Good Timing for a Lighter Inflation Report

-

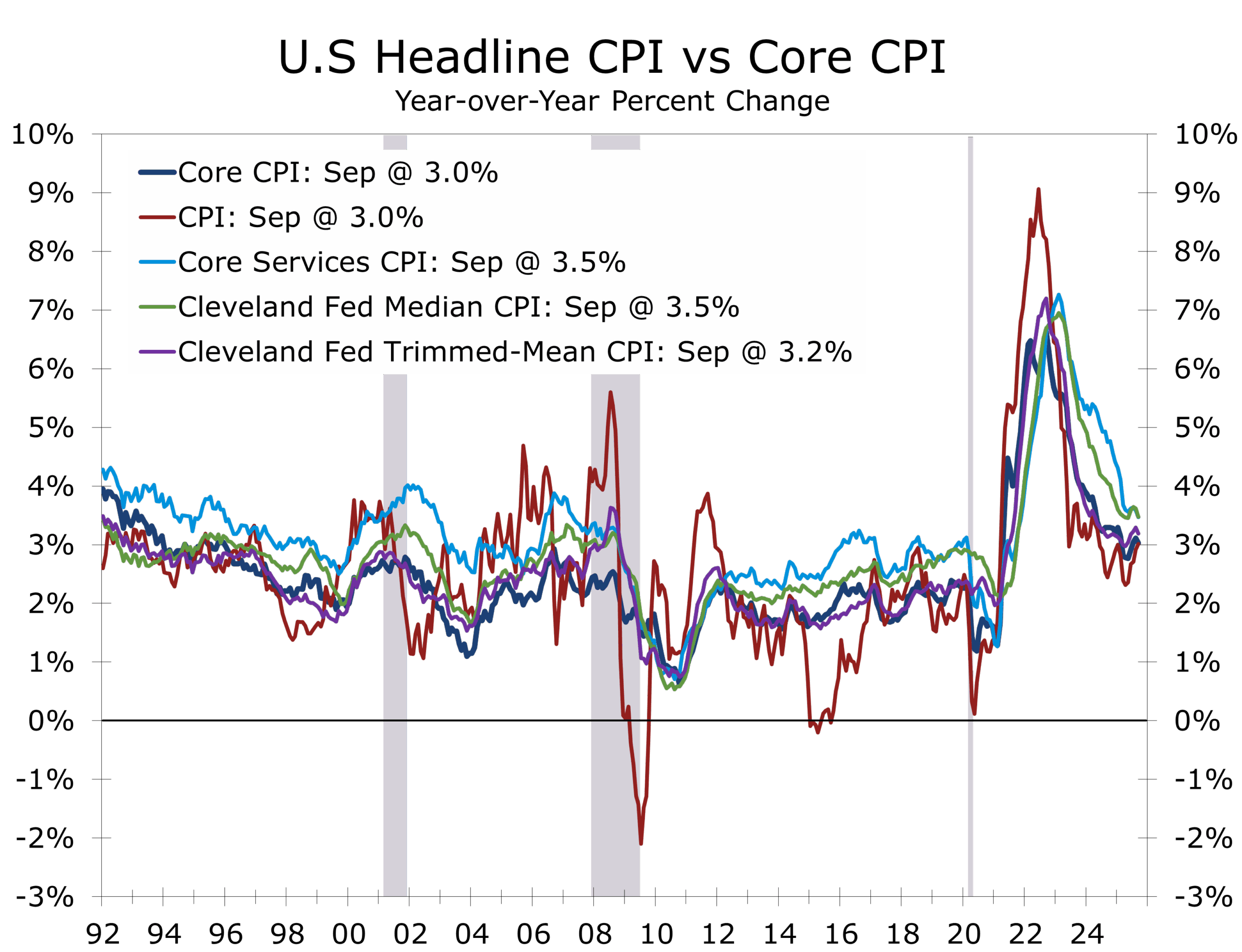

- Headline CPI rose 3% in September (vs. 0.4% in August), while core CPI advanced 0.2%, the smallest increase in three months.

- Year-over-year CPI edged up to 0%, while core CPI held steady at 3.0%.

- Shelter inflation decelerated sharply, with owners’ equivalent rent (OER) up just 1%—the weakest since early 2021.

- Energy prices rose 5%, led by a 4.1% jump in gasoline, accounting for most of the month’s headline increase.

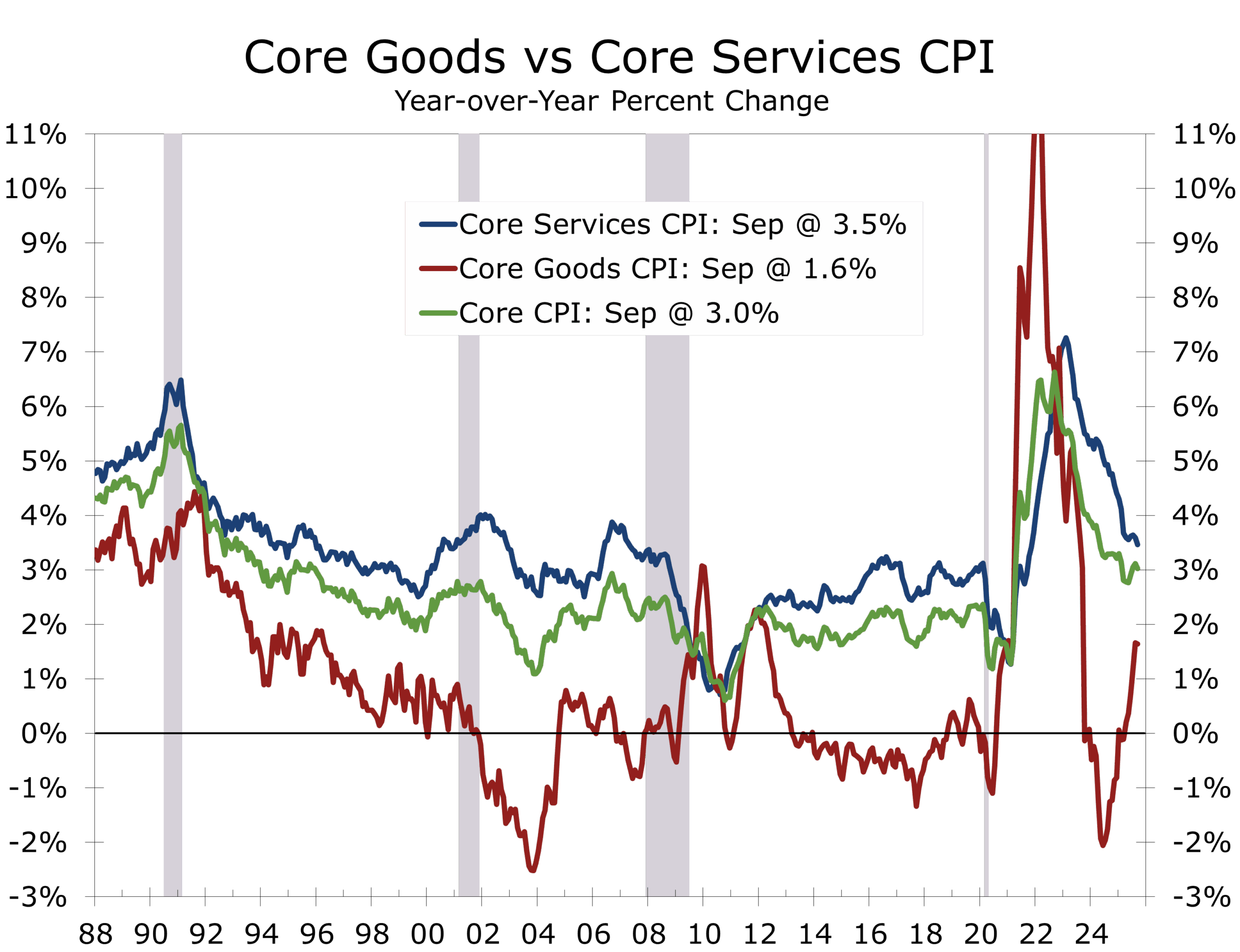

- Core goods rose 2%, with tariff-related gains in apparel, furniture, and personal goods offset by declines in used cars, insurance, and communications.

- Food prices rose 2%, rising 0.3% at grocery stores and 0.1% at restaurants.

- The Cleveland Fed’s Median CPI rose 2%, and the Trimmed Mean CPI increased 0.16%. We expect the core PCE deflator to rise 0.2%, leaving the Fed’s key inflation gauge up 2.9% year-over-year.

- This report reinforces expectations for a rate cut, though policymakers remain cautious that 3% inflation might linger.

Energy Lifts Headline, but Core Disinflation Resumes

Consumer prices rose less than expected in September, reinforcing the narrative that inflation is slowly cooling beneath the surface. The 0.3% monthly gain in headline CPI was powered by a 4.1% surge in gasoline, while electricity and natural gas prices declined. Excluding food and energy, prices rose 0.2%, and the three-month annualized pace of core inflation eased to roughly 2.5%—consistent with a slow glide path toward the Fed’s 2% target.

Shelter costs, which account for just over 44% of the core CPI, continued to moderate, rising 0.2%. Rent and OER slowed notably, with OER up only 0.1%, a figure partly influenced by regional volatility in Southern and Northeastern markets. The broader trend aligns with real-time rent data showing renewed softness, particularly across the South, where an influx of new supply is driving aggressive concession activity.

Shelter inflation has slowed to its weakest pace since early 2021, amidst a surge in new rentals.

Shelter and Core Services Show Genuine Cooling

The moderation in shelter costs, which account for just over 44% of the core CPI, represents meaningful progress for the Fed. This past month’s improvement coincides with weakening home prices and surge in apartment completions. Year-over-year shelter inflation has slowed to 3.6% from over 5% at the start of the year. Apartment completions will remain elevated through yearend, and market-based rent indices suggest further easing ahead.

Outside housing, core services presented a mixed picture. Airline fares rose 2.7% and hotel prices 1.7%, reflecting strong upper-income travel demand. However, declines in motor vehicle insurance (-0.4%), communications (-0.2%), and used cars (-0.4%) offset some of those gains, providing modest relief to middle-income consumers. Insurance and vehicle costs trimmed about 2 basis points from the core index.

Inflation remains uneven, with tariffs pushing goods prices higher and prices easing elsewhere.

Core Goods and Tariff Pass-Through Broadens

Core goods prices rose 0.2% in September, but the composition reflects widening tariff pass-through. Apparel climbed 0.7%, while furnishings and recreation goods each rose 0.4%. The weaker dollar and elevated import costs are feeding into retail pricing, though the overall pace remains moderate relative to 2021–22.

Tariffs and the weaker dollar have likely added roughly 0.4 percentage points to headline inflation this year. We expect the impact from tariffs to wane next year, while housing costs and prices for services outside of housing ease further.

Food prices rose just 0.2% in September, following a 0.5% gain in August. Groceries rose 0.3%, led by cereals, bakery goods, and beverages, while dairy declined 0.5%. Dining-out costs were muted—climbing 0.2% at limited-service restaurants and holding flat at full-service establishments.

Policy and Market Implications

The September CPI report bolsters the Fed’s confidence that its soft-landing game plan remains intact. Inflation is cooling without derailing growth, and alternative measures from the Cleveland Fed confirm underlying price pressures are ebbing. We expect the core PCE deflator—the Fed’s preferred inflation gauge—to rise 0.2% in September, up 2.9% year-over-year. That remains above target, but close enough to justify continued policy easing.

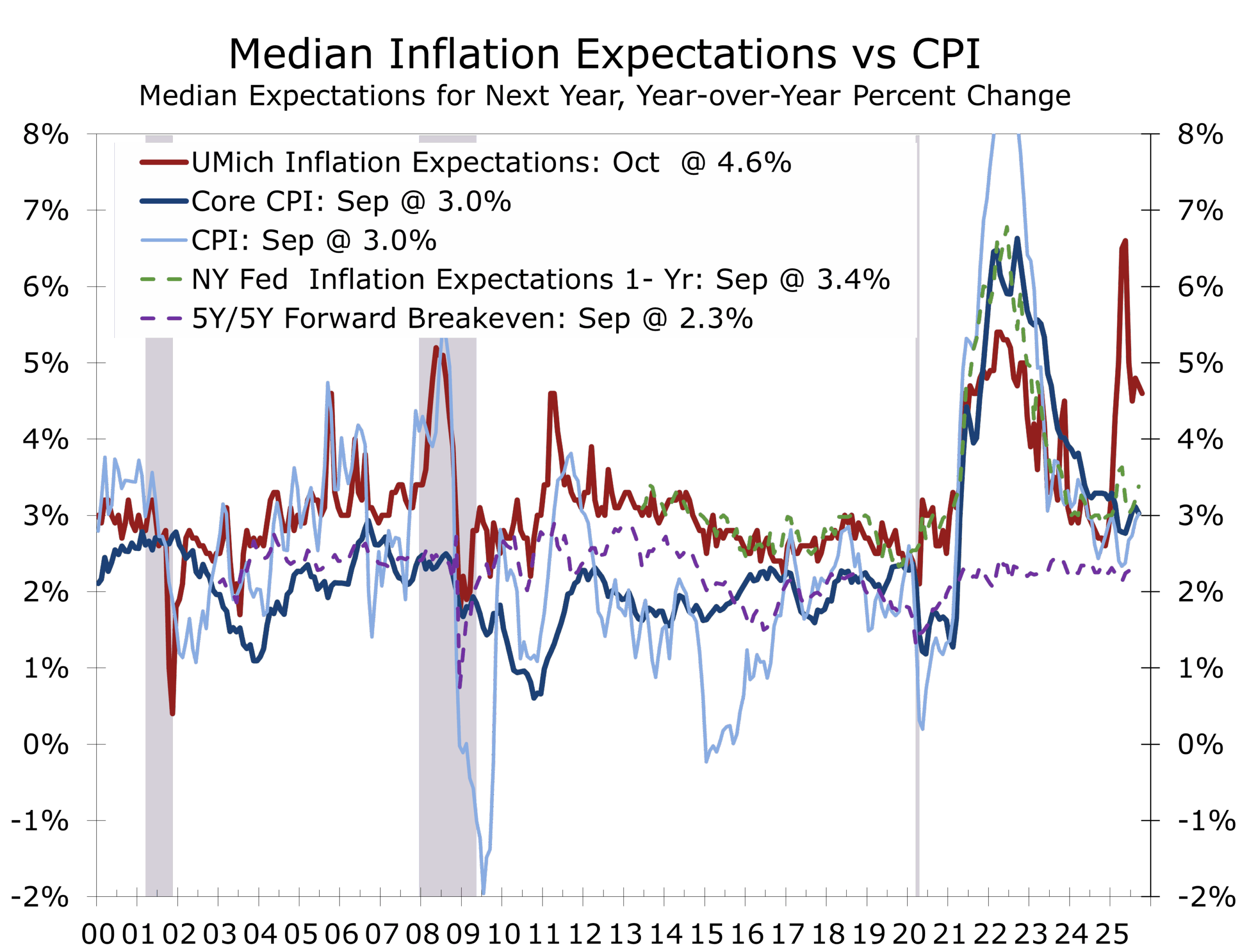

We now anticipate four quarter-point cuts in this cycle, including next week’s, followed by reductions in December and January. Long-term yields have eased modestly as markets adjust expectations. While the UMich survey still shows elevated inflation expectations, TIPS breakevens remain anchored near 2.3%, suggesting the Fed retains market credibility.

September’s CPI report was just what the Fed needed—a modest headline gain, a softer core, and a clear signal that shelter inflation is finally bending lower. While some of the recent weakness in rents could prove transitory, the underlying pattern—moderating services, stable goods prices, and improving real incomes—indicates the disinflation process remains on course.

.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

October 24, 2025

Mark Vitner, Chief Economist

(704) 458-4000