Consumers Get Another Pass on Tariffs

- Headline CPI rose 0.3% in June, up from 0.1% in May. Core CPI advanced 0.2%, consistent with consensus expectations.

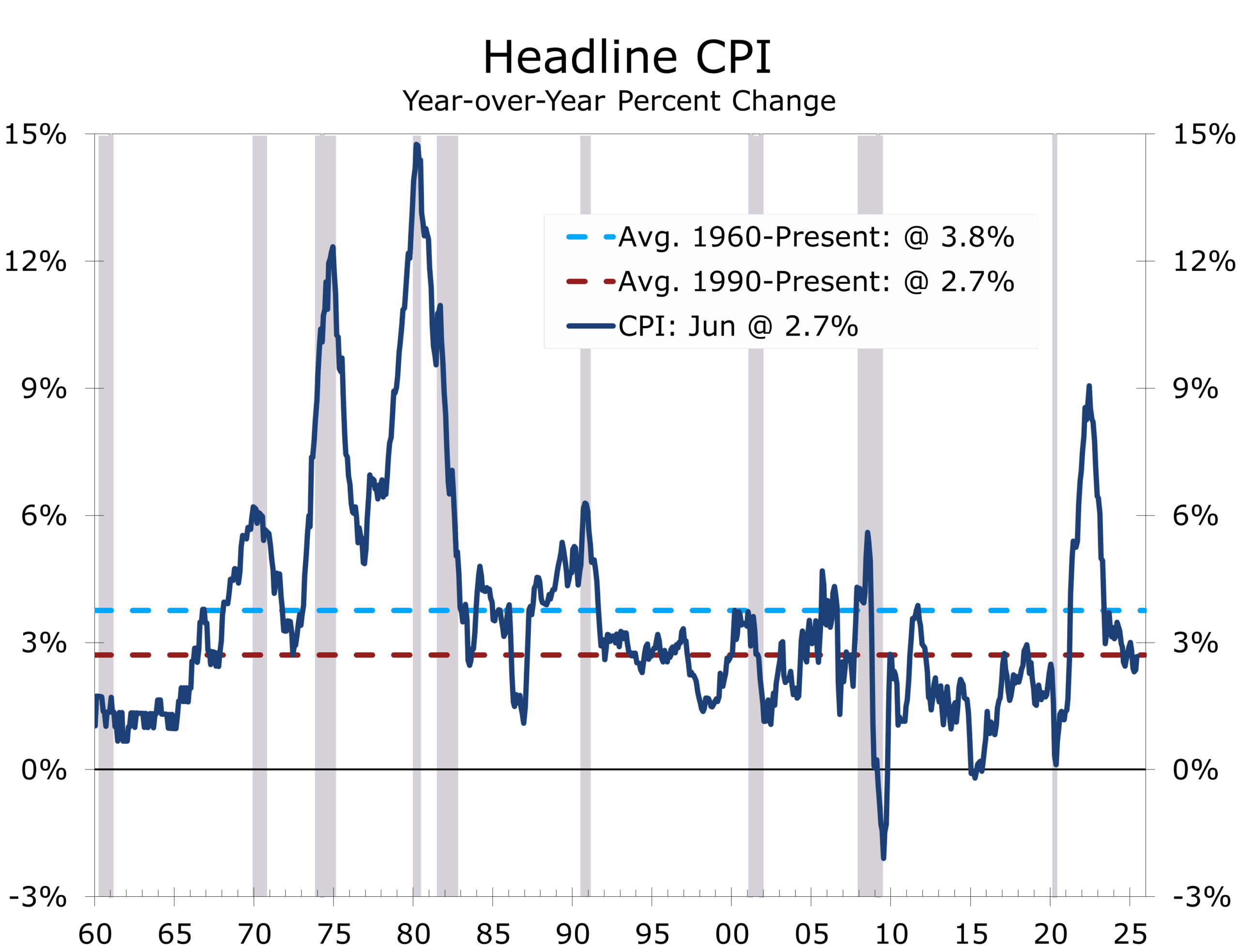

- Year-over-year headline inflation ticked up to 2.7%, while core CPI edged up to 2.9%.

- Energy prices bounced 0.9% in June; food prices also rose 0.3%.

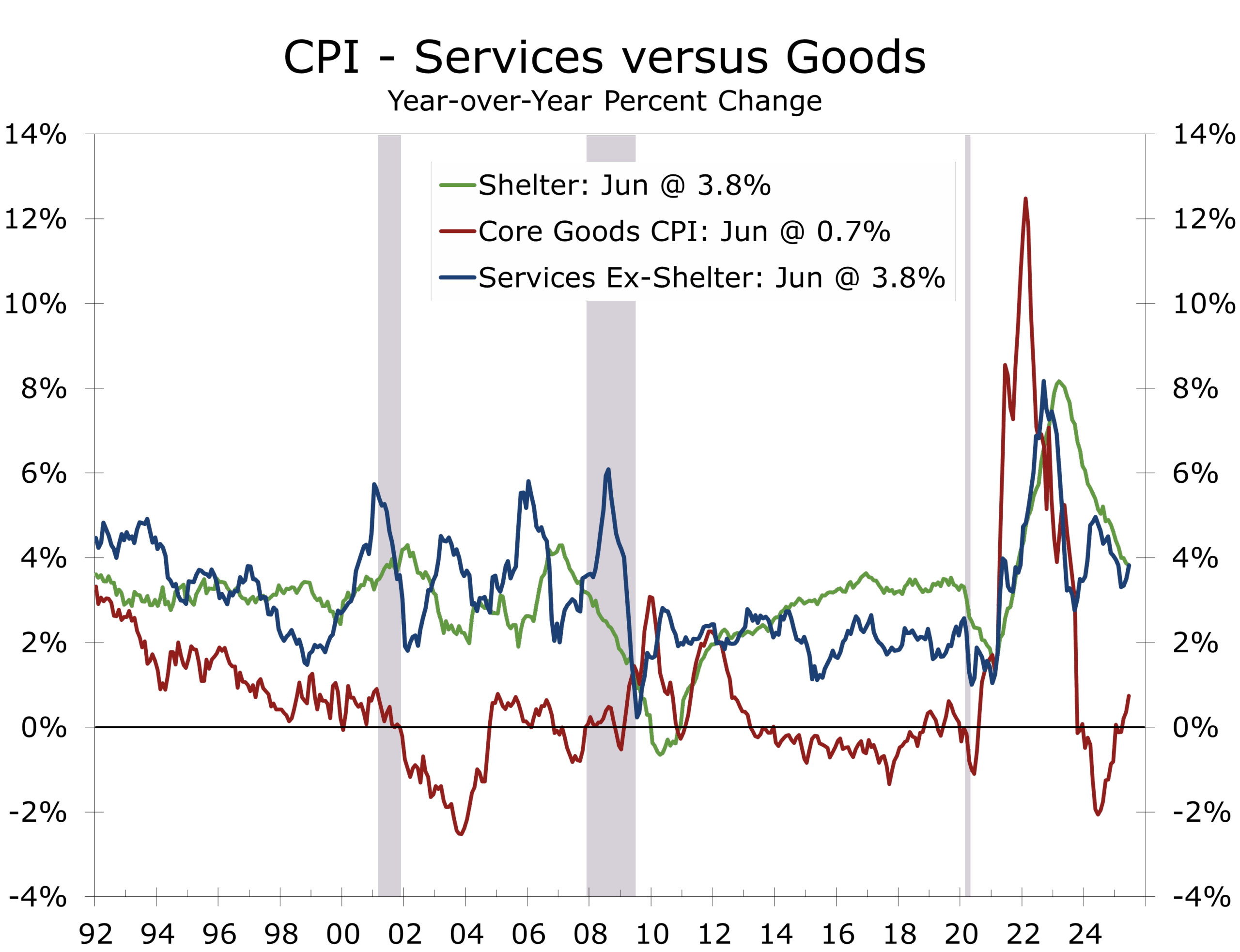

- Shelter inflation eased, with OER up 0.3% and rent up 0.2%, reflecting ongoing housing softness.

- Core goods disinflation persisted: used vehicle prices fell 0.7%, new vehicles -0.3%. Apparel rose just 0.4% and home furnishings rose 1.0%, with appliance prices up 1.9%.

- Real average hourly earnings declined 0.1% in June, while real weekly earnings fell 0.4%, as inflation outpaced wage gains and the average workweek shortened.

- The June CPI report keeps the door open for a September Fed rate cut. Prices rose largely in line with expectation and there is no evidence of broad passthrough of tariffs. Pressures are evident in a few areas, most notably washing machines, toys, coffee, men’s shirts and women’s dresses. There are also some offsets, however, as consumers are cutting back on big-ticket purchases and leisure and travel.

Inflation Eases Where It Matters Most

The Consumer Price Index came in firmer than May’s reading, but still well within the Federal Reserve’s comfort zone. Headline CPI rose 0.3%, driven largely by higher energy and food costs. Core CPI rose 0.2%, keeping the three-month annualized pace at a modest 1.9%.

Year-over-year, headline CPI rose to 2.7% and core to 2.9%. With base effects fading, inflationary momentum remains subdued—especially in categories that previously drove price spikes. Most encouragingly, core services outside of housing have shown sustained improvement over several months.

Base effects pushed up year-over-year inflation, but the underlying trend is still decelerating.

Energy prices posted a broad rebound in June, rising 0.9% following May’s 1.0% decline. Gasoline prices rose 1.0%, natural gas increased 0.5%, and electricity prices jumped 1.0%. However, base effects continue to hold the year-over-year energy index down 0.8%, with gasoline still down 8.3% over the past 12 months. Energy inflation may reemerge this summer if global oil supplies tighten further—but so far, the inflation pass-through has been modest.

While 2.7% inflation remains above the Fed’s 2% target, it aligns with the 35-year historical average. The underlying trend continues to decelerate, driven by easing wage pressures and softer demand for discretionary services.

Food prices rose 0.3% in June, matching May’s gain. Grocery store prices climbed 0.3%, while food away from home rose 0.4%. Within grocery categories, nonalcoholic beverages jumped 1.4%, led by a 2.2% increase in coffee. Fruits and vegetables also posted solid gains (+0.9%), though egg prices plummeted 7.4%, offering some relief. Dining costs continue to outpace grocery inflation, with full-service meals up 0.5% and limited-service up 0.2%.

The housing slowdown is easing pressure on household budgets and services inflation.

Shelter costs, which carry outsized weight in the CPI, are finally showing clearer signs of slowing. Owners’ equivalent rent rose 0.3% and primary rent increased 0.2%—both down slightly from earlier this year. Lodging away from home declined 2.9%, contributing to the broad deceleration. A continued influx of multifamily supply and slowing lease renewals suggest further cooling ahead, although BLS methodology lags real-time rental data by several quarters.

Despite persistent tariff headlines, core goods prices continued to decline. Used vehicles fell 0.7%, new vehicles 0.3%. Apparel, which is a small component of the CPI, rose 0.4%, hinting at early tariff effects, but gains remain modest. Retailers appear to be absorbing higher costs through supplier diversification, margin compression, and delayed restocking.

Tariff effects are beginning to surface in home furnishings, which rose 1.0% in June and are up 1.7% year-over-year. Major appliances led the increase, climbing 1.9% in June and 2.4% over the year, driven by washing machines, which jumped 1.8% on the month and 7.7% year-over-year. Toys and sporting goods also rose 1.8%, likely reflecting early-stage tariff pass-through.

Real average hourly earnings declined 0.1% in June, while real weekly earnings fell 0.4%, as inflation outpaced wage gains and the average workweek shortened. Despite a 1.0% year-over-year increase, the monthly setback highlights the pressure households face from high housing, insurance, and food costs. Weaker real income growth will weigh on spending, particularly for big-ticket items.

The June CPI report gives the Fed room to ease. Core inflation remains subdued, and although year-over-year rates edged higher, they’re broadly consistent with a gradual path back to 2%. Markets now assign a 70–80% chance of a September rate cut, as the Fed grows more concerned about overtightening into a slowing labor market that’s softening even more quickly beneath the surface.

Still, tariff risks are building. While consumer prices have not yet reflected the full impact, producer prices are firming, and a weaker dollar is pushing import costs higher. A quicker pass-through could reignite inflation, but likely unevenly across sectors given softer demand.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

July 15, 2025

Mark Vitner, Chief Economist

(704) 458-4000