Tariffs Will Add to Stubborn Inflation in 2025

- The world continues to grapple with the rapid policy shifts introduced by the Trump Administration. Wide-ranging tariffs have become a reality—some serving as short-term negotiating tools, while others aim to reinforce trade agreements and reshape the global trading structure. These tariffs will contribute modestly to inflation in 2025, though their impact will diminish the following year. U.S. manufacturing is expected to see modest growth this year.

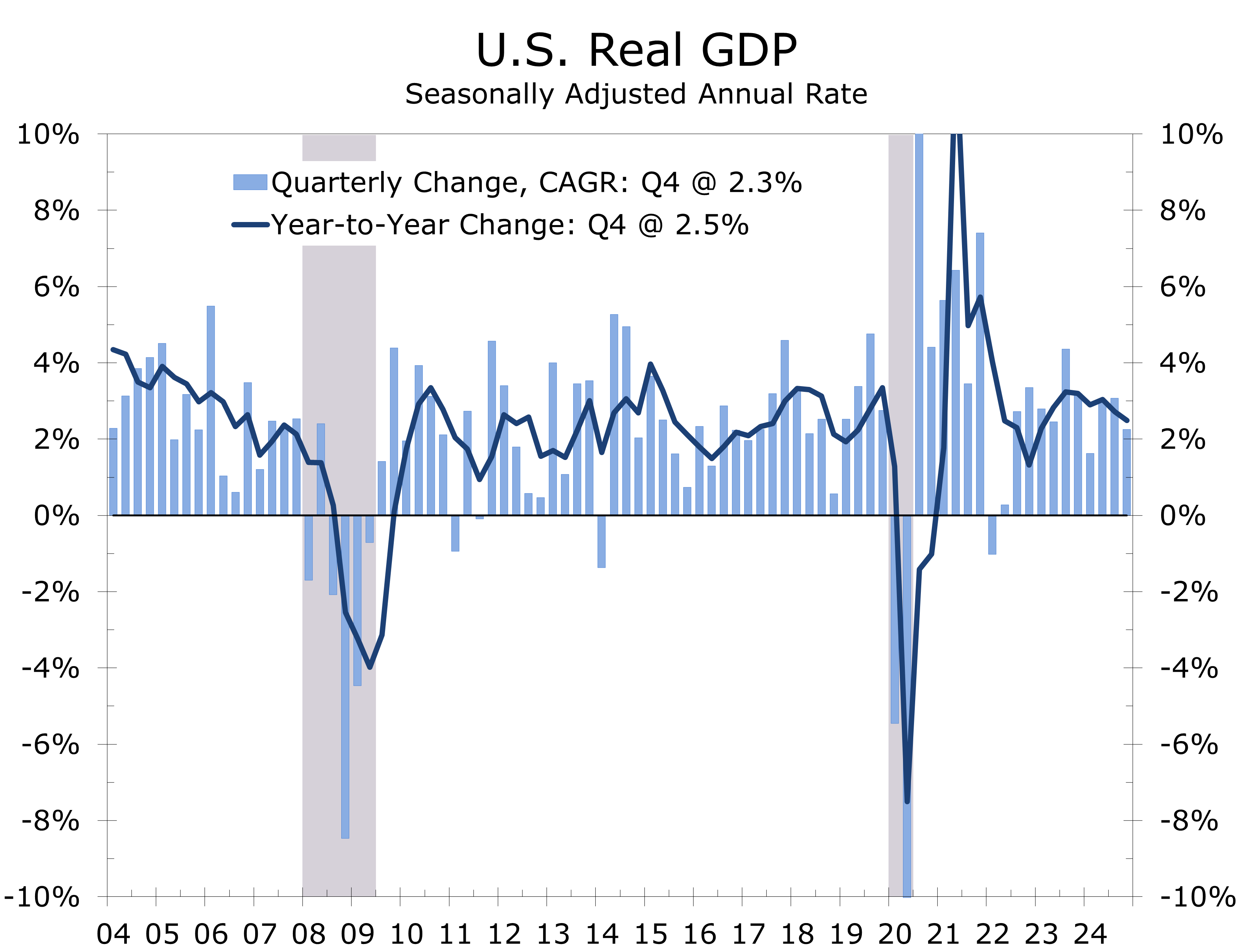

- Economic growth fell short of expectations in Q4, with real GDP rising at a modest 2.3% annual rate. However, final domestic demand remains steady at around 3%, consistent with the past two years. The Q4 GDP shortfall was primarily driven by a surge in imports ahead of anticipated tariffs, a trend that may persist in the early months of this year.

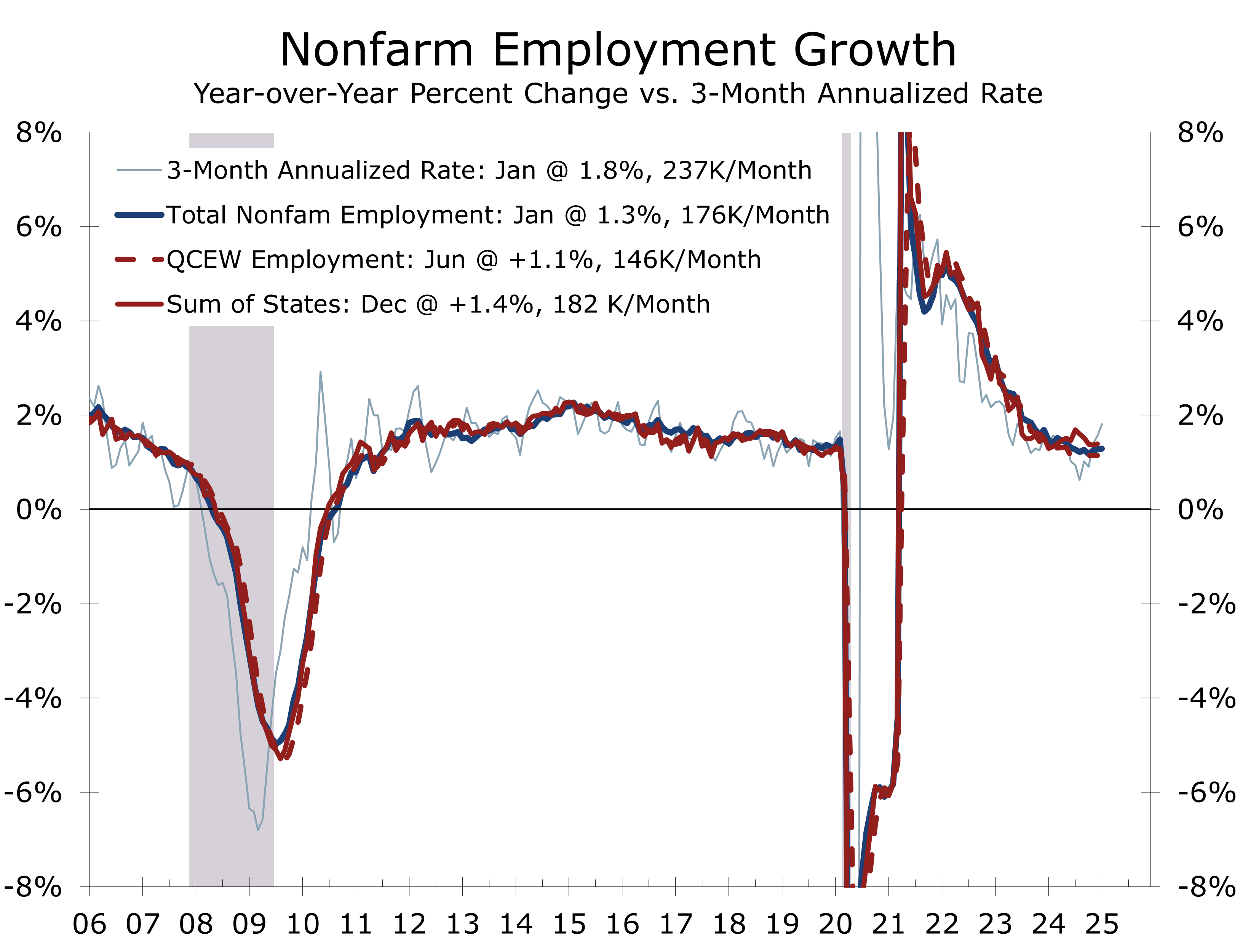

- Job growth began the year slowly, with employers adding just 146,000 jobs in January. However, upward revisions to the previous two months lifted the three-month average to 237,000. Annual revisions showed 589,000 fewer jobs added between March 2023 and March 2024, in line with expectations. Growth remains heavily concentrated in health care and social services, leisure and hospitality and government.

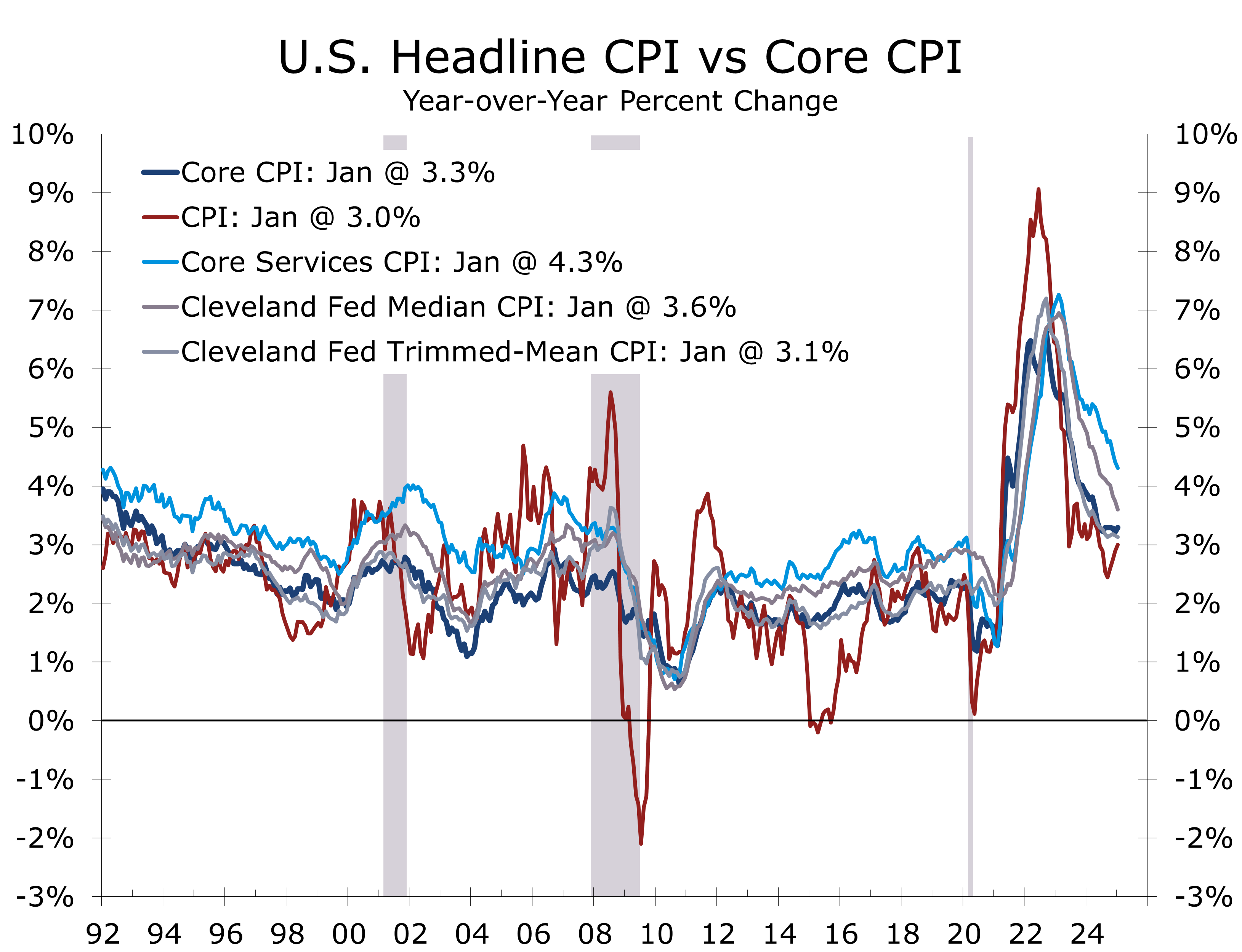

- Inflation began the year on a surprisingly higher note, and annual data revisions showed slightly less progress has been made at returning inflation to the Fed’s 2% target. With higher tariffs looming, inflation may prove persistent than had been anticipated, likely delaying the Fed’s next rate cut by at least a few months.

- President Trump has moved quickly to implement his campaign agenda, imposing tariffs, strengthening border security, expediting deportations of undocumented persons convicted of violent crimes, reducing government waste, and downsizing the federal workforce. The rapid pace has caught his opposition off guard, leading to some unexpected early progress. This month’s CAVU Compass explores the prospects and implications of these actions.

- The administration has secured trade deals with Colombia, Panama, Canada, and Mexico and recently announced plans to launch peace talks between Russia and Ukraine. We estimate a 65% probability that the war will end this spring. Meanwhile, the fragile ceasefire between Israel and Hamas remains at risk, as Trump and Netanyahu have taken a more aggressive stance to secure the release of hostages from the October 7 attacks. Renewed conflict could push oil prices and shipping costs higher, while a ceasefire in Ukraine would help ease inflationary pressures and support economic growth, particularly in Europe.

The world continues to grapple with the rapid policy shifts introduced by the Trump Administration, particularly in the area of trade. From steel and aluminum tariffs to broad-based reciprocal measures against countries that impose duties on U.S. goods, the Administration’s aggressive stance threatens to disrupt global markets, reshape supply chains, and force businesses to alter the way they source and produce products. While some tariffs are intended as short-term negotiating tools, others reflect a broader strategy to reinforce existing trade agreements, such as NAFTA/USMCA, and others seek to restructure the global trading system.

One of the most significant consequences of Trump’s tariffs is their impact on inflation and consumer spending. As tariffs raise the cost of imported goods, businesses often pass these costs on to consumers, driving prices higher. While the overall effect on U.S. inflation in 2025 is expected to be modest, it remains a concern for policymakers and the Federal Reserve, particularly as inflation has already proven more resilient than anticipated. Tariffs could also contribute to inflation by fueling inflation expectations, giving businesses greater flexibility to raise prices. The primary risk is a feedback loop—firms preemptively hike prices, households adjust expectations, and wage pressures build—potentially forcing the Fed to take a more restrictive stance.

We have adjusted our inflation forecast, with tariffs now expected to add between 0.4 and 0.5 percentage points to core inflation this year. While this impact is expected to gradually diminish, the path back to the Fed’s 2% target will be longer-. Higher inflation will also weigh on consumer spending, particularly among middle- and lower-income households. Recent consumer sentiment surveys indicate rising near-term inflation expectations and weaker overall sentiment, with middle- and lower-income households feeling the greatest strain.

U.S. manufacturing is projected to experience modest growth this year as some companies relocate production to the U.S. to circumvent tariffs. The steel industry stands to gain from the 25% tariffs on all imported steel, while aluminum producers may also benefit, though the impact will be limited due to the relatively small number of operating aluminum smelters in the U.S. The broader implications of tariffs are more intricate—higher input costs could negate some of these advantages, particularly for sectors heavily dependent on steel and aluminum. Furthermore, retaliatory tariffs from other nations have the potential to hinder U.S. exports. The economic strain of U.S. trade policies is anticipated to affect Europe, Canada, and Mexico more significantly, although exemptions for essential imports such as aluminum, softwood lumber, and auto parts might alleviate some of the impacts.

We expect U.S. economic growth to slow to a 2% pace in the first half of this year. Imports are likely to exert a modest drag on GDP growth in Q1, as firms front-load shipments ahead of tariff increases. However, some of this impact will be offset by increased inventory building. Additionally, higher long-term interest rates will continue to weigh on home buying and overall spending on big-ticket items. Efforts to curb government spending will also likely lessen the tailwind from the IRA and CHIPS programs driving business fixed investment.

Inflation began the year with higher-than-expected increases in both consumer and wholesale prices for January. The Consumer Price Index (CPI) rose by 0.5%, marking its largest monthly gain since August 2023, while core CPI increased by 0.4%. The Producer Price Index (PPI) also exceeded predictions, with a headline increase of 0.4%. Additionally, annual data revisions indicated that inflation has not decreased as much as previously estimated, raising concerns that the Federal Reserve may maintain higher interest rates for an extended period.

Market expectations have adjusted accordingly, with no anticipated rate cuts through spring and summer and only a slight possibility of one by the end of the year. Some former Federal Reserve officials have even suggested the possibility of a rate hike, though this is considered unlikely. In his February congressional testimony, Fed Chair Jerome Powell confirmed that the central bank is not in a hurry to reduce rates, supporting the view that the federal funds rate will remain above its neutral level well into next year.

The market’s initial response to January’s inflation data may be exaggerated. While inflation is still on a downward trend, the final reduction from 3% to 2% is expected to take longer than the drop from 9.1% to 3%. The post-pandemic unwinding of price spikes, particularly in used cars and gasoline, amplified earlier progress. Moreover, upcoming tariff increases could apply upward pressure on prices, although consumer resistance to price hikes may mitigate the impact, affecting sales and prompting some companies to adjust their pricing strategies. Higher productivity and moderating wage growth are expected to contribute to easing inflation later in the year, creating a more stable environment for businesses and consumers.

Although the notable increases in CPI and PPI sparked concerns, they may exaggerate the potential inflation threat. Seasonal factors likely influenced the January data, as price adjustments for items with infrequent changes tend to cluster at the beginning of the year. Similar patterns have been observed in previous years, driven by one-time factors such as insurance premium resets and wage negotiations from the prior year. These seasonal distortions suggest that progress in reducing inflation is slowing but not halting or reversing. Importantly, the underlying data in the PPI report indicate that the personal consumption expenditures (PCE) deflator—the Federal Reserve’s preferred inflation measure—is unlikely to rise as sharply as CPI and PPI. Furthermore, both median and trimmed-mean CPI continue to trend downward, as do similar measures for the PCE deflator.

The financial markets were further unnerved by unexpectedly poor results from the early January University of Michigan Consumer Sentiment Survey. Consumer sentiment dipped slightly, falling to 73.2 from 74.0 in December, which was only modestly worse than expected. The decline was entirely driven by the expectations component, which fell 3.1 points to its lowest level in six months, reflecting increased concerns over future economic conditions and inflation. In contrast, the current conditions index rose 2.8 points, as low gasoline prices and solid employment conditions continued to bolster perceptions of personal finances.

The divergence between the two indices highlights consumers’ growing worries about inflation and some trepidation about the incoming Trump administration, which promises to unleash significant changes. While earlier progress in slowing inflation had brought some relief, concerns about future price increases—exacerbated by uncertainty surrounding tariffs—dampened sentiment. Year-ahead inflation expectations surged to 3.3%, up from 2.8% in December, marking the highest level since May 2024. Long-term inflation expectations also increased, climbing 0.3 percentage points to 3.3%, the largest monthly increase since May 2021 and the highest level since June 2008.

While the surprisingly large jump in inflation expectations is unnerving, it is important to note that the preliminary Consumer Sentiment data, particularly the inflation components, are often misleading. The more comprehensive data reported at end of the month often reverse early-month swings in inflation expectations entirely. That said, there are ample reasons to believe the uptick in inflation expectations is more genuine than in the past. Progress on reducing inflation has stalled in recent months, and the Fed has acknowledged that the path back to its 2% inflation target is likely to be longer and more uneven than previously anticipated.

Heightened concern about inflation likely reflects recent price hikes at grocery stores, particularly for frequently purchased items such as eggs. The UMich notes that the rise in inflation concerns is evident across various demographic groups, with particularly strong increases among lower-income households and politically Independent-leaning individuals. Combined with added inflationary risks from tariffs, inflation expectations may remain elevated in the near term, giving the Federal Reserve further reason to remain cautious. The Fed places significant emphasis on keeping inflation expectations anchored and will work to discourage consumers from accelerating purchases to stay ahead of anticipated price increases.

Retail sales experienced a significant decline in January, with the headline figure contracting by 0.9% alongside a broad-based pullback across key categories. While adverse weather and seasonal adjustment factors played a role in the reduction, the widespread weakness indicates a softer start to Q1 consumer spending. A major contributing factor was the downturn in auto sales, while discretionary categories—such as sporting goods, furniture, and building materials—witnessed the steepest declines. Additionally, non-store retail sales, primarily online, decreased, prompting questions about whether weather alone was responsible for January’s weakness.

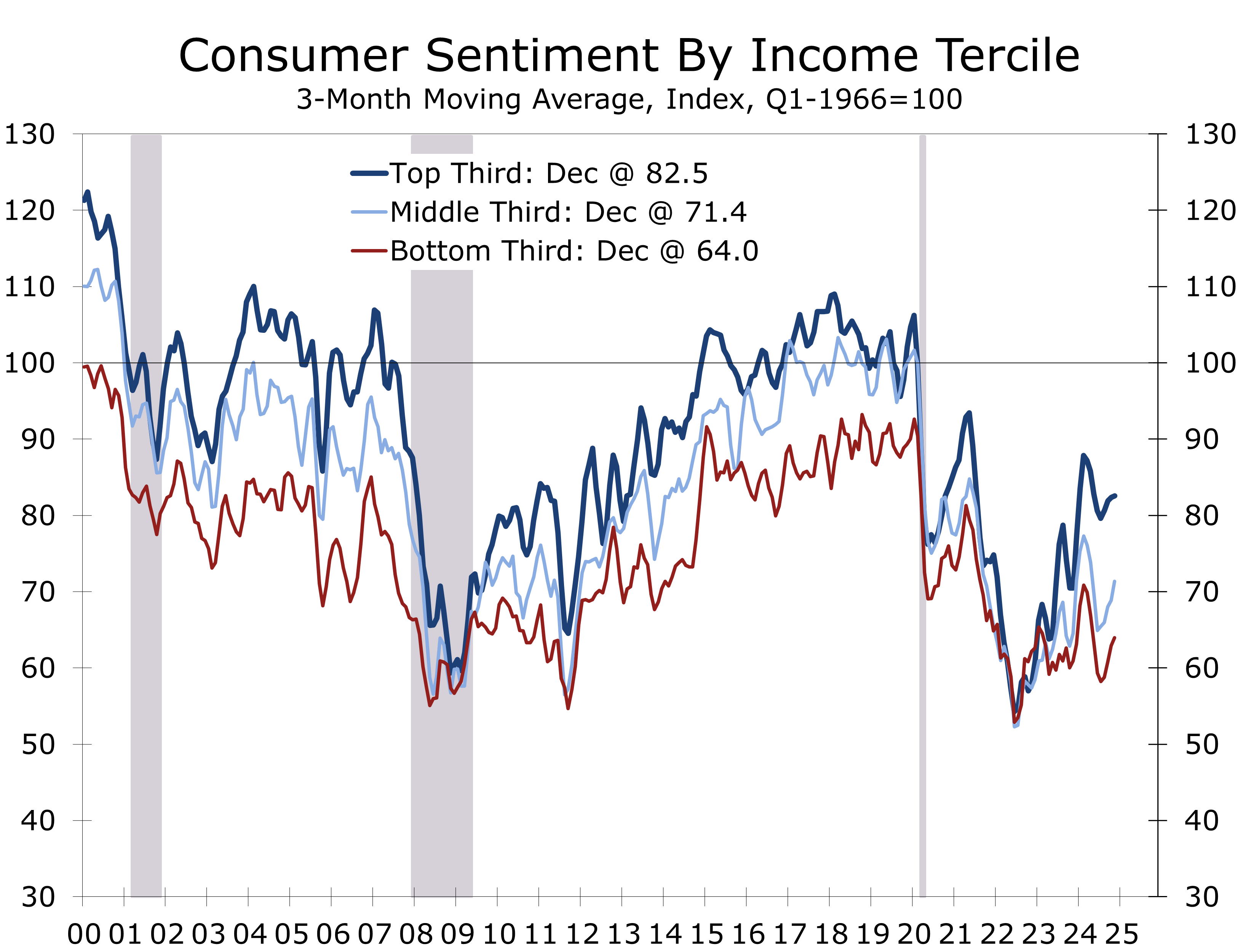

Consumer sentiment has continued to deteriorate in early February, reflecting increasing policy uncertainty. With excess savings largely exhausted, current spending relies more on employment and income growth. Elevated grocery prices and rising insurance costs are likely significant contributors to the decline in sentiment. Consumers’ assessment of current conditions has dropped 6.4 points since December to 68.7, while expectations for future economic conditions—which have a closer link to actual spending—have fallen by 6.0 points to 67.3.

The University of Michigan’s consumer sentiment survey highlights particular weakness among lower-income households. Sentiment for the lowest income tercile has decreased to 64, matching the levels seen during the depths of the Global Financial Crisis. Middle-income households are only slightly more optimistic, with sentiment at 71.3. These figures suggest that economic uncertainty and rising costs are disproportionately affecting consumers with tighter budgets, posing a potential obstacle to discretionary spending.

Despite these concerns, underlying fundamentals support consumer spending in 2025. The unemployment rate remains low at 4%, and weekly jobless claims are near historic lows. Wage growth is robust, and household balance sheets—along with slightly lower interest rates compared to a year ago—should provide some support. Low-rate financing incentives are expected to sustain light vehicle sales and big-ticket spending.

However, financial strength is not evenly distributed across income groups. Rising costs for necessities are disproportionately impacting lower- and middle-income households, putting pressure on discretionary spending. Given these dynamics, we have slightly reduced our estimate for Q1 consumer spending and continue to anticipate a below-consensus gain of just under a 2% annual rate.

An old axiom in economic analysis advises distinguishing between what you think the Fed will do and what you think it should do. In today’s hyperpolarized political climate, this principle is just as relevant when assessing the Trump administration. It is more constructive to focus on what the administration will do rather than what one believes it should do. Another key rule to apply—take Trump seriously, but not literally—meaning the most hyperbolic rhetoric from both Trump and his opposition should be ignored or at least downplayed.

The administration’s priorities include strengthening border security, deporting undocumented migrants convicted of violent crimes, and using tariffs as a policy tool, revenue enhancement, and a means to leverage U.S. market power. DOGE also aims to reduce government waste to curb the deficit and build credibility for any potential future entitlement reform. In foreign affairs, securing strategic shipping chokepoints such as the Panama Canal and Northwest Passage is a focus, alongside recalibrating NATO to reflect post-Cold War realities. Trump has also expressed a desire to broker lasting peace in the Israel-Hamas and Russia-Ukraine conflicts.

The administration’s agenda is advancing rapidly, catching opponents off guard. Tariffs have been implemented faster and more decisively than expected. While Mexico and Canada secured an extension, comprehensive tariffs are set to take effect on March 4 and are expected to remain in place, along with a 25% tariff on steel and aluminum imports. A primary objective is curbing the transshipment of Chinese steel via Canada and Mexico.

Legal challenges against DOGE are likely to prove fleeting, as the administration has utilized the U.S. Digital Service—an agency created under Obama—to execute its plans. DOGE also remains popular with the public. Total savings from DOGE are likely to fall well short of solving the government’s spending crisis and persistent deficits, although DOGE has already proven more effective at uncovering savings than most previous efforts.

Securing peace between Israel and Hamas remains difficult. The Trump administration has resumed arms shipments to Israel, hoping to pressure Hamas into submission. In contrast, a Russia-Ukraine ceasefire appears more plausible. While Ukraine will not join NATO, an increased European military presence and US economic ties would be relied upon to deter renewed Russian aggression. A ceasefire could ease inflationary pressures in Europe and the U.S. and would support economic growth in Europe.

The weaker-than-expected January employment data, higher-than-expected inflation, and a sharp drop in retail sales align well with our below-consensus call for Q1 GDP growth. We noted last month that the Los Angeles wildfires would weigh more heavily on Q1 growth than early consensus estimates suggested. Recoveries from fires and floods tend to take longer than those from hurricanes or earthquakes, delaying any lift from rebuilding. Given the size of Los Angeles’ economy, the disruption is significant enough to impact national data on employment, income, retail sales and manufacturing.

Beyond natural disasters, the uneven distribution of economic strength remains our key concern. Upper-income households are more insulated from inflation due to rising asset prices, while lower-income, asset-light households face increasing pressure from higher costs of essentials like groceries, housing, and transportation. This divergence is contributing to weaker discretionary spending and broader economic uncertainty.

Technical factors will also restrain Q1 growth. Accounting for housing losses will weigh on consumer spending, while inventory building ahead of potential tariffs will boost imports and temporarily inflate inventory levels. Despite slower Q1 growth, the Fed is unlikely to cut rates with unemployment near 4%. However, inflation should continue to decelerate gradually this year, paving the way for a 25-basis-point cut in late spring or early summer. While we still expect two quarter-point cuts this year. The case for a second cut is now less certain.

Policy uncertainty will also restrain business investment. Concerns over tariffs, the Inflation Reduction Act, and the CHIPS Act will weigh on capital spending in the first half of the year. However, as more clarity emerges on trade, taxes, and deregulation, we expect growth to strengthen in the second half of this year.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice. Any forward-looking statements or forecasts are not guaranteed and are subject to change at any time. Information from external sources have not been verified but are generally considered reliable..

February 18, 2025

Mark Vitner, Chief Economist

Piedmont Crescent Capital

704-458-4000