Even Weaker than Lowered Expectations

-

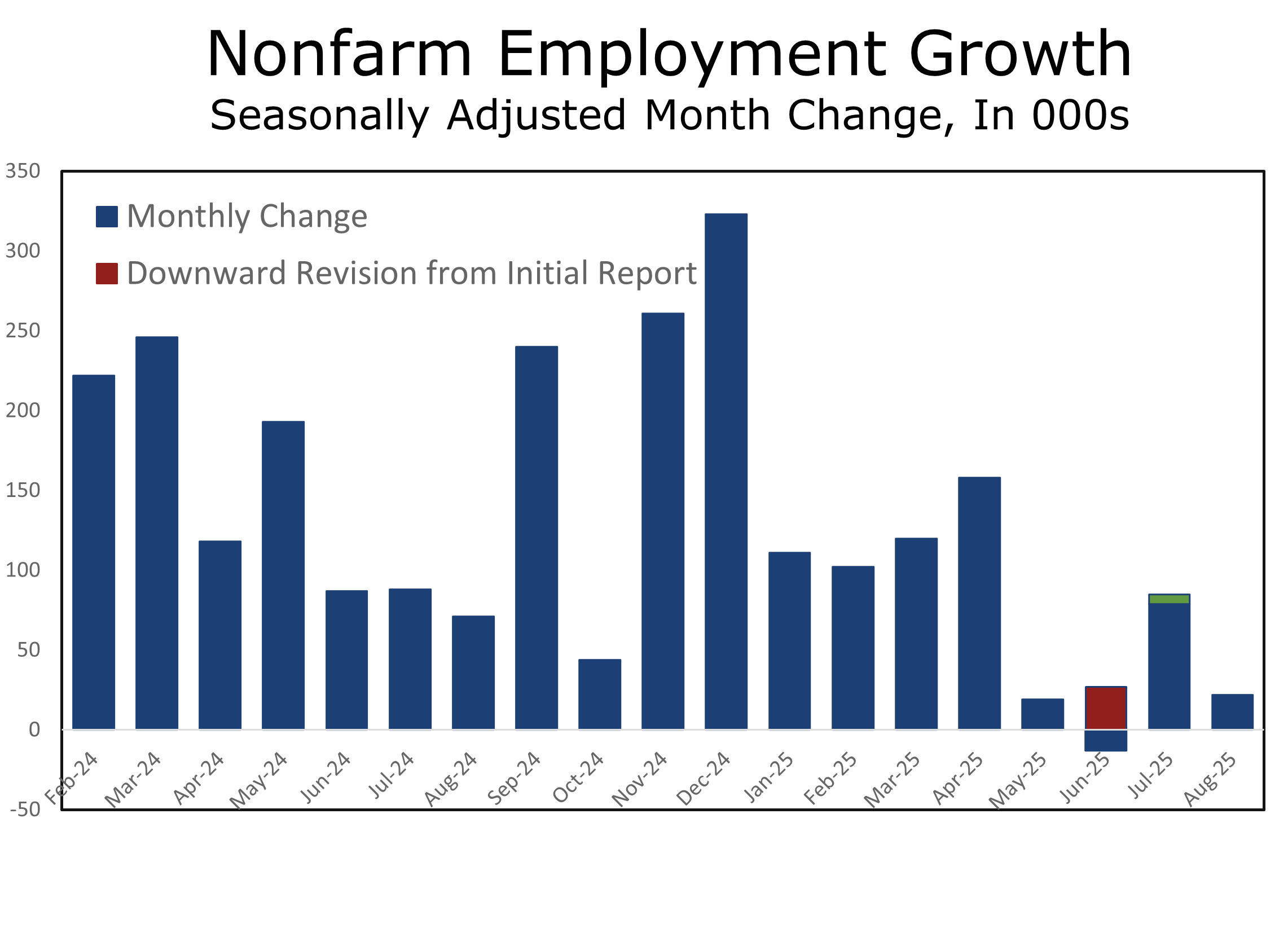

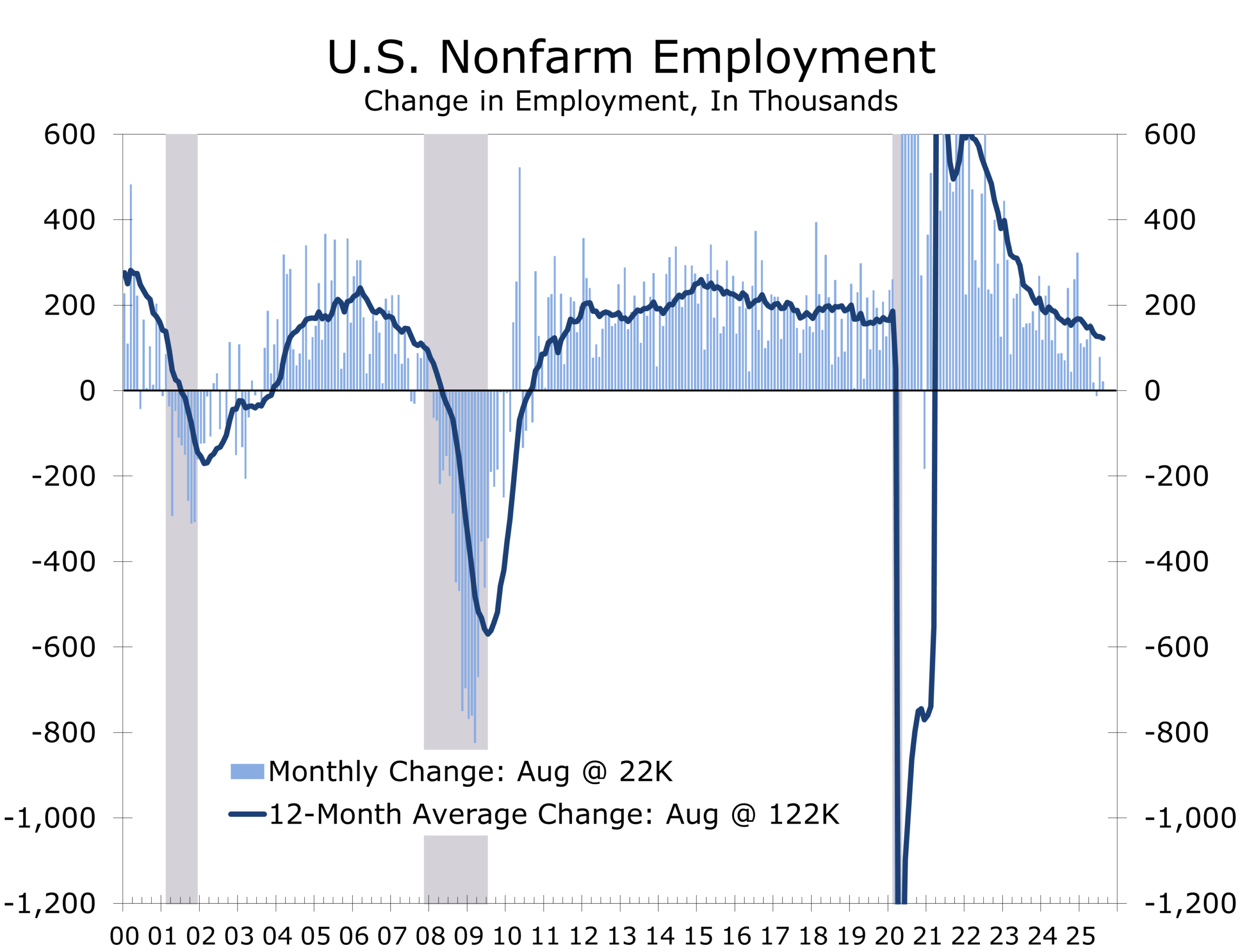

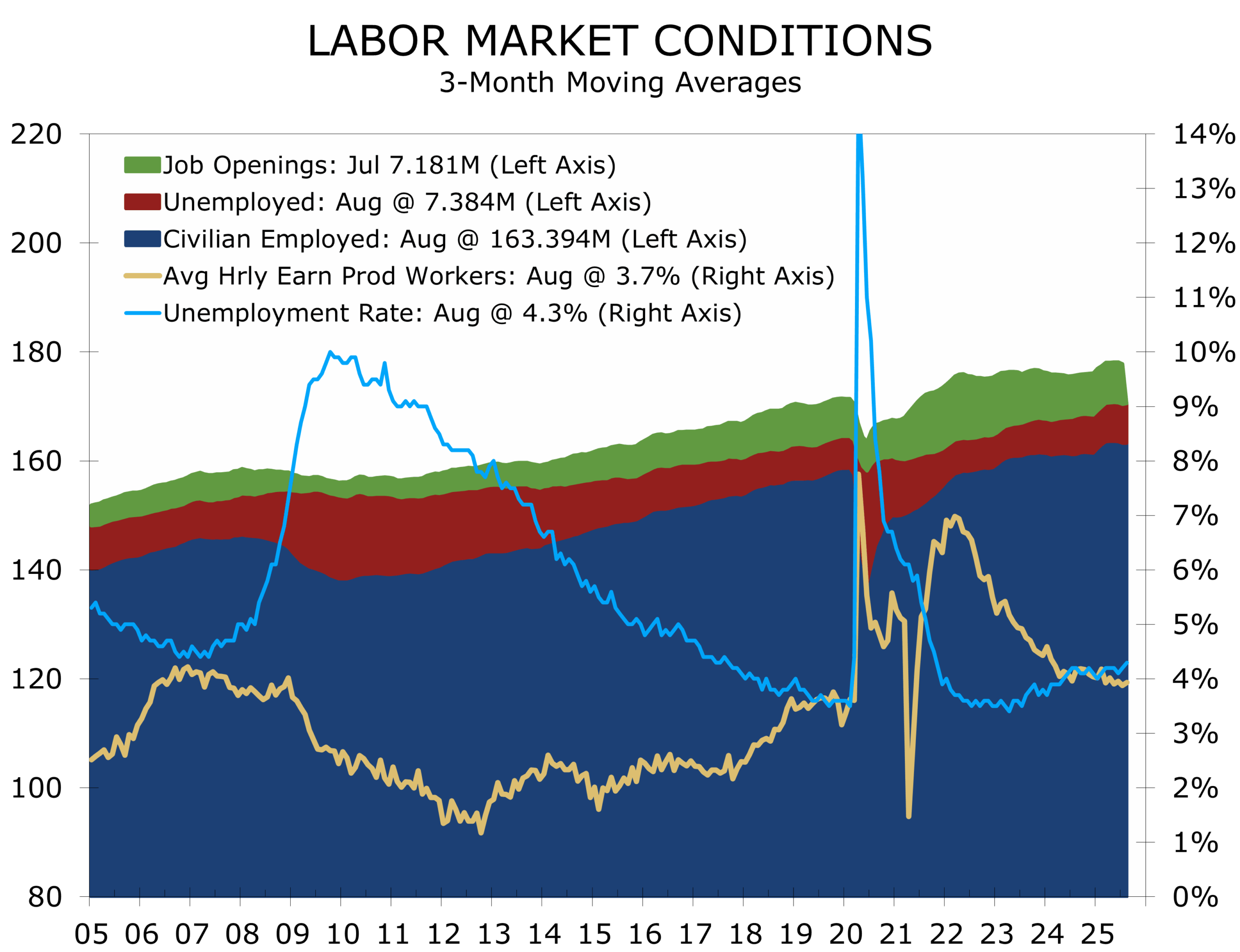

- Nonfarm payrolls rose just 22,000 in August, with downward revisions subtracting 21,000 from prior months. Job growth has averaged only 29,000 over the past three months.

- We had warned that August tends to be a rogue month, with initial estimates coming in inexplicably weak and typically revised higher. We expected a below-consensus 60,000-job gain.

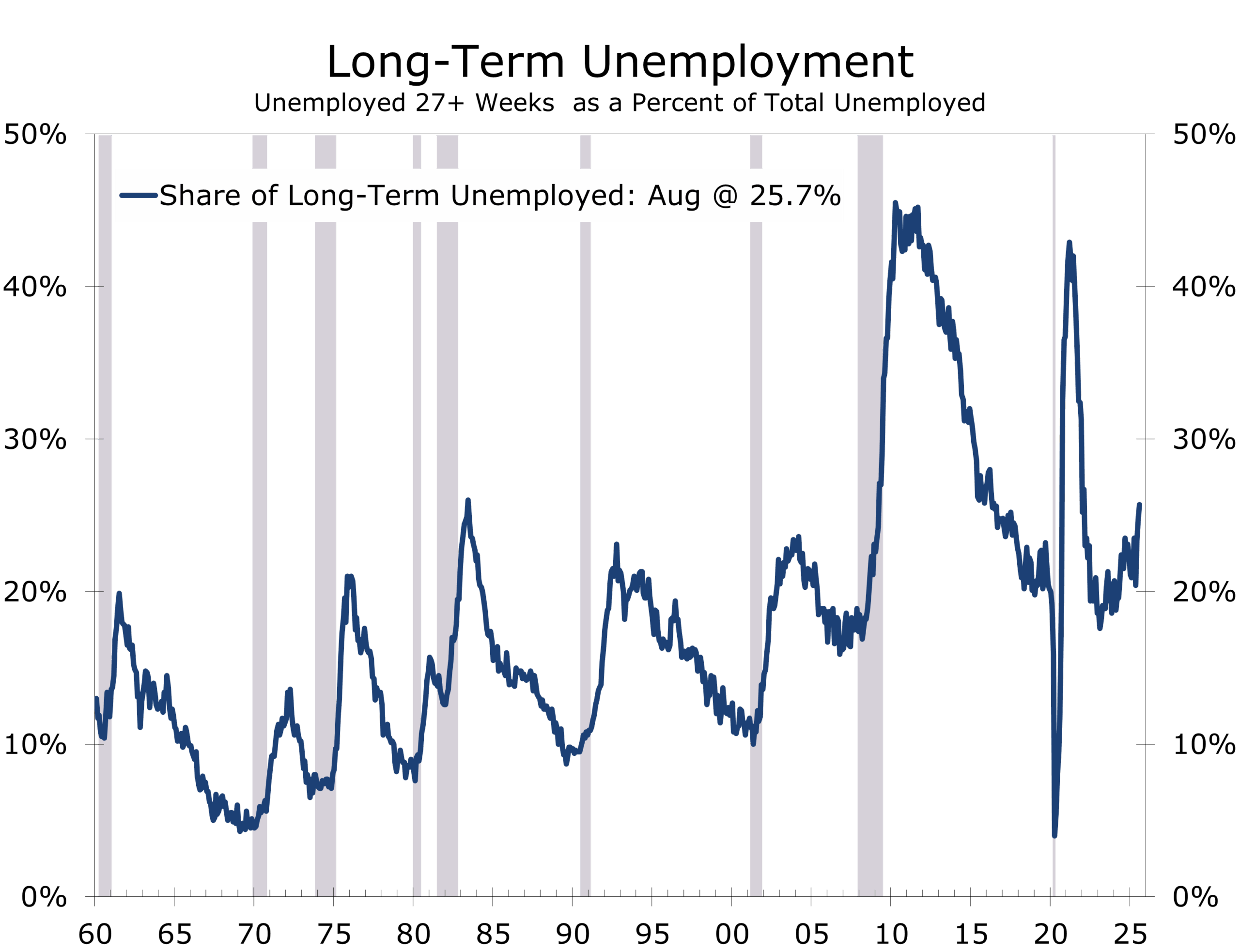

- The unemployment rate rose to 4.3%, its highest since late 2021. Long-term unemployment is elevated, with outsized growth in those jobless for extended periods.

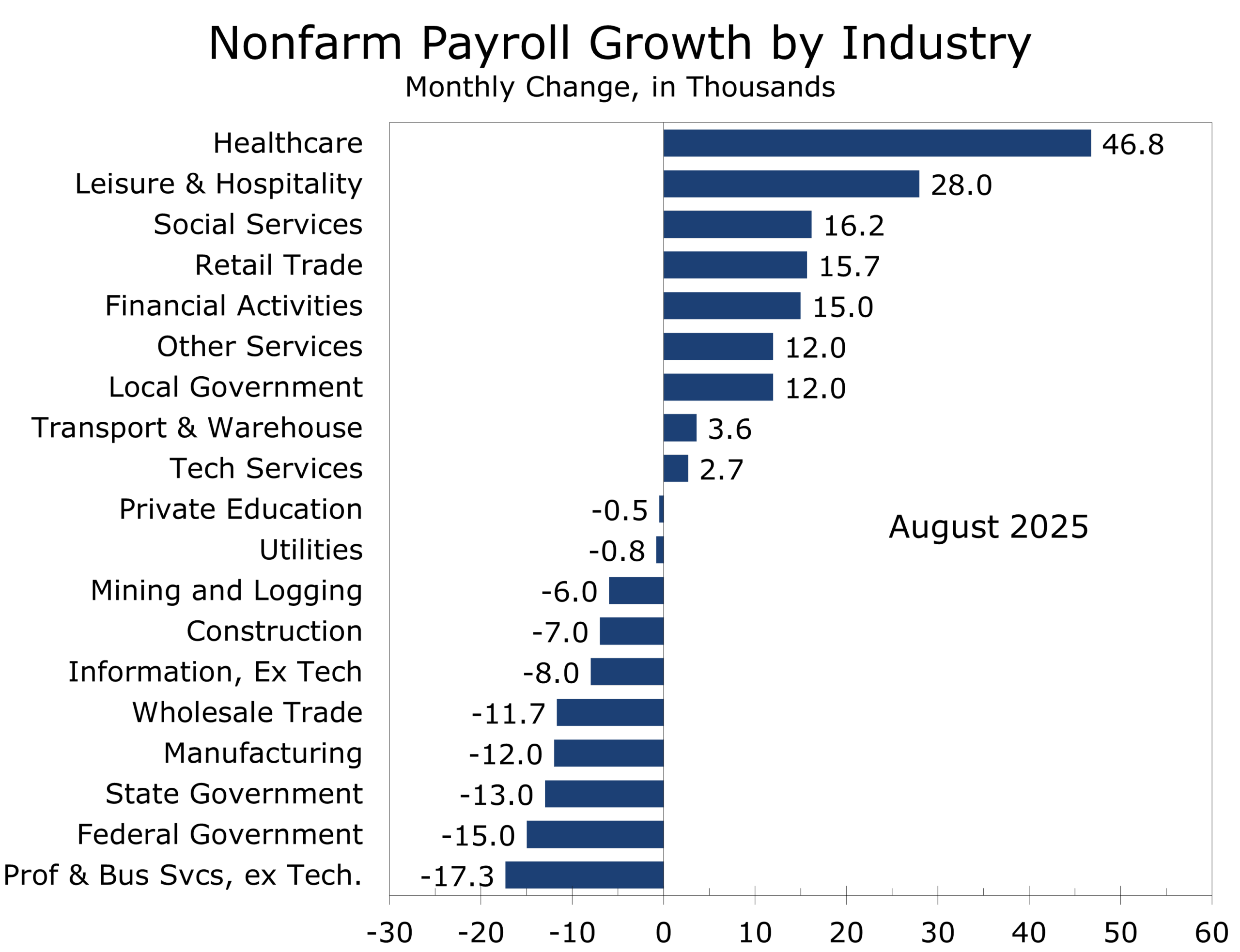

- Health care (+31,000) and social assistance (+16,000) again led job creation, offset by declines in federal employment (–15,000), manufacturing (–12,000), and mining (–6,000). Transportation equipment was held back by strikes (–15,000).

- Household measures remain soft: labor force participation stayed at 62.3%, the employment-population ratio held at 59.6%, and new entrants to the labor force fell.

- Immigration enforcement is slowing labor force growth, limiting supply and muting the signal from a still-low headline unemployment rate. Finding a job is becoming more difficult as job openings fall to pre-pandemic lows.

- Average hourly earnings rose 0.3% (3.7% y/y), while the workweek was steady at 34.2 hours.

- We continue to estimate payrolls are overstated by roughly 30,000 per month, meaning actual job growth since April may be near zero. Benchmark QCEW data, due September 9, will clarify the true trajectory heading into the tariff storm.

The Labor Market Is Losing Steam—with Nowhere Left to Hide

August employment data underscored a slowing labor market. Nonfarm payrolls rose by just 22,000, and revisions to June and July reduced prior gains by 21,000. Over the past three months, job growth has averaged only 29,000—well below the replacement rate needed to keep up with labor force growth.

August is notoriously difficult to forecast. It coincides with the start of the school year, but the timing of when universities and public school systems report hiring varies year-to-year. It is also the peak of vacation season, which reduces the survey response rate. These quirks often depress the initial estimate, which is typically revised higher in subsequent months. That is why we had anticipated a below-consensus gain of 60,000 jobs, even before the data confirmed far weaker growth.

August’s first print is notoriously weak—revisions almost always move higher

Hiring continues to be narrowly concentrated. Health care added 31,000 jobs and social assistance added 16,000. Leisure and hospitality also posted a larger gain, adding 28,000 jobs in August. That game is a bit ephemeral, however, as weaker hiring earlier this summer meant there were fewer than usual seasonal separations. Several sectors posted outright job losses, including federal government (–15,000), manufacturing (–12,000), wholesale trade (–12,000), temporary held (-12,000) and mining (–6,000). Within manufacturing transportation equipment dropped 15,000, reflecting strike activity at a major defense contractor. Private sector hiring outside care-related industries remains flat.

.

Unemployment Creeps Higher, With Slack Deeper Than It Appears

The unemployment rate ticked up to 4.3%, the highest since December 2021. Labor force participation rose 0.1 point 62.3% but remains in its recent range and is down 0.4 percentage points from a year ago. The employment-population ratio held at 59.6% and has drifted lower since last summer.

Long-term unemployed now make up more than 1 in 4 jobless workers

Long-term unemployment rose to 1.9 million, accounting for more than a quarter of the unemployed—an unusually high share outside of recessions. Job openings have fallen to their lowest since before the pandemic, making it harder for workers to find new positions. New entrants to the labor force fell by nearly 200,000 in August, highlighting the fragility of supply.

Tighter immigration enforcement is compounding these pressures. Slower inflows of workers are constraining labor force growth, making the headline unemployment rate appear lower than underlying slack would normally justify. Meanwhile, the number of people not in the labor force but wanting a job rose to 6.4 million, up more than 700,000 over the past year.

AI Disruption and Budget Caution Continue to Reshape White-Collar Work

White-collar employment remains soft. Tech-related jobs Hiring also rebounded slightly in technology services, adding 2,700 jobs in August. The gain follows a long string of declines and hiring has been sluggish amidst to rollout and continuous improvement of various AI platforms. Professional and business services show no momentum, as firms curb use of consultants in response to AI-driven productivity, tighter budgets, and slower final demand.

This erosion contrasts with buoyant stock market headlines and points to deeper structural changes rippling through white-collar work.

FOMC Outlook: The Clock Is Ticking

The Fed now has multiple months of evidence showing a labor market that is not collapsing but is clearly losing momentum. Average hourly earnings are up just 3.7% from a year ago, and participation has stalled. The risks of overheating have receded; stagnation is now the larger concern.

Chair Powell has argued the labor market is “in balance,” but the balance appears increasingly fragile—maintained by weakness on both supply and demand sides. Further softness in consumer demand, renewed geopolitical risks, or a cooling housing market could tip that balance quickly.

With unemployment edging higher, payroll growth near zero, and immigration limits tightening supply, the case for a September rate cut is strong. Waiting risks losing control of the narrative—and letting stagnation slip into contraction. The financial markets have now also fully priced in a second cut in October, which we believe the Fed will push back on in order to prevent an uptick in the 10-Year Treasury yield and mortgage rates.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

September 5, 2025

Mark Vitner, Chief Economist

(704) 458-4000