What Newton’s Law of Motion Means for Fed Policy

In light of recent political news, new inflation data, and next week’s FOMC meeting, we are releasing some supplemental thoughts to our most recent monthly forecast. We have also updated the forecast with the latest GDP and personal income data.

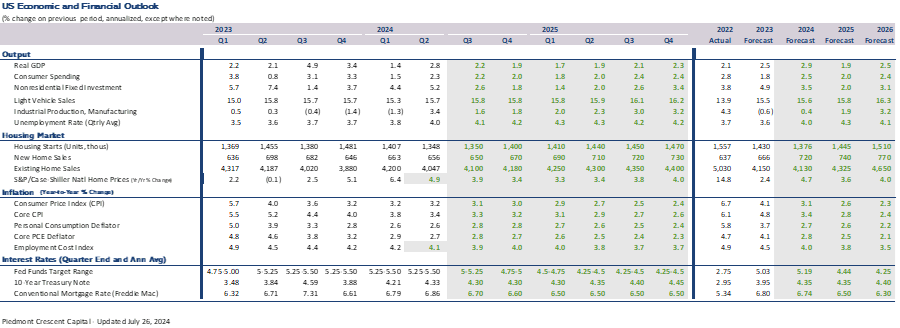

As we noted in the CAVU Compass, second quarter real GDP surprised to the high side, as increased inventory building added 0.8 percentage points to growth. Inventories are one of the most volatile components of GDP and hardest to forecast ahead of the advance report. Businesses appear to have stocked up as a precaution against lengthening delivery times due to the disruptions to shipping around the Red Sea, as well as to rising fears of a Longshoremen’s strike.

The advance report will be revised next month, and the BEA will release comprehensive revisions going back the past five years in September.

We look for the Fed to set the table for lower interest rates at the July FOMC meeting and then further outline the mechanics of how monetary policy impacts the economy at the annual Jackson Hole symposium. The first quarter-point cut should come in September, followed by another cut in December. We expect a total of four or five quarter point cuts, pulling the federal funds rate down to around 4.25%.

The yield curve should flatten as cuts become more evident and possibly normalize. This is usually a warning sign of a recession. The economy will be at risk during this transition and uncertainty surrounding the election may cause businesses to hold off on major projects.

The economy still has a great deal of stimulus left over from the pandemic, which is driving investment in new plant and equipment and important infrastructure. Consumer spending is being driven by higher asset prices and slower but still solid wage and salary growth.

As for politics, the most likely outcome remains a republican sweep in November, although the odds have diminished somewhat due to Biden handing off the democratic nomination to Kamala Harris. Either way, we expect major stimulus programs such as the Inflation Reduction Act and Infrastructure Act to remain in place in 2025. The “Trump tax cut” will likely be extended.

The political environment remains unusually volatile, and we will get a better read after the democratic convention and likely first Trump-Harris debate in September. – Mark Vitner, July 26, 2024

- There is increasing evidence the Fed has successfully countered the nation’s most serious bout with inflation in forty years. After a Q1 scare, nearly all measures show inflation cooled over the past three months, most patently expressed by June’s 0.1% drop in the headline Consumer Price Index – the first such drop since the pandemic. Various measures of core inflation are also easing, and wages continue to moderate as the labor market gradually returns to balance.

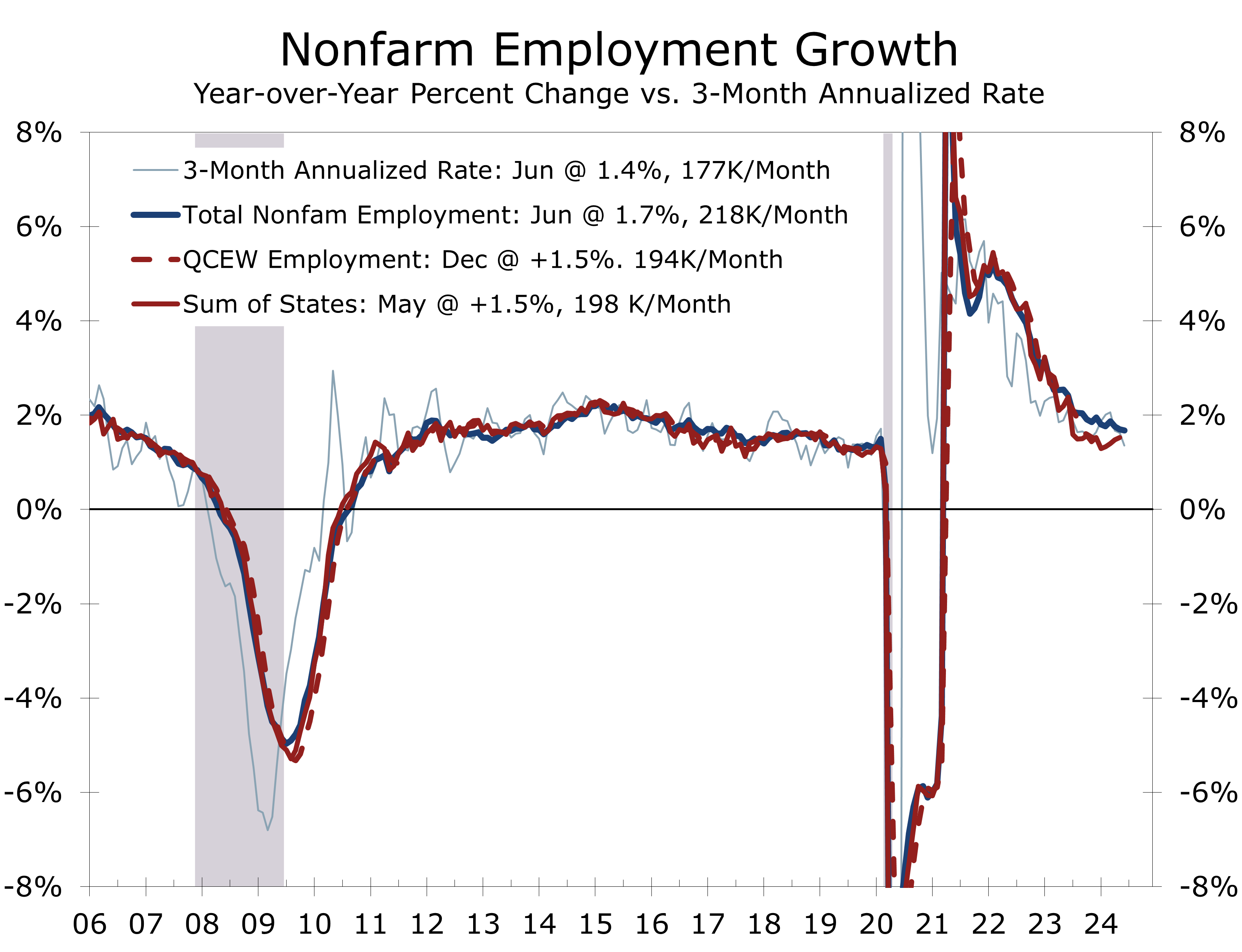

- Employment growth has slowed largely in line with our long-running forecast, with employers adding an average of 177,000 jobs a month for the past three months, down from 274,000 per month a year ago. The latest data are now more consistent with the Quarterly Census of Employment and Wages data, which are the source of the annual revisions. Hiring is also less broadly based than it was previously, with the bulk of job growth coming from just a handful of industries, including health care, social services, restaurants, and state and local government.

- Consumer spending remains solid. June retail sales came in stronger than expected, and sales for April and May were revised significantly higher. The widely followed Atlanta Fed GDPNow estimate, which began the quarter near 4%, rose from 2% to 2.5% following June’s stronger retail sales. Our own forecast remains at 2.2%, which is on the high side of the most recent consensus.

- The political environment has changed considerably, with the far-left winning elections in the UK and France. In the U.S., former President Trump has jumped ahead in most polls and leads in most swing states following the first presidential debate. The assassination attempt on the former president will likely change the tone of the campaign and make it more difficult for the Democrats to remove Joe Biden from the ticket. The most likely outcome currently is a Republican sweep in November. We will get a clearer view once we get past the mid-August Democratic convention.

- We have reduced our 2024 forecast slightly further, reflecting slower growth in the first half of the year. Inflation should continue to moderate, although we could see some periodic rebounds driven by seasonal adjustment issues. We look for the Fed to begin to cut interest rates in September, or possibly sooner, and expect four or five quarter-point cuts over the next year.

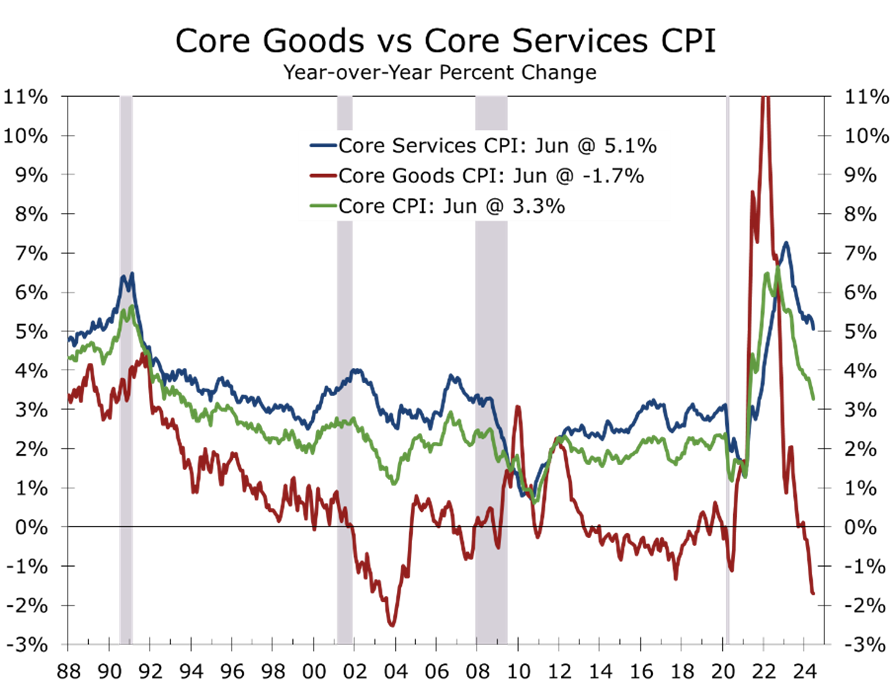

The inflation fever has finally broken, paving the way for lower interest rates. Nearly every major price index moderated meaningfully during the second quarter. The headline Consumer Price Index even posted a modest decline at the end of the quarter, as lower gasoline prices pulled the headline number down. Core inflationary pressures are also easing, with the core CPI slowing to 3.3% year-over-year in June and core services prices moderating to a 5.1% gain. Price pressures are also easing further back in the production pipeline. The Producer Price Index slowed to just 2.6% year-over-year in June, while average hourly earnings slowed to just a 3.9% rise over the past 12 months.

Suddenly, inflation looks far less menacing. The headline Consumer Price Index fell 0.1%, marking its first monthly decline since July 2022 and the largest drop since the throes of the pandemic back in 2021. A 2% seasonally adjusted drop in energy prices was responsible for much of June’s drop. Gasoline prices tumbled 3.8% in June, following a 3.6% drop the prior month. Food prices are also moderating. Overall food costs rose 0.2% in June and are up just 1.1% over the past year. Prices at the grocery store have risen 1.1%, while prices at restaurants are up 4.1%. With June’s decline, the CPI is now up 3.0% year-to-year, compared to its peak of 9.1% in June 2022 and just 2.3% prior to the onset of the pandemic.

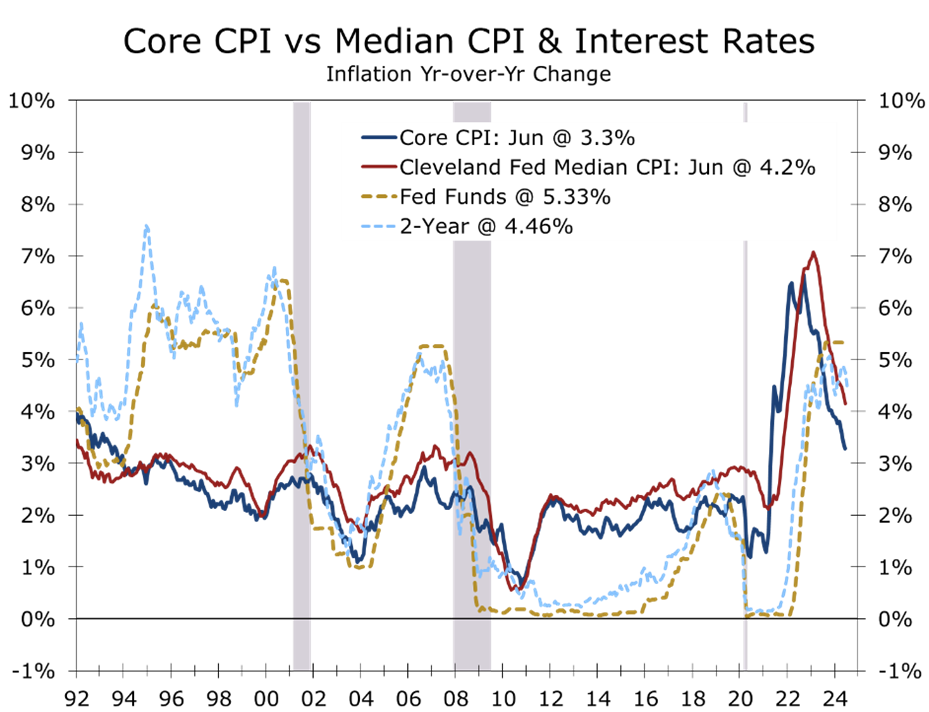

The core CPI has also moderated, rising just 0.1% in June and just 3.3% year-to-year. The core CPI peaked back in September 2022 at 6.1% and was just 2.4% before the pandemic. The moderation in price increases is broad-based. Airfares (-5.0%) and lodging (-2.0%) were two of the more notable price drops in June and are consistent with recent comments about the competitive price environment from Delta Airlines CEO Ed Bastian. Core goods prices were mixed. Prices for new vehicles fell 0.2%, while prices for used vehicles fell 1.5%. Prices for recreation goods rose 0.4%, with pet products rising 0.8%. Overall, core goods prices have fallen 1.7% over the past year, largely reflecting a 10.1% drop in used vehicle prices.

Services prices, excluding energy services, rose just 0.1% in June. Shelter costs are also cooling, with both rent and owners’ equivalent rent rising 0.3% in June, which is close to the pace averaged prior to the pandemic. Several areas that have been problematic in recent months moderated in June, including motor vehicle repair costs and medical care services, which both rose 0.2%. Motor vehicle insurance remains a problem area, with costs rising 0.9% in June and 19.5% over the past year.

On an overall basis, the CPI rose at a 2.8% annual rate, and the core CPI slowed to a 3.4% pace. Price pressures are also moderating further back in the production pipeline. The Producer Price Index rose just 0.2% in June and has slowed to just 2.7% over the past year. Average hourly earnings rose just 0.3% in June and have risen just 3.9% over the past year, down from a recent peak of 5.9% in March 2022. The inflation data should remain relatively benign over the next few months, although higher freight rates may raise the price of imported goods impacted by shipping disruptions around the Red Sea.

While inflation is still running well above the Fed’s 2% target, it has moderated enough for the Fed to begin lowering interest rates. We expect the Fed to make the case for a quarter-point cut in the federal funds rate at its July 30 meeting and look for three or four more quarter-point cuts over the next year. The financial markets will likely get ahead of themselves once again, as they did late last year when the Fed indicated they had likely finished hiking interest rates for this cycle. Shortly after the December FOMC meeting, the financial markets were pricing in 6 or 7 rate cuts for 2024. That view progressively gave way during the first four months of this year, following a string of stronger-than-expected economic reports.

Monetary policy works with a long and variable lag, with the bulk of the impact of a shift in policy typically taking at least a year to 18 months to take hold. This view has been challenged in recent years because of the growing role financial markets play in allocating credit. The financial markets tend to rally in anticipation of the Fed’s first move, which pulls some of the impact of monetary policy shifts forward. Reductions in mortgage rates and interest rates on auto loans, credit lines, and credit cards will not occur until well after the Fed begins to cut short-term interest rates. The effectiveness of the monetary policy transmission mechanisms will be the focus of this year’s Jackson Hole Economic Symposium held in late August.

The timing of the Fed’s next move is only one of the concerns. There is also a great deal of uncertainty about how much the Fed will ultimately cut interest rates. The magnitude of the Fed’s cuts is governed by Newton’s First Law of Motion, namely that an object in motion will remain in motion at the same speed and trajectory until it is met with an unbalanced force. The Fed demonstrated this when it aggressively raised interest rates (unbalanced force) in 2022 and 2023 to combat rising inflation. The larger-than-expected rate hike was needed to upend what was then the worst bout of inflation in more than forty years.

Today, however, the economy remains near full employment and inflation, while above the Fed’s target, is moderating in a way that the Fed should need to lower rates less aggressively. In terms of physics, the Fed needs to lower rates just enough to break the economy’s downward momentum without reversing the moderating trend in inflation. That is why we believe the Fed will ultimately make four or five quarter-point cuts and then hold the federal funds rate around 4% until economic growth either reaccelerates or decelerates further.

Recent comments by Fed officials suggest there is an emerging consensus that the labor market has already moved back into balance. Attitudes changed considerably following the June employment report, which showed employers adding 206,000 jobs that month but also sharply reduced estimates for job growth in April and May. Employers added an average of just 177,000 jobs a month during the second quarter, which is close to what we had expected based on our analysis of the Quarterly Census of Employment and Wages data.

Fed Governor Christopher Waller noted in a recent speech to the Federal Reserve Bank of Kansas City that he felt “current economic data are consistent with a soft landing” and that he would be looking for “data over the next couple of months” to confirm that view. Waller went on to say that he felt the labor markets were now back in balance and that inflation was moving toward price stability. Waller’s remarks, along with statements by Fed Chair Powell and other Fed officials, suggest they would like to look at another couple of months of data before cutting interest rates, making a move before September unlikely.

The Fed will get to see quite a bit of data between now and their September 17-18 FOMC meeting, including two more rounds of ISM reports, two more employment reports, an early estimate of the annual revision to nonfarm employment, two more months of retail sales data, two more months of CPI reports, and the first two estimates of second quarter GDP growth. We expect the output and employment data to remain consistent with a soft landing. The jobs data may even slow a bit, as recent gains have been highly concentrated within a handful of industries. The unemployment rate has trended up to 4.1% and is now at the upper end of the Fed’s long-run view of full employment.

On August 21, the BLS will also release the Q1 Quarterly Census of Employment and Wages data, which are the primary source data for the annual revisions released in February of each year. Our latest estimate puts the size of that revision at around 0.4 percentage points to the downside, which means that employers added roughly 750,000 fewer jobs than has been reported through March of this year. The QCEW data are a big reason why we expected nonfarm payrolls to slow to around 180,000 per month by the middle of this year.

While employment growth has slowed, the latest retail sales data show that consumer spending remains robust. Industrial production also rose solidly in Q2. We now estimate real GDP grew at a 2.2% annual rate during the second quarter, and we could see an upside surprise from increased inventory building.

Elections in France and the United Kingdom saw the far-left win enormous majorities and brought a new prime minister to the UK. We see the growing frustration in both nations being driven by the persistence of large budget deficits, which has prevented both the right and the left from enacting policies favored by their constituencies. The one thing both nations’ elections have in common is that the huge electoral victory was not driven by widespread support for Labour or the New Popular Front (NFP) but rather apathy and frustration with the incumbent party – Conservatives in the UK and Macron’s Centrist Alliance in France.

If there is a message for the US, it is that voters are restless and looking for change. The critical question is whether there are the fiscal resources available to deliver that change. The financial markets are fearful that what fiscal discipline was left in France and the UK will be jettisoned in favor of more populist spending.

The election landscape has changed dramatically in the US as well, following Joe Biden’s disastrous debate performance on June 27. A series of gaffes during the debate and in the weeks afterward has called into question whether Joe Biden will be the Democratic candidate in November. That is still the base case, at least before the failed assassination attempt on President Trump and President Biden’s Covid-19 diagnosis. Current polling shows Trump leading slightly in the national polls but well ahead in most swing states. Republican House and Senate candidates are also doing well, and enthusiasm is stronger for the GOP than it is for the Democrats, raising the possibility of a Republican sweep in November.

If Trump wins and the GOP takes both houses of Congress, we expect to see a full extension of the 2017 tax cuts. We would also likely see a rollback in regulations and some easing in restrictions on oil and gas exploration and pipeline construction. Trump has also vowed to boost tariffs and use the revenue to cut taxes. We see this as less likely. Trump would also likely scale back incentives for EVs but would not completely reverse programs currently in place. The infrastructure law would remain as is, or possibly be tweaked slightly.

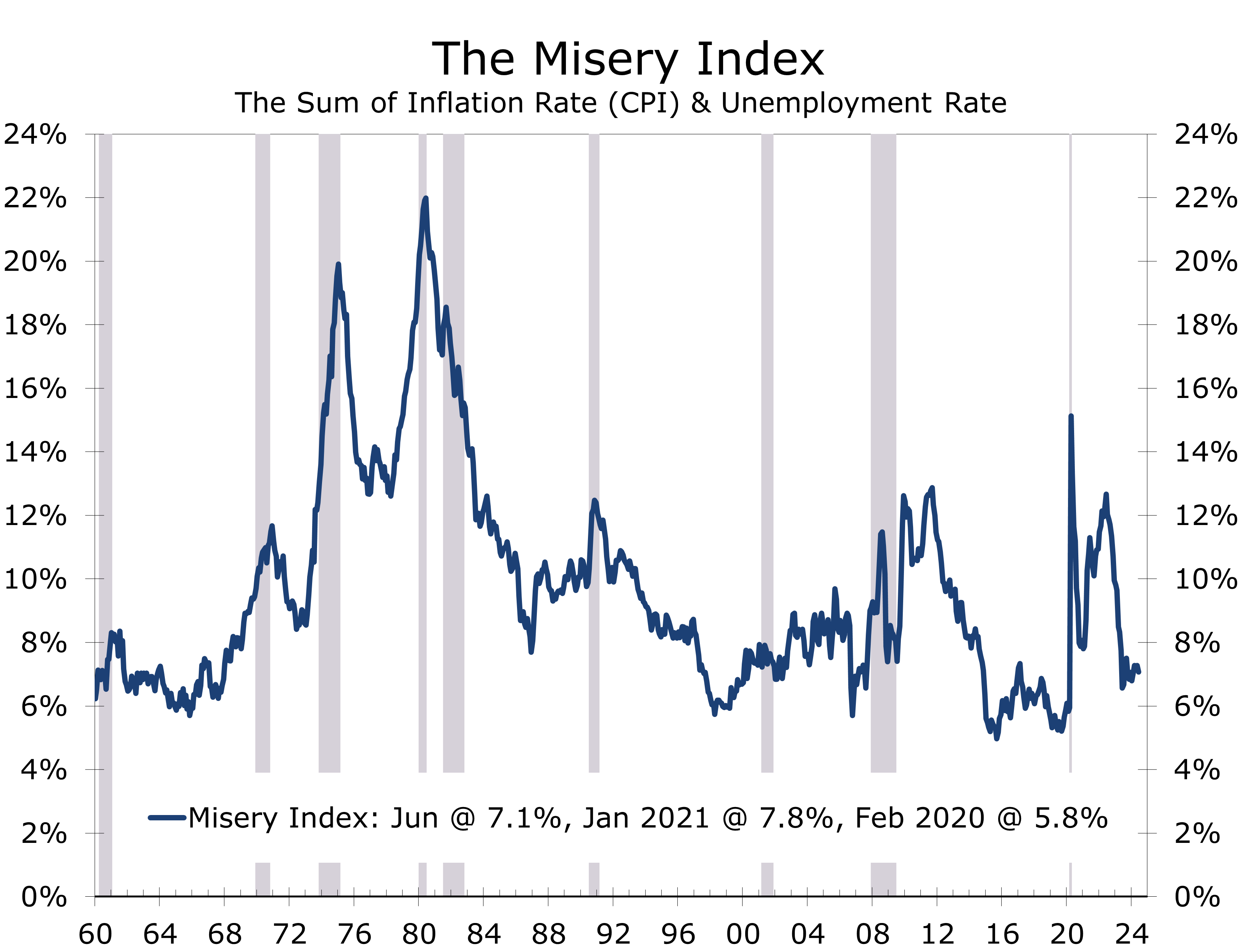

The Misery Index, which is the sum of the trailing inflation rate and unemployment rate, does a good job of capturing voter angst and closely tracks various consumer confidence measures. The Misery Index is lower today than it was when Joe Biden took office. Inflation is higher and unemployment is lower. Unfortunately for Biden, both are moving in the opposite direction and lower inflation does not mean lower prices; it simply means they are rising less rapidly.

June’s surprising strength in retail sales, which saw core retail sales climb 0.9% and included upward revisions to the April and May data, has boosted expectations for Q2 GDP growth. Moreover, the strength in retail sales at the end of the quarter means that spending in the current quarter starts off at a high level. We still see the economy losing momentum. We see real GDP climbing at a 2.2% pace in Q2, helped by a resilient consumer, continued strong gains in business fixed investment, and increased inventory building, part of which likely reflects some precautionary moves ahead of a feared longshoreman strike.

While real GDP growth looks to be on firmer ground, the economy still appears to be in a near textbook soft landing. Overall growth has slowed, allowing inflation to moderate. The soft landing has come about due to tighter monetary policy, which has slowed demand, and increased immigration, which has boosted labor force growth. The unemployment rate has risen 0.4 percentage points since the start of the year to 4.1% and is likely headed slightly higher.

The Federal Reserve is expected to make the case for a quarter-point cut in the federal funds rate at its July 30 FOMC meeting. We expect four or five quarter-point cuts in total and look for the funds rate to settle at around 4.25%. Long-term rates will decline only modestly from current levels and will rise slightly as economic growth strengthens again in 2025. We look for the spread between conventional 30-year fixed-rate mortgages and 10-Year Treasuries to gradually narrow, bolstering home sales and housing starts next year.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice. Any forward-looking statements or forecasts are not guaranteed and are subject to change at any time. Information from external sources have not been verified but are generally considered reliable.

© 2024 CAVU Securities, LLC