Inventory Drawdowns Slash Q1 Output

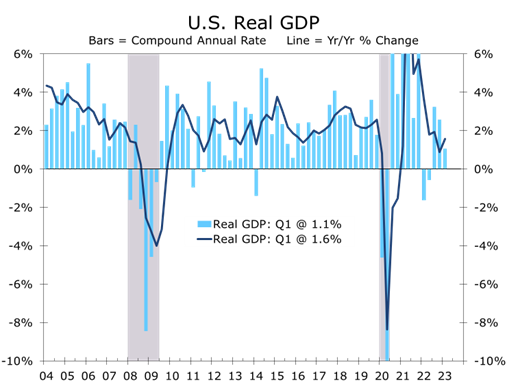

- Real GDP rose at a 1.1% annual rate, coming in a full percentage point below our forecast.

- Real personal consumption rose at a stout 3.7% annual rate. Spending started the quarter red hot, however, and ended the quarter ice cold.

- Business fixed investment fell at a 0.4% annual rate, with equipment outlays plummeting at a 7.3% pace.

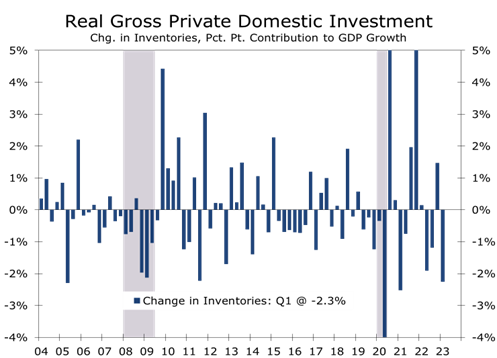

- Inventory drawdowns were much larger than expected, particularly among wholesales and manufacturers.

- Government spending was an upside surprise, with federal nondefense outlays surging at a 10.3% pace.

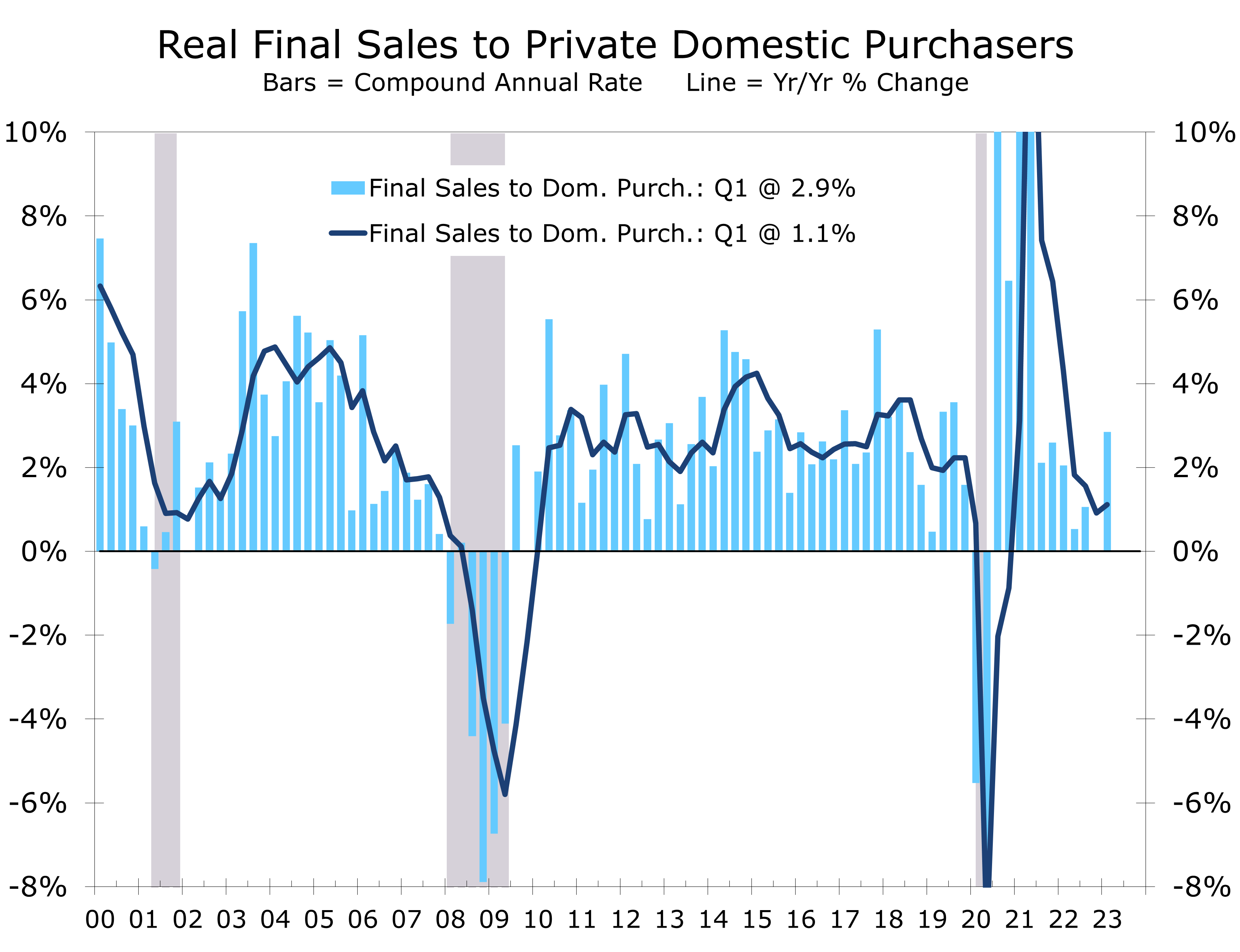

- Real final sales to domestic purchasers, or private final demand, rose at 3.2% pace, precisely in line with expectations.

- There is huge mismatch between output and employment, with employers adding more than a million jobs in Q1, while output climbed at just a 1.1% pace.

The advance report on first quarter real GDP came in on the softish side. Real GDP grew at just a 1.1% annual rate, as continued strength in consumer spending was largely offset by a big drawdown in inventories.

The underlying details of first quarter GDP were generally more positive. The large drawdown in inventories sliced 2.3 percentage points off overall growth. Inventories have been unusually volatile since the pandemic began. Much of the reduction in Q1 occurred at wholesalers and manufacturers. Real final sales to private domestic purchasers, which is our preferred measure of final demand, rose at a 2.9% annual rate in Q1 and is now up just 1.4% year-to-year.

While there is undoubtedly still more work to be done to bring inventories back in line with demand, particularly at retailers, a significant portion of this correction now appears to be behind us. The drawdown in inventories has weighed on industrial production in recent months.

The Fed has achieved a soft landing but needs to maintain it to pull inflation back to target.

Economic growth now appears to have slowed to a pace consistent with a soft landing. Getting there, however, was the easy part. With the core PCE deflator still up 4.9% over the past year, the Fed will likely need to hold growth at its current pace or less for at least a year to bring inflation down close enough to its 2% target that they can begin to ease.

Real personal consumption grew at a 3.7% annual rate, marking the strongest quarterly gain for consumer spending since the second quarter of 2021, when the last round of stimulus checks sent spending into overdrive. Transfer payments also helped support Q1 spending, as a big rise in social security payments fueled a surge in leisure and travel at the start of the year. Light vehicle sales were another bright spot. Spending on big-ticket items surged at a 16.9% annual rate, the strongest rise since the first quarter of 2021. Spending on nondurables rose at a 0.9% pace.

The spending spree lost momentum in February and March, however, and personal consumption will likely rise only marginally in Q2 as consumers have increasingly been tapping credit cards to support spending. Technical factors will also make it harder for spending to add to GDP growth in Q2. Unseasonably mild weather likely pulled some spending forward into Q1, which will weigh on spending this spring.

Consumer spending appears to be losing momentum, as consumers have increasingly been tapping credit cards to support spending.

The slide in inventories subtracted 2.3 percentage points off first quarter GDP growth. Wholesalers and manufacturers accounted for most of the drop, with a jump in shipments of commercial aircraft helping clear out inventories at aircraft manufacturers.

Sustaining a soft landing is difficult, as once economic growth slows that deceleration tends to become self-reinforcing. We are already seeing considerable knock-on effects as a growing number of businesses announce spending cuts and layoffs. Business fixed investment slowed to a 0.7% pace in Q1, with equipment purchases declining at a 7.3% pace. That drop was offset by another large gain in nonresidential structures, much of which appears to be fueled by the Inflation Reduction Act and CHIPs act.

Sustaining a soft landing is difficult, as the deceleration tends to become self-reinforcing.

Government outlays rose strongly in Q1, with federal outlays rising at a 7.8% clip. Defense spending rose at a 5.9% pace, while nondefense outlays surged 10.3%, marking their second consecutive double-digit gain. The surge in federal outlays is at the center of the current battle over the debt ceiling. We suspect some agreement will be reached, restraining nondefense outlays later this year and into 2024. Constraints on federal spending might make the soft landing a little softer but also make the Fed’s job a little easier, possibly even pulling interest rate cuts up a quarter or two.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.