Real GDP Surges at a 4.9% Annual Rate in Q3

- Real GDP grew at a 4.9% annual rate during the third quarter, with strength evident across the board.

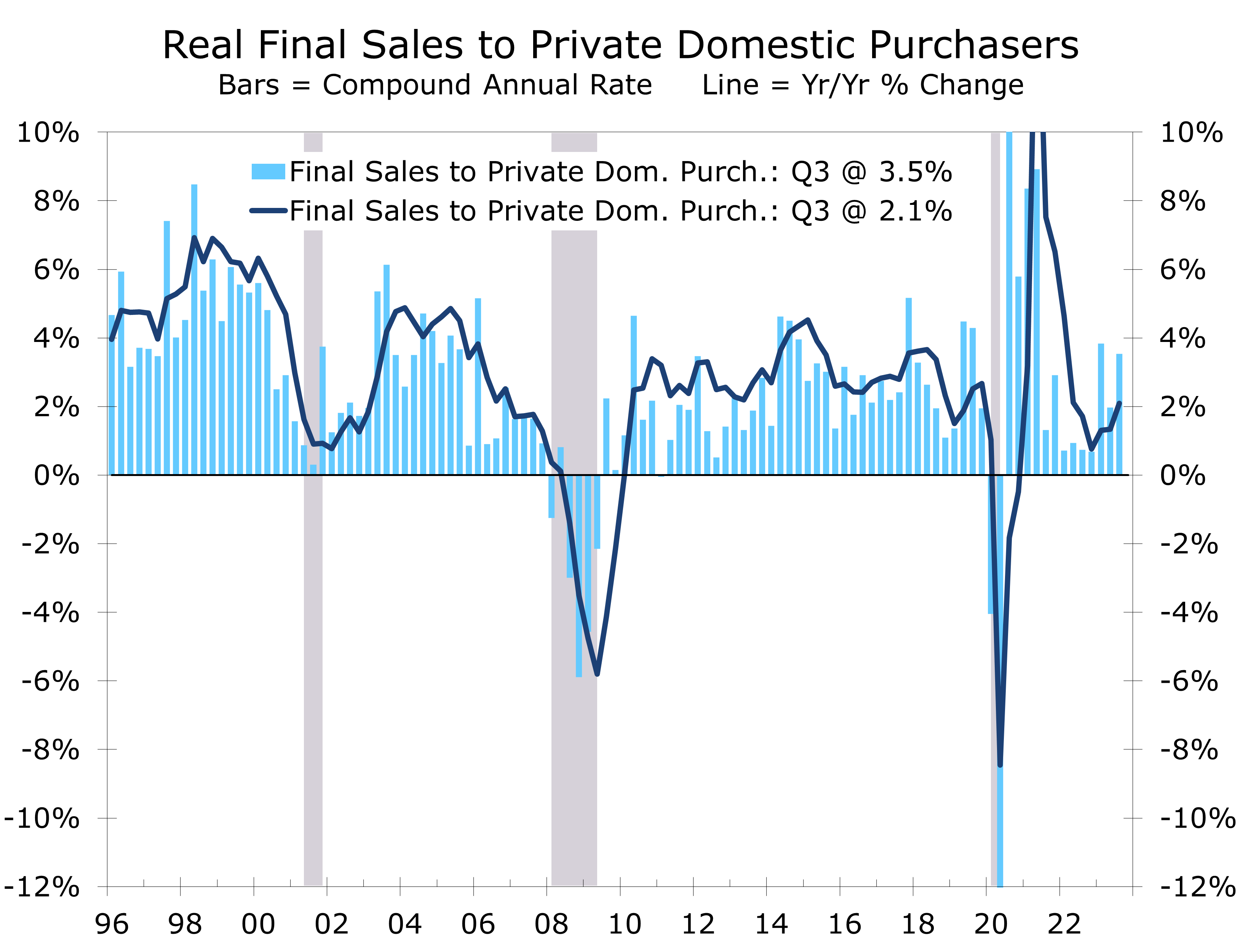

- Consumer spending rose at 4.0% annual rate, with spending up solidly for both goods (+4.0%) and services (+3.6%).

- Business investment in new equipment was a rare soft spot, declining at a 3.8% pace, but outlays for structures (+1.6%) and intellectual property (+2.6%) both increased.

- Residential investment rose at a 3.9% pace, marking its first increase since Q1 2021.

- Inventories added 1.3 points to Q3 growth, partly reflecting efforts by car dealers to build inventories ahead of the UAW strike.

- Government spending rose at a 4.6% annual rate, led by an 8% surge in defense outlays, as well as solid gains in nondefense outlays and state and local government spending.

- There is decidedly less enthusiasm surrounding the robust 4.9% real GDP growth reported for the third quarter. The economy’s remarkable resilience will pull interest rates higher, adding to the building headwinds facing the economy in coming quarters.

Real GDP growth soared at a 4.9% annual rate during the third quarter, marking the strongest quarterly growth since Q4 2021 when stimulus payments were still in full force. The rise was widely expected, following a string of stronger reports showing consumer spending grew solidly this past summer. Inventory building ahead of the UAW strike and defense spending also added meaningfully to growth.

There is decidedly less enthusiasm surrounding the blowout third quarter GDP report. While strength was evident across the board, the report adds to concerns that the economy’s resilience will pull interest rates even higher and cause rates to remain higher for a longer. Higher interest rates will add to the growing litany of concerns ranging from the resumption of student loan payments, tightening financial conditions, fights over persistent budget deficits, and ongoing wars in Europe and the Middle East.

While Q3 growth slightly topped consensus estimates, it hardly came as a surprise. Consumer spending was incredibly strong this past summer, driven by outlays for experiences like concerts and travel. Spending for services grew at a 3.6% annual rate, the strongest since the 2021 pandemic recovery.

Spending for goods also rose solidly, with spending for durable goods jumping at a 7.6% pace and spending for nondurables climbing at a 3.3% pace. The spending spree largely came out of savings, however, as real after-tax income declined at a 1.0% annual rate in Q3 and saving rate fell from 5.2% to 3.8%.

The strength in consumer spending likely carried into the current quarter, as evidenced by strong ‘core’ retail sales in September. We expect consumer spending to rise at a more modest 2.5% pace in Q4, which should be enough to ensure solid overall growth for the quarter. While concerns about the toll the resumption of student loan payments, slowing income growth and tightening credit conditions are valid, the impact will not be immediate and become more evident next year.

Home building made a positive contribution to third quarter growth, with residential investment climbing at a 3.9% annual rate. The gains is the first rise since the first quarter of 2021 and likely reflects efforts by home builders to speed up deliveries of homes under construction to take advantage of the shortage of existing homes for sale.

Rising interest rates and tightening credit are taking a toll on business fixed investment.

Business fixed investment slowed sharply during the third quarter. Spending for new equipment declined at a 3.8% annual rate and reflects a broader slowdown in goods production as well as the impact on rising interest rates and tightening credit conditions on small businesses. Outlays for nonresidential structures continue to increase, climbing at a 1.6% pace, which is well off the pace of recent quarters.

Spending for nonresidential structures has benefitted from the incredibly generous benefits provided by the CHIPS & Science Act and Inflation Reduction Act, which have significantly boosted construction of semiconductor plants and EV plants, predominantly in Midwest and South.

Government spending rose at a 4.6% annual rate during the third quarter. The rise reflects healthy gains in both defense and nondefense outlays. Defense spending jumped at an 8% annual rate in Q3, reflecting replenishment of supplies provided to Ukraine. Nondefense outlays rose at a 3.9% pace. State and local government spending grew at a 3.7% pace.

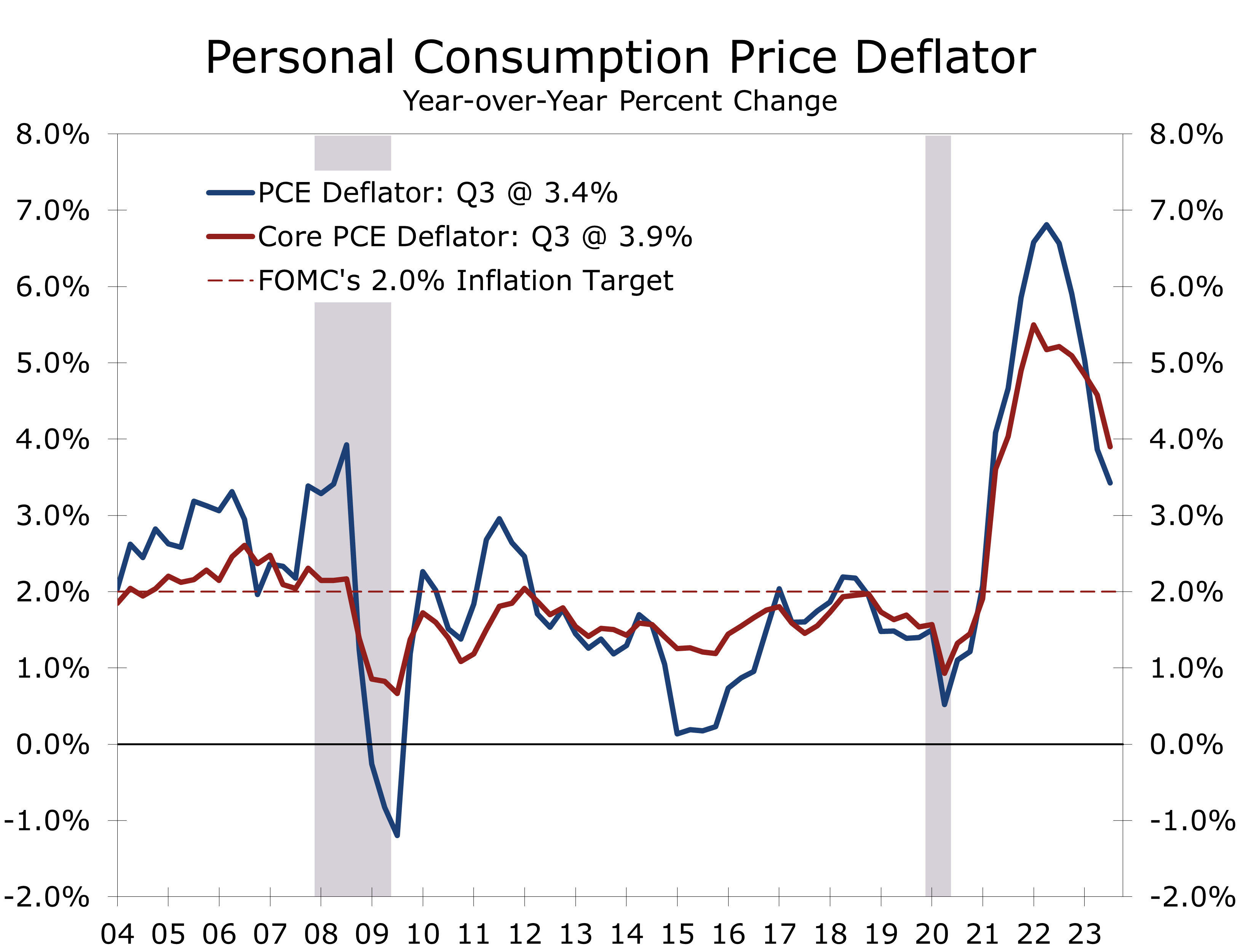

Inflation continues to cool off but remains well above the Fed’s 2% target.

Increased government spending contributed to a larger than expected 3.5% annual rate increase in the GDP Deflator. The more closely watched core PCE deflator was better behaved, however, climbing at just a 2.4% pace and slowing to 3.9% year-to-year. Ongoing wars are expected to drive defense spending higher, posing further challenges for controlling the deficit and bringing inflation back down to the Fed’s 2% target.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.