One of the things you can almost always count on with the monthly employment report is plenty of surprises. The November report did not let us down on that front. Nonfarm payrolls rose by a much hotter than expected 263,000 jobs in November, versus a consensus estimate of around 190,000 jobs. Expectations had been whittled away all week, with weaker reports from many of the high-frequency series, the monthly ADP report and employment components in both the consumer confidence and ISM manufacturing surveys.

The Labor Market is Proving Resilient

- Nonfarm employment easily topped expectations in November, with employers adding 263,000 jobs.

- Hiring continues to be led by industries that suffered the largest losses during the pandemic and reopened slowly. Leisure and hospitality, health care and government all posted outsized job gains this past month.

- November’s 263,000-job gain is only modestly below the 282,000 jobs added on average during the prior 3 months. Employers have added an average of 392,000 jobs a month this year, down from 562,000 a month in 2021.

- The unemployment rate was unchanged at 3.7%. Both the labor force participation rate and employment-population ratio fell 0.1 percentage point.

- Average hourly earnings jumped 0.6% in November, nearly twice what was expected, and is now up 5.1% year-to-year.

The key initial takeaway from November’s stronger job gain is the Fed has more work to do. While that is certainly understandable, we would be remiss not to caution folks of the oft repeated maxim that monetary policy works with a long and variable lag. Moreover, labor market conditions are a lagging economic indicator and have become even more so in recent years, as employment in the most cyclical parts of the economy has become a smaller part of the employment base. We still see plenty of evidence that employment conditions are losing momentum, particularly in the more cyclical parts of the economy.

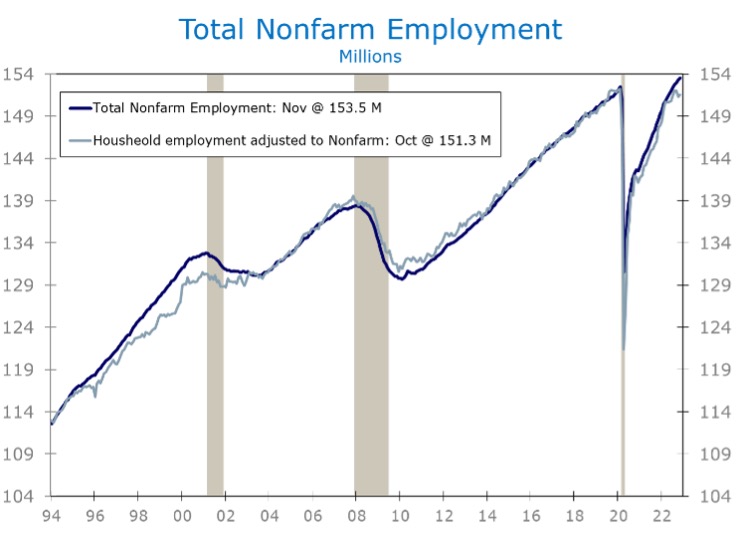

Household employment typically tops out before nonfarm employment. While this series is more volatile, the BLS has made it somewhat easier to compare it to the more widely followed nonfarm series. On a nonfarm employment adjusted basis, household employment rose by 228,000 in November, after tumbling by 761,000 the prior month. While it is too early to call a top, the household series looks like what we saw at previous cyclical peaks.

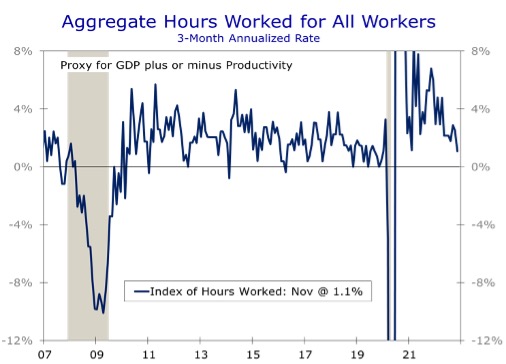

Another series we follow closely is aggregate hours worked, which is a good proxy for real GDP growth. Aggregate hours worked fell 0.2% in November and have risen at just a 1.1% over the past three months. That pace is still consistent with positive real GDP growth, but at a notably slower pace. Aggregate hours worked rose at 2.9% annual rate during the three months ended in September, when real GDP subsequently grew at a 2.9% pace.

There are several other aspects of the employment report pointing toward slower growth. Hiring at temporary staffing companies, a reliable leading indicator for future job growth, declined by 17,200 jobs in November, following a 6,100-job loss the prior month. There was also far less hiring at retailers and of warehouse and delivery workers than usual this time of year, leading to seasonally adjusted job losses.

The key takeaway from November’s stronger job gain is the Fed has more work to do.

Even after taking all the weaker aspects of November’s employment report into account, a recession now appears to be a more distant prospect than it was a month ago. That is good news for the Fed, which has made it clear they need to push short-term interest rates higher to bring inflation back down to their 2% target. We expect a half point hike in December and look for another half point hike in early February, followed by quarter-point hikes at the next few meetings after that.

While a recession is further off, economic growth will slow further. We still see a better than even chance of a downturn beginning around the middle of 2023. Soft landings are hard to pull off and even harder to maintain.

The bulk of November’s job growth came from parts of the economy where employment was hit particularly hard during the pandemic and hiring has been slow to recover. Leisure and hospitality added 88,000 jobs in November, 62,000 of which were at restaurants and bars. Employment in the sector remains 980,000 jobs below its pre-pandemic peak.

Hospitals, doctors’ offices, and dentists’ offices all suffered huge job losses at the start of the pandemic, as did nursing homes, day care centers and social service providers. All have been slow to rehire but have seen hiring pick up more recently. Health care providers added 45,000 jobs in November and have added an average of 47,000 jobs a month in 2022. The sector added an average of just 9,000 jobs a month in 2021. Employment in social services increased by 23,000 in November and has added an average of 18,000 jobs a month this year.

Considerable attention has been focused on the surge of layoffs at well-known tech firms. So far, those cutbacks have not shown up in the official data. Professional and technical services added 27,900 jobs in November and another 19,000 jobs were added in the information sector. The cutbacks are real, however, and we expect them to become apparent in coming months. We are already seeing spillover into other parts of the economy in many tech-centric areas.

November’s data may prove to be a harbinger of what we will see in coming months. Industries that were slower to add back staff following the pandemic still have a great deal of hiring to do before they are fully staffed. A visit to just about any restaurant will attest to this. At the same time, the pain in the tech and housing sectors is just beginning and those cutbacks will eventually flow through to the monthly jobs data.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.