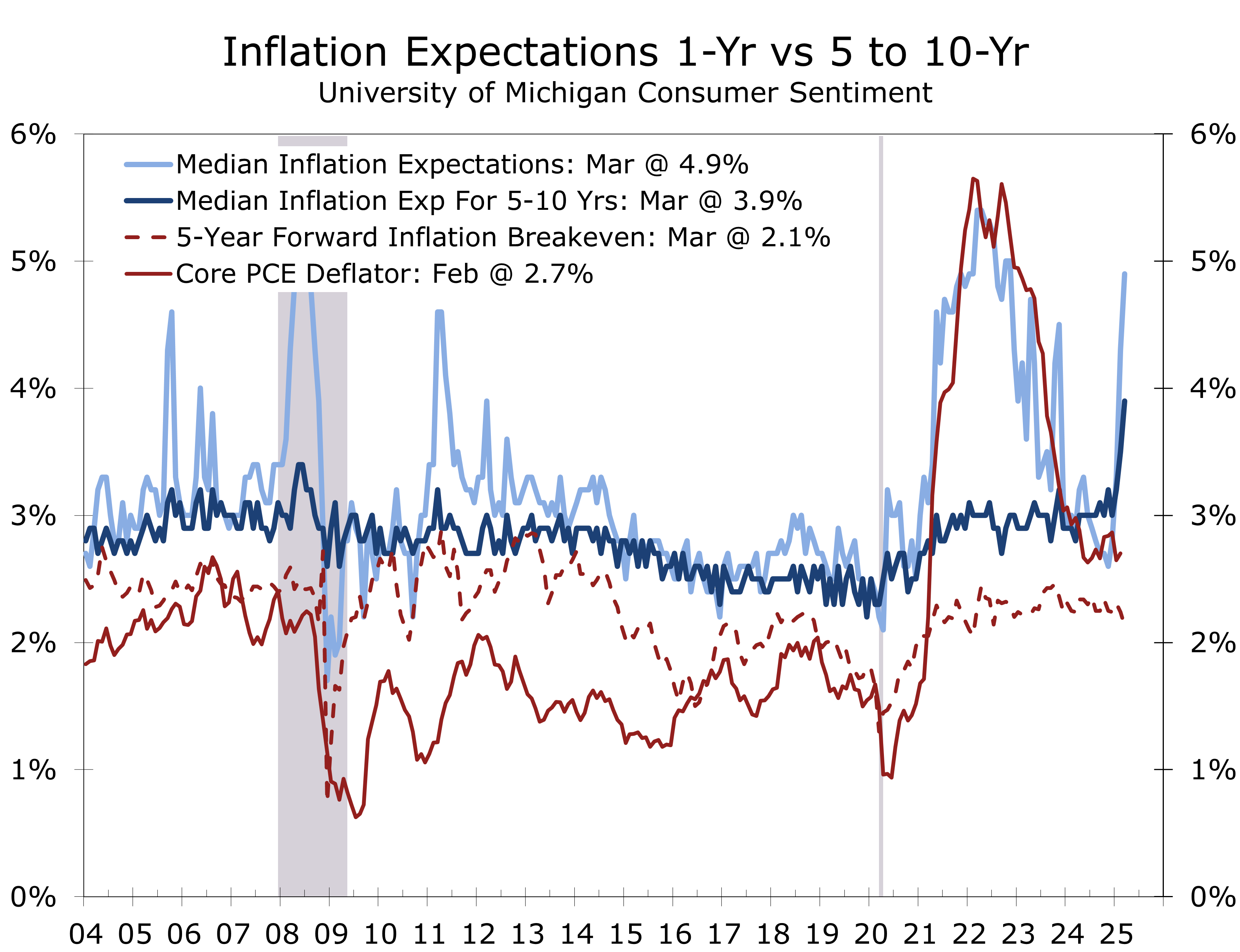

Concerns over tariffs’ impact on consumer prices have driven a sharp rise in inflation expectations. The University of Michigan’s Consumer Sentiment Survey showed one-year inflation expectations climbing 0.6 percentage points to 4.90% in March, while five-year expectations rose 0.4 points to 3.90%. Since the end of last year, one-year expectations have surged 2.1 points, and five-to-ten-year expectations have increased 0.9 points. Meanwhile, market-based measures, such as the five-year, five-year forward inflation breakeven, have remained stable, even edging down from 2.24% to 2.12% over the same period.

Federal Reserve officials, including Chair Jerome Powell, have acknowledged this divergence but prioritize market-based indicators. At his March 19, 2025, FOMC press conference, Powell dismissed the University of Michigan survey as an “outlier,” emphasizing that long-term inflation expectations remain well-anchored. The Fed views the inflationary impact of tariffs as a one-time shock rather than a sustained driver of inflation, reinforcing confidence that inflationary pressures will stay contained despite short-term consumer concerns.

The gap between consumer inflation expectations and market forecasts likely stems from an information disparity. Many consumers assume tariffs apply to retail prices, but they are actually levied on the lower imported value of goods, excluding transportation, insurance, and financing costs. This significantly reduces their direct impact on prices. For clothing for example, the imported value is typically just 10% of the retail price. Financial markets, which are better informed on these intricacies, expect tariffs to raise prices in the short term but also slow economic growth, leading to lower inflation over time.

Our view is more nuanced. Trump’s tariff initiative is larger and more variable than expected. We foresee a slightly greater near-term inflationary impact, as businesses preemptively raise prices to cushion against rising costs. This could be worse than the financial markets and the Fed anticipate, particularly for automobiles, computers, and consumer electronics, where the imported value comprises a larger share of retail prices. Supply disruptions may further raise operating costs, which would be passed on to consumers. Additionally, the wave of tariff-related news effectively provides businesses cover to raise prices more easily.

President Trump’s recent executive order imposes a 25% tariff on imported light vehicles starting April 3, 2025, with key auto parts following by May 3 and all parts within 90 days. While vehicles and components under the USMCA receive partial exemptions, tariffs still apply to non-U.S. content. As a result, the effective U.S. tariff rate will rise by approximately 2.5 percentage points by July, with some non-USMCA imports facing tariffs as high as 50%. Reciprocal tariffs set to take effect on April 2 could complicate the impact.

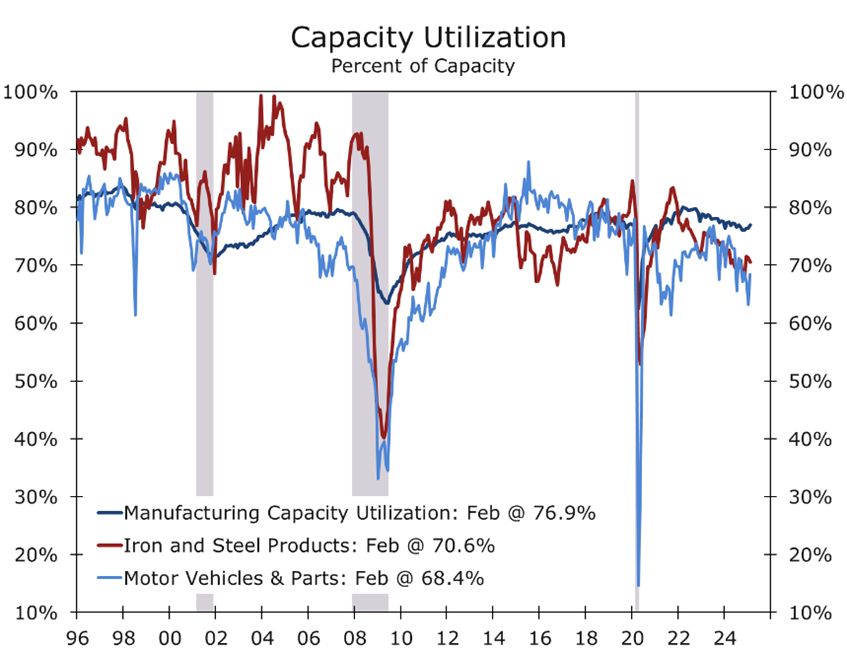

The Administration justifies the move on national security grounds and the need to bolster domestic manufacturing. The White House highlights a $93.5 billion auto parts trade deficit in 2024 and a shrinking industry workforce. By raising import costs, the policy aims to push consumers toward American-made vehicles and incentivize domestic production. A study cited by the administration suggests a global 10% tariff could significantly boost the U.S. economy and employment. There is some room to boost output. The Fed’s latest data show the U.S. auto industry operating at 68.4% of capacity, compared to a historical average of 74.9%. While domestic production should theoretically rise, the broader economic impact remains uncertain. The iron and steel industry is operating at 70.6% of capacity versus an historic average of around 78%.

Higher vehicle prices will likely burden consumers, as the average new car now costs nearly $50,000. Affordability concerns are at a multi-decade high, with automobiles—both new and used—out of reach for a historically large share of U.S. consumers. Automakers like Ford and General Motors, reliant on international supply chains, will likely face higher costs. Meanwhile, major trading partners such as China, Japan, and Germany may impose retaliatory tariffs, further complicating the outlook.

Tariffs align with Trump’s broader economic nationalism, echoing tariffs on steel, aluminum, and Chinese goods during his first term. The auto industry’s economic and symbolic significance makes it central to his trade strategy. However, complexities surrounding exemptions, administrative burdens, and retaliation risks create uncertainty about long-term effects on the U.S. economy and global trade.

Trump’s ultimate goal is unclear—whether to raise revenue, boost domestic manufacturing, or ultimately reshape the global trading system with lower and more transparent trade barriers. The likely outcome is a mix of these objectives. We expect the tariff battle to be largely contained to 2025, with the administration working to minimize economic disruptions ahead of the 2026 midterm elections.

The Trump Administration’s aggressive tariff policies have clouded the economic outlook. Businesses have accelerated imports ahead of tariff implementation, sharply widening the trade deficit and weighing on first-quarter GDP growth. The extent of the drag depends on how quickly these imports move into inventories or reach end users, both of which contribute to GDP. While Q1 output may decline, final domestic demand remains positive, and any shortfall from front-loaded imports should reverse in later quarters, boosting growth.

Beyond trade volatility, the broader economy has also lost momentum. We estimate job growth has been overstated by roughly 550,000 over the past year, with hiring also heavily concentrated in health care, social services, leisure and hospitality, and state and local government. With heightened uncertainty, hiring is expected to slow this spring and summer. However, tighter border enforcement has significantly curbed immigration and labor force growth, limiting any upward pressure on the unemployment rate.

Business investment is a bright spot. Shipments of nondefense capital goods have risen solidly in Q1, driven by equipment for new plants constructed under the Inflation Reduction Act and CHIPS Act. Additionally, commercial aircraft shipments have surged as Boeing works through its backlog.

Our outlook remains cautious, with real GDP projected to grow 1.6% in 2025. However, strong late-2024 growth should lift the annual average to 2.1%. Risks remain skewed to the downside, as the Administration prioritizes early wins on trade and tax reform at the expense of short-term economic disruptions. We expect the Federal Reserve to cut rates twice this year, with the first cut possibly as early as June.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice. Any forward-looking statements or forecasts are not guaranteed and are subject to change at any time. Information from external sources have not been verified but are generally considered reliable..

February 28, 2025

Mark Vitner, Chief Economist

Piedmont Crescent Capital

704-458-4000