Slower Growth but No Recession, At Least Yet

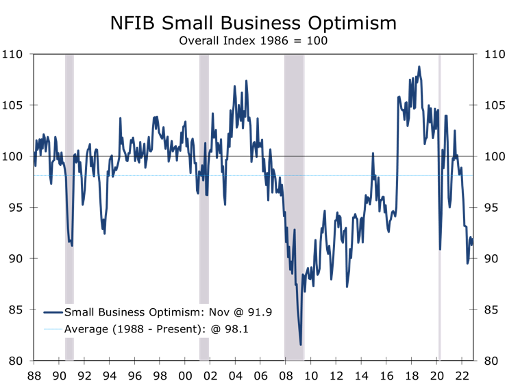

- The Small Business Optimism Index rose 0.6 points to 91.9 in November, as a growing number of business owners noted modest improvement in the business environment.

- Despite November’s slight increase, small business optimism remains below the average for its 49-year history and is also at levels consistent with past recessions.

- Six of the index’s 10 components improved in November, led by earnings, which rose by 8 points. The share of firms expecting real sales to increase also improved.

- Inflation and labor issues rank as the top concerns for businesses, although trends on both now show clear improvement.

- The NFIB report is another data point suggesting it is too soon to give up on the Fed pulling off a soft landing.

Small Business Optimism was one of the first indicators to reflect the impact of the Fed’s abrupt shift in its policy to contain inflation. The Small Business Optimism Index fell sharply as the Fed ramped up the pace of interest rate hikes and has remained below its historic average of 98 all year. While the level of small business optimism remains consistent with a recession, the index has inched higher since the middle of the year.

While we still see a recession as the most likely scenario for 2023, it is not preordained. Many of the hurdles facing business owners appear to have come down slightly over the past few months, most notably supply chain disruptions, which have been reduced significantly. Labor remains in tight supply and there is still considerable upward pressure on wages. Even here, however, there has been some improvement.

The risks to the economy remain stacked to the downside. While it rose 0.6 points in November, Small Business Optimism had tumbled 13.5 points from the June 2021 to June 2022. Declines of this magnitude have nearly always been associated with recessions. The economy clearly slowed during this period, particularly in the first part of this year, with real GDP declining in both the first and second quarters of 2022.

The improved tone of the Small Business Optimism survey continues a recent string of reports hinting a soft landing may still be possible. Consumer sentiment, retail sales and factory orders have all improved in recent months. One key determinant of whether the economy will be able to avoid a recession is whether the labor market cools off enough so the Fed will be able to raise rates less aggressively. Right now, that still looks like a distant prospect, as wages continue to rise at a pace that is inconsistent with inflation returning to the Fed’s long-run target.

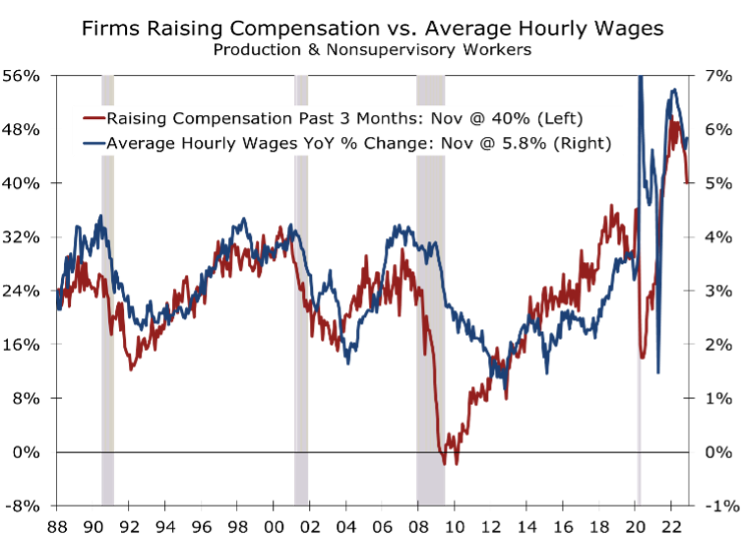

The latest data on average hourly earnings show wages up 5.8% (3-Month Moving Average basis) over the past year. While that is down from a peak of 6.8% in March, the pace is still well above what businesses can offset with productivity gains, leaving inflation well above the Fed’s 2% target.

The link between wages and inflation has become more apparent as the headline inflation data have moderated. Price increases have moderated the most for items tied to energy or supply chain bottlenecks. Prices for services that require a great deal of labor content have cooled off much less. The greater sway rising wages are playing is evident in the small business survey, which still shows an elevated 40% of firms reporting they had raised compensation during the past 3 months, which is down from 44% the prior month and a peak of 50% at the start of this year.

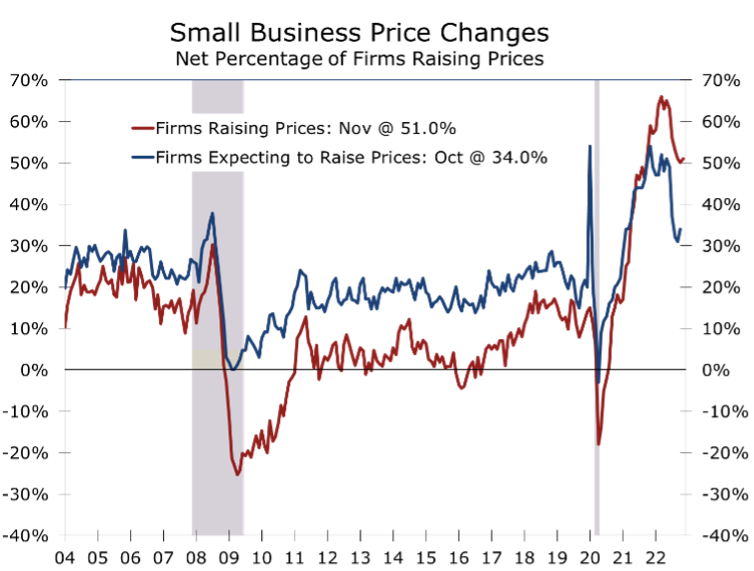

The net share of business owners reporting they raised prices over the past three months rose 1 point to 51% in November. Despite the setback, the share of businesses raising prices appears to have peaked earlier this year, hitting an all-time high of 66% in March. Even with the recent improvement, the share raising prices is still higher than it was in during the high inflation periods of the 1970s and early 1980s.

More than half of all business owners report they raised prices during the past three months.

Price increases are extraordinarily broad based. Price hikes were most prevalent in wholesale trade, with 73% of wholesalers raising prices during the past three months and zero reporting they lowered them. Other sectors where prices are rising broadly include retail trade (69% raising prices against 7% reducing prices), construction (66% raising and 5% reducing), and manufacturing (63% raising and 5% reducing). The prevalence of price gains, particularly in industries where labor costs account for a large proportion of final costs, suggests the Fed will continue to hike rates, albeit by smaller increments, until wage gains have definitively subsided.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.