The Fed Continues to Look Beyond the Headlines

- The FOMC held the fed funds target range at 5.25%-5.50% at its May meeting and remains cautiously optimistic about inflation.

- The Committee took note of the recent lack of progress toward its 2% inflation objective but still sees the broader economy, labor market, and inflation moving into better balance.

- The Committee also announced a more substantial slowdown in its balance sheet drawdown, or QT, than was expected.

- The winding down of QT is more geared toward maintaining market stability than providing economic relief.

- Powell said it was ‘unlikely’ the Fed would need to raise interest rates, stating that monetary policy is tight enough.

- Powell was also unusually frank and dismissive of any risks of stagflation, pointing to stronger private final domestic demand.

- We are still looking for the Fed to ease this year but now look for just two quarter-point cuts (September and December) followed by two more in early 2025. We expect job growth to slow later this spring and look for inflation to moderate in the second half of this year.

As expected, the Fed held its federal funds target range unchanged at 5.25%-5.50% at its May 1 FOMC meeting. The financial markets were prepared for a more hawkish take on inflation, given the string of disappointing inflation reports during the first quarter. The Fed acknowledged that progress at reducing inflation has slowed but still sees the economy on track for more modest economic growth and lower inflation.

The Fed’s policy statement and Powell’s press conference emphasized that they believe the economy is moving toward better balance. While job growth was clearly stronger than expected in Q1, with employers adding an average of 276,000 jobs a month, Powell sees that strength balanced by rising prime-age labor force participation and increased immigration.

The latest JOLTS numbers add credence to this notion, with job openings and the quit rate both falling notably in March. The narrowing of the jobs-to-workers gap should allow wages to ease further.

There has been a lack of further progress toward the Committee’s 2 percent inflation objective.

The biggest change to the Fed’s statement was the acknowledgement that progress on reducing inflation came up short in the first quarter. Powell seemed remarkably unfazed, noting long-term inflation expectations remain well anchored and reaffirming that monetary policy remains appropriately tight.

We see Powell’s assessment as appropriate. While inflation came in higher than expected in the first quarter, much of the surprise was at the start of the quarter. There has also been a tendency for inflation to surprise to the upside in the first half of the year and then moderate during the second half. This pattern has been even greater in the aftermath of the pandemic.

Jay Powell got a little animated when asked about the prospect of a return of stagflation, noting that he did not see the ‘Stag’ of the ‘-Flation’. The source of much of the stagflation talk appears to have come from the weaker than expected Q1 GDP report, which showed real GDP growth slowing from a 3.4% pace in Q4 2023 to a 1.6% pace. The Fed’s preferred inflation measure, the core PCE deflator, accelerated to a 3.7% annual rate in Q1 from a 2.0% the prior quarter.

I don’t see the ‘stag’ or the ‘-Flation’. Final demand remains strong in the private sector.

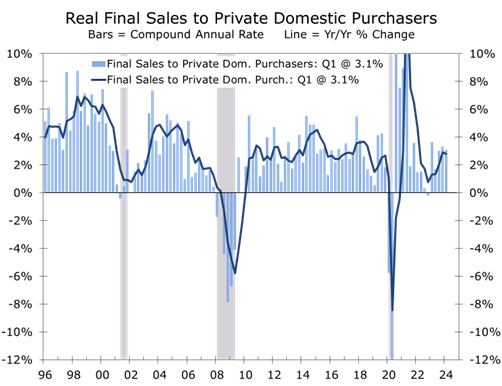

Powell downplayed the recent slowdown in GDP growth, attributing it to a decrease in net exports and temporary federal spending cuts. Real Final Sales to Domestic Purchasers, which excludes inventories, government spending, and net exports; grew at a 3.1% pace in Q1, consistent with the second half of last year. This measure provides a better gauge of the parts of the economy most influenced by monetary policy.

With no ‘stag’, there is even less need to cut interest rates. Powell noted that the recent strength in consumer spending is being supported by improving supply conditions. Part of that supply is a rising tide of less expensive imports.

While inflation is still too high for the Fed to entertain any thoughts of cutting interest rates, we are still looking for two quarter-point rate cuts this year. The first cut should come in September, followed by a second in December. By then, we feel core inflation will have decelerated to around a 2.5% pace, which should be more than enough progress for the Fed to begin to normalize interest rates.

Recent months show no further progress toward the 2 percent inflation objective.

The big surprise was that the Fed announced a more substantial winddown of its balance sheet reduction program, or QT. Beginning in June, the Committee will slow the pace of decline in its securities holdings by reducing monthly redemptions from $60 billion to $25 billion. Redemptions of agency and mortgage-back securities will remain at $35 billion a month. The move is aimed more at maintaining financial market stability than providing interest rate relief.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

May 1, 2024

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000