Key Takeaways from November’s ISM Services Report

-

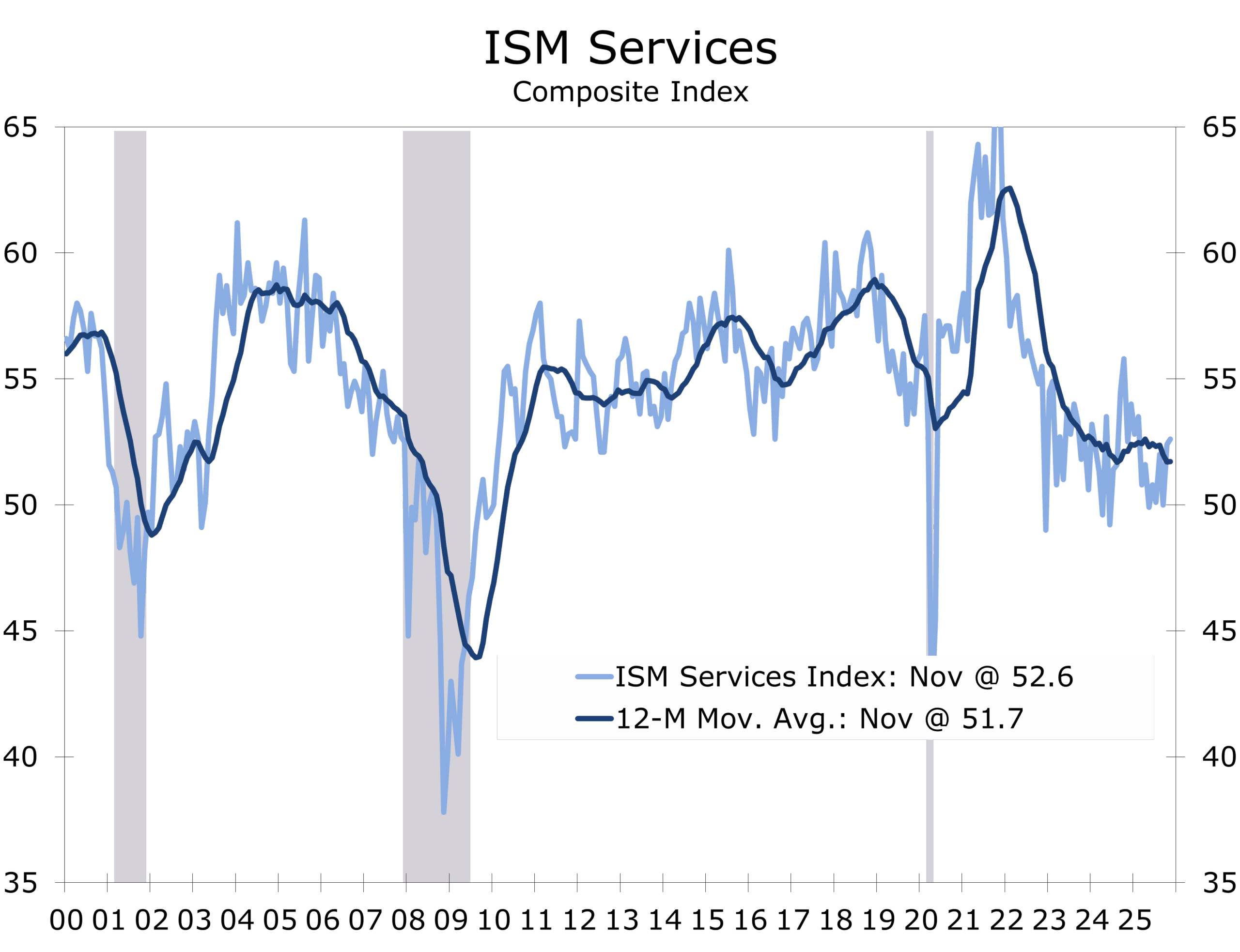

- Services PMI rose to 52.6, modestly above expectations and the 12-month average of 51.7, marking the ninth month of expansion in 2025 and implying roughly 1.3% annualized real GDP growth.

- Business Activity held at 54.5, its seventh reading above 54% this year, consistent with solid—but not spectacular—underlying demand.

- New Orders fell to 52.9 from 56.2, still above their 12-month average but clearly pointing to a softer fourth-quarter pipeline.

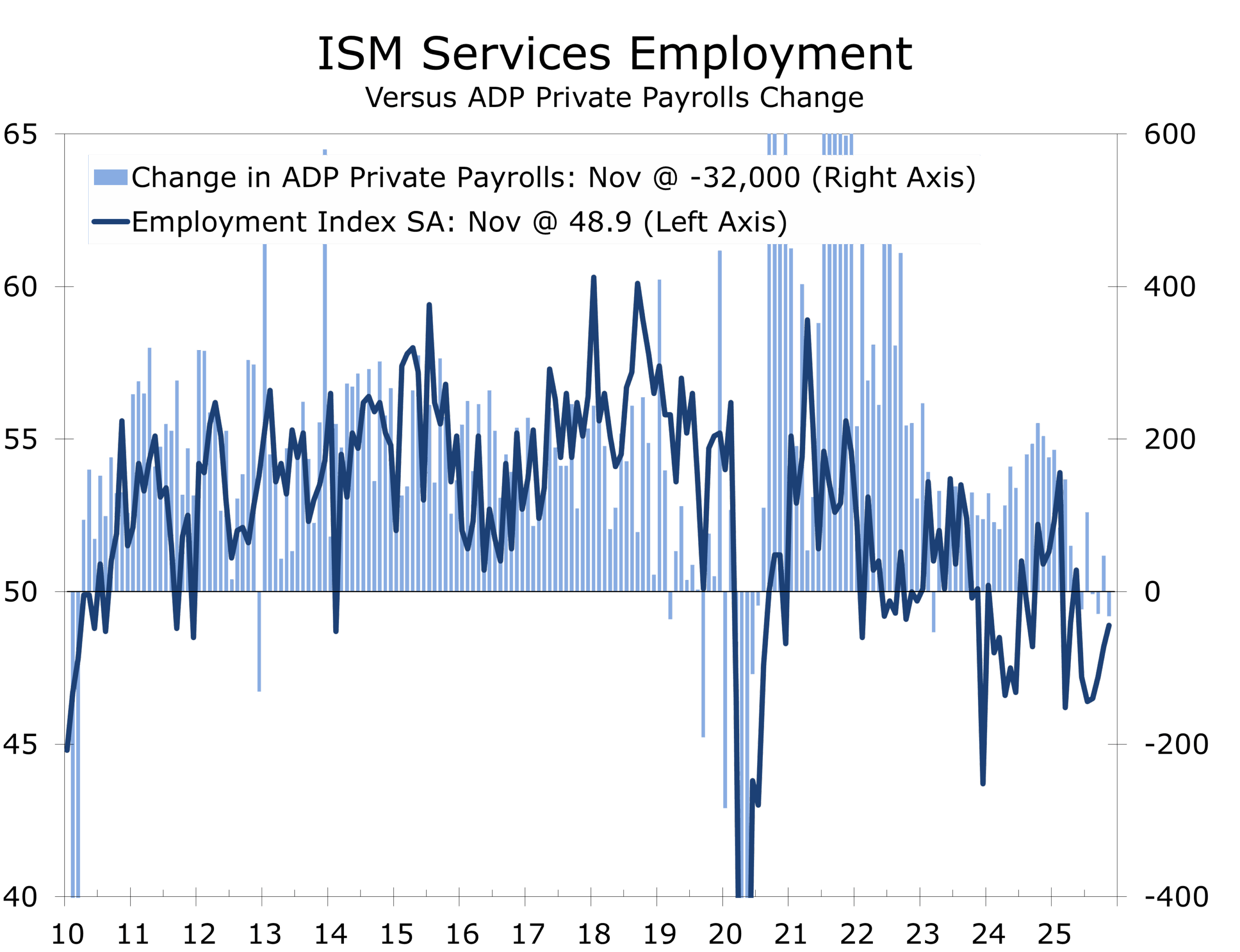

- Employment remained in contraction at 48.9, the sixth straight sub-50 reading, even as the index has edged higher since July.

- Supplier Deliveries jumped to 54.1, the highest since late 2024, reflecting slower deliveries tied to tariffs, customs delays, the government shutdown, and air-traffic disruptions.

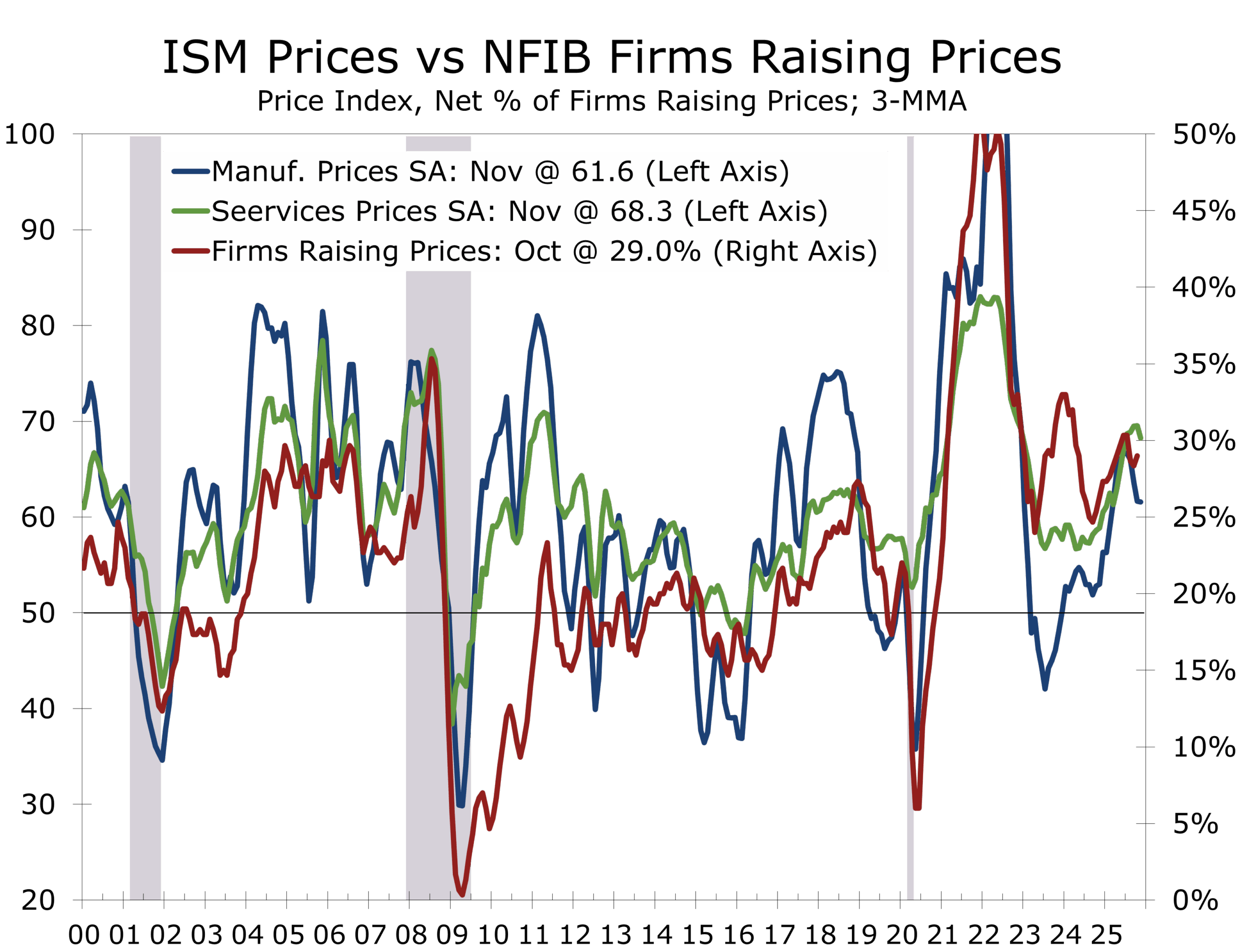

- Prices eased but stayed elevated: the Prices Index fell to 65.4, its lowest since April, but has now been above 60 for 12 straight months.

- Inventories returned to expansion at 53.4, and backlogs rebounded sharply to 49.1, the highest since February 2025, easing fears of a more abrupt slowdown.

- Breadth improved: 12 industries reported growth, while only five reported contraction.

- Overall tone: the services sector is still carrying the expansion, but the 12-month trend in the PMI has dropped more than 10 points since early 2022, underscoring a slower, narrower cycle.

Expansion Endures, Even as Underlying Currents Slow

The November ISM Services PMI® edged up to 52.6 from 52.4, modestly beating expectations and extending the services sector’s expansion for a ninth month this year. Historically, a reading above 48.6 is consistent with overall GDP growth, and November’s figure corresponds to roughly a 1.3% annualized gain in real output. The broader backdrop is less impressive. The 12-month average of the Services PMI remains stuck at 51.7, its lowest level since 2010, and more than 10 points below the 62.6 peak reached in February 2022. The expansion is intact, but the cycle has clearly downshifted from the roaring prints of the early post-pandemic period to something more akin to a late-cycle glide.

Solid activity, softer demand: Business Activity holds at 54.5 while New Orders drop 3.3 points.

Compositionally, the report reinforces that story of “steady, not strong.” The Business Activity Index held at 54.5, up a modest 0.2 point from October and above 54% for the seventh time in 2025, signaling that day-to-day output in the services sector remains in solid expansion. New Orders, however, told a cooler story. The index fell 3.3 points to 52.9. It is still in growth territory and sits nearly a point above its 12-month average, but the step-down points to a softer fourth-quarter pipeline. Respondents describe a split environment: big pharma is spending more aggressively than in the first half of the year, while other customers are pulling back or delaying commitments amid tariff uncertainty and mixed economic signals.

Backward-looking momentum is being cushioned by backlogs. The Backlog of Orders Index rose sharply to 49.1 from 40.8, its biggest monthly gain since mid-2022 and the highest reading since February 2025. Backlogs remain in mild contraction, but the rebound from very weak levels indicates that the worst of the backlog bleed may be behind us. In practice, that means firms still have enough work in the queue to buffer activity as new orders cool. New export orders remained in contraction at 48.7, the fifth straight sub-50 reading and the eighth this year, reflecting slower international demand and tariff-related frictions, even as some respondents reported a relatively strong fourth quarter in Europe.

Services Employment stayed in contraction at 48.9, the sixth straight sub-50 reading

The labor picture continues to transition from tight to merely firm. The Employment Index improved to 48.9 from 48.2, its highest reading since May but still in contraction for the sixth consecutive month. This run of sub-50 readings marks a clear shift away from the earlier era of pervasive labor shortages. Respondents noted that some firms are now “filling vacancies,” yet others still struggle to attract candidates, particularly for roles that require employees to be in the office. Employment increased in retail, accommodation and food services, wholesale trade, agriculture, health care, and utilities, but declined in mining, transportation and warehousing, management of companies and support services, public administration, construction, professional services, finance, and information.

When cross-checked against the November ADP data, which posted a decline of 32,000 private sector jobs in November, the ISM readings reinforce the conclusion that labor-market is softening is gaining momentum and broadening.

Price and cost dynamics remain one of the clearest constraints on policy. The Prices Index fell to 65.4 from 70.0, its lowest level since April and a welcome sign that the most intense pressure is easing. Yet prices have now been above 60 for 12 consecutive months, and 14 industries reported higher input costs in November, with construction the only sector reporting lower prices. Labor, software licensing, copper products, and steel were cited as up in price, while a handful of items—including gasoline, lumber, and engineered wood products—moved lower. On the parallel survey side, the S&P Global services PMI showed declines in both input and output prices, reinforcing a narrative of gradual disinflation rather than outright cost relief.

Prices are cooling at the margins, but firms continue to manage elevated cost

Inventories and inventory sentiment tell a story of cautious normalization. The Inventories Index returned to expansion at 53.4 after two months of contraction, with several respondents reporting that they are drawing down stocks after a quiet storm season or recalibrating inventories as trade deals are resolved. At the same time, the Inventory Sentiment Index stood at 54.8, indicating that many firms still view their inventories as “too high” relative to current business needs. That combination—modest inventory rebuilding alongside a persistent sense of excess—suggests that firms remain reluctant to carry much buffer and will continue to favor lean, just-in-time stock positions as long as demand remains choppy.

Supply conditions, meanwhile, have become more complicated. The Supplier Deliveries Index rose to 54.1 from 50.8, signaling slower deliveries for the 12th consecutive month and the highest reading since October 2022. A reading above 50 indicates worsening delivery performance, and respondents pointed squarely at tariffs and the federal government shutdown. Several noted items being stopped at borders or slowed by customs processing. The tragic UPS cargo plane crash on November 4 loomed in the background of the comments, a sobering reminder of the operational risks facing logistics providers as they move into the holiday shipping season.

Imports remained in mild contraction at 48.9, but the underlying narrative has shifted: rather than purely reflecting weak demand, the survey indicates that many firms are deliberately moving sourcing toward USMCA suppliers to mitigate steep tariffs on food, apparel, and electronics from Asia.

Breadth across industries improved modestly in November. Twelve out of seventeen services industries reported growth, including retail trade, arts and entertainment, accommodation and food services, wholesale trade, health care and social assistance, educational services, public administration, agriculture and related activities, finance and insurance, information, professional and technical services, and utilities. Only five industries—construction, real estate and rental and leasing, mining, management of companies and support services, and transportation and warehousing—reported contraction.

The respondent anecdotes bring this divergence to life. Retailers describe business as “strong, driven by customer traffic,” with stable pricing. Health-care systems report patient volumes leveling off, better fill rates in supply chains, less dependence on travel labor, and an overall optimistic outlook despite still-elevated costs. Construction and real-estate respondents, by contrast, highlight mortgage-rate headwinds and tariff pressures, framing the current slowdown as an “intentional pause” with margins expected to erode as competitors fight harder for fewer projects. In information and management services, tariffs, shutdown effects, and mixed macro indicators are fostering a more defensive stance heading into early 2026. Wholesale trade sits in between: respondents are bracing for margin compression as competition heats up, even as they anticipate higher lumber prices in 2026 due to reduced production.

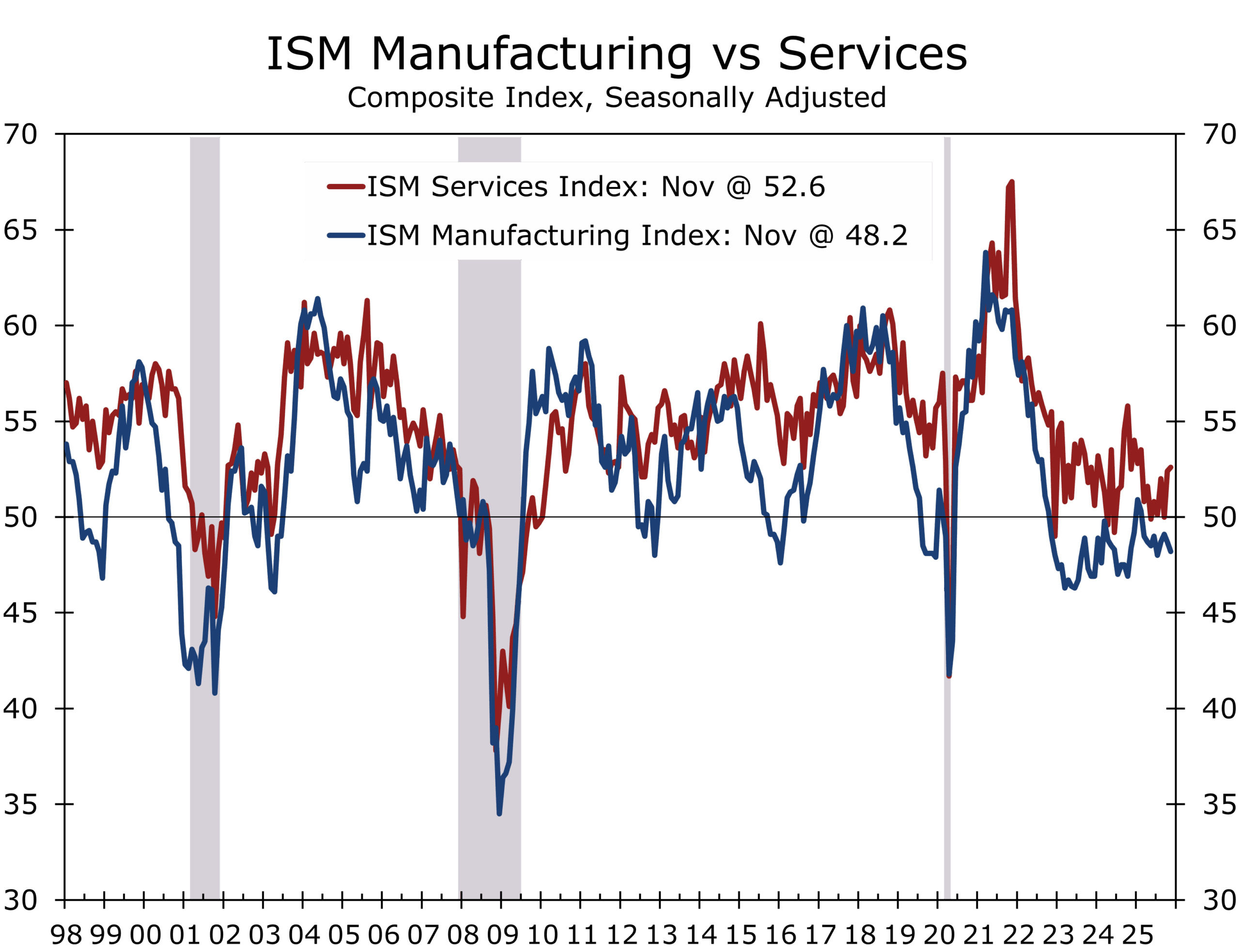

From a macro perspective, the November report underscores a two-speed U.S. economy. The services sector, with a PMI of 52.6, remains in expansion and is modestly above its 12-month average. Manufacturing, by comparison, shows a PMI of 48.2, pointing to ongoing contraction. The services PMI has now held the line above 50 in nine of eleven months this year, but the trend has drifted steadily downward since early 2022, leaving the 12-month average at its lowest since the early 2010s. That profile is consistent with an expansion that has matured and slowed, yet remains intact.

For the Federal Reserve, the signal is nuanced but broadly supportive of a measured easing path. Growth is clearly slower than in the immediate post-pandemic rebound, but still positive. Labor demand is softening in services and outright weakening in manufacturing, yet there are no clear signs of a hard break. Inflation pressures are easing, but services prices remain elevated enough to keep policymakers wary of cutting rates too quickly. Layered on top of that, tariffs, trade re-routing, and episodic shutdown risk are now regular features of the operating environment rather than one-off shocks.

Against this backdrop, the November ISM Services report suggests that services will continue to carry the expansion into early 2026, but with less thrust than earlier in the cycle. New orders are cooling, employment is contracting modestly, and supply-chain and tariff frictions are still feeding into prices and delivery times. At the same time, business activity remains solid, backlogs have stabilized at more sustainable levels, and the breadth of growth across industries has widened slightly. The bottom line is that the economy is still growing, but the cycle is running at a lower gear—and policy, margins, and capital allocation decisions will need to adjust accordingly.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 3, 2025

Mark Vitner, Chief Economist

(704) 458-4000