Sticking with Our Touch and Go Scenario: A Stronger but Uneven Expansion

- Growth Surprises to the Upside: The U.S. economy is tracking 2.6% Q3 GDP growth, well above midyear expectations, confirming a rebound after a slowdown following the rollout of tariffs.

- Survey Signals Lower Recession Odds: CNBC’s September Fed Survey places the probability of recession over the next 12 months at 40%, up from 31% before the July 31 FOMC meeting but broadly in line with the prior four meetings. We put recession odds closer to 30%, reflecting recent soft employment data but resilient consumer spending.

- Consumers Driving Q3: Retail sales in July and August were stronger than expected, but spending is being driven predominantly by higher-income households while lower-income segments show rising financial stress.

- AI and Aerospace Lead Investment: Massive AI infrastructure buildouts and a surge in aerospace and defense spending are offsetting weakness in other sectors and driving productivity gains.

- Housing Remains Weak: Housing starts fell in August, and inventories of new homes are at their highest since 2009, delaying a sector recovery until mid-2026.

- Inflation Progress, but Tariffs Complicate: Core CPI rose 0.3% in August as tariffs pushed up goods prices, while services inflation remains well-behaved and expectations stay anchored.

- Messaging Matters: The Fed has to get its messaging right and may be able to accomplish more by doing less. Long-term yields are more likely to remain contained if the Fed avoids appearing politically driven while keeping expectations measured. Post-FOMC speakers largely share this view.

- Geopolitical Flashpoints Rising: Conflicts in Gaza and Ukraine, European recognition of Palestine, and sharper U.S. pressure on allies highlight rising risks to global stability.

Outlook: Growth Holding, Recession Risks Persist

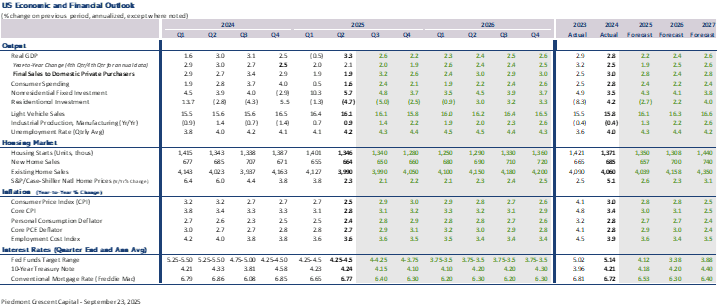

The U.S. economy continues to outperform expectations, defying the cautious outlooks that dominated the summer. The Atlanta Fed’s GDPNow model currently tracks 3.9% for Q3—a sharp improvement from earlier forecasts near 2% and well above private estimates that initially carried a “1-handle.” Our own forecast is more measured, with Q3 at 2.6% and Q4 at 2.2%. For 2025, we project 1.9% growth, fourth quarter-to-fourth quarter, rising to 2.5% in 2026 as interest rates ease and fiscal tailwinds take hold.

The CNBC Fed Survey is more cautious, pegging Q3 at 1.9% and Q4 at 1.4%, with full-year growth of 1.5% in 2025 (Q4/Q4) and 2.0% in 2026. Many of those forecasts were submitted before the stronger mid-September retail sales report for August, which lifted near-term consumption estimates. The divergence between official trackers, survey consensus, and our own forecast highlights just how fluid this expansion remains.

Underlying data confirm the uneven nature of growth. Consumer spending and business investment are carrying the economy, but the breadth of hiring is narrowing, and housing remains stuck in neutral. That mix has allowed GDP to look healthy even as cracks appear below the surface. Strong productivity gains linked to AI and aerospace are buying time, but they are not yet broad enough to ensure a durable cycle on their own.

We have said repeatedly that if the economy could avoid slipping into recession through the summer and early fall, it would likely be fine. That outlook remains intact. The near-term risk of a downturn has diminished as growth has accelerated, but the recovery is still fragile. The economy has momentum, but it remains vulnerable to policy mistakes, external shocks, and the risk that tariff-related price pressures linger longer than expected.

This dynamic fits our “Touch and Go” framework outlined in earlier reports. The economy slowed sharply earlier this year, briefly touched down, and is now climbing again. The question is whether it can gain enough lift to reach cruising altitude or whether turbulence forces another pass. The uneven distribution of strength across sectors makes this one of the most complex expansions in recent memory.

Recession risks are diminished but not extinguished. Policy should focus on broadening the recovery—through labor-market participation, housing affordability, and infrastructure channels—rather than assuming resilience in a few sectors will carry the cycle indefinitely.

Consumers: Resilience Amid Uneven Labor Markets

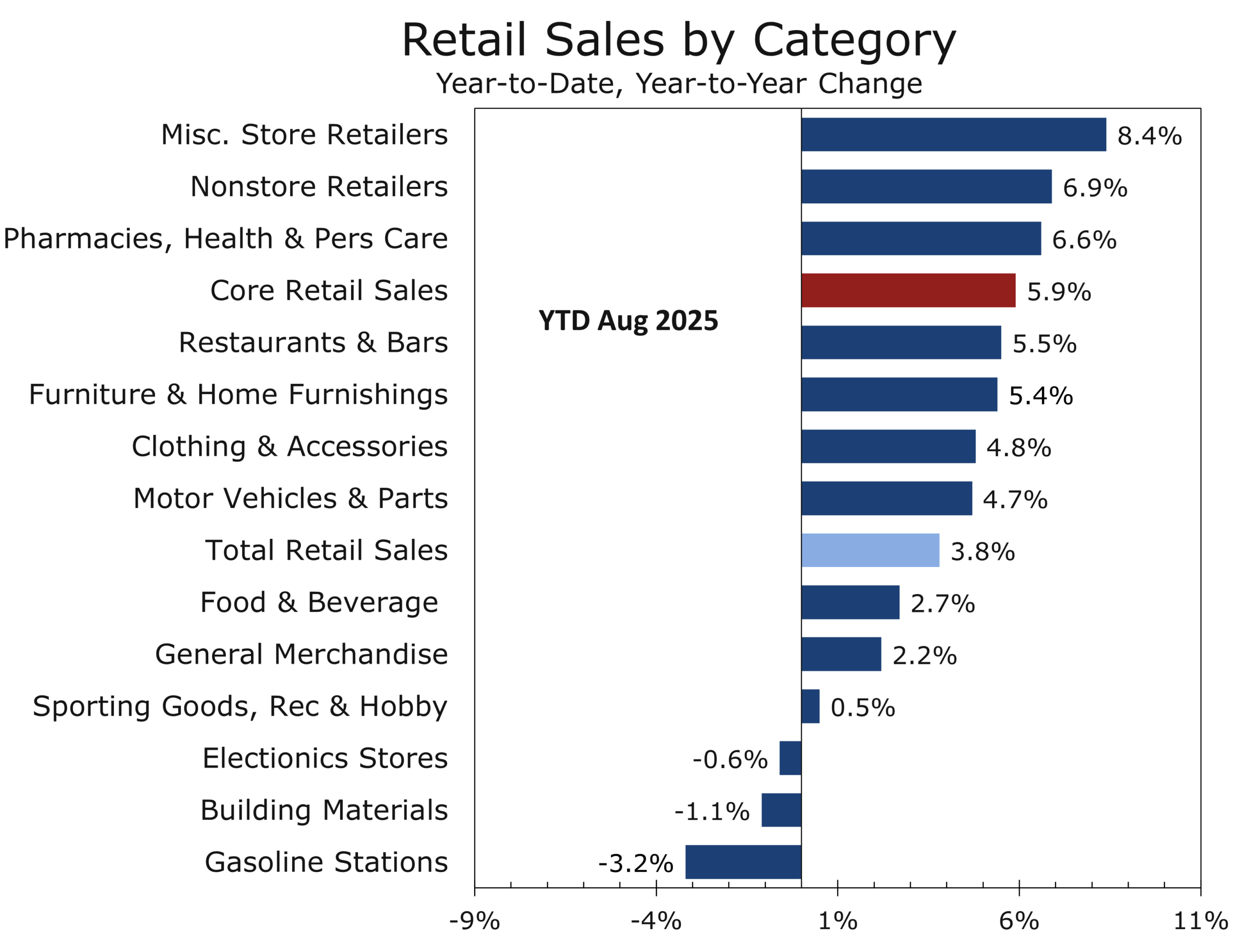

Consumer spending remains the backbone of the rebound. August retail sales rose 0.6%, while July was revised up to 0.5%, following June’s 0.9% jump. Gains were broad-based: non-store retailers +2.0%, clothing +1.0% (a strong back-to-school season), and food services +0.7%. We estimate real core retail sales rose 0.5% in August and are running at a 5.5% three-month annualized pace, placing Q3 consumption growth well north of 2% annualized and providing upside risk to GDP.

The resilience is clearly bifurcated. Higher-income households—roughly one-fifth of the population but responsible for more than two-fifths of spending—continue to fuel discretionary categories such as dining, travel, recreation, and e-commerce. Their balance sheets remain healthy, supported by wealth gains from equities and home values. In contrast, middle- and lower-income households are increasingly pressured by higher borrowing costs, tariff-driven price increases, and a softening labor market. Rising auto and credit-card delinquencies are early warning signs that stress is mounting.

The labor market’s narrowing breadth amplifies the divide. The employment diffusion index has slipped below 50, showing that job gains are concentrated in just a handful of sectors—health care, aerospace, and leisure/hospitality—while hiring in many other industries has stalled. Real disposable income growth is slowing as wage gains moderate and pandemic-era savings are nearly depleted. Sentiment surveys capture the fragility, with households citing tariffs, borrowing costs, and job security as top concerns.

While consumer spending will keep Q3 GDP afloat, the expansion is becoming increasingly top-heavy. Deferred purchases and pent-up demand are still providing a lift, but without broader labor-market gains and relief for financially stretched households, aggregate demand risks losing momentum heading into 2026—underscoring why the Fed has placed greater emphasis on supporting the labor market.

Business Investment: AI and Aerospace Take the Lead

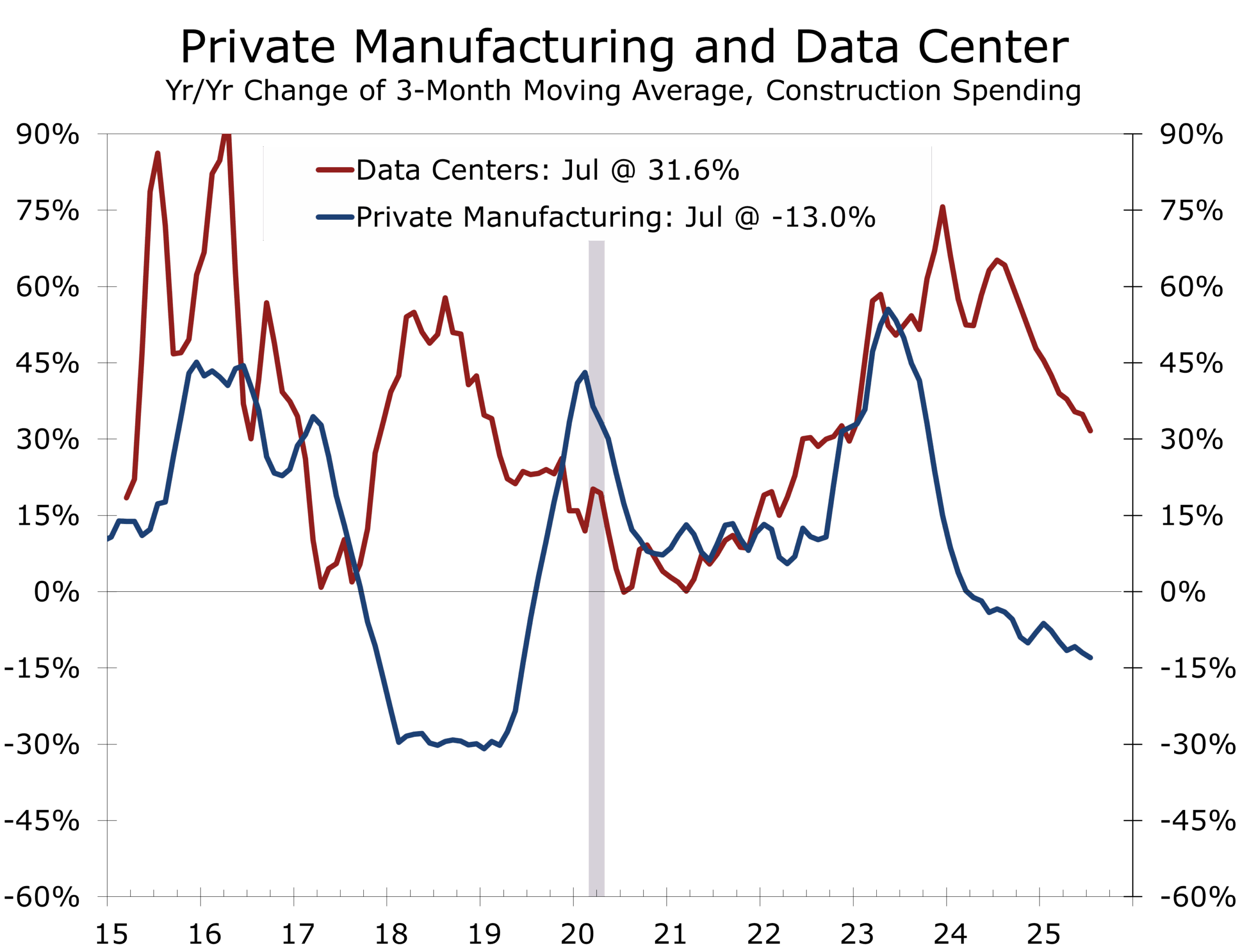

The defining story of this cycle is the rise of artificial intelligence infrastructure and aerospace/defense as the dominant engines of business investment. Data-center construction is expanding at a record pace, with spending up more than 30% y/y and accelerating. Corporate outlays on high-tech equipment—servers, GPUs, and networking systems—are surging, with some subcategories growing more than 40% y/y. AI-related spending could exceed $350 billion in 2025, directly adding around 0.5 percentage point to GDP growth and potentially closer to a full point in 2026 as adoption broadens. More importantly, these investments are reviving productivity, the foundation for long-run growth.

The impact is not confined to Silicon Valley. Mega-projects are reshaping regional economies from Northern Virginia’s data-center corridor to new builds in Texas, Arizona, and across the Southeast, driving demand for skilled labor, energy infrastructure, and industrial construction. These localized booms are creating new growth corridors and reinforcing America’s competitive edge in emerging technologies.

Aerospace has re-emerged as the second growth pillar. Commercial aviation is supported by record backlogs at Boeing and Airbus, while defense budgets are lifting demand for advanced fighter jets, drones, and space-based systems. Aerospace exports are cushioning the drag from weaker auto sales and softer consumer-goods manufacturing, keeping industrial output on firmer footing.

Together, AI and aerospace have kept nonresidential investment positive even as office construction, energy exploration, and other manufacturing activity weaken, following a tax-incentive and stimulus driven surge. These sectors are acting as stabilizers, preventing the economy from losing altitude and giving policymakers a wider margin of safety.

Investment strength is effectively raising the economy’s speed limit—but execution will matter. Permitting, power generation, and transmission capacity will need to expand alongside workforce pipelines to translate record capex into durable productivity gains. Without this support, investment could lose momentum as bottlenecks mount.

Housing: A Sector Stuck on the Ground

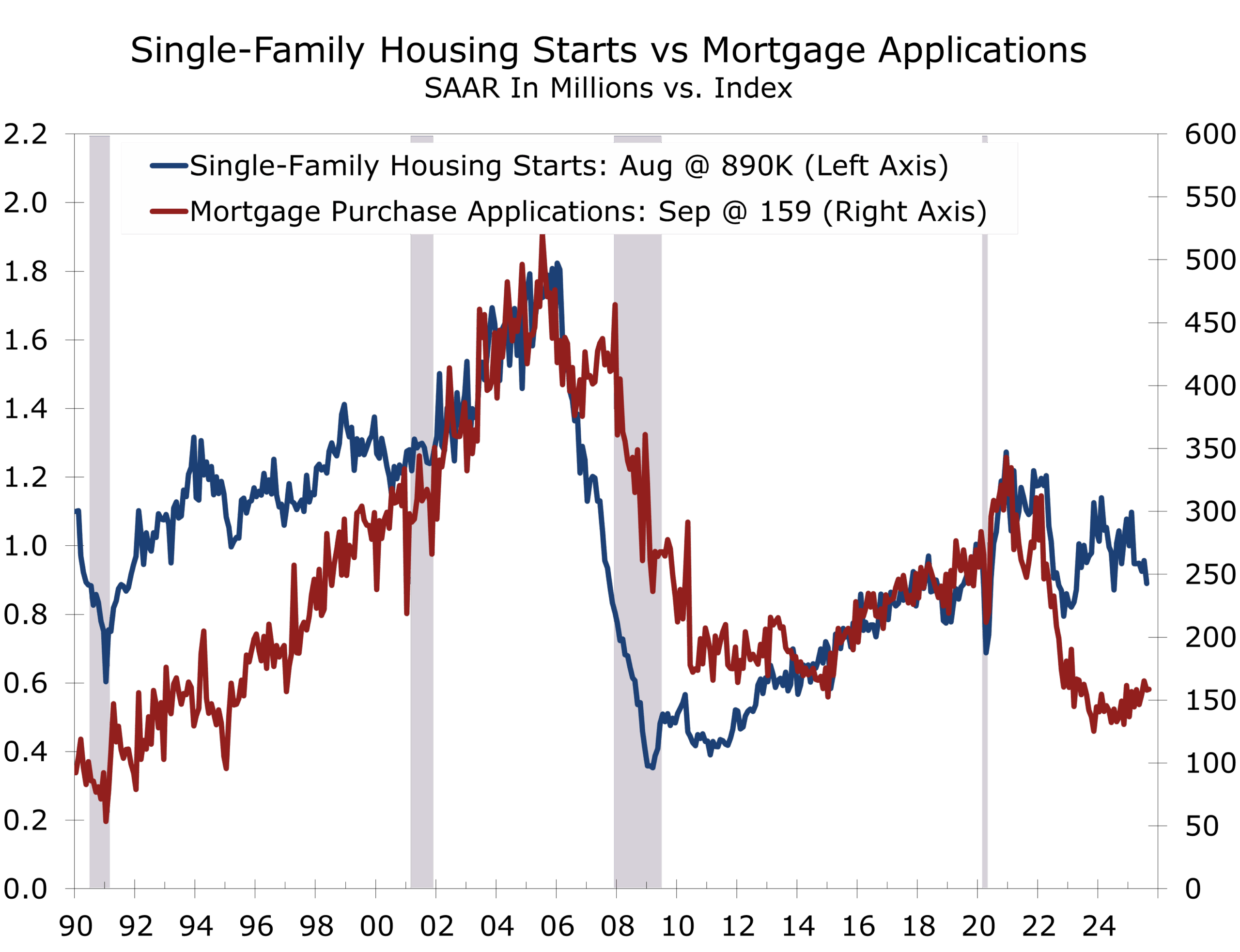

Housing remains the weakest sector of the economy, weighed down by both structural and cyclical headwinds. After a brief rebound in July, August housing starts fell 8.5% and permits dropped 3.7%, leaving them more than 11% below year-ago levels. Inventories of new homes have risen to a 9.3-month supply, the highest since 2009, prompting builders to slow starts and focus on clearing speculative units already on the market. Discounts and incentives are increasingly being used to move this excess stock, particularly in the South and West where building had been most aggressive.

The two biggest impediments to a healthier housing recovery are clear. First, a lack of affordable product continues to lock out entry-level buyers. Elevated home prices, combined with higher insurance costs and property taxes, leave few options for households trying to buy at the lower end of the market. Second, slowing job growth has reduced relocations, traditionally a major driver of home sales and construction in fast-growing regions. The cooling labor market has blunted one of housing’s most reliable sources of demand.

Meanwhile, the inventory of existing homes remains historically tight, as many owners are reluctant to sell and give up sub-4% mortgages. This limits buyer choice in the resale market and keeps pricing pressure elevated even as demand has softened.

Taken together, these dynamics leave housing unlikely to contribute meaningfully to GDP growth before mid-2026. At best, the sector may move from drag to neutral in 2025 as builders finish working through their backlog of spec homes and inventories gradually normalize. Mortgage applications have picked up as conventional mortgage rates briefly fell back to 6%, which should lift new home sales this fall. Inventories will have to fall back to historic norms before construction ramps up again, which is unlikely until spring or summer 2026.

Inflation: Tariffs Complicate the Descent

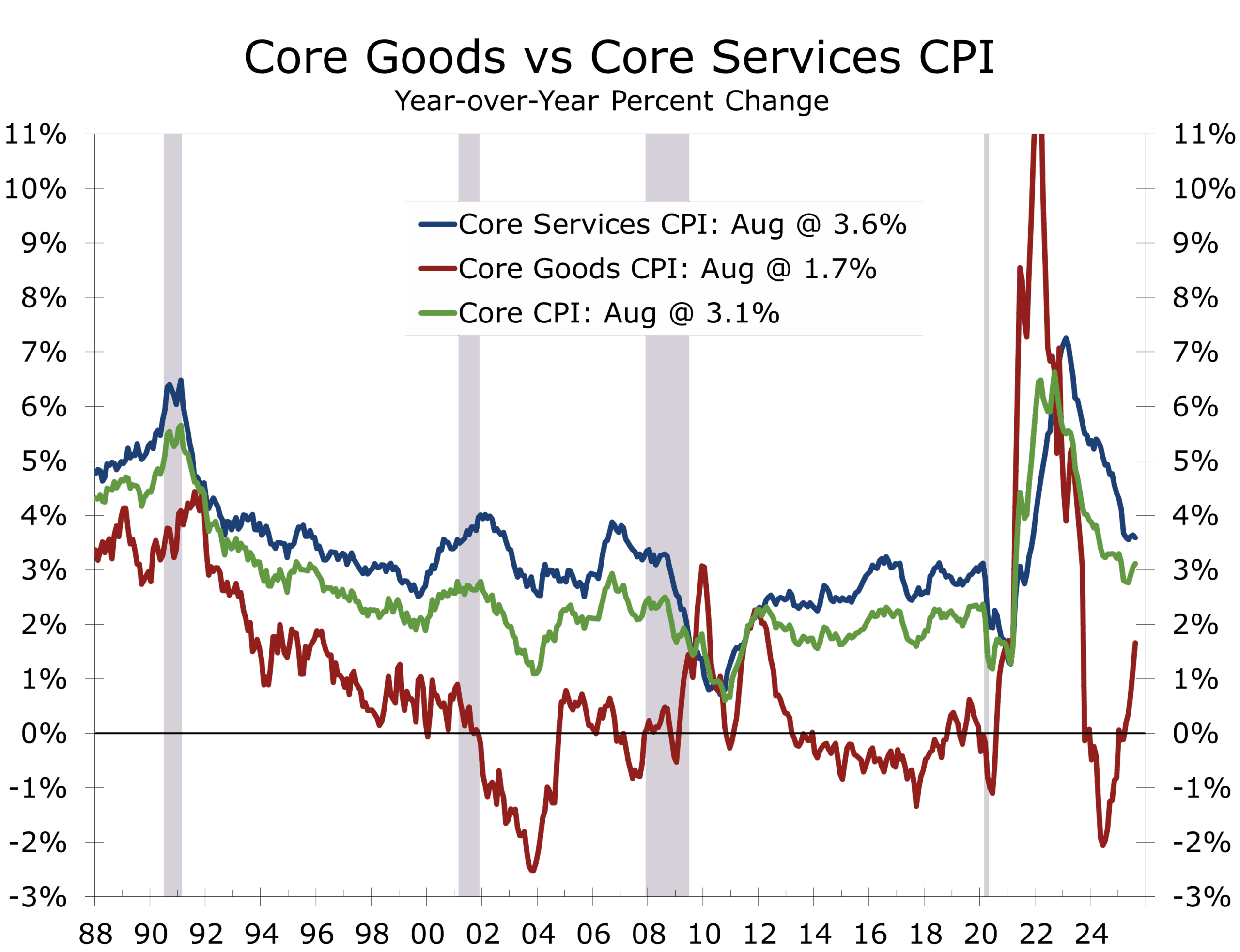

The disinflation trend has slowed but has not reversed. Headline CPI rose 0.4% in August (2.9% y/y), while core CPI increased 0.3% (3.1% y/y). Goods inflation, which had been easing for much of the past year, has re-firmed as tariff-related costs work their way through supply chains. By contrast, services inflation has leveled off near 3.6%, still above the Fed’s target but no longer accelerating. Market-based expectations remain stable, with the five-year/five-year forward inflation swap at 2.4%, broadly consistent with the Fed’s long-run objective.

Tariffs remain the wild card. Participants in the CNBC pre-FOMC Survey generally expect tariffs to generate “somewhat more” price pressure but not a broad-based spiral. This aligns with the Fed’s stance of looking through tariff-driven goods inflation while focusing on underlying trends in rents, wages, and services. Powell and other policymakers have made clear they will not react to every tariff-induced bump but will monitor whether these pressures risk becoming embedded.

The greatest risk is persistence. If tariffs remain in place long enough to alter corporate price-setting behavior—or if firms use them as cover to widen margins—the final leg of disinflation becomes harder to achieve. Already, some categories of durable goods, such as washer machines, are showing firmer prices despite slowing demand. On the other hand, wage growth has cooled, labor demand is narrowing, and shelter inflation is steadily grinding lower as new supply filters into the market. These forces suggest that underlying inflation is still on a gradual downward path.

The Fed has some room to continue easing cautiously, but credibility depends on expectations staying anchored. If households or businesses begin to doubt the Fed’s ability to contain inflation, long-term yields could rise even as policy rates fall. Trade policy will be just as important as monetary policy in the months ahead: avoiding new supply frictions in goods, energy, or labor markets is essential to sustaining disinflation without sacrificing growth.

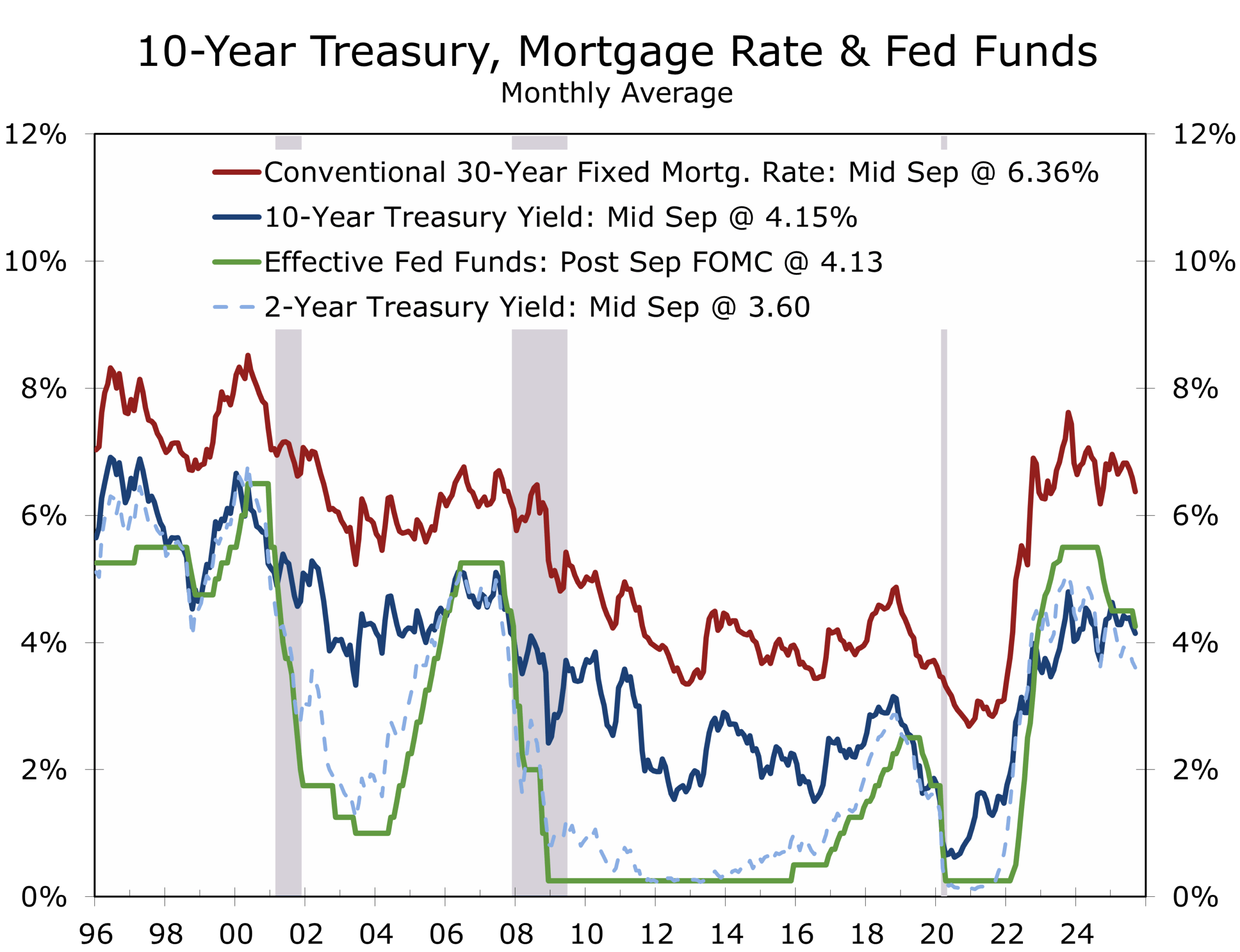

Monetary Policy: Powell’s Risk-Management Pivot

The Fed cut 25 bps in September to 4.00%–4.25%, calling it a “risk-management” step to cushion labor-market risks without reigniting inflation. Chair Powell emphasized that slower hiring reflects narrowing job growth across the economy, not weakness in a single sector. With consumption increasingly dependent on higher-income households, stabilizing employment is now as critical as sustaining disinflation.

Markets expect two more cuts by year-end, with our baseline including a third in January before a pause as growth steadies into spring 2026. The Committee may stretch the cycle—cutting in December, March, and June—but the direction is clear.

Divisions within the FOMC remain. Governor Stephen Miran dissented for a 50 bps cut and reaffirmed his 2025 dot of 2.75%–3.0%, underscoring the doves’ call for faster action. St. Louis Fed President Alberto Musalem supported the September cut but warned against pre-committing, arguing that inflation expectations—not just labor data—should drive decisions. He signaled that two more cuts this year could be excessive without a sharper slowdown. Atlanta Fed President Raphael Bostic reinforced the cautious view, stressing that the Fed must not “overshoot on the downside” and reignite price pressures, calling instead for patience and balance while guarding against political influence.

Much of the easing path is already priced, leaving limited scope for further repricing absent clearer labor-market deterioration. The dollar has remained firm despite political noise, reflecting the U.S.’s relative growth and yield advantage even as policy begins to ease.

The Fed has to get its messaging right and may be able to accomplish more by doing less. Long-term yields are more likely to remain near their current low levels if markets believe policymakers are not bending to political winds at a time when headline inflation is rising. By setting expectations deliberately low—through the dot plot and measured communication—the Fed reduces the risk of disappointment if inflation runs hot or the pace of cuts undershoots market hopes.

A divided FOMC raises communication risk. Consistency and data-dependence will be essential to avoid either re-inflation or a confidence shock that could derail an expansion that remains narrow but resilient.

Geopolitics

Israel’s campaign in Gaza has entered a decisive phase, with ground operations pressing into Gaza City in an effort to deliver a knockout blow to Hamas. The battlefield is shaping the diplomatic terrain: several European governments have recognized a Palestinian state—without borders or functioning institutions—reflecting humanitarian concerns and domestic political calculus. Critics in Jerusalem and Washington view this as rewarding violence while Hamas remains intact.

European leaders are balancing humanitarian aims against the risk of unrest among immigrant and diaspora communities. The recognition strains transatlantic ties but reflects domestic pressures across Europe. The Abraham Accords remain the most promising path to durable normalization and economic integration; symbolic recognitions risk hardening divisions.

In parallel, Ukraine’s refinery strikes have disrupted more than 1 mb/d of Russian capacity, exposing vulnerabilities in Russia’s domestic supply. Moscow’s attritional strategy persists, but sanctions and revenue pressures are eroding fiscal buffers. The prospect for larger disruptions is increasing, which is boosting oil and natural gas prices.

At the UN General Assembly, President Trump’s remarks were sharper than in past years. He criticized European recognitions of Palestine, pressed allies to end purchases of Russian energy, praised Ukraine’s resilience, and warned Moscow of stronger economic measures should aggression persist. He also signaled that NATO must be ready to respond to violations of allied airspace. The message was clear: Washington will lean harder on Europe to align policy, with tariffs and sanctions on the table. He further suggested he is prepared to increase support for Ukraine to retake all territory lost to Russia, “if not more.”

Democrats Can Shut Down the Government, But Not Yet. We see roughly a one-third probability of a partial federal government shutdown before November, with odds rising toward year-end. The sticking point is the $350 billion, 10-year extension of enhanced ACA subsidies. A short shutdown would have little macro impact—a temporary dip in GDP followed by a rebound when furloughed workers return—but a month-plus disruption could rattle markets at elevated valuations. Furloughs would also coincide with a wave of federal retirements this fall, risking some ugly employment prints. Past episodes suggest shutdowns can catalyze volatility in both equity and bond markets, especially amid heightened geopolitical uncertainty.

Rising geopolitical flashpoints and domestic brinkmanship elevate uncertainty for businesses and markets. Policymakers will need to balance security, humanitarian, and fiscal priorities while avoiding moves that worsen supply frictions or financial-condition volatility.

The Outlook: Narrow Strength, Rising Altitude

The third quarter has exceeded expectations, so far, underscoring the economy’s surprising resilience. If momentum carries into early Q4, near-term recession risks should ease further. By 2026, lower rates, modest fiscal support, and AI-driven productivity gains should help broaden the expansion.

For now, growth remains uneven. Consumers—especially at the upper end—along with AI infrastructure and aerospace are providing lift, while housing, manufacturing, and many services remain soft. The labor market remains fragile, with just 22,000 jobs added in August, and gains narrowly based. This mix leaves the economy more shock-sensitive than the headline numbers suggest but also preserves upside as policy support builds. Business confidence has stabilized from earlier lows, but investment outside AI and aerospace remains hesitant, reflecting uncertainty about tariffs, regulation, and global demand. Global developments will also matter: a stronger dollar and tighter financial conditions abroad could restrain exports even as domestic drivers improve.

Resilience has bought time, but durability requires breadth. Policy should focus on bottlenecks in labor, energy transmission, and housing supply to shift the economy from “Touch and Go” to a sustained climb.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

September 25, 2025

Mark Vitner, Chief Economist

704-458-4000