Capex, Hiring Plans Signal Continued Caution

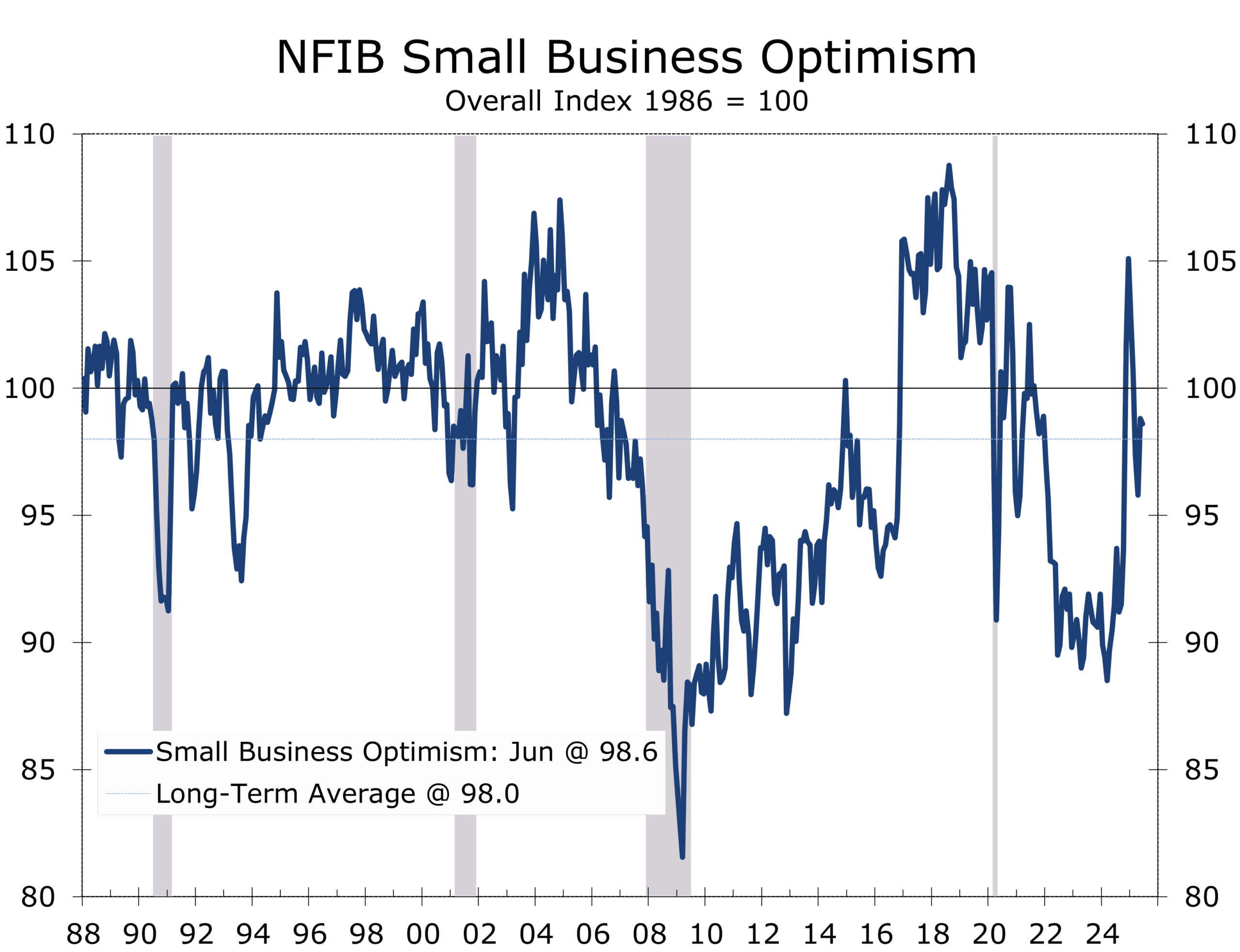

- The NFIB Small Business Optimism Index ticked down 0.2 points to 98.6 in June, still slightly above the 51-year average of 98.

- Inventory satisfaction dropped sharply: the net share viewing inventories as “too low” fell 6 points, dragging the headline index lower.

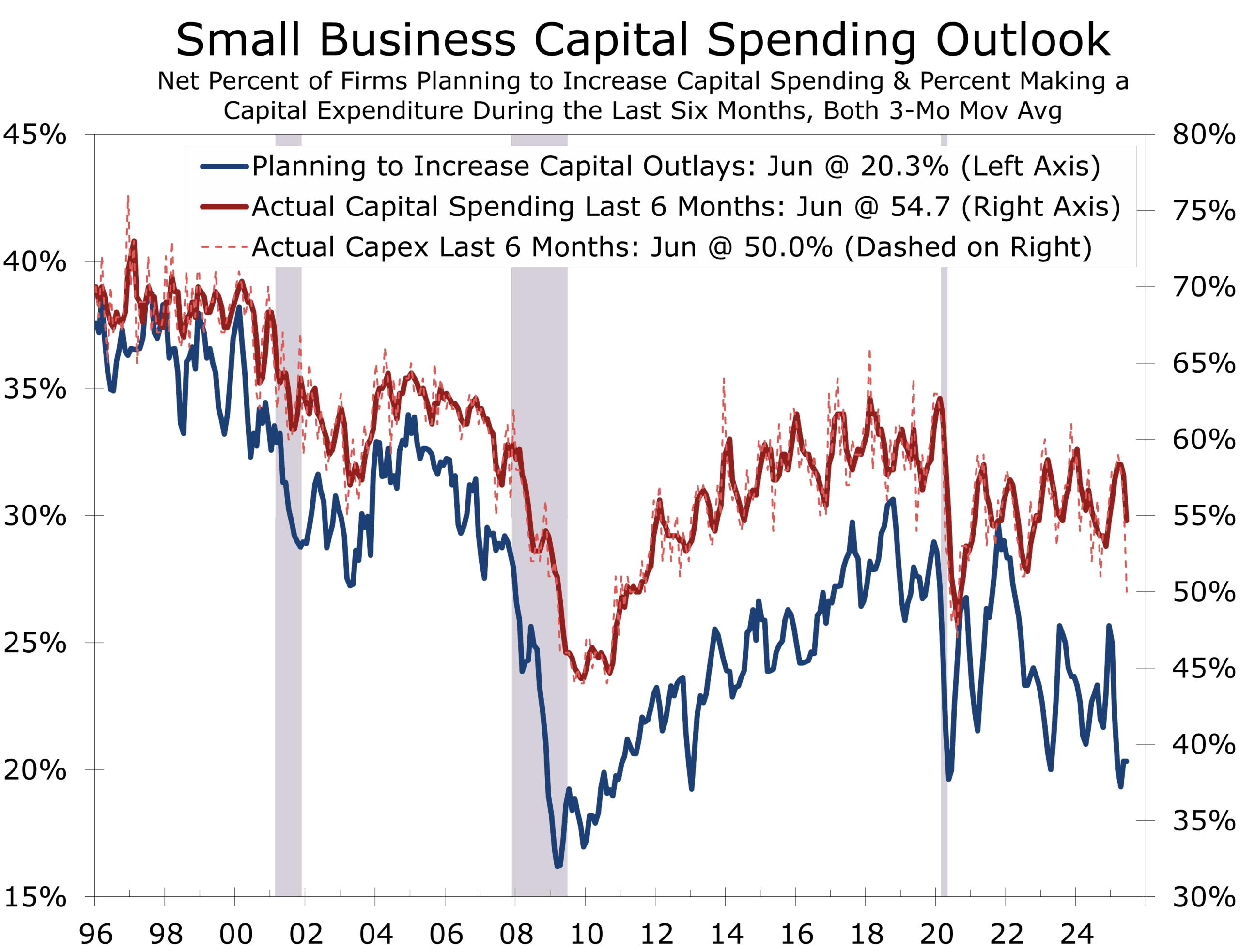

- Capital outlays fell to 50%, the lowest level since August 2020. Equipment and vehicle spending fell by 7 and 8 points, respectively.

- Compensation pressures continue to build: 33% of firms raised wages in June, up from 26% the prior month. That marks the sharpest monthly increase since January 2020 but only brought the measure back to its prior tend.

- Even with fewer firms hiring, finding workers remains difficult. While 58% of firms tried to hire, 36% had positions they couldn’t fill, and net job creation held at a subdued +13%.

- The top concern among small businesses was taxes (19%), followed by labor quality (16%) and inflation (11%). The Uncertainty Index fell 5 points to 89, the lowest of the year. Owners remain eager for more clarity on taxes, trade and interest rates.

Passage of the sweeping Republican tax bill, which was signed into law on the Fourth of July, came too late to boost Small Business Optimism in June. The NFIB Small Business Optimism Index edged down 0.2 points to 98.6 , continuing to hover just above its long-term average of 98. Business owners remain cautious and are wrestling with cost pressures, labor shortages, and shifting trade policy.

June’s modest pullback was driven largely by a sharp deterioration in inventory sentiment, with the share of firms citing current stocks as “too low” declining 6 points to a net –5%. That swing accounted for the bulk of the index’s decline.

Encouragingly, some hard indicators, such as earnings trends and hiring plans, improved modestly. But capital outlays—a key forward-looking measure—fell to a post-pandemic low, underscoring persistent concern about the economic outlook, borrowing costs, and policy ambiguity.

Small business sentiment remained stuck in neutral, ahead of new fiscal tailwinds.

The newly signed tax law—which includes full and immediate expensing of capital equipment—is expected to provide some delayed support in the coming months. But for now, businesses remain hemmed in by higher financing costs, constrained pricing power, and the ongoing uncertainty surrounding tariffs.Top of Form

Capital Spending and Labor Weigh on Outlook

Hiring demand remains firm, but execution is faltering. In June, 36% of firms reported unfilled positions (up 2 points), while 58% attempted to hire. However, 50% of those hiring found few or no qualified applicants. Net hiring plans rose slightly to a still historically weak 13%, highlighting the persistent talent mismatch in construction, manufacturing, and transportation.

Labor market pressure is fueling wage growth. A net 33% of firms increased compensation—up 7 points from May and the largest monthly gain in over four years. Yet only 19% plan further increases, suggesting the compensation surge may be peaking. Labor quality remains a top challenge, particularly for smaller firms facing larger wage offers from bigger competitors.

Despite demand for workers, job creation remains subdued as employers remain selective.

Capital spending fell sharply in June, with just 50% of firms reporting outlays—a 6-point drop from May and the weakest reading since August 2020. Equipment and vehicle purchases saw the largest declines. Only 21% plan to invest in the next six months, reflecting ongoing caution. The pullback came even as the Senate passed a tax bill restoring full expensing—suggesting some firms held back in anticipation of more favorable treatment. The stimulus will be welcome, but the response may be gradual.

Tariff Pressures Continue, but Pass-through is Limited

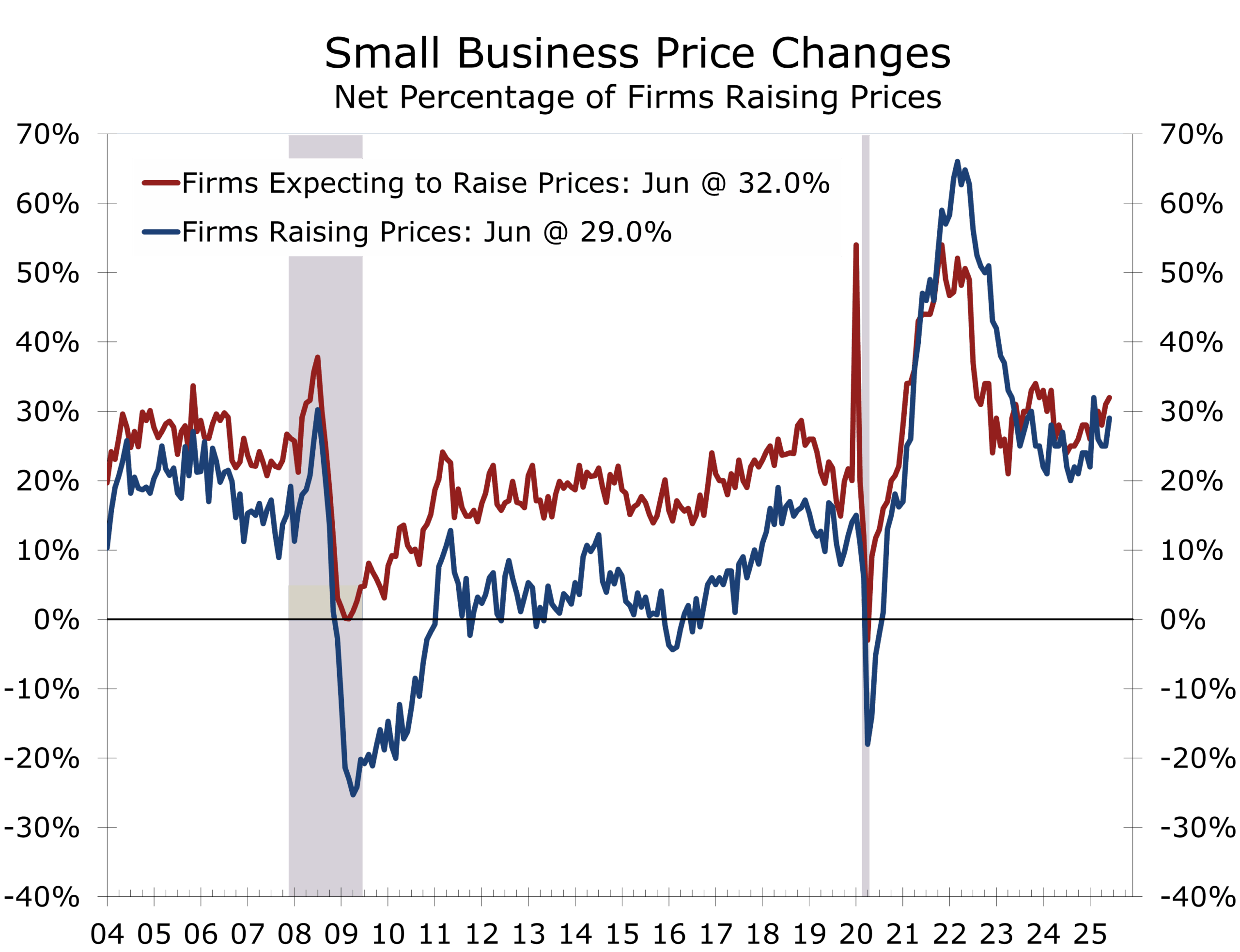

The share of firms raising selling prices rose to a net 29%, and those planning hikes climbed to 32%—the highest in over a year. Yet businesses are reluctant to push too far, wary of weakening sales. In fact, the share of firms citing poor sales as their biggest problem rose to 10%, the highest since March 2021. Real sales expectations slipped to +7%, down from May but still slightly above the long-run average of +3%.

Firms are being squeezed from costs they cannot pass on and higher interest rates.

Credit conditions remain tight. The average short-term interest rate rose to 8.8%, and 9% of firms reported paying a higher rate on their most recent loan. While only 3% cited financing as their top concern, borrowing costs continue to weigh on business expansion.

NFIB’s June survey highlights a growing disconnect between steady headline optimism and mounting operational headwinds. High borrowing costs and soft demand are curbing hiring and investment. While the new tax law may boost sentiment later this year, most owners remain defensive, prioritizing margin preservation over growth. A rate cut may be necessary for the tax stimulus to gain traction.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

July 8, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

704-458-4000