Private Sector Growth Slows in Q4

- Real GDP grew at a 2.9% annual rate during the fourth quarter, which was toward the top side of market expectations.

- Consumer spending rose at a solid 2% pace, with the strongest gains coming in services.

- Inventory building added 1.5 percentage points to Q4 growth. The trade deficit also shrank, adding 0.6 percentage points to growth. Final domestic demand grew by the remainder, which was 0.8%.

- Government spending grew at a robust 3.7% annual rate. Federal outlays grew at a 6.4% pace, with nondefense outlays surging at a 11.2% pace – reflecting federal stimulus – while defense grew at a 2.4% pace.

- Private final domestic demand – the part of the economy most influenced by monetary policy – slowed to just a 0.2% pace in Q4.

- Outlays for consumer durables, housing, and business investment – the most cyclical parts of the economy – fell at a 2.6% pace.

Real GDP grew at a 2.9% pace in the fourth quarter, which was toward the top end of market expectations. Real GDP grew at 3.2% pace in Q3, after declining slightly in both the first and second quarters of the year. On a year-to-year basis, real GDP rose 1.0%. That meager economic growth was still enough to reduce the unemployment rate by nearly half a percentage point to 3.5%, which raises real questions about the lack of productivity growth and rising labor costs.

The composition of economic growth was not nearly as strong as the headline gain suggests. Real consumer spending rose at respectable 2.1% pace, with outlays for services climbing at a 2.6% pace and spending for goods rising at a 1.1% pace. Services outlays were led by spending for health care, housing and upkeep and other services. Spending for discretionary services, such as personal services, international travel and restaurant dining grew solidly, indicating consumers are still making up for experiences put off during the pandemic. Spending on goods was largely driven by outlays for motor vehicles and maintenance.

Consumer spending came in very close to our 2.0% estimate. Real personal consumption had risen 0.5% in October and was unchanged in November. Data for December will be reported tomorrow and are expected to be weak. Today’s GDP data implies a net decline of around 0.9% for December. The weakness at the end of the year means the current quarter faces a steep uphill climb. We are looking for consumer spending to rise at just a 1% pace in the current quarter and look for real GDP growth to be around a 0.4% pace.

Business fixed investment edged out a 0.7% annualized gain, all of which was in software. Equipment purchases fell sharply, particularly for IT equipment.

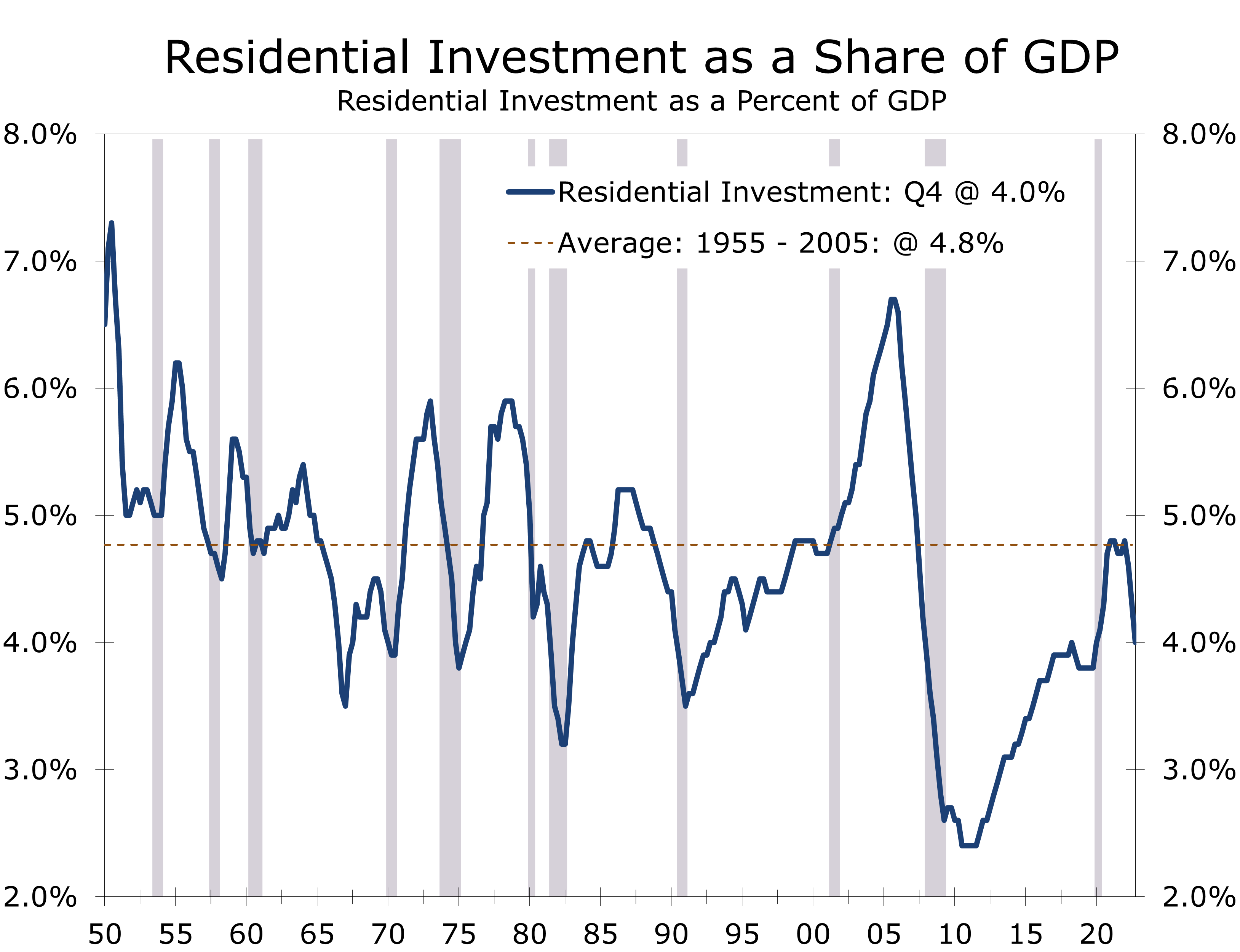

Housing is the clearest area of weakness. Residential investment tumbled at a 26.7% annual rate in the fourth quarter, following a 27.1% decline in the prior quarter and 17.8% annualized drop in Q2. Residential investment has now fallen for seven quarters in a row, which is the longest string of declines since the housing bust. Most of the drop has been in single-family construction, which has seen starts tumble some 29% since peaking two years ago. Home prices are also falling, which is reducing commission income.

The slide in housing is impacting other areas of the economy. Demand for furniture and appliances has slowed in recent quarters, although spending rebounded slightly in Q4. Demand for lumber and other building products has slowed significantly and several mortgage lenders have cut staff, as demand for mortgages has fallen along with home sales.

While the slide in home building is the longest and deepest since the housing bust, there are some important distinctions between the two periods. For starters, housing is not overbuilt like it was back then. While home building took off after the economy reopened, residential investment never climbed back to its long-run average of 4.8% of GDP. Moreover, much of the increase has been in apartment construction. The biggest challenge for the housing market today is affordability.

Inventory building accounted for half of the increase in fourth quarter GDP, and a slowdown in imports accounted for about a quarter of Q4 growth. The two are related. Concerns about a possible shutdown of West Coast ports caused shippers to divert traffic to the East Coast, which clogged up ports and distribution facilities. The surge in inventories added 1.5 percentage points to Q4 growth, but with warehouses filled and containers stacked up at major ports, imports slowed later in the fourth quarter.

The diversion of traffic to East Coast ports has clogged up ports and distribution facilities.

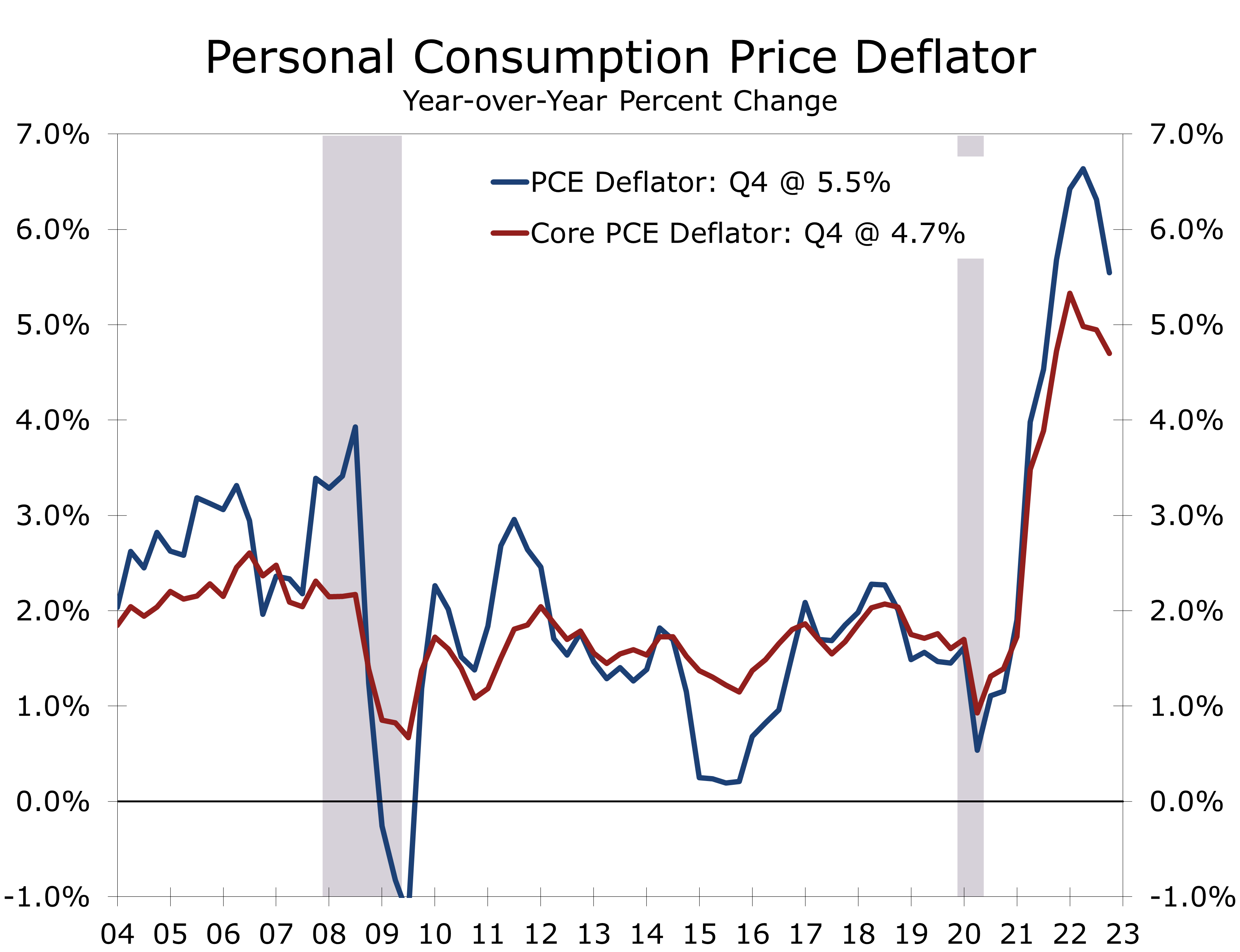

Inflation eased considerably in the fourth quarter. The overall PCE deflator ended the year up 5.5% and the core PCE deflator, which is the Fed’s preferred inflation measure, finished the year up 4.7%. Both numbers came in slightly below expectations and the core PCE deflator slowed to just a 3.9% pace in Q4, which was its slowest pace since the first quarter of 2021.

Stronger Q4 GDP growth gives the Fed the cover they need to boost rates by half a percentage point at next week’s FOMC meeting. The lower inflation data also give credence to those arguing for a smaller rate hike.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.