Growth Re-accelerates, but the Signal Is Nuanced

-

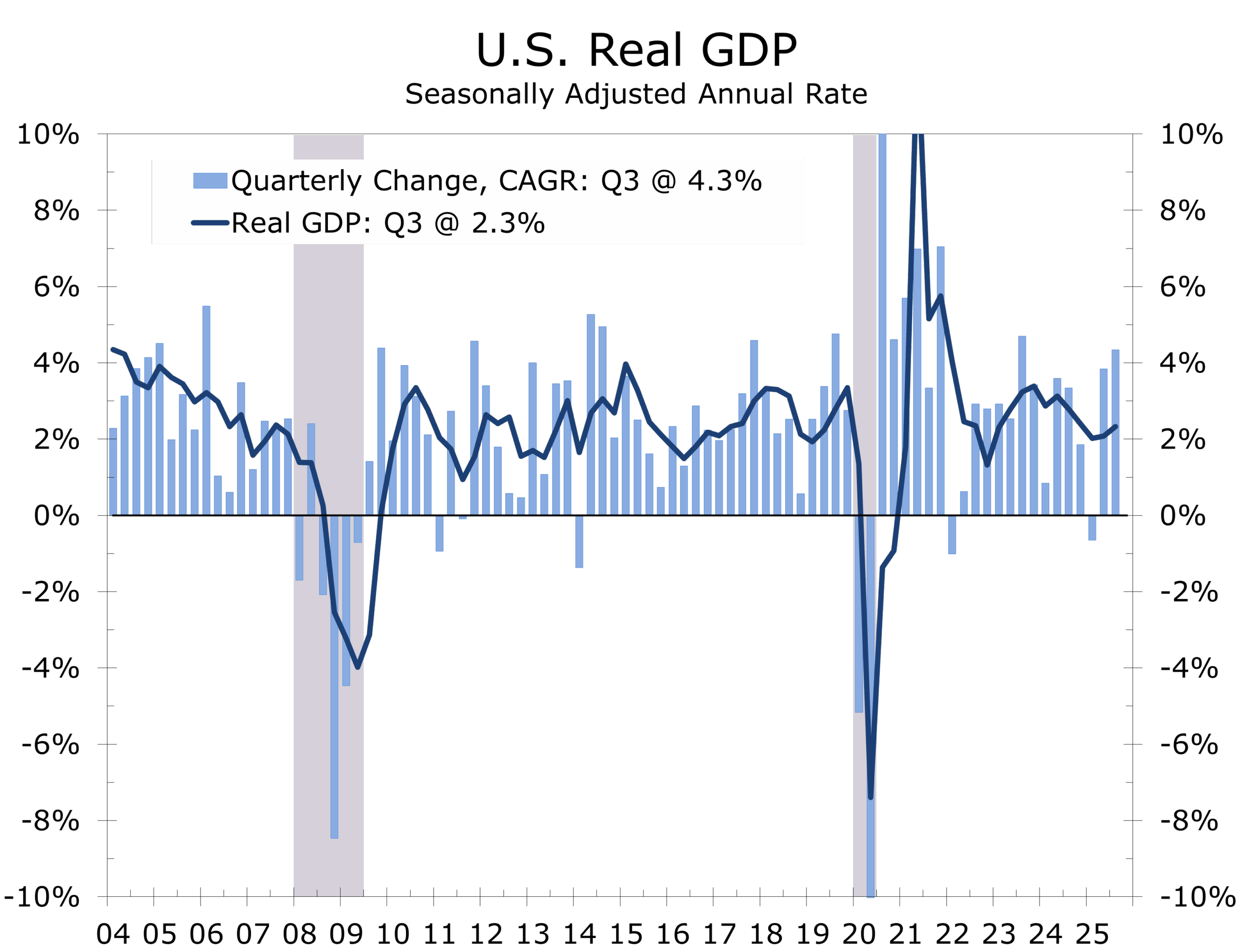

- Q3 real GDP jumped 4.3%, the fastest pace of 2025, but the headline was amplified by swings in trade, inventories, and government spending rather than a step-change in underlying demand.

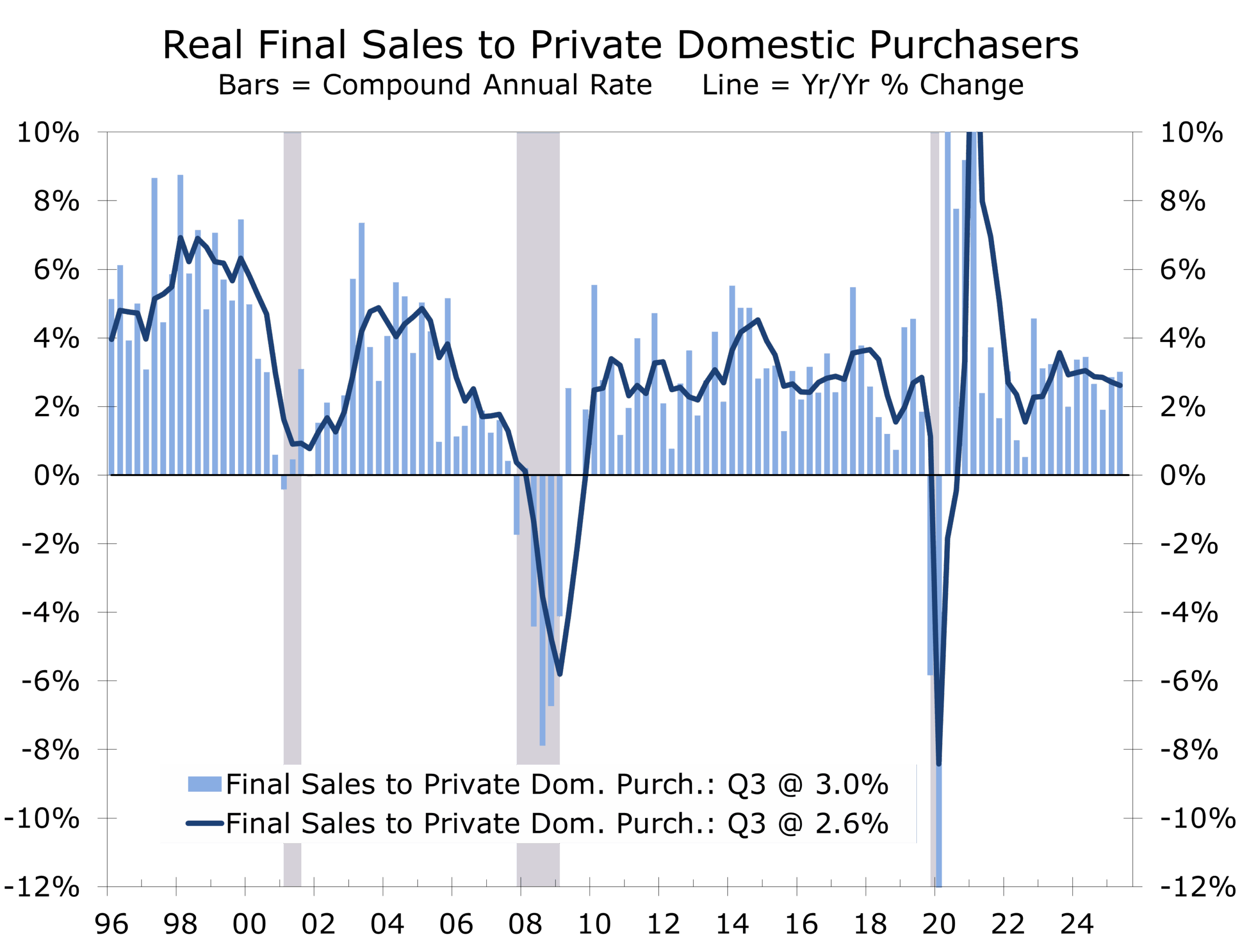

- Core private domestic demand grew a solid 3.0%, maintaining its recent strong pace and confirming continued expansion.

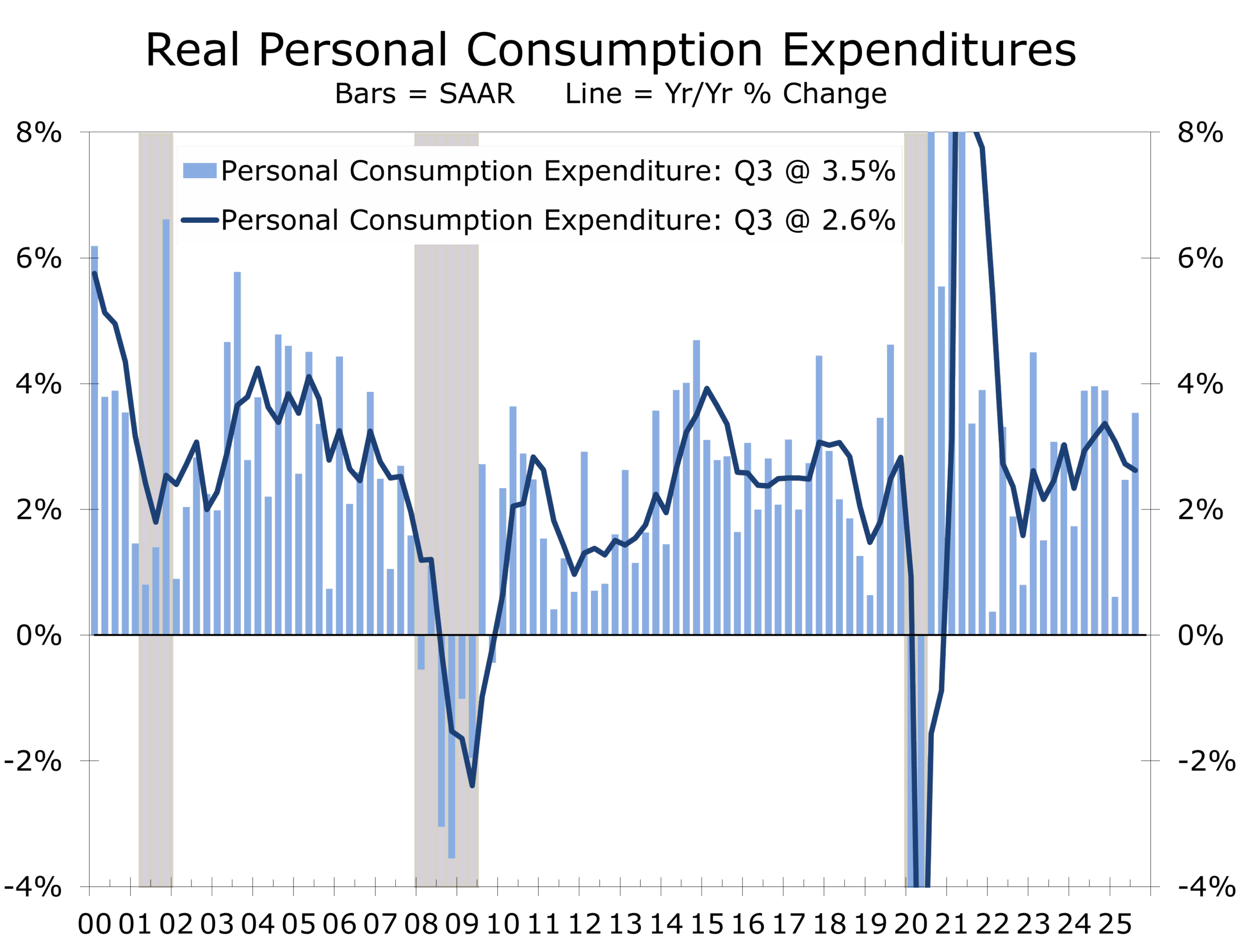

- Consumer spending perked up, led by health care, travel, professional services, recreational goods, and prescription drugs, signaling ongoing resilience.

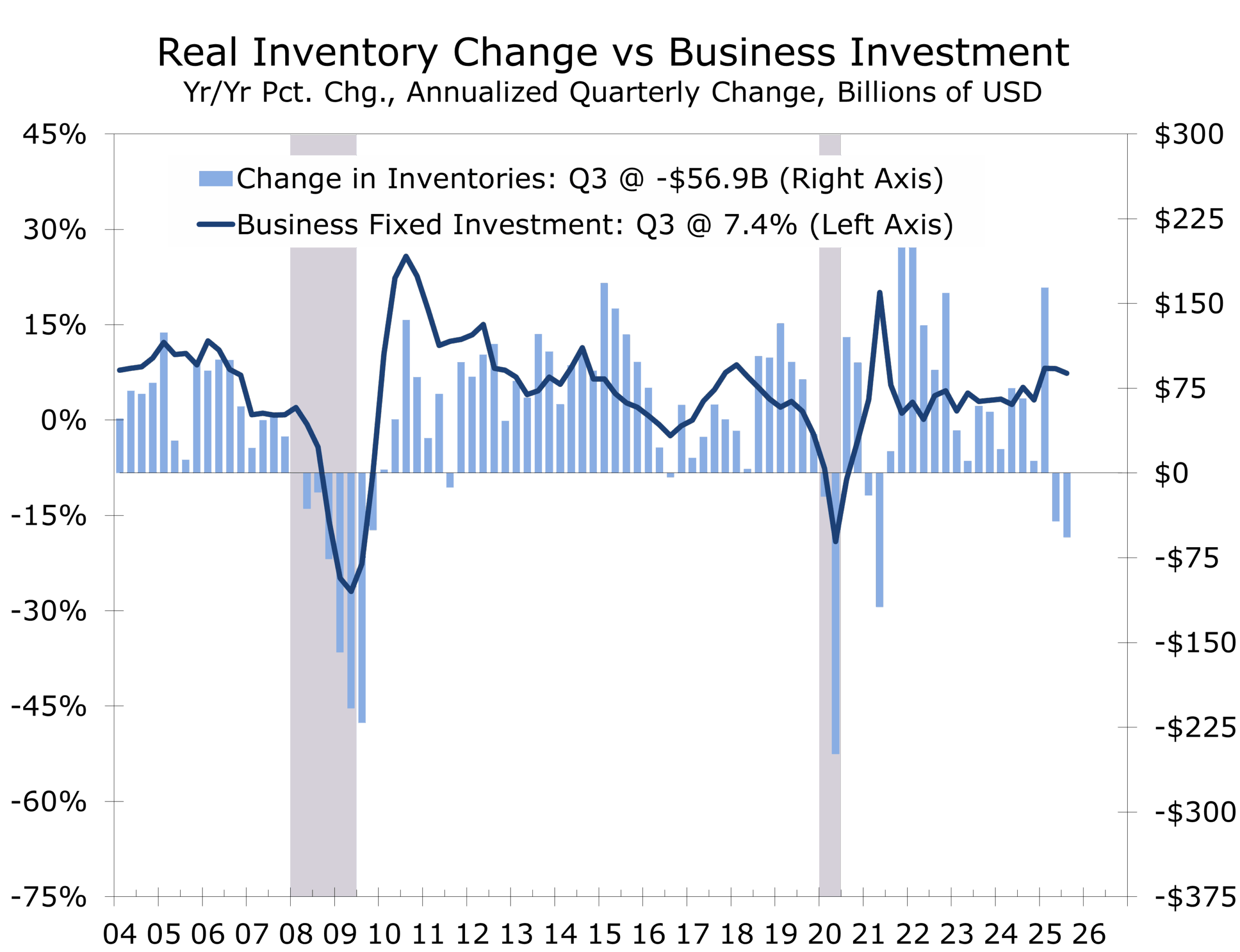

- Investment remained uneven, with further inventory drawdowns weighing on growth, particularly in manufacturing, trucking, and warehousing, while fixed investment held up better than the headline suggests.

- Inflation firmed at the margin, with core PCE rising at a 2.9% annual rate in Q3 and also climbing 2.9% over the past year. With tariff pass-through already visible in price data, the third quarter likely marked the high-water mark for trade-related inflation pressure.

- The third quarter delivered a headline surge in growth, but the signal beneath the noise points to a resilient—rather than overheating—economy, increasingly driven by business fixed investment and value-conscious consumer spending. This emerging mix should prove modestly disinflationary over time, easing the Fed’s balancing act.

A Strong Headline, Filtered Through the Noise

Real GDP accelerated sharply in the third quarter, rising at a 4.3% annualized pace, marking the strongest quarterly growth rate of 2025. On the surface, the report suggests a decisive reacceleration in economic momentum following solid growth in the first half of the year. Beneath the headline, however, the picture is more nuanced. Core private domestic demand advanced at a still-healthy but far less dramatic 3.0%, while the top-line surge was amplified by trade flows, inventory dynamics, and government spending, all measured through a release affected by the recent federal government shutdown.

The economy is growing—but not at the breakneck pace the headline implies. We continue to stress that real final sales to private domestic purchasers provide a more reliable assessment of the economy’s underlying momentum.

Income-side measures reinforce this interpretation. Real gross domestic income (GDI) rose at a 2.4% pace, notably below the headline GDP gain and more closely aligned with trend growth in labor income and profits. Because GDI is constructed from wages, salaries, profits, and other income flows, it is typically less sensitive to short-term swings in trade and inventories that can distort GDP in any single quarter. Averaging GDP and GDI, which rose 3.4% in Q3, offers a more balanced read on underlying activity, particularly in a quarter affected by data disruptions.

Q3 growth was lifted by trade, inventories, and defense spending—but the economy’s core continued to expand at a steady, sustainable pace.

Historically, gaps between GDP and GDI tend to emerge late in the cycle, when investment surges, inventory swings, or policy timing inflate measured output even as income growth slows. A comparable episode occurred in late 1999, when headline GDP growth remained strong amid the tech boom, but GDI and labor income growth had already begun to cool, signaling that momentum was becoming increasingly concentrated in investment and asset-driven activity. In that period, GDP continued to look robust even as income-based measures provided an earlier warning that underlying growth was losing breadth.

Averaging GDP and GDI points to growth near the upper end of trend—not a breakout.

Core Domestic Demand Remains the Anchor

The cleanest read on underlying momentum comes from real final sales to private domestic purchasers, which grew at a 3.0% pace, slightly above Q2’s 2.9%. This measure, which strips out inventories, trade, and government spending, confirms that demand driven by households and businesses remains firmly expansionary.

Final sales to private domestic purchasers remain the most reliable signal—and they continue to tell a story of resilience, not acceleration.

Consumer spending re-accelerated, with gains across both services and goods. Services spending was led by health care, international travel, and professional services, reflecting continued normalization in activity that had lagged earlier in the cycle. Goods spending was supported by recreational goods, vehicles, and prescription drugs, with information processing equipment again playing a notable role.

Real disposable income growth slowed during the quarter, suggesting that recent spending strength is being supported in part by a lower saving rate and wealth effects rather than accelerating labor income. The decline in saving was exacerbated by a spike in light vehicle sales, as households pulled purchases forward ahead of the expiration of attractive electric vehicle tax credits. Together, these dynamics reinforce evidence of a K-shaped consumer, with higher-income households driving discretionary categories such as travel, recreation, and professional services.

Part of the decline in saving reflects timing, not stress—vehicle purchases were pulled forward ahead of expiring EV tax credits.

This is not a consumer-driven boom, but it is a consumer that remains resilient in the face of elevated borrowing costs and ongoing affordability pressures.

Investment: Inventory Noise Masks a Steadier Core

Private investment remained a modest drag on growth, but far less so than in prior quarters. The decline was driven primarily by inventory liquidation, particularly in wholesale trade and manufacturing. Inventories were built up earlier in the year ahead of tariffs, and businesses have since been drawing down stocks as trade relationships are refined and demand patterns normalize.

Importantly, gross private fixed investment held up better than the headline suggests, reinforcing the view that businesses remain cautious but not retreating. Growth slowed outside of data-center-related construction, with intellectual property investment cooling modestly and structures investment weakening as factory and mining construction softened following earlier front-loaded buildouts. Firms appear to be managing balance sheets and inventories conservatively while preserving the ability to expand investment once policy uncertainty and financial conditions improve.

Trade and Government Spending Flatter the Headline

Exports rebounded in the third quarter, supported by gains in both goods and services. Imports declined again, boosting measured GDP but complicating interpretation of domestic momentum. These trade dynamics have become a recurring source of volatility in recent quarters and are best viewed as amplifiers rather than drivers of the business cycle.

Government spending also contributed positively, with increases at both the federal and state and local levels. Defense spending led the federal gains, while state and local consumption expenditures also rose. As with trade, these contributions lift the headline but offer limited insight into the sustainability of private-sector growth.

Inflation Moves the Wrong Way at the Margin

Inflation data were less reassuring. The gross domestic purchases price index rose at a 3.4% pace, while PCE inflation accelerated to a 2.8% pace and core PCE increased to a 2.9% pace. While inflation remains well below its 2022 peak, the third-quarter uptick was already apparent in earlier CPI data.

Tariff-related price pressure likely peaked in Q3; broader inflation trends remain contained.

Encouragingly, core capital goods prices remain well behaved, suggesting that underlying investment-related inflation pressures are contained even as headline deflators temporarily firm. With tariff effects now largely reflected in the data, we look for the deflators to follow the CPI lower in coming quarters.

Profits Quietly Improve

Corporate profits from current production increased $166 billion in the third quarter, a sharp rebound from the prior period. Combined with steady income growth, this improvement supports margins, balance sheets, and capital spending optionality heading into 2026. This aspect of the report received less attention than the headline GDP number but remains an important underpinning for medium-term growth.

Policy and the Road Ahead

From a policy perspective, the third-quarter report argues for flexibility rather than urgency. Growth remains above potential, inflation has firmed modestly, and labor income continues to support demand. At the same time, the absence of broadening inflation pressure and signs of cooling outside of AI-related investment argue against renewed tightening.

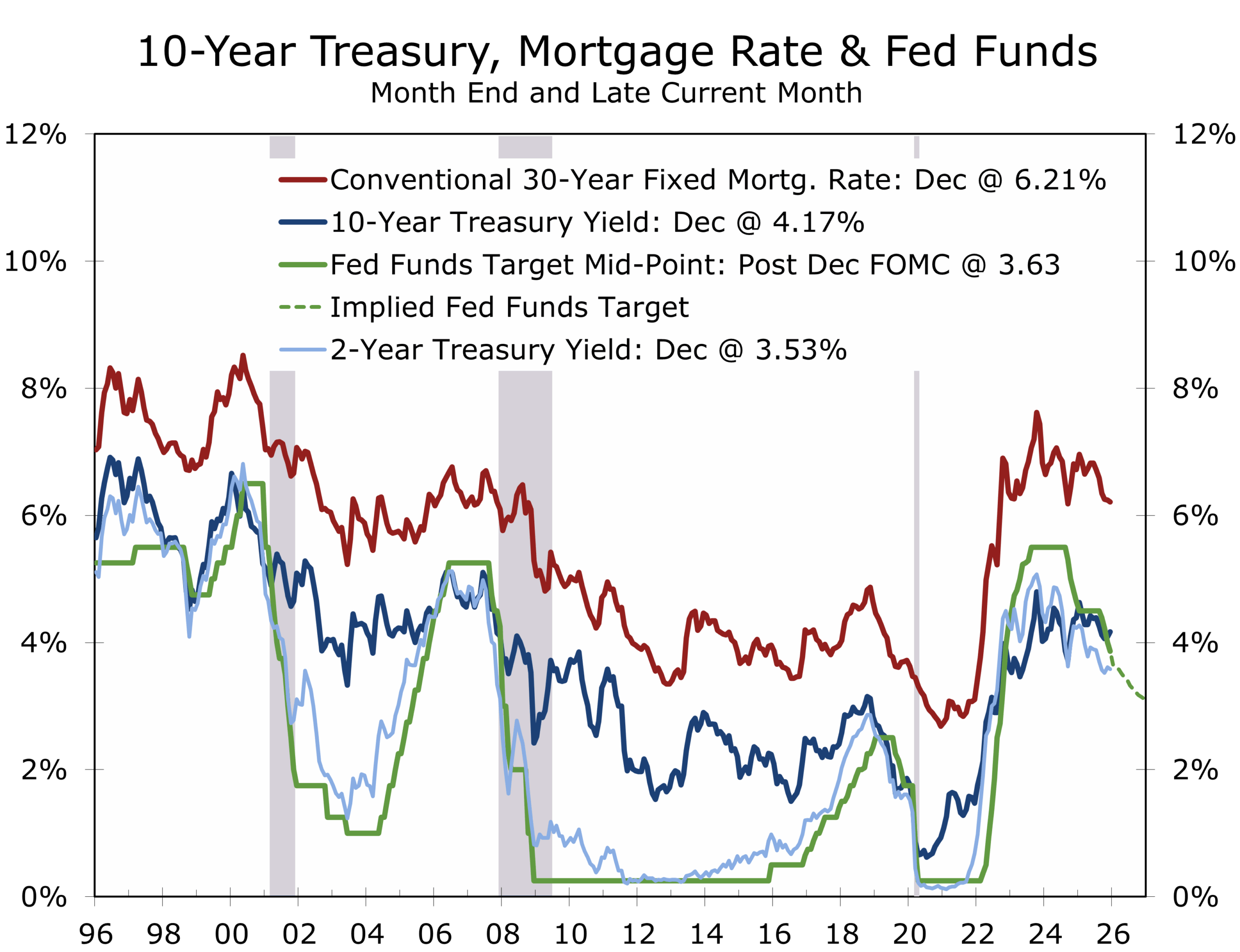

The most likely outcome is a for the Fed to cut rates more slowly, by perhaps cutting at every other FOMC meeting, which will not only allow for a clearer read of the data but also extend the easing cycle. The expansion remains intact, underlying momentum is moderating gradually. Yet the labor market is still deserving of additional Fed support but without undermining hard-won progress at reducing inflation.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 23, 2025

Mark Vitner, Chief Economist

(704) 458-4000