Retail Sales Get Q3 Off to a Strong Start

- Overall retail sales rose 0.7% in July, with spending up solidly in most key categories.

- Core retail sales – a key input into the GDP calculation – rose 1.0% in July and gains for the prior 2 months were revised higher.

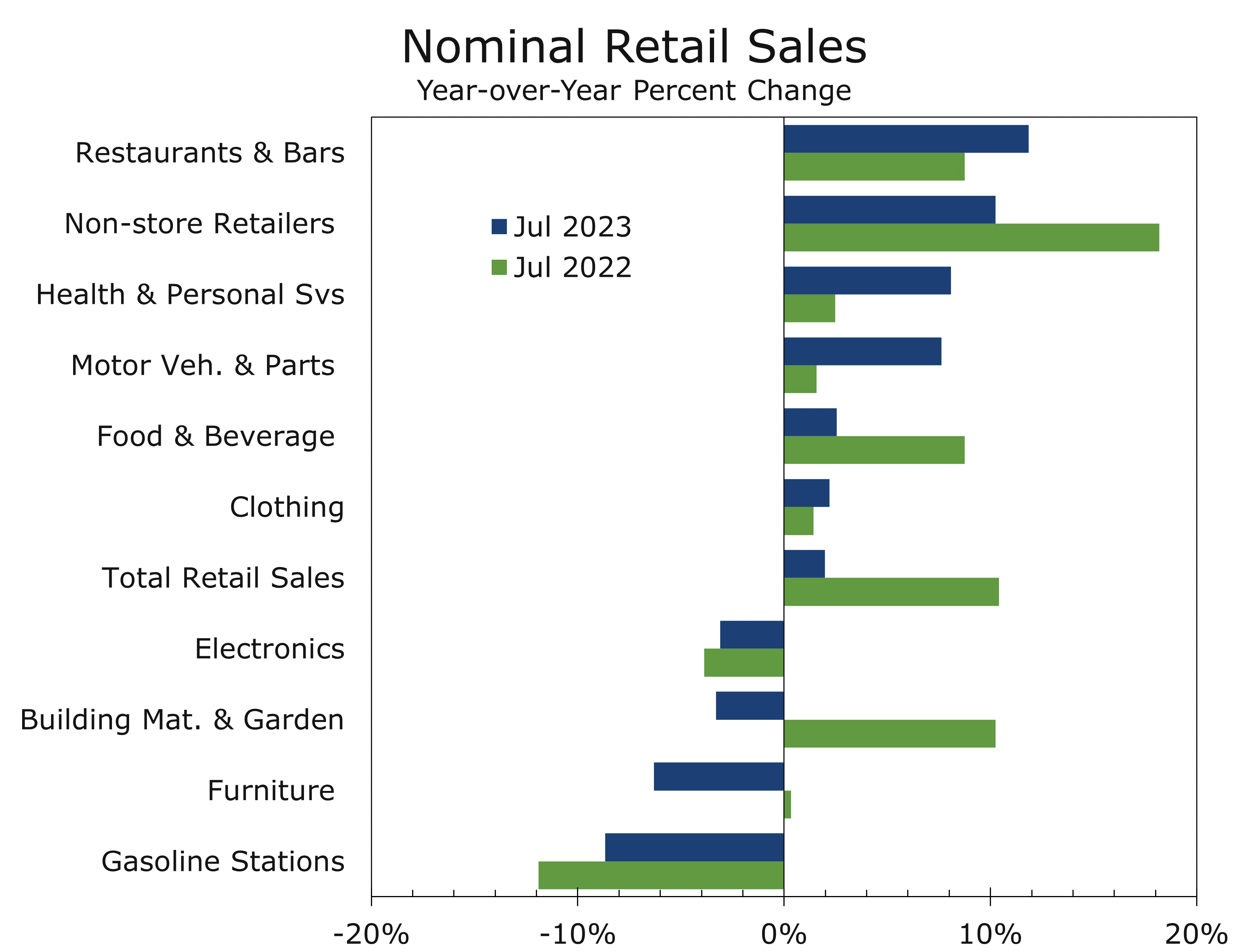

- Retail sales were bolstered by Amazon Prime Day. Non-store retail sales surged 1.9% during July and are up 10.3% over the past year.

- Brick and mortar stores also did well. Sales at sporting goods stores rose 1.5%, while sales at clothing shops rose 1.0% and sales at department stores rose 0.9%.

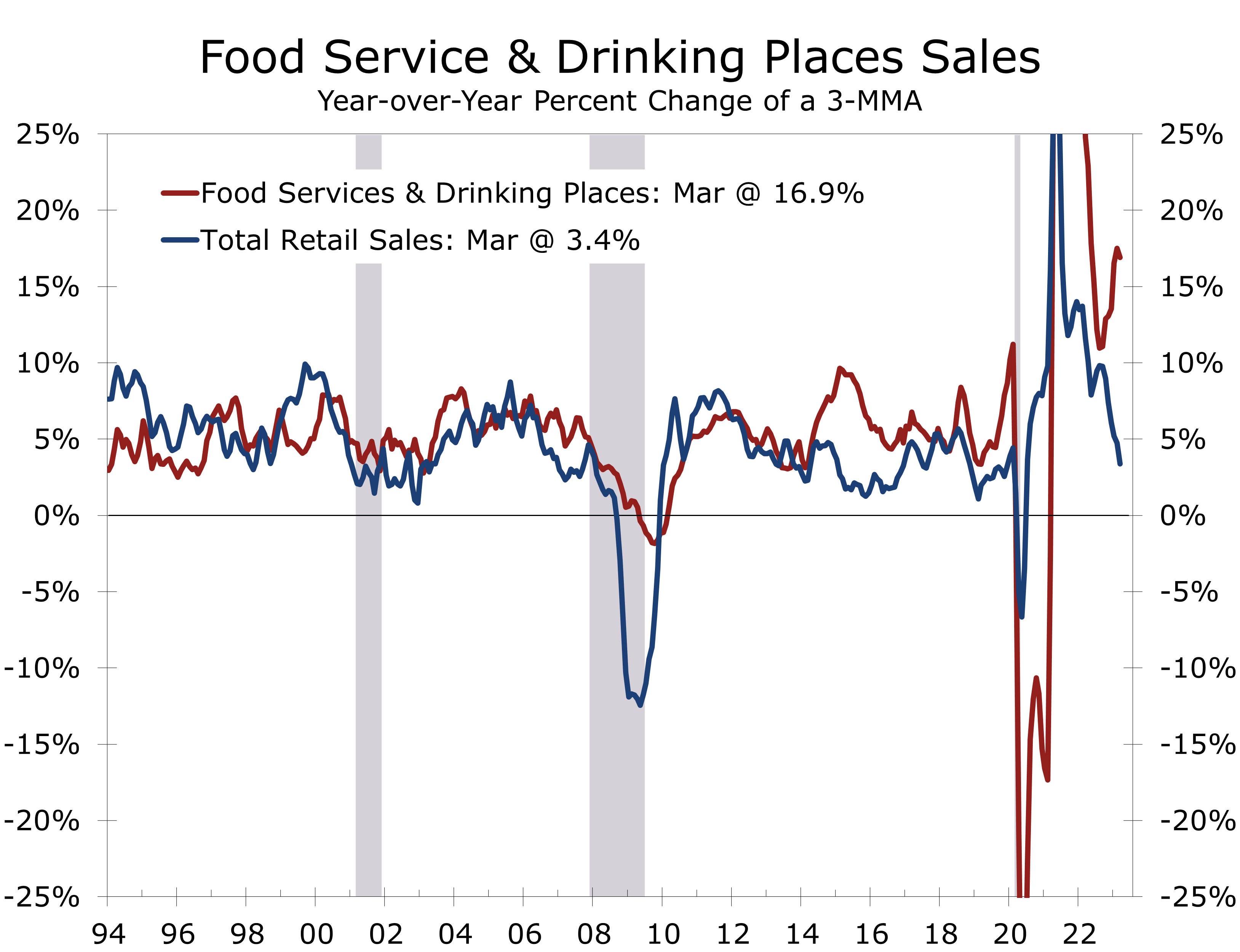

- Restaurants and bars had another blowout month, with sales surging 1.4% in July and 11.9% over the past year.

- Furniture and electronics store sales were notable weak spots, falling 1.8% and 1.3% in July, respectively.

- The robust gains at the start of the quarter and upward revisions to the May and June data enhance the prospects for Q3 growth. Real GDP now looks like it well rise at around a 2.5% in current quarter.

Retail sales showed surprising strength in July. Overall sales rose 0.7% and core retail sales jumped 1.0%. July is a shoulder month, with retailers typically marking down summer items ahead of the back-to-school season. Amazon Prime Day and competing promotions at brick-and-mortar retailers may have pulled some sales forward from August.

Retail sales are notoriously volatile and subject to a wide variety of short-term distortions that can be magnified by seasonal adjustment. That is one of the reasons why economists tend to look at sales excluding motor vehicles and gasoline. While motor vehicle sales have been strong in recent months, gasoline sales have been a drag on overall sales, as falling gasoline prices have depressed reported sales at gasoline stations.

Sales at motor vehicle dealers, parts stores and repair shops fell 0.3% in July but have been exceptionally strong of late. Sales actually breached their all-time high hit just after the economy reopened back in April 2021 in June. Part of the recent strength likely reflects some catch up at repair shops and body shops, which have built up enormous backlogs due to parts shortages, which are abating.

Sales at building materials stores rose 0.7% in July. Sales at home improvement centers have been struggling this past year, falling 3.3% over the past year. Part of that drop is due to the continuing weakness in existing home sales, which usually prompt several trips to home improvement stores by both the seller and buyer. Consumers also appear to be more interested in spending more of their free time traveling or going out rather than fixing up their homes.

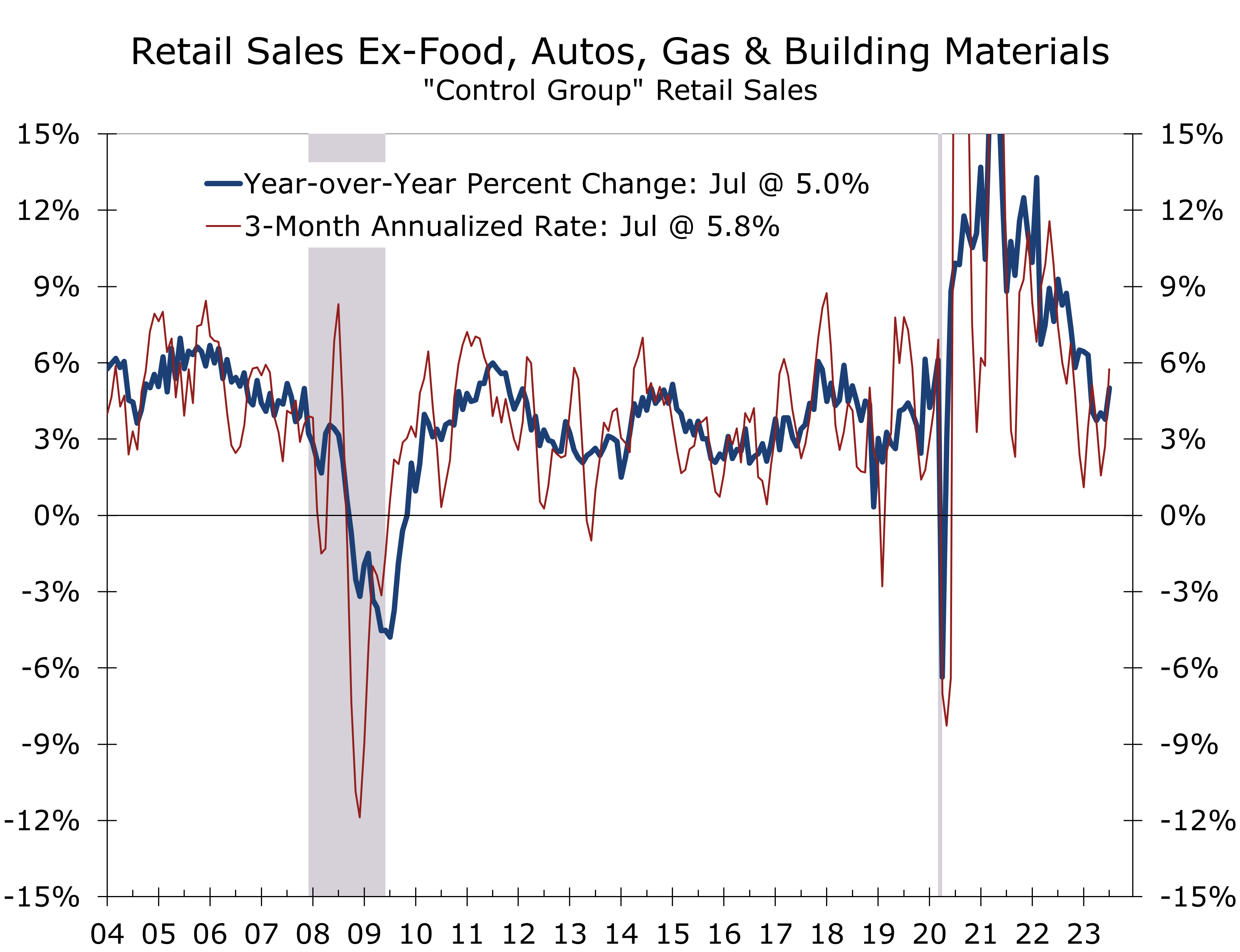

Core retail sales, or retail states excluding motor vehicles, gasoline stations, food and building material stores, are a key input in calculating consumer spending on goods in the quarterly GDP data. The most recent data show core, or ‘control group’, retail sales climbing at a 5.8% pace over the past three months. The recent moderation in the CPI suggests much of the recent rise in core retail sales will flow through to Q3 growth. We had been expecting real GDP to rise at a 1.1% annual rate, growth now looks to be close to a 2.5% pace.

With inflation moderating, much of the rise in core retail sales will flow though to Q3 growth.

Sales rose across nearly every key category in July. Spending at sporting goods stores rose 1.5%, while spending at clothing stores rose 1.0% and sales at department stores rose 0.8%. We suspect that some of this strength reflects promotions by brick-and-mortar retailers to compete with Amazon Prime Day.

Sales at grocery stores and gasoline stations rose 0.8% and 0.4% respectively. Higher prices are likely responsible for much of those gains, however. Gasoline prices had plummeted for much of the past year, which has pulled sales at gasoline stations down 20.8% over the past year. Gasoline prices have rebounded more recently, which will cut discretionary spending in August and September.

Consumers have been cutting back on some larger discretionary purchases for some time. Spending at furniture stores fell 1.8% in July and are down 6.3% over the past year. The persistent weakness in furniture sales reflects some payback from the pandemic when consumers purchased furniture to accommodate remote work and remote learning. The weakness in furniture sales is falling back on manufacturers, leading to plant closures and bankruptcies.

The payback from the pandemic is also likely weighing on sales at electronics stores. Sales fell 1.3% in July and have fallen 3.1% over the past year.

Another reason consumers are spending less on furniture and electronics is they spending more time away from home. Spending at restaurants surged 1.4% in July and is up a whopping 11.9% over the past year. While higher prices account for part of that rise, much of it is increased volume.

July’s stronger retail sales report has brought back talk of a ‘no landing’ scenario, which sent Treasury yields higher on concerns the Fed has more work to do. We suspect the strength in Q3 consumer spending will likely prove to be frontloaded and look for some payback in August and September.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.