Retail Sales Suggest Another 3%+ Quarter

- Retail sales rose 0.4% is September, slightly exceeding consensus expectations. The underlying composition was notably strong.

- Sales at motor vehicle dealers were unchanged and are down 0.3% year/year.

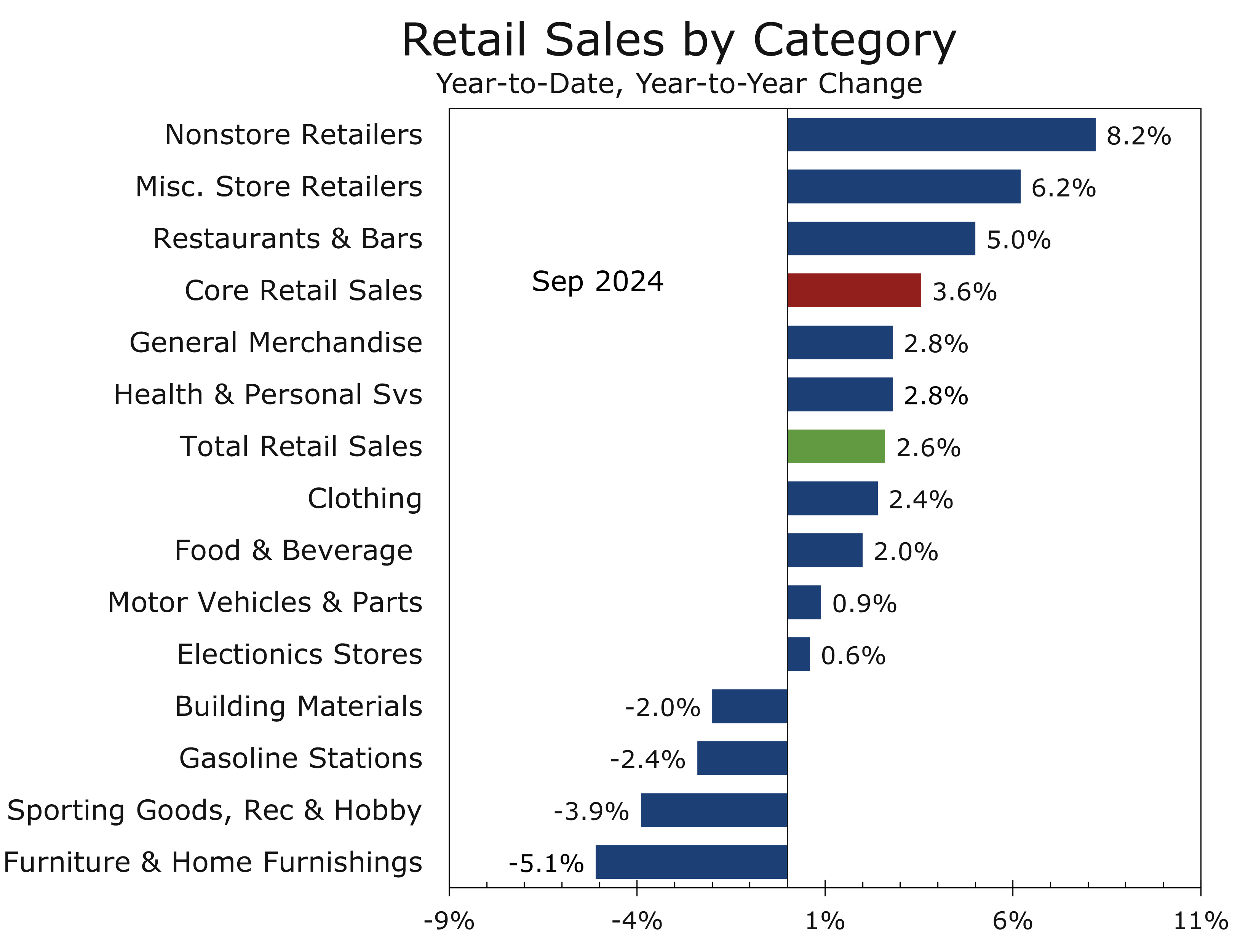

- Excluding autos, retail sales increased by 0.5%, with 11 of the 12 other major business categories posting gains in September.

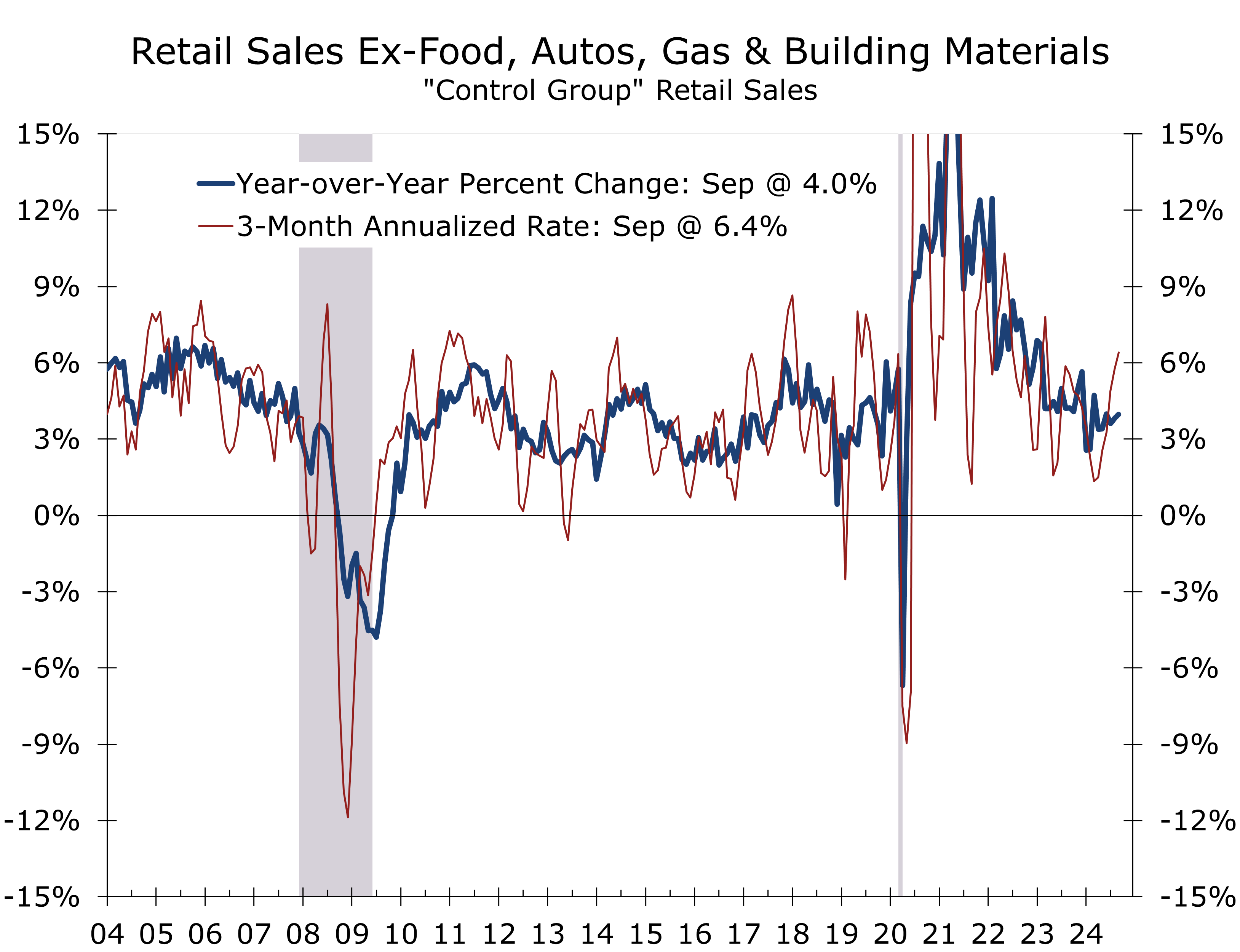

- Core retail sales, which exclude autos, gasoline, and building materials; rose 0.7% and are up 4.0% year-to-year.

- Nominal control group retail sales rose at a 6.4% annual rate in Q3, consistent with real PCE rising at a 3.5% annual rate.

- September’s retail sales reinforce the improved trend implied by the upward revisions to GDP data and national income data. Consumers clearly have the wherewithal to boost spending and keep the economy humming along. The housing market, which continues to suffer from the lock-in effect, continues to weigh on sales furniture, household appliances and building materials.

U.S. retail and food services sales posted a 0.4% rise in September 2024, slightly exceeding the 0.3% consensus forecast. The underlying details are encouraging, implying stronger Q3 GDP growth. Excluding auto dealers, gas stations, building materials, and food services, “core” retail sales rose 0.7%, more than double the anticipated 0.3% gain. This marked the strongest rise in three months, and the prior month’s sales figures were also revised higher, suggesting consumer spending retains substantial momentum.

A key highlight was the strength in control group sales, which surged 0.7%—the largest increase since June. Coming at the end of the quarter, the strength in control group retail sales not only boosts prospects for Q3 but also means that spending has strong momentum headed into the holiday season.

Sales at motor vehicle dealers were unchanged in September and are down 0.3% year-over-year. The slowdown in light vehicle sales reflects the impact of higher short-term interest rates, which have increased the cost of financing. The average monthly payment on a new automobile in September was $740 for a 60-month loan. When factoring in sharply higher insurance costs, new vehicle ownership is simply out of reach for many potential buyers.

Excluding motor vehicles and parts, which includes maintenance and repairs, retail sales rose 0.5%. Sales were held back by a 4.1% plunge in gasoline prices, which drove down sales at gasoline stations. Excluding motor vehicles and gasoline, retail sales rose 0.7%.

Among major categories, the strongest gains were apparent at miscellaneous retail stores (+4.0%), clothing shops (+1.5%), drugstores (+1.1%), department stores (+1.0%) and grocery stores (+1.0%). Some of these gains were price-driven, as clothing and food prices both rose sharply in September. Control group sales, a more consistent measure of spending momentum, rose 0.7% in September and rose at a strong 6.4% annual rate over the past three months.

Consumer spending grew solidly in Q3 and has strong momentum ahead of the holiday season.

The strength in core retail sales increase leaves real consumption growth on track for a 3.3% annualized rate in Q3, up from a 2.8% gain in Q2. Even if control group sales remain flat in October and November, control group sales would rise at a 4.3% pace in Q4.

As it is, we expect so see some pullback in October. The hurricanes will likely take a toll on consumer spending in early October. Strong back-to-school sales, apparent at clothing shops and department stores in September, might also reverse in October. The strength in back-to-school sales, however, has typically been a good predictor of holiday retail sales. The National Retail Federation recently published their forecast for a 2.5% to 3.5% rise in holiday sales this year. We put the increase at closer to 3.5% to 4%.

With existing home sales hovering near the lows reached during the global financial crisis, sales of furniture, appliances, and building materials remain under pressure. Unlike the financial crisis, today’s home sales are constrained by limited supply. Homeowners who locked in mortgage rates at 5% or lower are reluctant to part with their low-rate mortgages and are staying put.

Sluggish home sales continue to weigh on housing-related outlays, including furniture.

The Fed’s September rate cuts have provided limited near-term relief. While financing costs for furniture, appliances, and home improvements have eased slightly, existing home sales remain the key driver for sales of these items. With bond yields and mortgage rates now back above their pre-September FOMC meeting levels, we do not expect significant relief before spring.

While furniture store sales fell 1.4% in September, they have shown some improvement in recent months, rebounding at a 5.8% annual rate over the past three months. Year-to-date, sales are down 5.1% compared to last year, leading to numerous store closures.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

October 17, 2024

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000