Roots of American Resilience: Shaped by the Boreal Winds

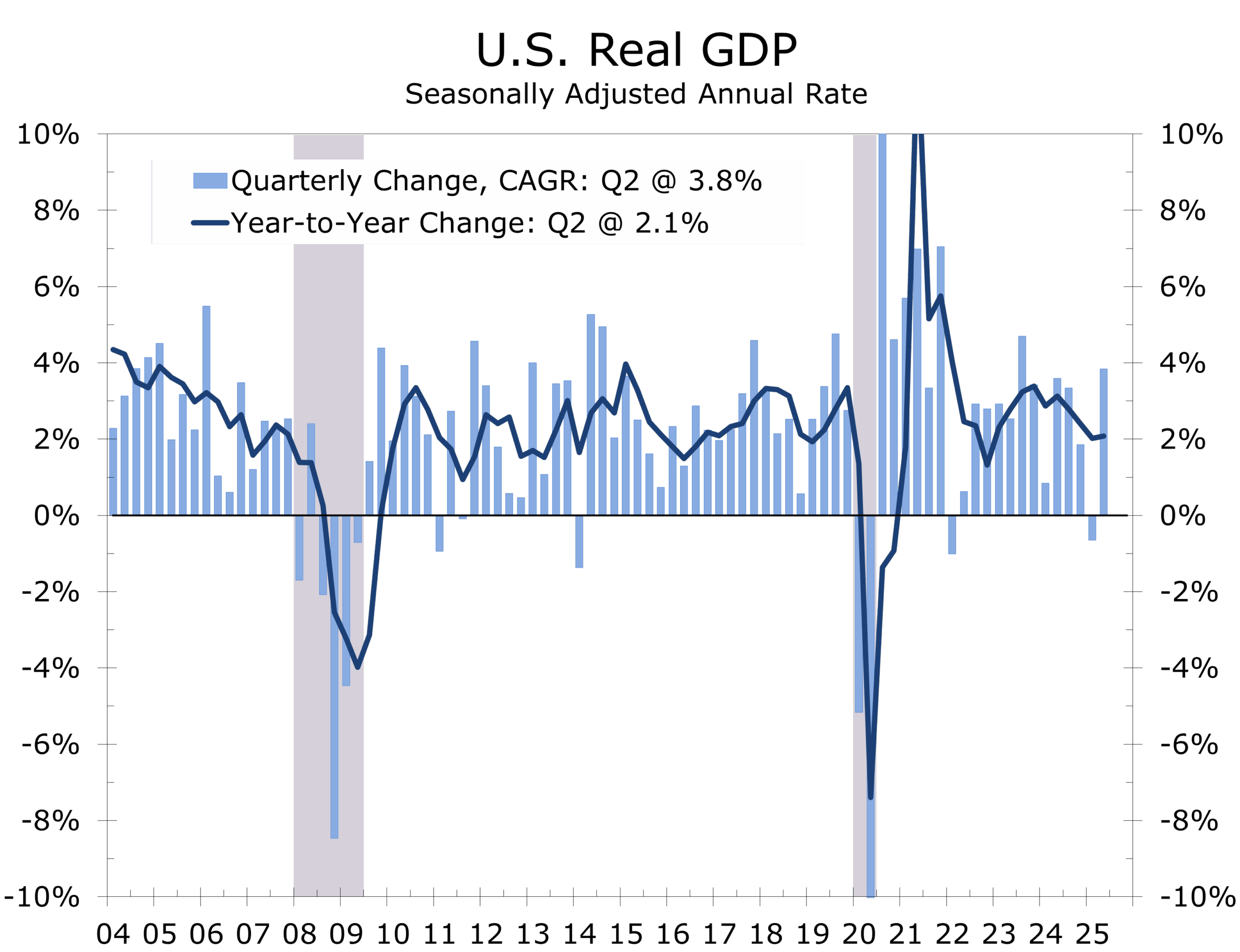

- Growth Exceeds Expectations: Q3 GDP tracking estimates have increased to between 3.4%–3.9%, supported by the buildout of AI and related infrastructure, resurgent aerospace production, and resilient consumer spending.

- Aerospace Resurgence: FAA approval for increased Boeing 737 MAX output underscores the manufacturing rebound, while defense restocking further extend backlogs.

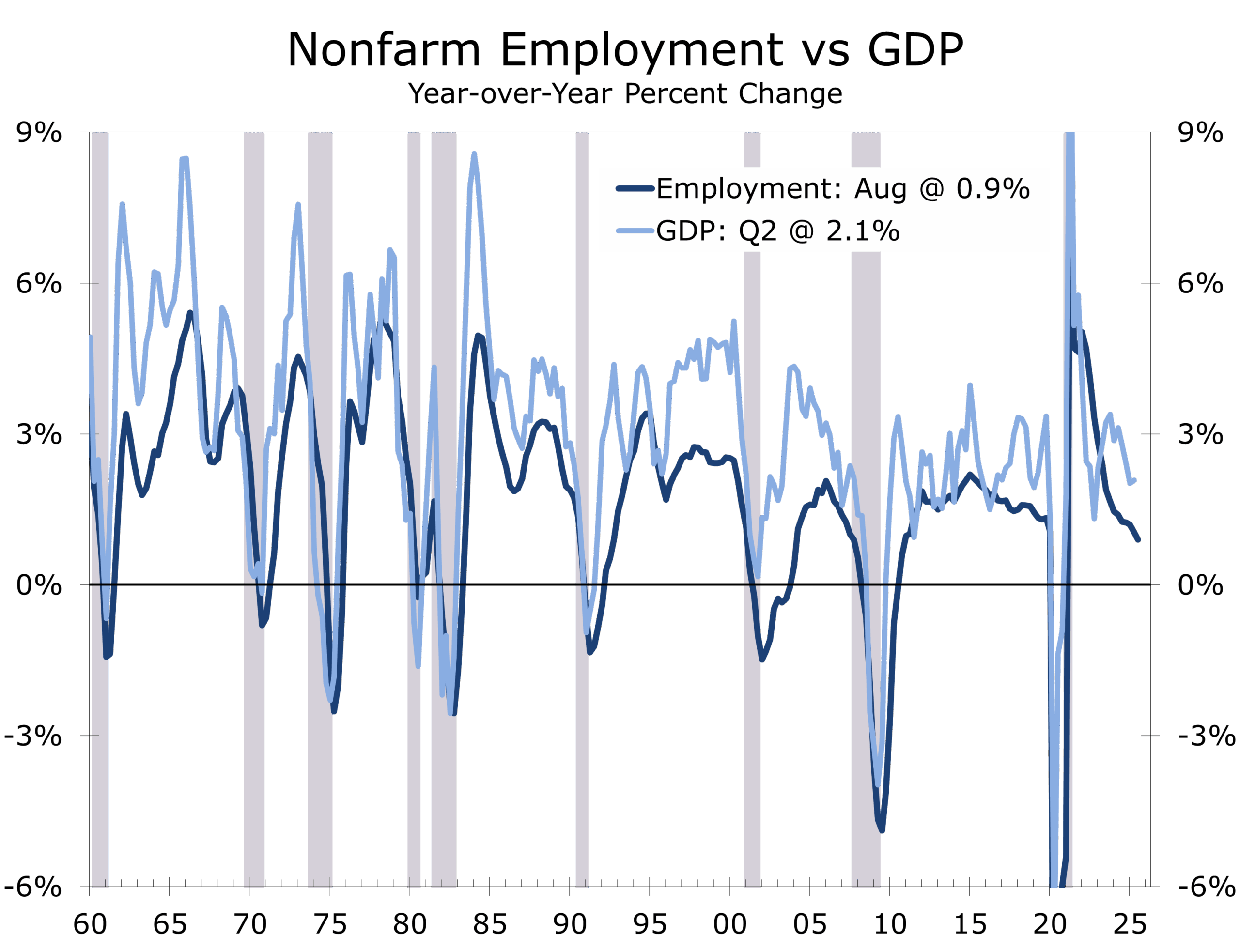

- Growth–Employment Split: Output remains strong, but job creation has stalled — signaling potential hurdles to growth estimates rather than labor acceleration.

- Roots of Strength: America’s free enterprise system, protected IP, and deep, liquid capital markets continue to channel innovation and renewal.

- Consumers Selective but Steady: Spending has narrowed to upper-income households and affluent retirees, cushioning middle-income weakness.

- AI and Aerospace Investment: Twin drivers adding 0.4–0.5 percentage points to annual GDP growth; reshoring, defense, and data centers remain pivotal.

- Housing Still Soft: Elevated inventory and affordability constraints limit near-term growth; lower mortgage rates in 2026 may unlock pent-up demand.

- Inflation Eases, Unevenly: Core CPI steady near 3.1%, restrained by slower wage gains and rents but offset by tariff-related goods costs.

- Fed Nears End of Runoff: Powell’s tone suggests a pivot to growth management, with two more rate cuts likely this year.

- Markets Regain Lift: Steeper yield curves, stronger cyclicals, and resilient risk appetite reflect belief in a “strong but narrowing” expansion.

- Geopolitics Still a Wild Card: Fragile ceasefire barely ‘holds’ in Gaza, further U.S.–China tech decoupling, and European stagnation and political discord frame the global risk backdrop.

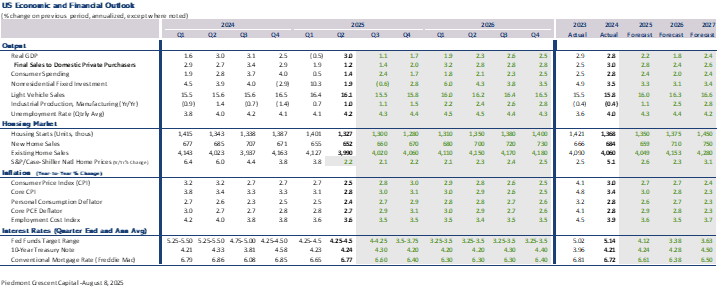

Forecast Summary:

The economy continues to evolve rather than erode, revealing a widening split between resilient real GDP growth and softening employment conditions. Growth is being reshaped by the rapid rollout of AI infrastructure, a resurgent aerospace sector, record defense outlays, and remarkably resilient consumers — including a growing cohort of affluent retirees whose spending forms the deep roots sustaining the canopy through shifting global winds.

Much like cycling through Puglia’s olive country, the journey is uneven: the path alternates between steep climbs and smooth coastal descents, yet the centuries-old trees endure — gnarled, resilient, and deeply rooted in fertile soil. The U.S. economy today mirrors that landscape: tested by headwinds yet anchored by enduring strengths that adapt rather than break.

Macro Overview – Growth Exceeds Expectations but Remains Uneven

The U.S. economy remains a study in contradictions. The Atlanta Fed’s GDPNow model pegs Q3 growth at 3.9%, well above potential and nearly double what forecasters expected earlier this summer. Our own estimate, at 3.4%, is only modestly lower — still impressive given the stall in job creation and moderation in hours worked.

Beneath the surface, however, momentum looks less robust. The NFIB Small Business Optimism Index and regional Fed manufacturing surveys signal rising uncertainty, weaker demand, and subdued capital spending intentions. The divergence between output and sentiment reflects an economy powered by narrow, capital-heavy engines — AI infrastructure, aerospace, and defense — that lift GDP but not necessarily payrolls.

Fed Governor Waller acknowledged this imbalance, observing that policy calibration will depend on “how the growth–employment split resolves.” In effect, the economy is producing more with fewer hands — a productivity rebound that complicates the inflation debate.

Boeing’s FAA approval to expand 737 MAX output from 38 to 42 planes per month, with potential to reach 45 by early 2026, captures this dynamic perfectly. Industrial momentum is reviving through sectors that are capital-intensive but labor-light, while defense contractors continue to work through record order backlogs as allied nations rearm and replenish depleted stockpiles. This underpins a durable manufacturing cycle even as broader business sentiment cools.

The service sector shows signs of fatigue — particularly in middle-income discretionary categories — but upper-income consumers remain the quiet engine behind growth. Spending in travel, leisure, and premium goods continues to expand, while home renovation and repair outlays partially offset the drag from new construction.

Taken together, the economy is expanding unevenly but firmly — evolving, not eroding.

Like those ancient olive groves that have weathered centuries of storms, the U.S. expansion is rooted in structural strengths that sustain it through changing winds. If the growth–employment split resolves through slower output rather than faster hiring, as we expect, long-duration assets and yield-curve steepeners should outperform into year-end.

The Growth–Employment Split – A Cycle Out of Sync

Economic activity and employment typically move in a circular, self-reinforcing pattern — spending and capital investment drive income, which drives jobs and strengthens confidence, which fuels further spending and investment. Today, that feedback loop has weakened. GDP is expanding above potential, yet hiring has slowed and job openings have fallen to two-year lows just as federal retirements and furloughs have increased.

The causes behind this split are structural as well as cyclical. The AI buildout is labor-light but capital-deep, while the aerospace and defense sectors are operating under long-lead contracts that boost output before hiring. Tariffs and inventory restocking also inflate nominal GDP through price effects. The NFIB data confirm that small businesses face cost pressures and weaker sales expectations, signaling that hiring will remain modest.

The divergence will close primarily through slower economic growth rather than a meaningful rebound in jobs. Hard data, including hours worked and manufacturing employment, which typically preceded employment trends, have slowed since spring. For policymakers, this implies lower potential growth in the near term but less inflationary risk — a backdrop favoring rate cuts and longer duration. Longer term, the investment surge should strengthen potential growth and reduce inflationary pressures.

Markets are already reflecting this adjustment: breakeven inflation has stabilized, and forward-rate spreads point toward a softer landing. The U.S. may be entering a phase of “quiet deceleration” — with economic activity cooling without cracking.

.

Consumers – Spending Through the Headwinds

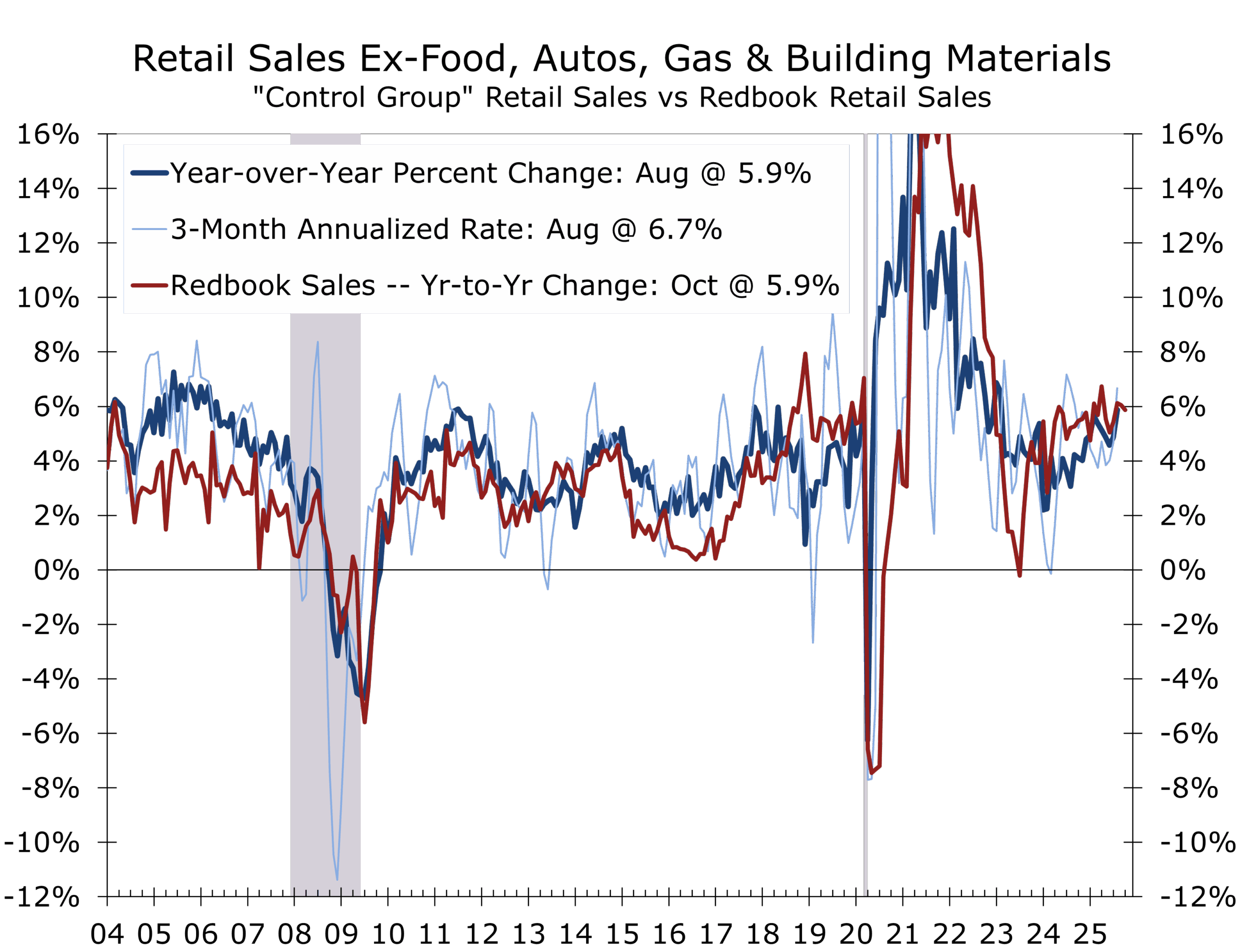

Household spending remains the economy’s ballast, though its composition is shifting. Retail sales surprised to the upside through late summer, with strength in travel, healthcare, and restaurants. Credit costs are rising, with auto-loan delinquencies at ten-year highs and revolving credit balances outpacing income growth twofold. With the government shutdown, August is the last data point for retail sales. Redbook retail sales, which measure same-store sales at department stores, discount stores and chain stores, suggest sales have kept pace with their previous trend through October. We estimate that core retail sales rose at around a 0.4% pace in September and should rise by a like amount in October.

One stabilizing influence is demographics. Affluent retirees now account for an outsized share of discretionary consumption, supported by wealth gains and Social Security COLAs. This cohort’s spending is less sensitive to labor-market fluctuations and acts as an anchor during cyclical slowdowns. In contrast, lower- and middle-income households are increasingly value-conscious, trading down to discount brands and stretching loan maturities. Sales at chains dependent upon middle- and lower-income consumers have been lagging, with the exception of a few giant firms with marketing budget heft.

The Beige Book described consumer behavior as “price-aware but persistent.” Retailers report steady traffic but lower ticket sizes, a pattern consistent with slowing but sustainable real consumption. Inflation-adjusted spending remains positive, suggesting that while demand is cooling, it continues to stabilize the broader economy. Inventories remain in line with sales.

Over time, as borrowing costs ease, pent-up demand in autos and housing should reemerge, helping reignite related outlays. Until then, consumers are spending selectively — but they are still spending.

Business Fixed Investment – The AI and Aerospace Flywheel

AI and aerospace have become the twin engines of America’s capital cycle. Data-center construction is up more than 30% year-over-year and now accounts for nearly one-fifth of all private nonresidential structures. The AI capex surge is large enough to lift broader growth—its spillovers extend across utilities, logistics, and industrial construction—without crowding out other activity or fueling overheating.

Aerospace and defense form the second axis of strength. Boeing’s 737 MAX production ramp, alongside record backlogs at Lockheed Martin, RTX, and Northrop Grumman, underscores a durable manufacturing upturn. Defense suppliers across the U.S. and Europe are expanding capacity to rebuild arsenals, keeping output and exports elevated.

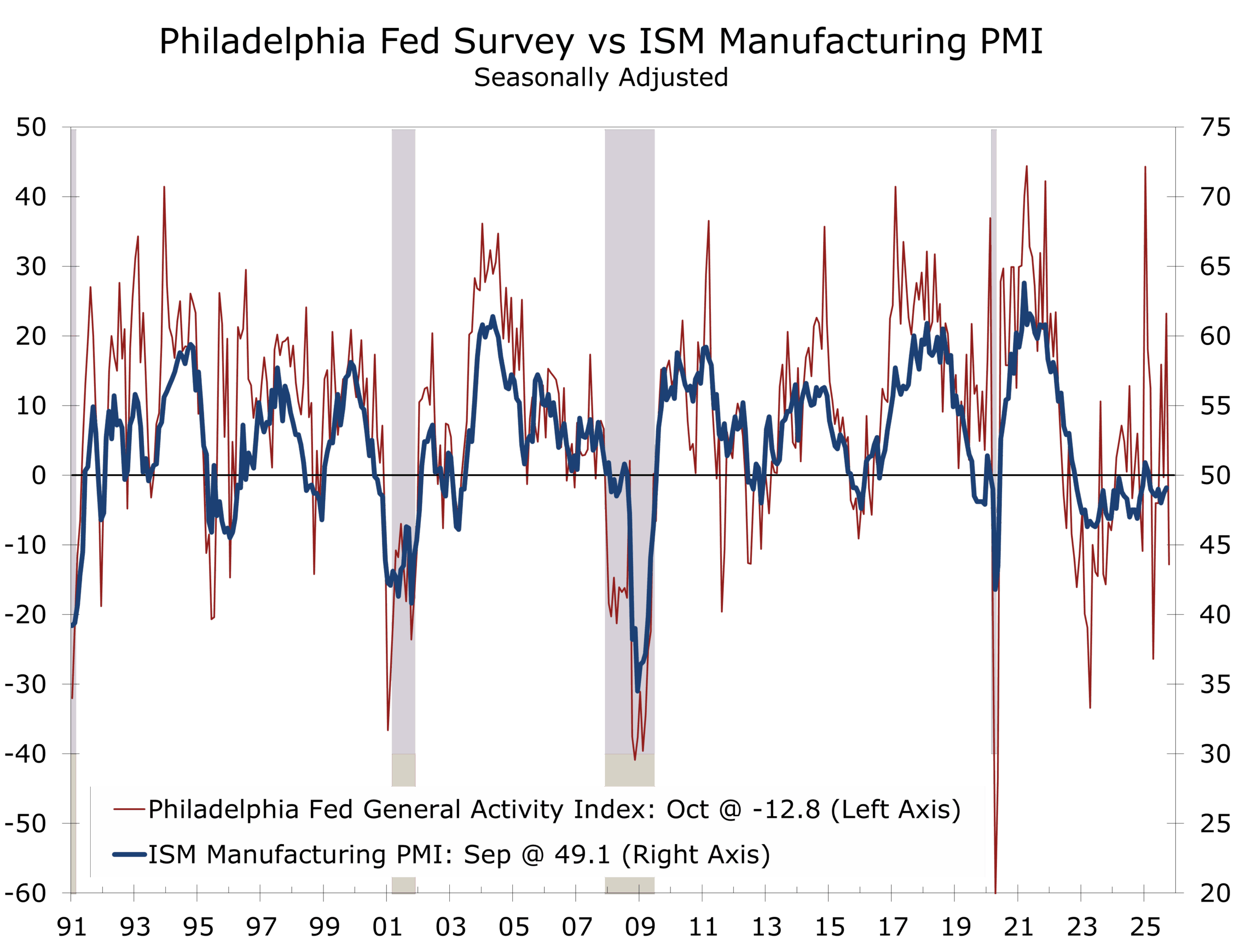

Outside these sectors, private investment remains mixed. Pharmaceuticals and medical devices are bright spots, but housing-related and consumer-linked spending remain soft. The Philadelphia Fed’s October survey showed a sharp headline decline, while the Empire survey jumped; together they imply manufacturing activity hovering just below the ISM’s 50-point threshold. Financing conditions remain tight, yet the scale of AI, defense, and blockbuster pharma projects—especially in the South—continues to move the needle for industrial demand.

The result is an economy driven by capital-deep innovation rather than broad expansion—one where productivity rises faster than payrolls. The pattern recalls the late 1990s tech cycle, though this phase appears earlier in its trajectory, with structural investment still gathering momentum. We expect capital spending to broaden, as the AI boom begins to materially reshape nearly every sector of the economy. The recent retrenchment in EV investment was an inevitable correction that will redirect capital toward internal combustion and hybrid platforms, strengthening the industrial base. Like those ancient olive trees in Puglia, today’s capex cycle is rooted deeply but growing deliberately—its expansion measured, resilient, and likely to bear fruit over a longer horizon.

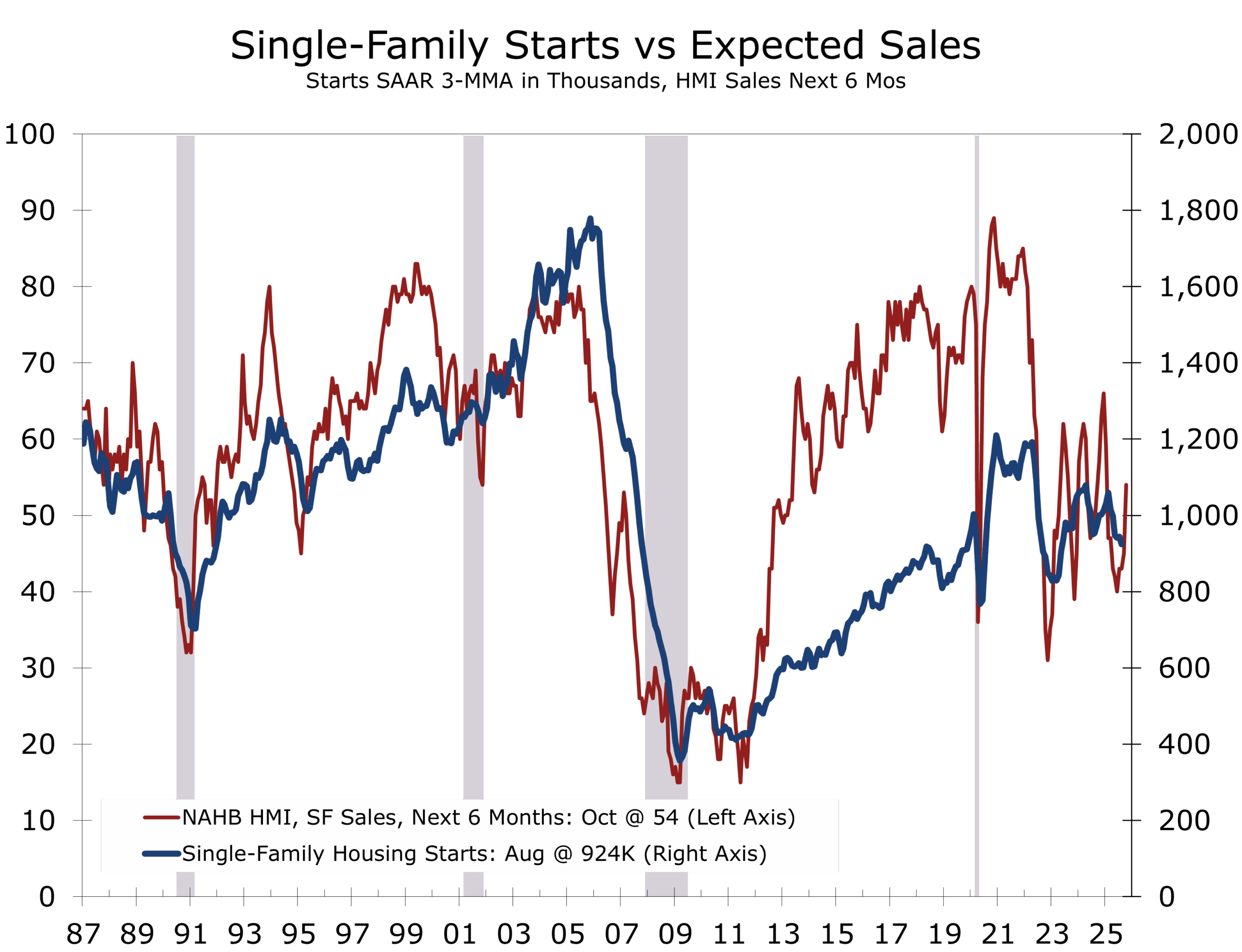

Housing – Waiting for Lower Rates to Take Root

Even as builders continue to grapple with elevated costs and macro uncertainty, sentiment in the single-family sector posted a meaningful uptick in October. The National Association of Home Builders/Wells Fargo Housing Market Index (HMI) climbed five points to 37 — the highest reading since April — as the sub-index for future sales expectations rose above the key 50-point breakeven threshold for the first time since January.

The improvement reflects two converging forces. Mortgage rates have edged down, with the 30-year fixed rate falling from just over 6.5 percent in early September to roughly 6.3 percent in early October, offering modest relief to strained affordability. At the same time, builders are positioning for a 2026 recovery, reporting firmer demand in premium and Sunbelt markets and a steady flow of well-capitalized buyers — including older, wealthier households driving remodeling and luxury activity. Yet most prospective buyers remain sidelined, awaiting more significant rate declines before re-entering the market.

Despite better sentiment, the market remains fragile. In October, 38 percent of builders reported cutting prices, with average reductions of 6 percent, while two-thirds offered sales incentives to preserve absorption rates. These tactics illustrate the sector’s bifurcation: strength in luxury and remodeling contrasts with persistent weakness in starter-home and turnover-driven segments. The NAHB estimates that single-family permits likely rose about 3 percent in September, despite the government shutdown delaying official Census data releases.

The broader outlook remains one of cautious optimism. Housing is unlikely to make a major contribution to GDP in 2025, but it is poised to regain momentum in 2026 as rates decline further and pent-up demand is released. For now, the economic spillovers are showing up in adjacent categories — furniture, appliances, home improvement, and repair services — rather than in new construction. The housing market, like the broader economy, is waiting for lower rates to take root — and once they do, it could set the stage for a glorious spring.

Inflation and Monetary Policy – Flying by Instruments

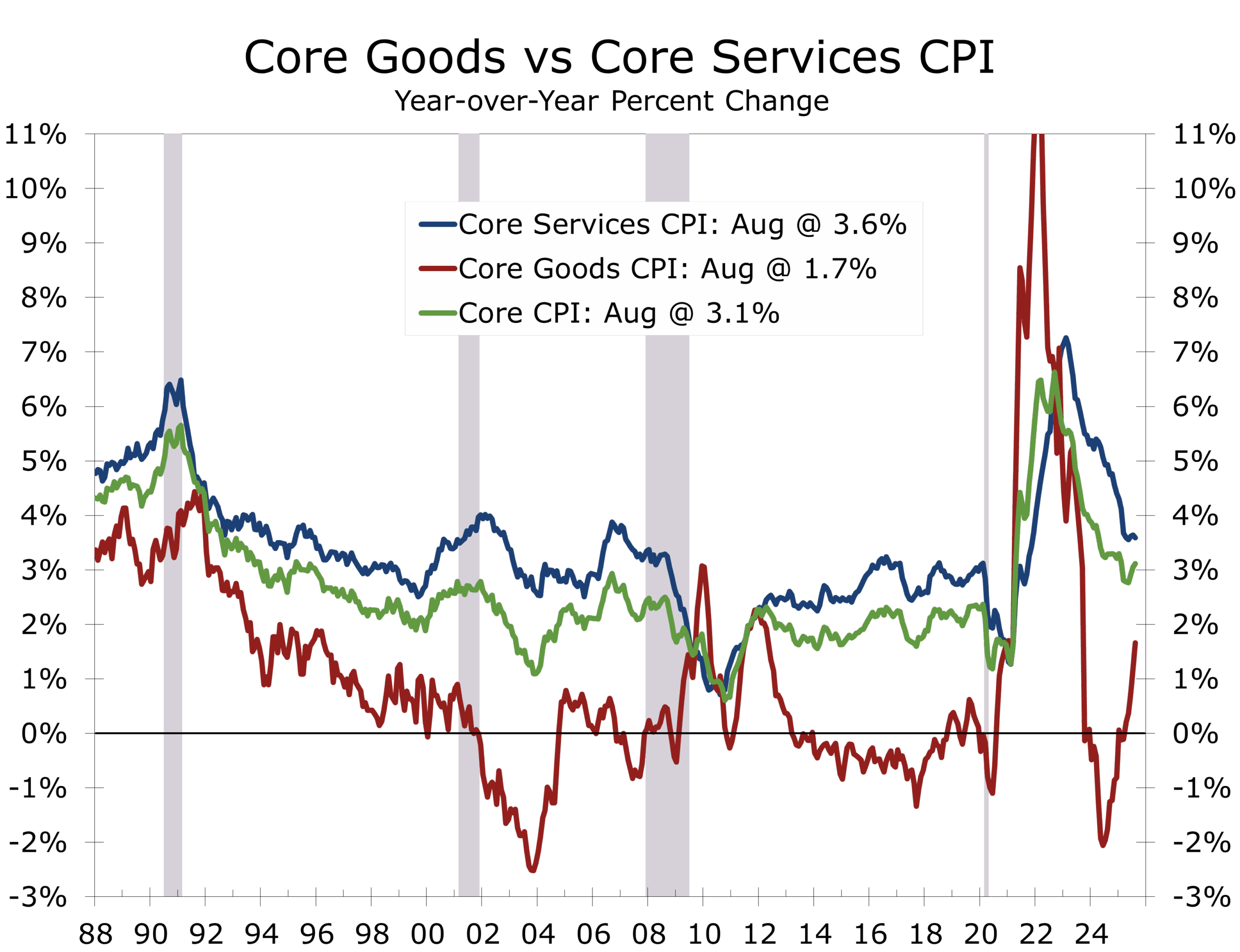

The latest inflation reading for August showed headline CPI up 0.4% month-over-month and 2.9% year-over-year, while core CPI rose 0.3% month-over-month and 3.1% year-over-year. Rent disinflation continues, but tariff-related goods prices and lingering auto supply bottlenecks have delayed a full return to target.

In a notable sign of the Fed’s priorities, the Bureau of Labor Statistics (BLS) recalled furloughed staff to complete the September CPI and rescheduled its release for October 24 — just days ahead of the Federal Open Market Committee (FOMC) meeting on October 29. That move highlights how essential the data are to policy direction: both to build internal consensus for a possible October cut and to preserve credibility with markets, calming volatility and helping anchor long-term yields.

Jerome Powell has signaled that the Fed is nearing the end of balance-sheet runoff “in the coming months,” marking a full pivot toward risk-management. Market expectations now price in two additional rate cuts by year-end (including October), consistent with easing inflation pressures and anchored expectations — as also shown by the National Federation of Independent Business (NFIB) survey’s moderation in wage growth and price intentions.

Volatility has eased as policy communication has become clearer. The Fed is now flying by instruments, guided by inflation expectations, credit conditions, and labor-market data rather than headline GDP. The divergence between core goods inflation (which remains elevated due to tariffs and supply constraints) and core services inflation (which continues to carry the bulk of sticky cost pressures but is also gradually easing as middle and lower-income consumers pull back discretionary spending) underscores the uneven nature of disinflation. Tariffs and supply frictions will likely keep core inflation hovering just above 2½% into 2026, but the overall trajectory remains benign enough for the Fed to ease policy cautiously while preserving market credibility.

Financial Markets – Shifting Gears on the Climb

Markets are recalibrating as if on a long, steady climb — momentum slowing, cadence controlled. The S&P 500 recently touched an intraday record near 6,735, up roughly 1.1 % for the month and within sight of its all-time high. Gold surged past $4,300/oz, reaching a new milestone after a 60 % rally year-to-date, fueled by rate-cut expectations, a softer dollar, and unrelenting geopolitical crosswinds. Investors, like seasoned cyclists cresting a ridge, are pacing for endurance rather than acceleration.

Beneath that smooth surface, the gears of credit are grinding. The IMF’s $4.5 trillion estimate of bank exposure to hedge funds and private-credit vehicles underscores the growing entanglement between regulated and nonbank finance — a chain drive of leverage that is well-oiled in good weather but vulnerable to sudden strain. Floating-rate, covenant-lite loans from the 2020–21 vintage are now colliding with tighter funding conditions, creating a slow-motion stress test for private markets and smaller lenders alike.

Investor psychology is shifting accordingly. The flight toward duration and quality continues, with surveys showing over half of institutional investors expect gold to top $5,000/oz within a year — not just a hedge against inflation, but a bet on policy stability and system resilience. Credit spreads remain tight, and within that narrow peloton, Ba-rated corporates still offer the best risk-to-reward drafting position. Yet complacency lurks on the downhill: the private-credit boom increasingly evokes 2007, when leverage hid in plain sight and liquidity vanished just as the descent began.

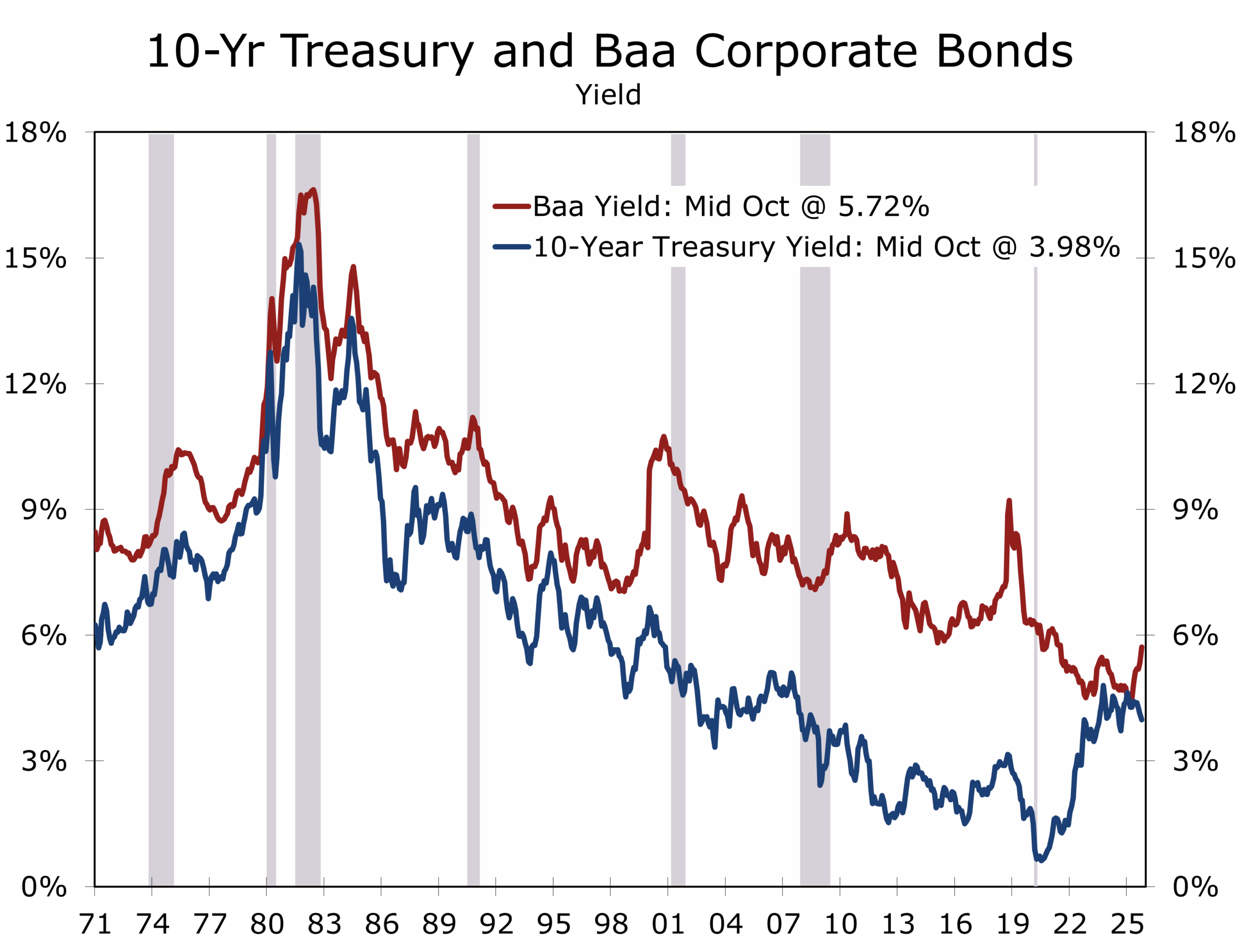

In today’s markets, the winners are the riders who pace the climb. Steepeners beat sprinters. Patience, liquidity, and balance-sheet agility remain the key gear ratios for performance. With the yield curve still steep, policy credibility restored, and risk appetite re-aligning, long-duration Treasuries and high-grade spread assets remain best positioned for those who ride the course rather than chase the crowd.

Geopolitics – Ceasefires, Stagecraft, and Supply Chains

Middle East: a truce on training wheels — The Hamas–Gaza Strip cease-fire is holding for now but remains fragile after weekend flare-ups and reciprocal allegations of violations. U.S. envoys are pressing both sides to recommit and preparing a “phase two” track. That said, core issues—Hamas disarmament, Israeli withdrawals, and the governance of Gaza—are still unresolved. For markets, the U.S.-brokered pause has reduced some energy risk premium, helping keep Brent around the low-$60s, after earlier trading sub-$60 on contentions of oversupply and logistical contango.

Trump–Zelensky: private heat, public cool. What likely happened? — Multiple credible outlets reported a contentious closed-door session in which Donald Trump pressed Volodymyr Zelensky to consider territorial concessions in the Donbas and warned of escalation by Vladimir Putin—even as the public press conference projected a measured tone and spoke of diplomatic “opportunities.”

Our read: Trump is negotiating on multiple fronts. His Middle East diplomacy feeds into the Russia-Ukraine axis, which in turn influences upcoming China talks. We believe the likely settlement will reflect the lines drawn today—rather than forcing Ukraine to relinquish more of the Donbas. If that fallback fails, we anticipate more sophisticated weapons transfers to Kyiv.

Energy diplomacy: calm by coordination, not coincidence — Simultaneously with the Gaza truce, Saudi pricing signals and incremental OPEC+ supply openings have aligned with softening demand data and a stronger dollar—together reinforcing the slide in crude. The upshot: Brent remains near $60 with a downside skew, provided surplus flows continue building.

U.S.–China: tariff détente on pause; controls tighten — Trade tensions remain under the surface but very active. Beijing expanded export controls on rare-earths, magnets and advanced manufacturing technologies—targeting inputs with as little as 0.1% China-origin content. Washington’s 100 % tariff threat remains suspended but not revoked, while new U.S. port fees due in coming years are nudging logistics costs higher. Net effect: supply chains are less brittle than during 2022-23 but are increasingly constrained for high-spec inputs.

Europe re-arms: risk and stimulus in one package — Defense spending keeps climbing and order backlogs are near historic highs—supporting capex cycles across aerospace, munitions, and sensors. The International Institute for Strategic Studies (IISS) documents a near-doubling of procurement since 2022; Fitch points to record backlogs boosting cash flow visibility. This is one of the rare geopolitical drivers that adds demand even while elevating headline risk.

Outlook – The Shape of Endurance

The U.S. economy is navigating an expansion on narrow but durable tracks. Growth remains stronger than expected, even as hiring loses pace and business confidence softens. The divergence reflects a structural transformation — an economy increasingly powered by capital-intensive industries rather than labor, by AI infrastructure, aerospace, and defense. Beneath the statistical noise, productivity is quietly rebuilding the foundation of growth. The challenge for policymakers is to recognize that this strength is real but uneven, and to calibrate policy easing without reigniting imbalances.

For now, the nation stands in a rare posture: robust overall growth, soft labor conditions, and a fading tariff-driven inflation flare-up that allows a gradual tilt toward easier policy. This equilibrium will not endure indefinitely, but it remains a favorable setup for both investors and households. As AI, aerospace, and affluent retirees reshape the composition of demand, the expansion is likely to moderate but remain structurally sound. The Fed’s task is to guide the economy through this labor-market deceleration without stifling renewal, preserving the potential for a lengthy, measured expansion.

Like the ancient olive trees of Puglia, the American economy draws its resilience from deep roots — free enterprise, property rights, innovation, and trusted financial markets. The winds may twist its branches, but not its foundations. Growth will bend but not break, and by the spring and early summer, the cycle is likely to show new shoots — evidence that endurance, not acceleration, remains the true measure of strength.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

October 21, 2025

Mark Vitner, Chief Economist

704-458-4000