Cutting Too Late is Preferable to Too Soon

- The FOMC held the fed funds target range at 5.25%-5.50% at its July meeting and sees inflation moderating further as the labor market moves into better balance.

- Powell’s press conference emphasized the fine line between cutting rates too soon and waiting too long but the bottom line was that they are close to cutting rates.

- The Fed’s Policy Statement noted the balance of risk between inflation and labor market conditions is now essentially even, as opposed to the earlier heavier focus on inflation.

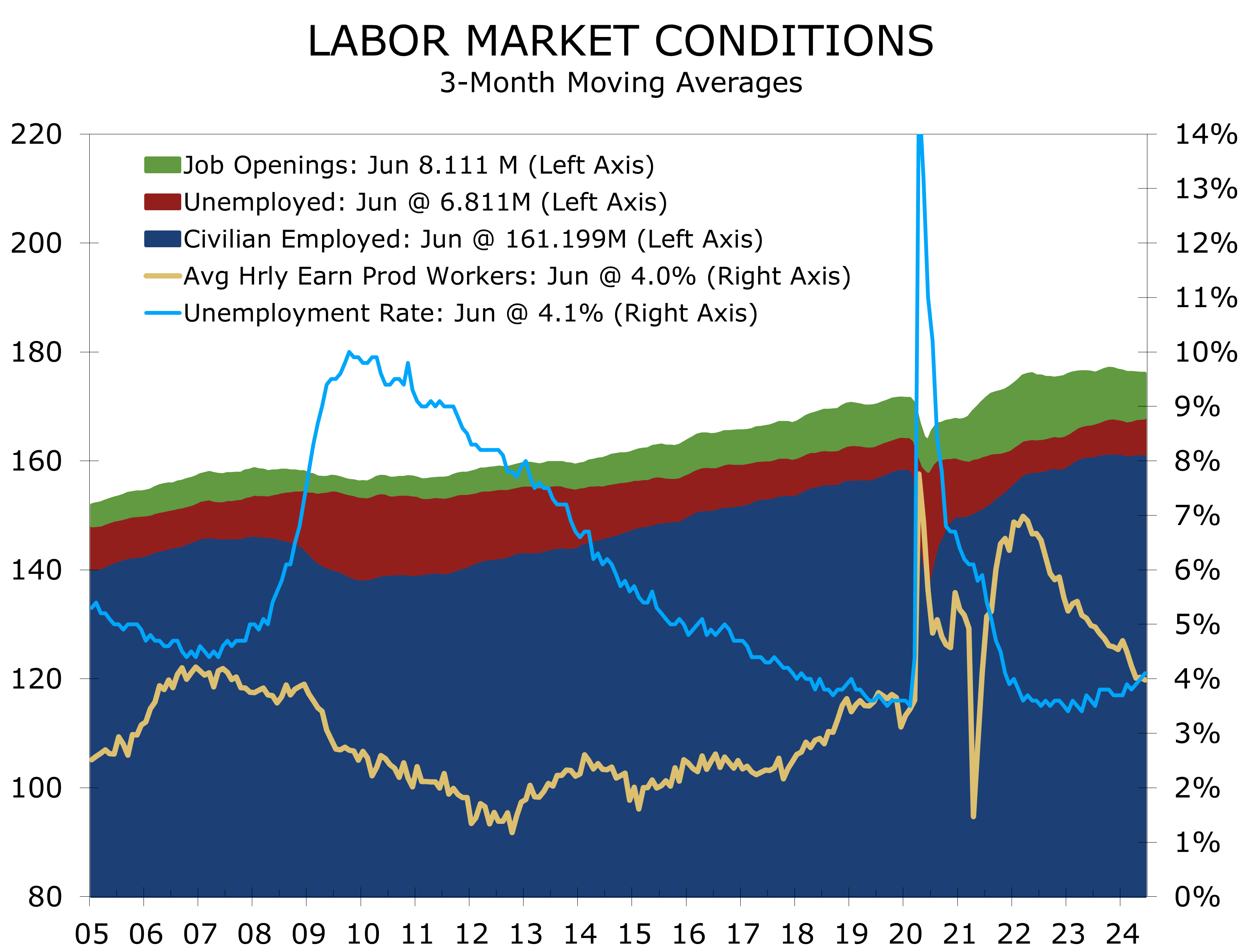

- Powell highlighted the rarity of bringing inflation down so sharply without a corresponding sharp rise in the unemployment rate.

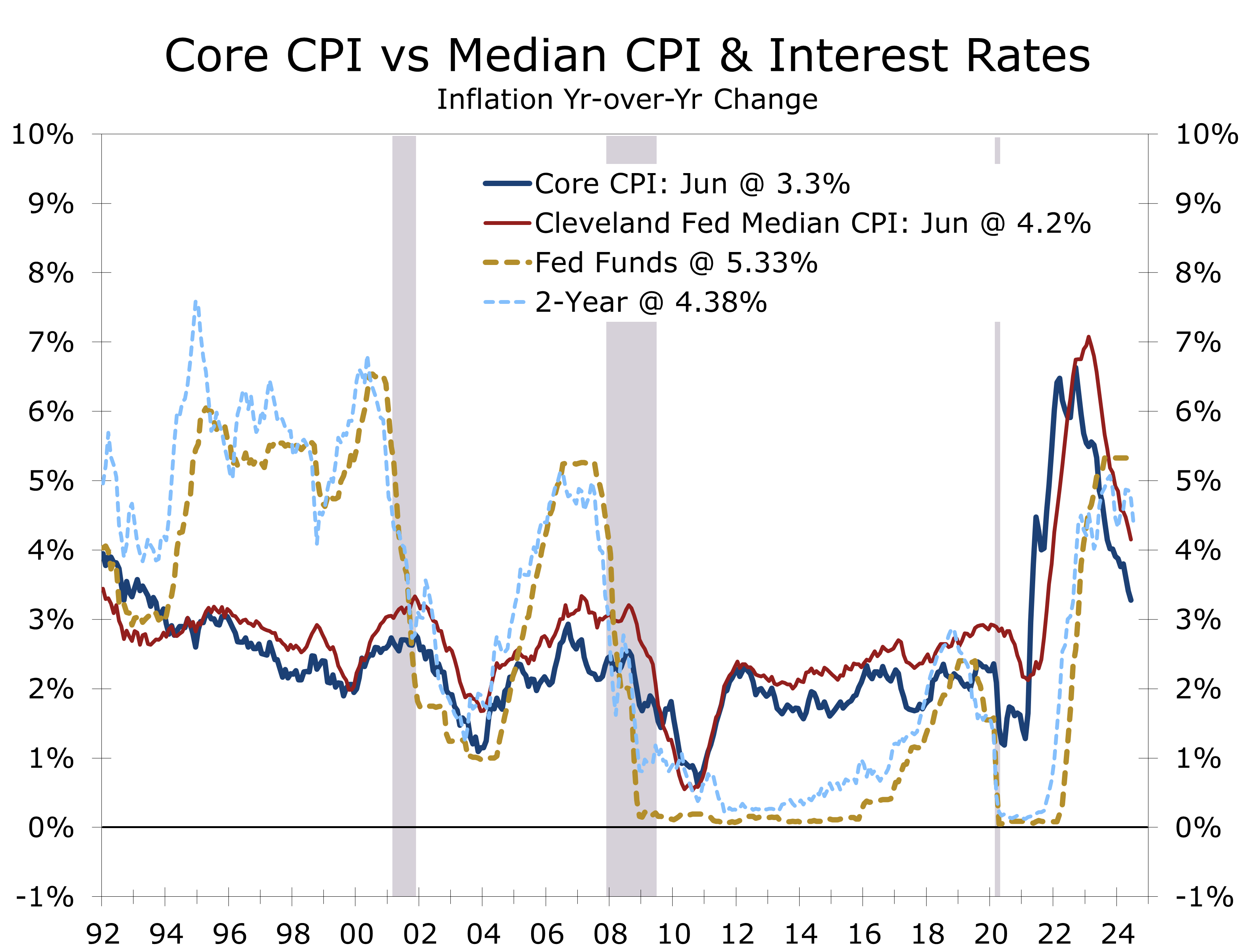

- We continue to look for the Fed to reduce the federal funds rate twice this year (September and December), followed by two more in early 2025. We are expecting a total of four or five rate cuts over the next year, which is consistent with the 2-Year Treasury post meeting which fell to 4.38%.

As was widely anticipated, the Federal Open Market Committee (FOMC) unanimously decided to maintain the target range for the federal funds rate at 5.25-5.5% at its July meeting. The Fed’s decision closely aligns with market expectations, as inflation continues to moderate and job growth continues to decelerate. The FOMC’s policy statement introduced a few key changes, signaling a potential shift in policy at the September meeting.

Balance was a key theme in the Fed’s policy statement and Powell’s press conference. The language in the policy statement was updated to reflect a focus on risks to both sides of the Fed’s dual mandate—price stability and full employment—moving away from the earlier singular focus on inflation risks. This shift suggests inflation may no longer be a significant barrier to lowering rates, particularly if the labor market continues to cool.

Inflation and unemployment risks are more balanced than at any time since the pandemic.

The policy statement and Powell’s comments were somewhat hawkish, emphasizing the necessity of sustained progress towards the 2% inflation target before implementing rate cuts. The recent moderation in inflation, coupled with signs of easing housing costs, supports this cautious optimism.

The 2-Year Treasury note has historically led the federal funds rate by about one year. This relationship is consistent with four quarter-point rate cuts.

Chair Powell provided additional clarity on the Federal Reserve’s stance during the press conference. He acknowledged the possibility of rate cuts beginning in September, contingent upon the continuation of recent inflation and labor market trends. Powell emphasized that a strong majority of FOMC members supported maintaining the current target range for the federal funds rate in July. However, he also hinted at some discussion within the committee regarding the potential benefits of rate cuts at the July meeting.

Powell does not fear the Sahm rule. Recession warning ‘rules’ only work until they stop.

Powell also addressed concerns about the recent rise in the unemployment, particularly in relation to the Sahm rule. He acknowledged that some traditional recession warnings, such as the inverted yield curve, had not followed their usual predictive patterns due to the unusual nature of the post-pandemic business cycle. He emphasized that the recent softening in the labor market should be viewed as a sign of normalization rather than excessive weakening.

Powell emphasized that the FOMC is closely monitoring the labor market and is well-prepared to provide support if necessary. This aligns with our reference to Newton’s Law of Motion, suggesting the Fed may need to ease more aggressively to counteract the downward momentum in the labor market.

The FOMC decision to hold rates steady likely reflects a compromise. Dovish members may have favored a rate cut now, given the progress on inflation and cooling labor market. By contrast, hawkish members, wary after the earlier “transitory” misstep, prefer to wait for more data.

The FOMC weighed an immediate cut before unanimously deciding to hold rates steady.

Powell mentioned the Fed’s consideration of external prognosticators, possibly alluding to former Fed Vice Chair Alan Blinder, who advocated for a July rate cut. Blinder cited potential difficulties in cutting rates in September due to election-year concerns. He also noted the November meeting, scheduled just one day after the election, would be an inopportune time to cut, potentially requiring a larger move in December.

We feel Blinder’s concerns are overblown. Inflation has moderated sufficiently enough for the Fed to cut rates, even if a disappointing inflation report surfaces before the September meeting. Powell also emphasized residual seasonality might have complicated the interpretation of monthly data, noting year-over-year data shows a more consistent pattern.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

July 31, 2024

Mark Vitner, Chief Economist

Piedmont Crescent Capital

mark.vitner@piedmontcrescentcapital.com

704-458-4000