Another Month of Steady but Moderating Job Growth

- Employers added 151,000 in February, topping January’s downwardly revised 125,000-job gain.

- The unemployment rate inched up to 4.1% from 4.0%.

- Job gains broadened, with health care (+52,000), financial activities (+21,000), transportation and warehousing (+18,000), and social assistance (+11,000) leading growth.

- Part-time employment for economic reasons jumped by 460,000; those not in the labor force but wanting a job rose by 414,000.

- Wage growth eased to just 4.0% year-over-year, down from 4.2% in January.

- Secretary Bessent noted the economy is shift away from stimulus-driven growth, which will likely result in more moderate job gains this year. The downside risks to growth have clearly increased, and softer hours worked and slower wage growth are consistent with our call for real GDP growth at around a 1.2% pace this quarter.

Sample report copy. Edit here to change this text. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

The February jobs report paints a labor market that’s holding firm but beginning to fray around the edges. Nonfarm payrolls rose by 151,000, outpacing January’s downwardly revised 125,000, though the three-month average dipped to roughly 200,000 from 237,000—a clear sign that hiring momentum is slowing. The unemployment rate crept up to 4.1%, a slight uptick that suggests the labor market’s tightness is beginning to loosen after a prolonged stretch near historic lows.

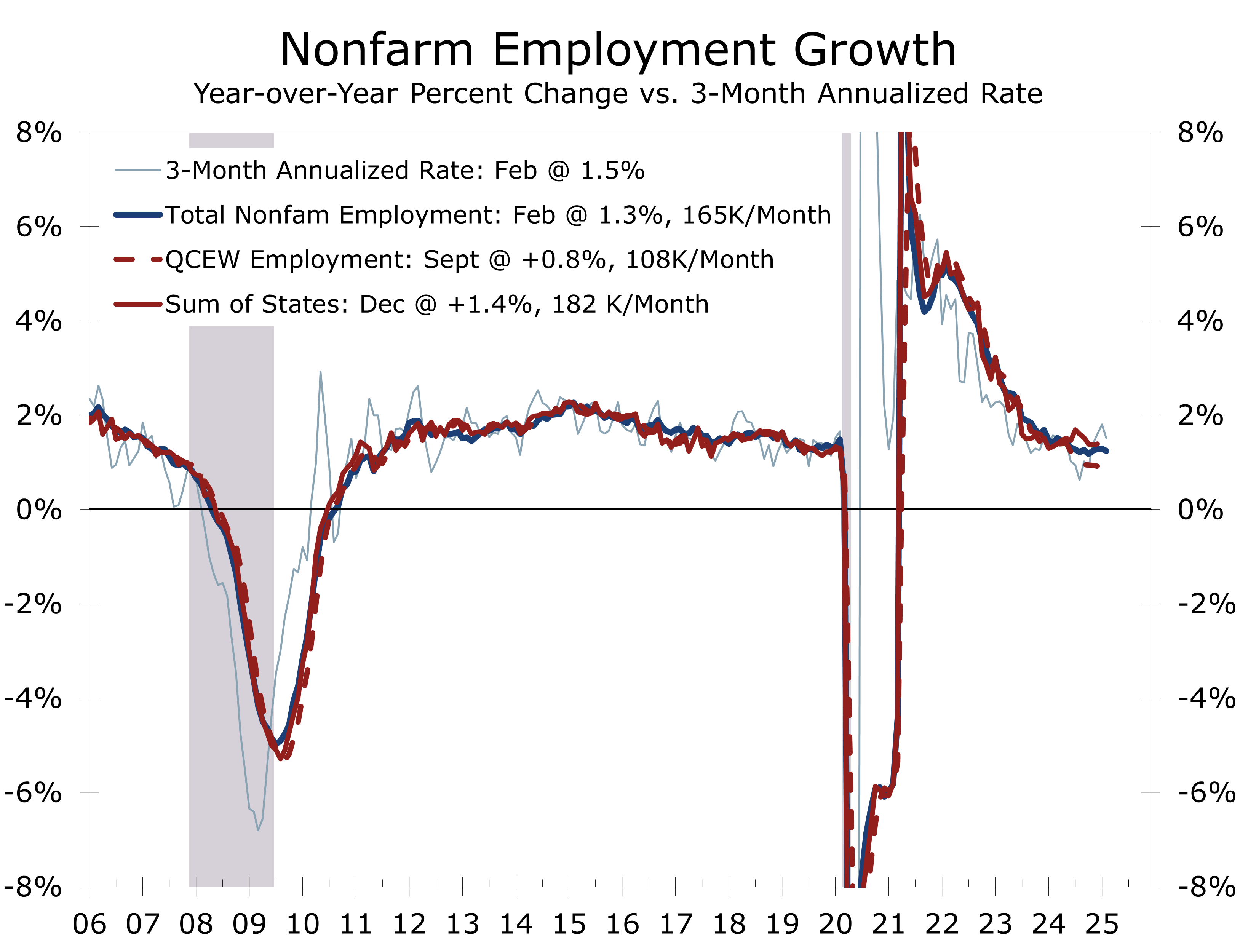

The latest jobs data offer a mixed view of the labor market. The average over the past three months looks perfectly healthy at 200,000 jobs per month. Net hiring the past two months, however, has averaged just 138,000 jobs. By comparison, the latest data show employers have added an average of 168,000 jobs per month over the past year.

The underlying trend of job growth is likely slower than recent data suggest.

QCEW data through September, released after last month’s annual employment revisions, show employers adding just 108,000 jobs per month from September 2023 to September 2024. This suggests job growth will likely be revised lower again in next February’s annual update. Our early projection points to a 0.3% downward revision, or about 475,000 fewer jobs than currently reported. This discrepancy raises caution around the current figures, indicating a weaker labor market than the headline numbers suggest. Slower immigration-driven labor force growth this year further supports this thesis.

Job gains were more broad-based than in recent months, driven by health care, financial activities, transportation and warehousing, and social assistance. The payrolls diffusion index rose 6.0 points to 58.4, near its average of 58.8 for the year prior to Covid, reflecting a welcome broadening beyond the few industries that have dominated growth over the past year. Health care, social services, leisure and hospitality, and government made up over 75% of job gains this past year. Federal government payrolls fell by 10,000, likely due to buyouts and layoffs, while retail trade lost 6,000 jobs, partly due to strike activity.

The breadth of industries adding job increased sharply, both overall and in manufacturing.

A few warning signs are emerging. Part-time employment for economic reasons jumped 460,000 to 4.9 million, indicating more difficulty finding full-time work. Those not in the labor force but wanting a job rose 414,000 to 5.9 million, suggesting more slack in the market. The employment-population ratio dipped 0.2 points to 59.9%, reinforcing the cooling trend.

Wages rose 4.0% year-over-year, down from 4.2% in January, with the average workweek holding at 34.1 hours. Slower earnings growth may ease concerns about wage-driven inflation, giving the Fed more flexibility in its next steps.

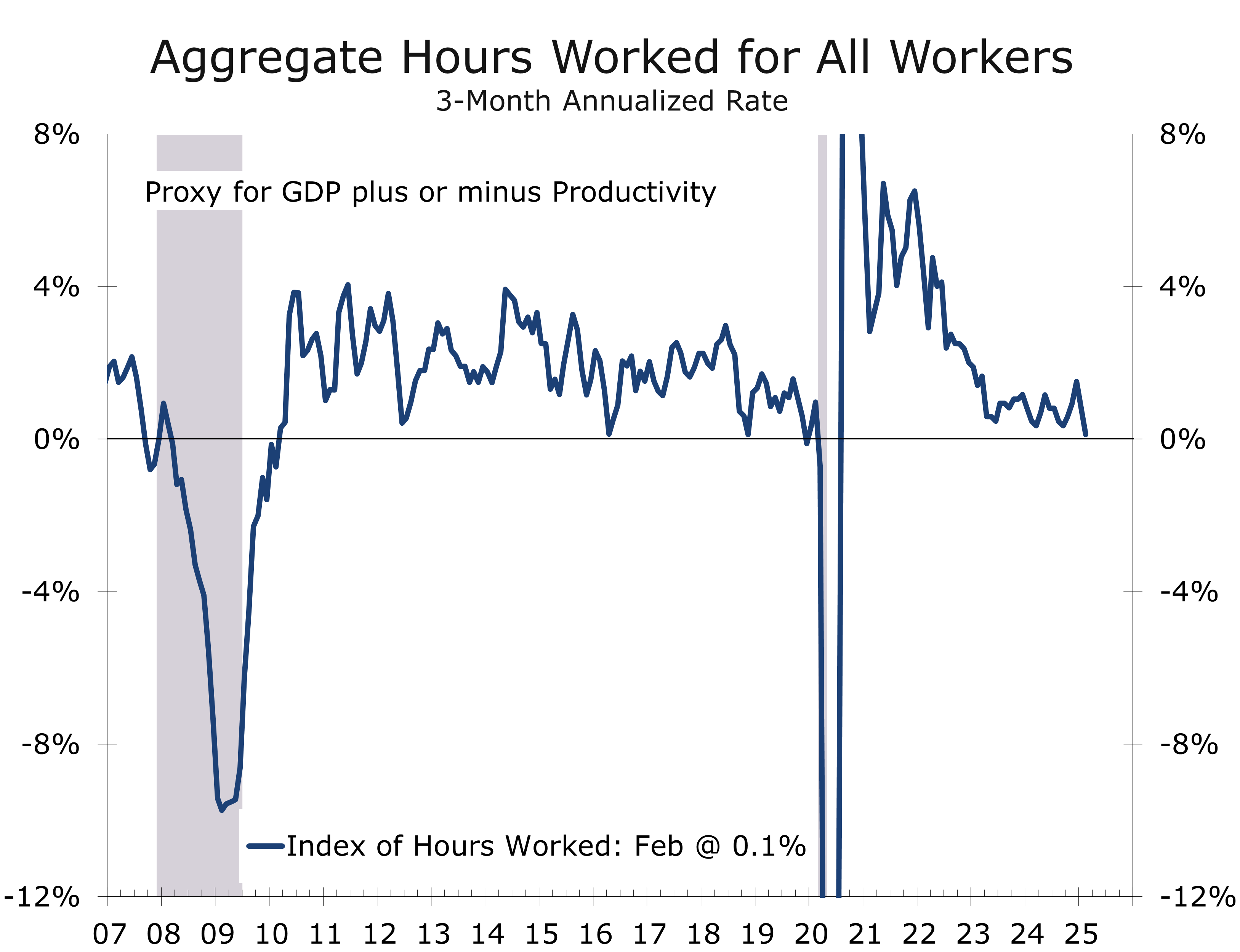

For policymakers, the report delivers a mixed bag. The labor market’s core strength—solid job growth, low unemployment, and slightly more diversified gains—argues for keeping rates steady, at least for now. But the slowdown in hiring, rising part-time work, and softening wage pressures are another indication of the economy losing steam, strengthening the case for an easing this spring. On that point, aggregate hours worked in the economy have risen at just a 0.1% pace over the past three months, implying Q1 real GDP growth somewhere between 1% and 1.5%.

With job growth fraying around the edges, the Fed is likely to focus more on supporting growth.

February’s employment data show a labor market still standing tall but fraying around the edges. Treasury Secretary Bessent noted that he sees signs of the economy rolling over as growth shifts from stimulus-driven growth to private sector-driven growth. The Fed faces a challenge of managing this transition, which currently appears chaotic and has more unknowns than usual. With elevated risks and a longer timeline for reaching its 2% inflation target, the Fed will likely lean more toward supporting growth.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

March 7, 2025

Mark Vitner, Chief Economist

Piedmont Crescent Capital

(704) 458-4000