Off the Cliff, But Not Out of the Woods

- Job growth is slowing, revisions are trending lower, and key labor metrics are weakening beneath the surface. The latest QCEW employment data imply the monthly jobs numbers are overstated by at least 500,000 jobs and the narrowing breadth of job gains and drop in labor force participation suggest the labor market is losing momentum.

- Tariff uncertainty continues to weigh on trade, manufacturing, and business confidence. Recent reprieves and postponements of tariff deadlines has bolstered confidence that a worst case outcome is less likely.

- Consumer spending is shifting; services are holding up, but goods outlays are softening after a brief surge ahead of tariffs. Income growth remains solid, although not quite as strong as recent headlines imply. Social Security catch-up payment have bolstered personal income growth. Wage and salary growth remains solid, however, and should support consumer spending.

- Actual inflation remains well-contained, but perceptions of rising prices are intensifying. The CPI and PCE deflators continue to come in below expectations and year-to-year gains are close to the Fed’s target. Producer Prices appear more vulnerable to higher tariffs, but tighter margins will limit pass throughs. With consumers spending more for imported goods, they will have less to spending on other goods and services, restraining price gains for these items.

- The Fed remains in ‘wait-and-see’ mode; a September cut seems plausible, but the Fed may wait longer for events to more fully play out. A surprise budget deal, with greater budget savings, would set the table for more aggressive easing.

- Geopolitical flashpoints—including Ukraine’s deep strikes and the unproductive nuclear talks with Iran—are raising tail risks. Domestically, President Trump’s deportation initiative has gained momentum in the courts but run into oppositions in the streets.

- Renewed U.S.-China trade talks in London offer hope but underscore persistent global uncertainty. A tentative deal looks promising and paves the way for a more substantial deal later this year. Trade deals have so far proved elusive, and the Trump Administration would like to implement the bulk of them before the run up to the midterm elections.

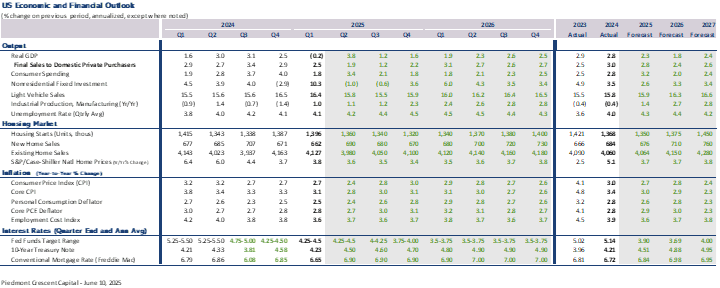

- Q2 GDP forecasts have been revised higher following a sharp drop in the trade deficit. We are currently looking for real GDP to rise at a 3.6% pace in Q2 and slow to a 1.5% pace in the second half of this year before rebounding in 2026. Full-year expectations remain cautious but could strengthen if consumer inflation fears prove overstated or fail to materially impact spending behavior.

Quiet Contraction, Rising Risk

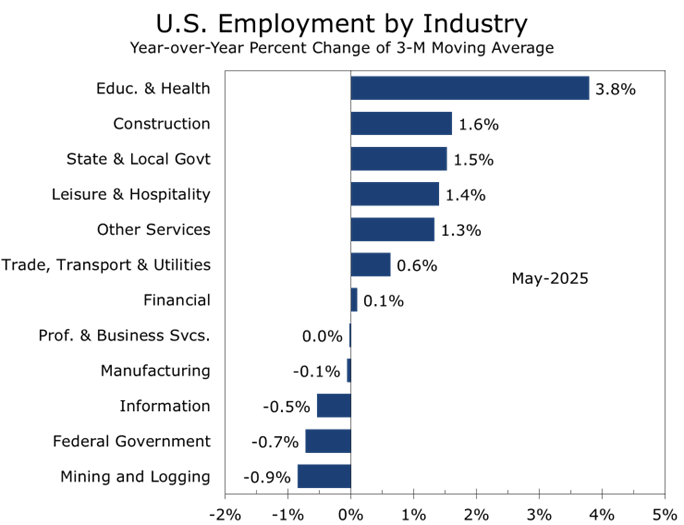

The U.S. economy continues to grind forward, but the gears are clearly slipping. The May employment report underscored a labor market that’s softening beneath the surface. Payrolls rose a modest 139,000, but the three-month average slipped to just 135,000. Downward revisions subtracted 95,000 jobs from prior months, and updated QCEW data suggest 2024 job growth may have been overstated by more than 500,000 jobs. The unemployment rate held at 4.2% but conceals a 0.2-point drop in labor force participation and a 0.3-point decline in the employment-population ratio. Slack is building quietly—and confidence is ebbing.

Job gains are increasingly narrow, centered in healthcare and hospitality. Retail, government, and staffing firms are all shedding jobs. Federal payrolls alone have dropped by 59,000 so far this year. Manufacturing has lost momentum, with the ISM showing sub-50 readings across new orders, employment, and production. Tariffs are complicating cost structures and raising policy risk, making it harder for firms to plan, invest, or pass along higher costs.

Consumer spending, which was front-loaded ahead of tariff hikes in Q1, is now normalizing. Personal consumption expenditures rose just 0.2% in April, entirely on services. Spending on goods declined, led by durables like autos and recreational equipment. Light vehicle sales fell to a 15.2 million unit annual pace in May, down from 15.6 million in March, as affordability constraints and higher insurance costs took their toll. The auto sector is contending with high interest rates, rising delinquency rates, and bloated inventories.

Consumer sentiment remains fragile. The University of Michigan’s final reading for May edged up to 52.2, effectively unchanged from April and still hovering near recessionary lows. The Conference Board’s Consumer Confidence Index rebounded to 98.0 from 85.7 in April but remains well below its historical average. Encouragingly, both surveys pointed to improved perceptions of income growth and durable goods buying conditions—early signs that easing trade tensions may be lifting consumer spirits at the margin.

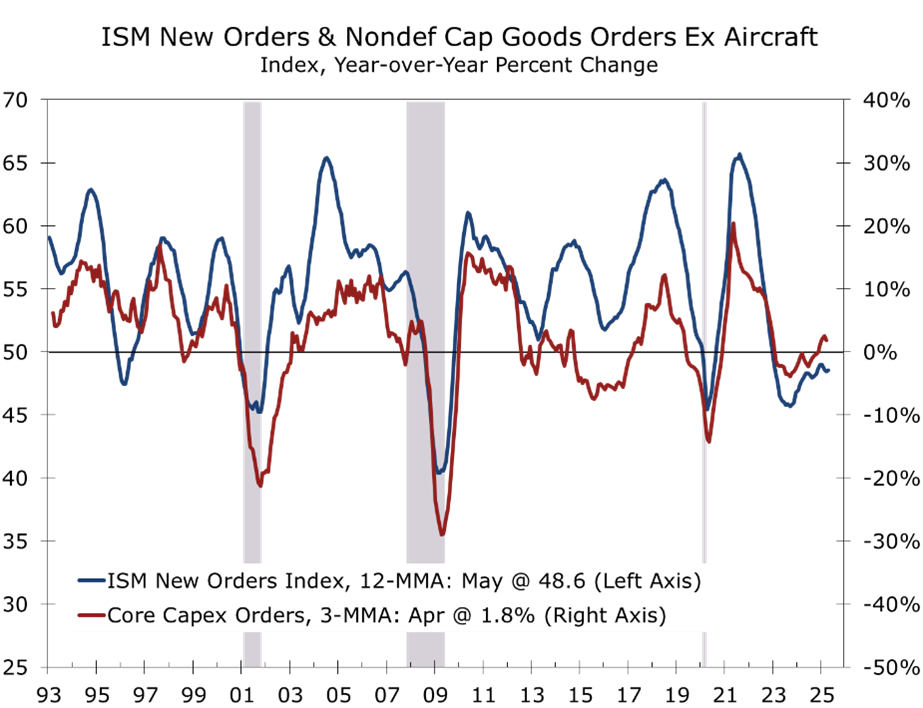

Factory orders rose 0.7% in April, driven by gains in defense and non-durable goods. But core capital goods orders—a key proxy for private business investment—were flat, reinforcing the narrative of cautious corporate sentiment amid ongoing policy uncertainty.

Bottom Line: the economy is not breaking down, but it is stalling in places. Consumers are more selective. Businesses are conserving cash. Trade frictions, tighter credit, and unpredictable policy signals are weighing on decision-making. With inflation pressures easing and tariffs retreating, conditions are in place for stabilization—but confidence remains brittle, and forward momentum uneven

Tariffs as a Taxing Distortion

The inflationary impact of tariffs remains hotly debated, but the data increasingly support a more nuanced conclusion. Tariffs are a tax and are not broadly inflationary in the monetary sense—they do not expand the money supply—but they do introduce costly distortions. They act as a tax on trade: shifting relative prices, rerouting supply chains, and redirecting household and business spending. This dynamic tends to reduce efficiency, compress margins and suppress real consumption elsewhere in the economy.

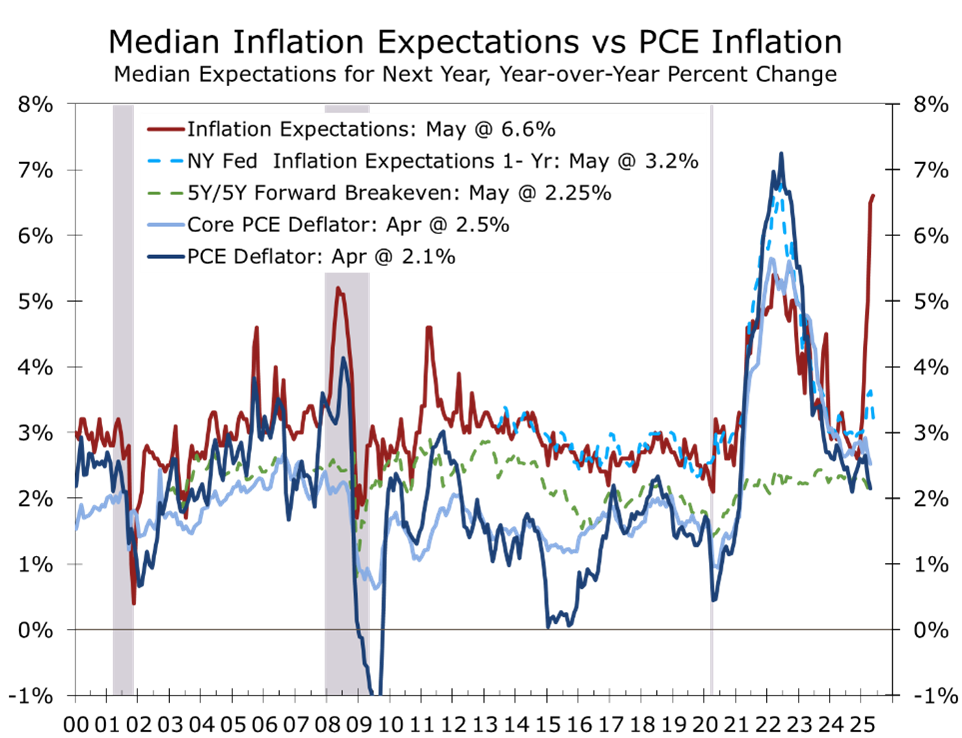

April’s PCE report confirmed that overall price pressures remain contained. Headline inflation rose just 0.1%, bringing the year-over-year rate to 2.1%, while core PCE eased to 2.5%. Goods prices fell slightly for the month—down 0.1%, driven by declines in grocery and gasoline prices—while services inflation was muted at 0.1%. Supercore services (excluding housing and energy) were flat. Importantly, the sharp tariff-induced front-loading seen in March reversed in April, with durable goods spending slipping—especially in motor vehicles and recreational equipment. The May CPI and PPI also came in below expectations, with both the headline and core CPI rising just 0.1%.

The latest Survey of Consumer Expectations from the Federal Reserve Bank of New York reinforces this picture. Short-, medium-, and long-term inflation expectations all declined in May. One-year-ahead expectations fell 0.4 points to 3.2%, while five-year expectations eased to 2.6%—close to the Fed’s 2% long-run target. Inflation uncertainty also decreased. This suggests that despite persistent rhetoric around rising prices, most households are not yet seeing evidence of sustained, broad-based inflation.

Still, businesses are clearly feeling the pinch. Most are not passing costs along to consumers—at least not directly. Instead, they’re eating the difference. Margins are tightening. Visibility has worsened. Hiring freezes, investment deferrals, and cost-cutting initiatives are becoming commonplace. Many firms now view tariffs as a tax hike they must absorb, especially as price increases risk political backlash. The optics matter: President Trump has repeatedly signaled willingness to “name and shame” companies perceived to be exploiting the inflation narrative.

Treasury Secretary Scott Bessent has defended the tariffs as “surgical and strategic,” aimed at rebalancing supply chains without stoking a consumer price spiral. Nonetheless, research from the Yale Budget Lab warns that tariffs could lift the PCE index by 0.5 percentage points by year-end—an appreciable drag, even if not an inflationary spiral. Meanwhile, former Treasury Secretary Larry Summers has warned of “stagflation-lite”: sectoral bottlenecks and price stickiness amid slowing growth. These scenarios increasingly look like worst-case outcomes.

The inflation conversation is now as much about perception and policy as actual price levels. Tariffs are acting as a brake—not an accelerator—on discretionary spending. The 2022-2023 inflation shock was monetary, as the Fed accommodated the humongous expansion of federal spending. Today’s inflationary pressures are fiscal, regulatory, and geopolitical and will likely prove temporary as long as the Fed does not accommodate them.

The Fed remains appropriately cautious. The path forward hinges not just on prices, but on how tariffs reshape behavior. For now, inflation expectations remain anchored—but sentiment is fragile, and the supply chain chessboard is still in motion.

Manufacturing’s Mixed Signals

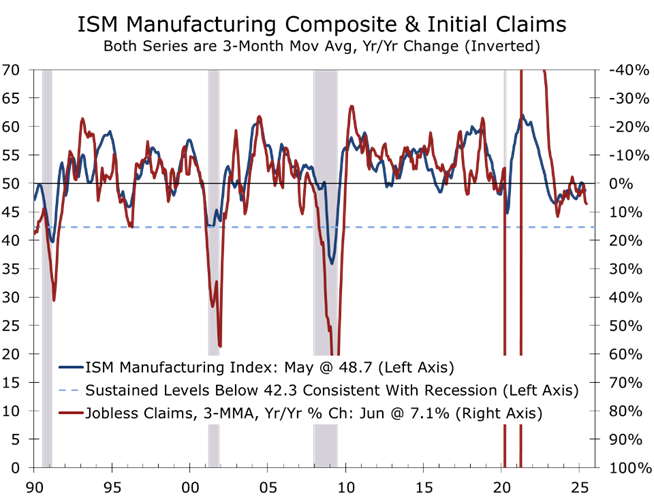

The ISM Manufacturing Index (PMI) fell to 48.5 in May, marking the third consecutive month of contraction after two months of expansion earlier in the year. Still, there are tentative signs of stabilization. New orders edged up to 47.6, while customer inventories remained lean at 44.7, suggesting firms are not overstocked and may soon need to restock. Businesses also appear less inclined to cut headcount outright, with the employment index rising slightly to 46.8.

Production remains weak, with the production index holding at 45.4, while trade-sensitive components remain deeply depressed—new export orders dropped to 43.1, among the lowest readings since the early months of the COVID-19 downturn. But the sector isn’t cratering—it’s adjusting.

Order backlogs climbed 3.4 points to 47.1, signaling that unfilled demand is beginning to accumulate. Rising backlogs are typically a precursor to renewed capital spending and hiring. For now, however, businesses are in defensive mode—preserving capital, managing inventories, and delaying expansion until policy clarity improves. The Q1 activity boost from tariff-driven front-loading has run its course.

The persistent trade turmoil has also reignited debate over the importance of U.S. manufacturing. A surprising number of academic papers have questioned whether manufacturing is even necessary in a modern service-based economy.

We find such arguments misguided and surprisingly arrogant. Manufacturing remains indispensable—especially in an era of strategic competition and fragile supply chains. Moreover, manufacturing jobs tend to be among the best-paying opportunities in the geography where new plants are opening (mostly in smaller cities and rural parts of the South, Midwest and Mountain West), particularly for workers without a four-year degree.

Though manufacturing represents just 10.3% of GDP, it typically contributes two-thirds of the swing in GDP during recessions and recoveries. That disproportionate cyclical influence is why the Fed and most forecasters place such weight on ISM Manufacturing data.

Alongside weekly initial unemployment claims, the PMI is considered a key early indicator for the overall economy. The PMI has now been in contraction territory—below 50—in 29 of the past 31 months, dating back to the 2022 slowdown. Still, May’s reading of 48.5 remains well above the critical threshold of 42.3, which historically, over time, aligns with outright recession. For now, the index is consistent with modest GDP growth of about 1.7%—weak, but still positive. That pace is slightly below the economy’s long-run potential, implying a modest rise in the unemployment rate. So far, however, unemployment claims have only risen modestly, reflecting the continued reluctance of businesses to let workers go amidst unusually slow labor force growth.

Global Flashpoints, Fragile Truces

Geopolitical risks continue to hover over the global economy. Kyiv’s audacious Operation Spiderweb—a long-range drone strike campaign against deep-inland Russian airbases—may mark a strategic turning point in the Ukraine war. Dozens of strategic bombers were damaged or destroyed, including nuclear-capable Tu-95s and early warning aircraft, inflicting billions in losses on the Russian Air Force. The precision and depth of the strikes stunned observers and undermined the credibility of Russia’s air defense network, particularly given the domestically-built nature of Ukraine’s drones and the asymmetric return on investment—some missions costing less than an iPhone. The campaign has also amplified doubts about Russia’s second-strike deterrent and exposed the vulnerability of high-value targets across its vast geography.

Even as the battlefield tilts toward stasis, the Kremlin’s ambitions remain expansive. A recently released Ukrainian intelligence assessment claims Russia intends to seize over 55% of Ukrainian territory by the end of 2026, including all of Donbas, Zaporizhzhia, Mykolaiv, and Odesa—denying Ukraine access to the Black Sea. The operational map, shown to U.S. officials, outlines a phased campaign that would require Russia to capture nine unoccupied oblast capitals and sustain a rate of territorial gains far beyond its demonstrated capacity.

Markets, for now, remain largely unshaken. But energy traders and defense analysts are watching closely. Russia’s ongoing efforts to cut off Ukrainian access to ports and conduct information warfare within NATO states suggest that risks are growing, not fading.

Talks between the United States and Iran over a potential nuclear agreement—aimed at limiting or prohibiting uranium enrichment and preventing Iran from developing a nuclear weapon—appear to be faltering. The risk of preemptive action by Israel, and possibly the United States, against Iranian nuclear research and enrichment facilities has increased. Any such strike would likely be highly destabilizing. Unlike Israel’s limited October 26th attacks on Iranian air defense systems and drone production infrastructure, Tehran would likely mount a far more robust response. There are growing concerns that Russia and China may provide Iran with intelligence support. In a sign of escalating tensions, the United States has ordered non-essential personnel to evacuate its embassy in Baghdad, citing fears of retaliatory strikes. Oil prices have responded, with WTI climbing to approximately $67 per barrel, up from $60 earlier in June.

Meanwhile, a new round of high-level U.S.-China trade negotiations is underway in London, where Treasury Secretary Scott Bessent, Commerce Secretary Howard Lutnick, and U.S. Trade Representative Jamieson Greer are meeting with Chinese Vice Premier He Lifeng. The talks follow the fragile Geneva framework established last month, which briefly eased tensions in equity and commodity markets. Implementation, however, has been uneven—particularly on critical exports such as rare earth elements. China’s abrupt suspension of rare earth shipments in April disrupted global supply chains and alarmed manufacturers reliant on Chinese inputs. A tentative agreement has been reached to lower tariffs to 55% on Chinese goods and 10% on U.S. exports to China. In addition, China will allow U.S. firms to purchase rare earths for at least six months.

The presence of Lutnick, who oversees export controls, highlights how central supply chains and dual-use technologies have become to the broader decoupling narrative. While both sides continue to signal optimism, sticking points remain over fentanyl, industrial espionage, Taiwan, and forced technology transfer. The stakes are high. Failure to maintain even a temporary truce risks reigniting a full-scale economic cold war—with cascading consequences for inflation, global investment, and energy security.

Looking Ahead: A Step Back from the Cliff

Markets have stabilized, and the economy is no longer teetering at the cliff’s edge. The S&P 500 has recovered most of its early-year losses. Headline inflation is easing. GDP forecast for the current quarter have been raised sharply, with our own estimate currently at a 3.6% pace. Underlying demand is softer, however, and appears to be running at around a 1.7% pace. The risks of recession have receded. But all is not smooth sailing. Business sentiment is cautious. Labor data is softening. Tariff uncertainty remains a pervasive drag.

The Fed is rightly cautious. Markets still anticipate two quarter-point cuts, with the first likely in September. The path ahead depends on clarity in inflation metrics, global trade conditions, the federal budget and geopolitical risks-all of which remain open questions. Our take is that the U.S. is past peak tariff turmoil and that inflation will heat up at the producer level this summer but less so at the consumer level, which means a further squeeze on profit margins and further slowing in hiring and capital spending.

Risks remain elevated, but worst-case outcomes will likely be avoided. Growth should improve in 2026, particularly in the second half of the year. We see a total of three quarter-point cuts in the federal funds rate by spring 2026. Home sales and new home construction should provide a modest boost to growth next year and capital spending should rebound once we have more clarity on taxes and trade.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

June 10, 2025

Mark Vitner, Chief Economist

704-458-4000