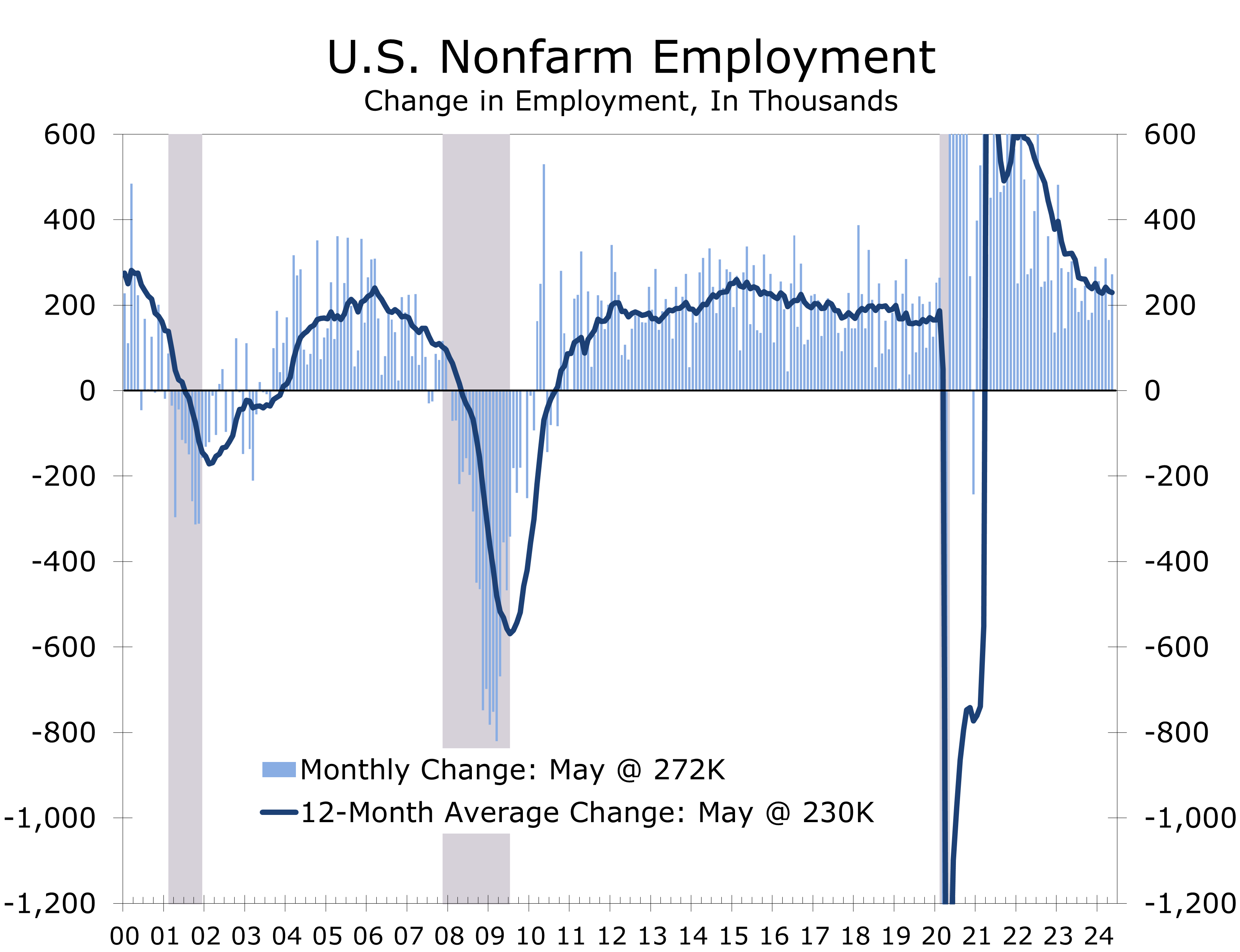

Nonfarm Payrolls Top Expectations

- Employers added 272,000 jobs in May. Payrolls for the prior two months were revised lower by a combined 15,000 jobs.

- Job growth was broad-based, although the bulk of gains continue to come from a handful of industries, including health care (+68K), government (+43K), and leisure and hospitality (+42K).

- Average hourly earnings for production workers rose 14 cents to $29.99, topping expectations, and are up 4.2% year-to-year.

- Weather and calendar effects likely boosted payrolls by about 45,000 jobs.

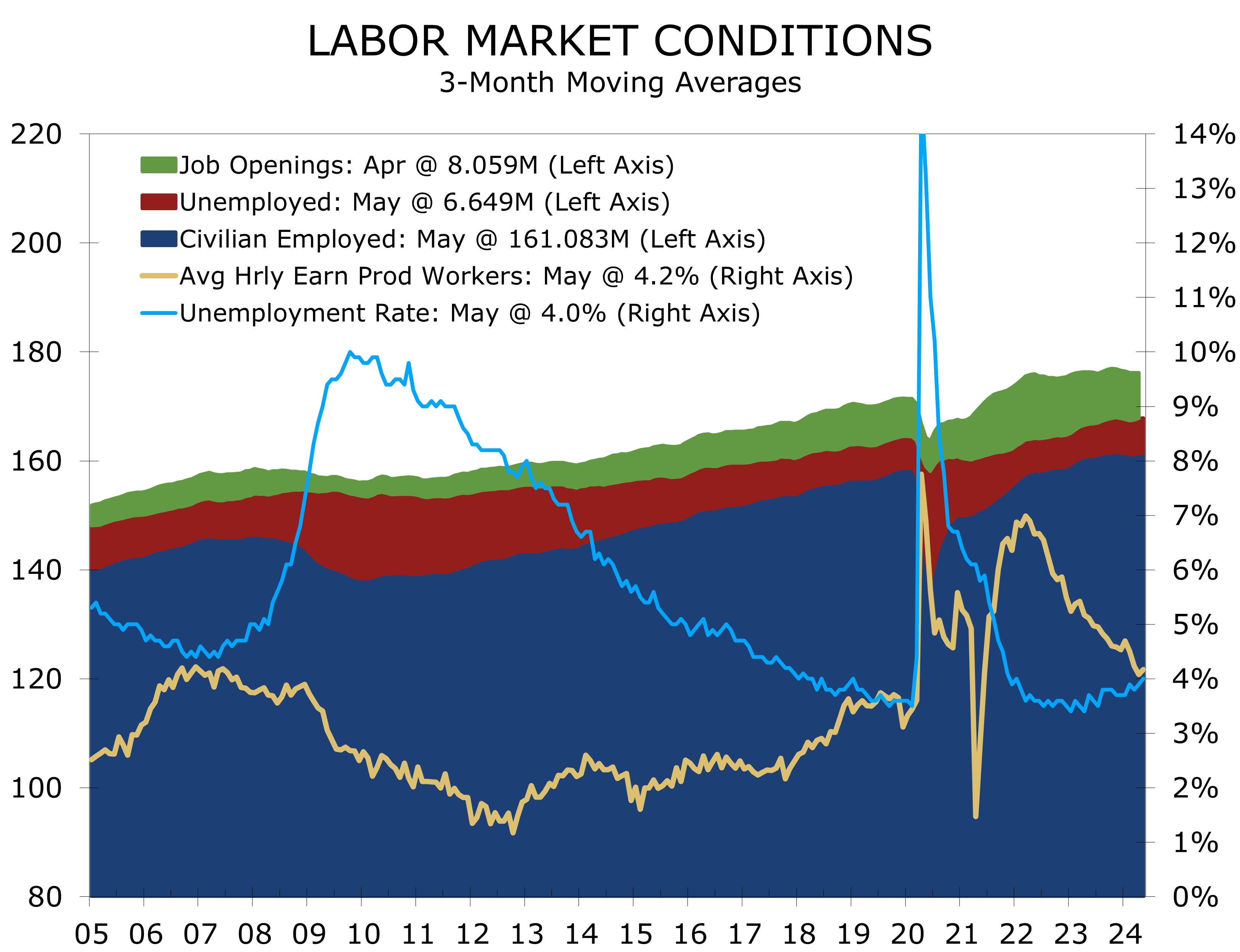

- The unemployment rate rose to 4.0%, up from 3.7% one year ago. The number of unemployed has risen by half a million persons since last May to 6.6 million.

- Aggregate hours worked rose 0.2% and have risen at a 2.1% pace over the past 3 months.

- Nonfarm payrolls blew past expectations, with employers adding 272,000 jobs. Gains were broad based but continue to be driven by lower paying jobs in health care, leisure & hospitality and government. The tech sector remains a standout, boosted by the AI boom. The rise in the unemployment rate should not be dismissed.

Nonfarm employment easily topped expectations, with employers adding 272,000 jobs in May. The gain beat consensus expectations by a whopping 92,000 and is well above the 230,000 jobs added per month on average over the past year. The unemployment rate edged higher to 4.0%.

Seasonal adjustments and weather effects likely boosted payrolls by around 45,000 jobs. There was an extra week between the April and May employment surveys, which we believe added around 15,000 jobs to total job growth. A return to more typical spring weather also allowed hiring to bounce back in construction and hospitality sectors, following an unusually rainy April.

Hiring rose broadly in May, but gains continue to be concentrated in a handful of industries

The diffusion index rose 6.8 points to 63.4% in May, hitting its highest level in 16 months. While job growth was broad-based, the bulk of employment gains continue to come from a handful of industries, much of which is occurring in lower-paying segments of those industry categories. Health care (+68K), government (+43K), leisure and hospitality (+42K), and professional, scientific, and technical services (+32K) combined accounted for more than two-thirds of May’s employment gain.

Manufacturing eked out a modest 8,000-job gain in May, with nondurable goods producers adding 10,000 jobs and producers of durable goods cutting 2,000 jobs. Within nondurables, chemical producers added 4,100 jobs, and food product producers added 3,400 jobs. Chemical producers are getting a boost from surging demand for pharmaceuticals, particularly GLP-1 diet drugs.

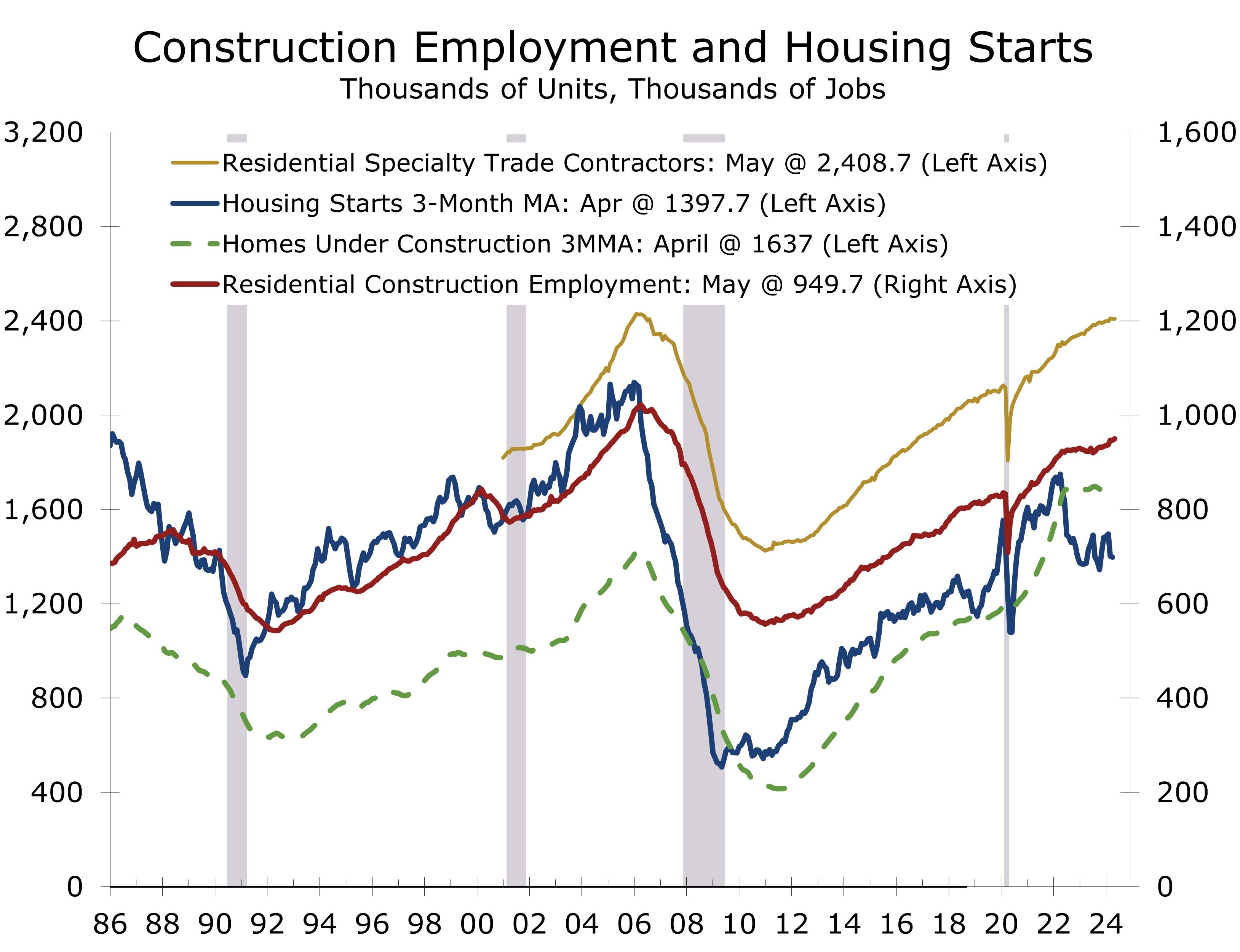

The massive backlog of construction projects is buoying construction payrolls.

Construction firms added 21,000 jobs in May, with three-quarters of the increase coming in nonresidential construction. Much of that growth reflects the ongoing buildout of industrial facilities and data centers. Residential construction also edged higher, with residential building contractors adding 3,500 jobs and employment at residential specialty contractors remaining unchanged.

Much has been made of the apparent resilience of construction payrolls in the face of higher interest rates. Rest assured; the Fed’s monetary policy transmission mechanism still runs through the housing market. The reason construction payrolls have held up so well is that there is still a historic backlog of single-family homes and apartments under construction. Payrolls will weaken as this backlog is worked off later this year.

The financial markets initially sold off after the jobs report was released. Stronger headline job growth combined with a larger-than-expected rise in average hourly earnings lessened the chances of a rate cut in July, which we saw as unlikely anyway.

Despite the larger-than-expected rise in hourly earnings, the May employment report still shows the labor market gradually moving back into balance. An earlier report from payroll processor ADP showed overall hiring slowing, particularly at smaller firms. Job openings in the JOLTS survey also ticked lower in April, falling to their lowest level since February 2021. The unemployment rate edged higher, climbing 0.1 points to 4.0%, its highest level since January 2022.

The labor market appears to be moving back into balance, with hiring moderating.

The rise in the unemployment rate was largely dismissed due to some large moves in the labor force among younger workers. The May/June period typically sees large numbers of workers enter the workforce as the school year ends, leading to large month-to-month swings. That said, the jobless rate has been trending higher for the past few months.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

June 7, 2024

mark.vitner@piedmontcrescentcapital.com

Chief Economist (704) 458-4000