November Data Provide a Number of Confirming Signals for Policymakers and the Markets

-

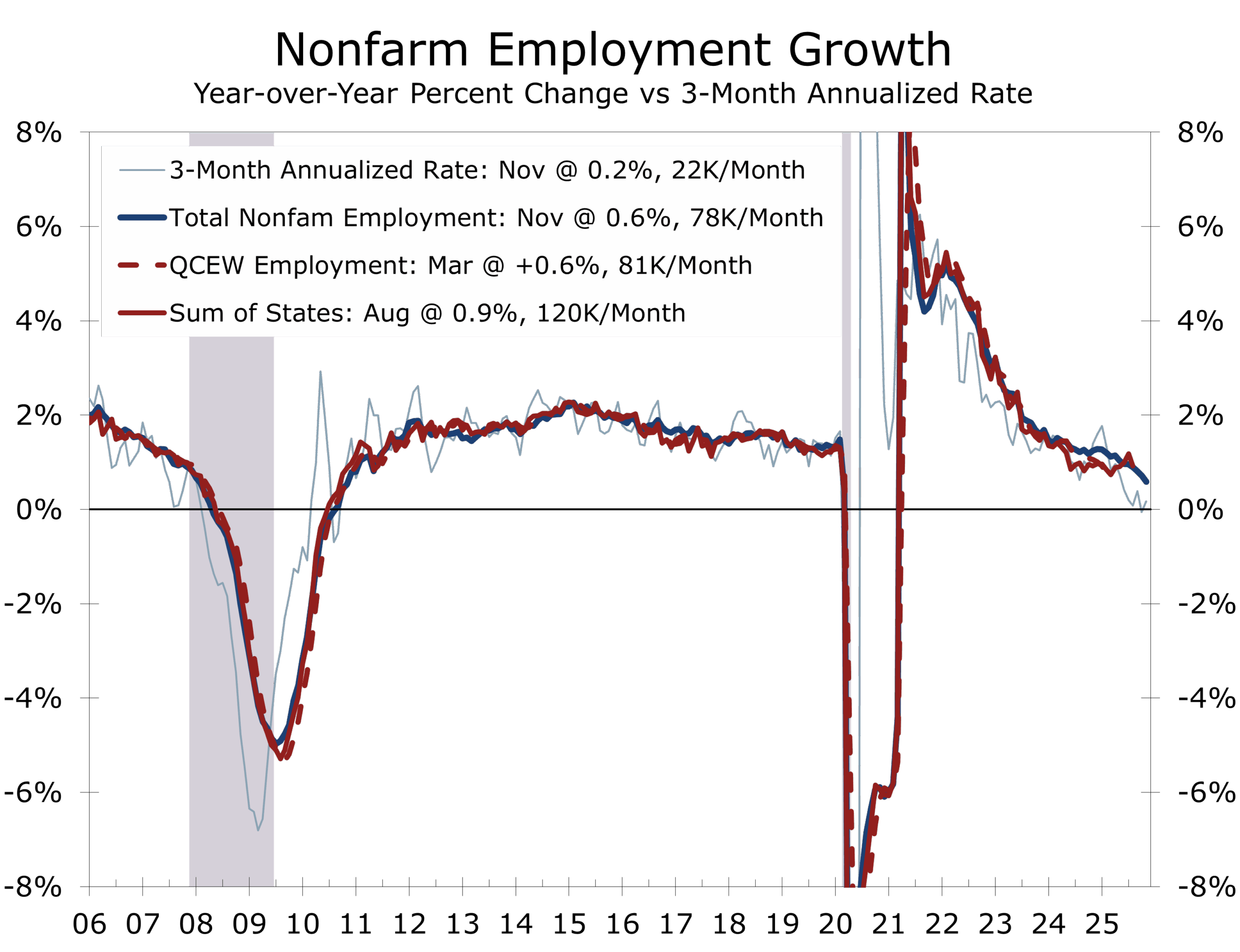

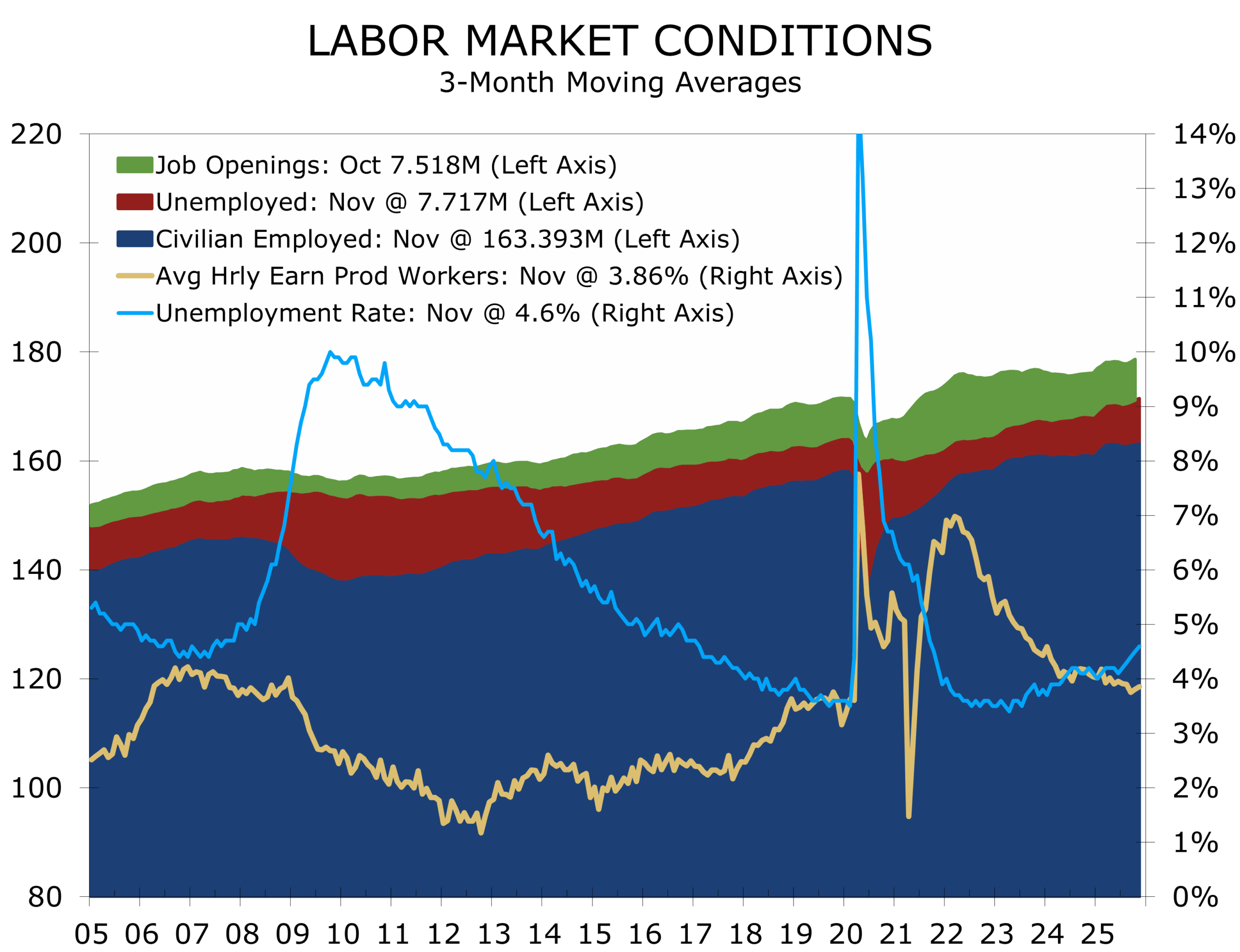

- Payroll growth remains stuck near stall speed. Nonfarm payrolls rose 64,000 in November, extending a pattern of minimal net job growth in place since April.

- Federal job losses are now a material drag. DOGE-related cutbacks have eliminated roughly 271,000 federal jobs year-to-date, distorting headline payrolls and tightening labor conditions in affected regions.

- Hiring is narrow and late-cycle. Job gains remain concentrated in health care, social assistance, and construction, while most other sectors show little or no growth.

- Slack is building beneath the surface. Underemployment surged, with part-time for economic reasons rising by 909,000, and short-term unemployment increasing.

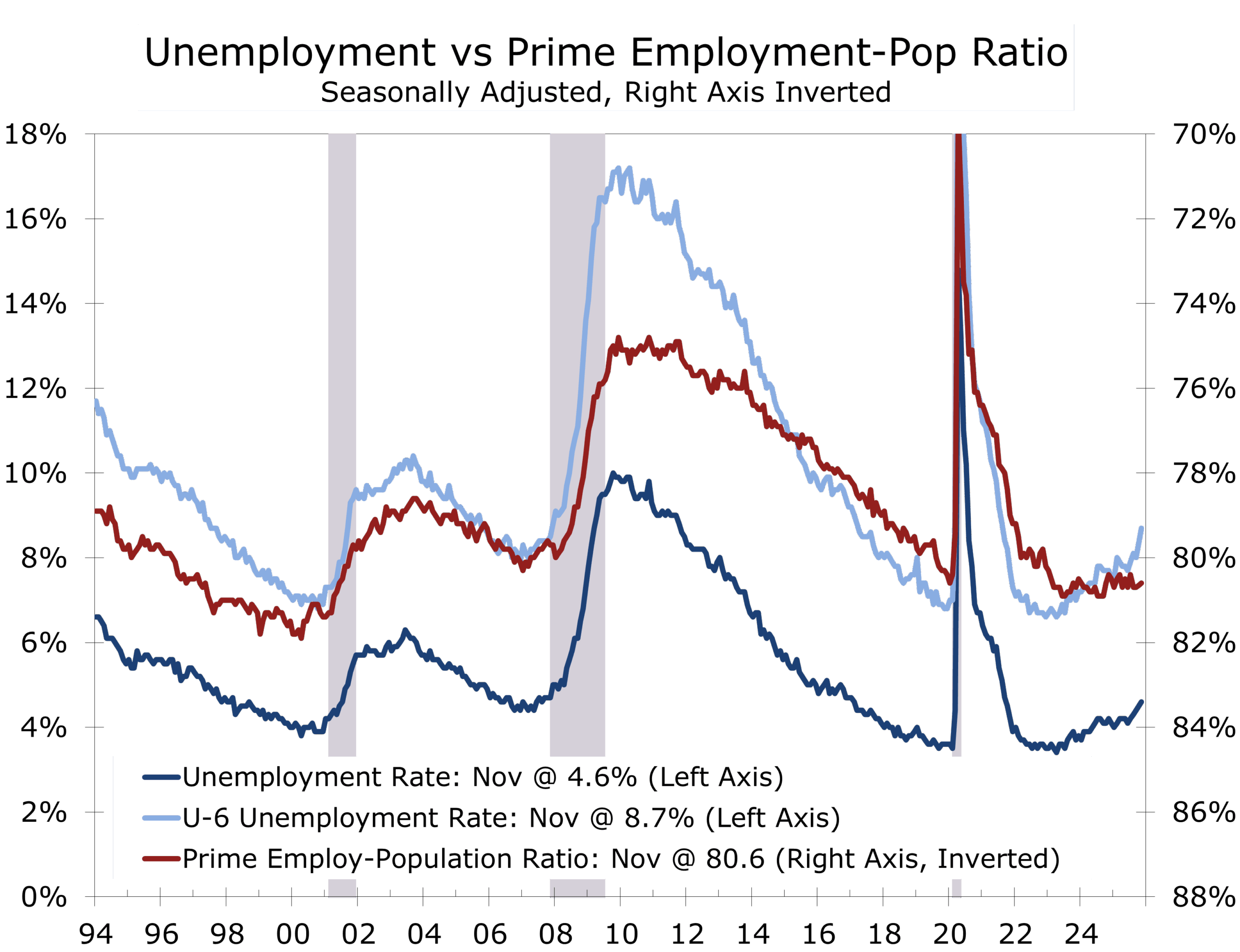

- Unemployment is drifting higher—but unevenly. The jobless rate rose to 4.6%, the highest since October 2021, driven largely by labor-force reentrants and concentrated among younger workers.

- Wage growth continues to cool. Average hourly earnings rose just 0.1% m/m and 3.5% y/y, consistent with the Fed’s inflation objective.

- Policy implications are clear, timing is not. The labor market is no longer tightening, but shutdown-related data gaps complicate the Fed’s near-term decision-making.

Momentum Fades as Slack Gradually Builds

November’s employment report confirms that the U.S. labor market is no longer tightening and is instead operating near stall speed. Nonfarm payrolls rose by 64,000, extending a pattern of muted job growth that has been in place since April. Revisions to August and September again leaned negative, subtracting a combined 33,000 jobs and reinforcing the view that underlying momentum is softer than headline figures initially suggested.

Job growth has slowed to a pace that barely offsets labor force growth, leaving the unemployment rate vulnerable to further drift.

The unemployment rate held at 4.6%, unchanged from September but materially higher than the 4.2% reading a year earlier. With 7.8 million Americans unemployed, labor market conditions now look meaningfully looser than earlier in the cycle. This is not a sudden break, but a gradual accumulation of slack—an economy decelerating rather than contracting.

Two structural forces stand out in this report. First, DOGE-related cutbacks have materially reduced federal payrolls, transforming what had once been a marginal factor into a meaningful drag on employment. Federal government payrolls declined by another 6,000 in November following a sharp 162,000 drop in October, bringing total federal job losses this year to roughly 271,000. These reductions are policy-driven, not cyclical, and will continue to weigh on headline payroll growth into early 2026.

Federal job losses are no longer a footnote—they are a structural headwind for headline employment.

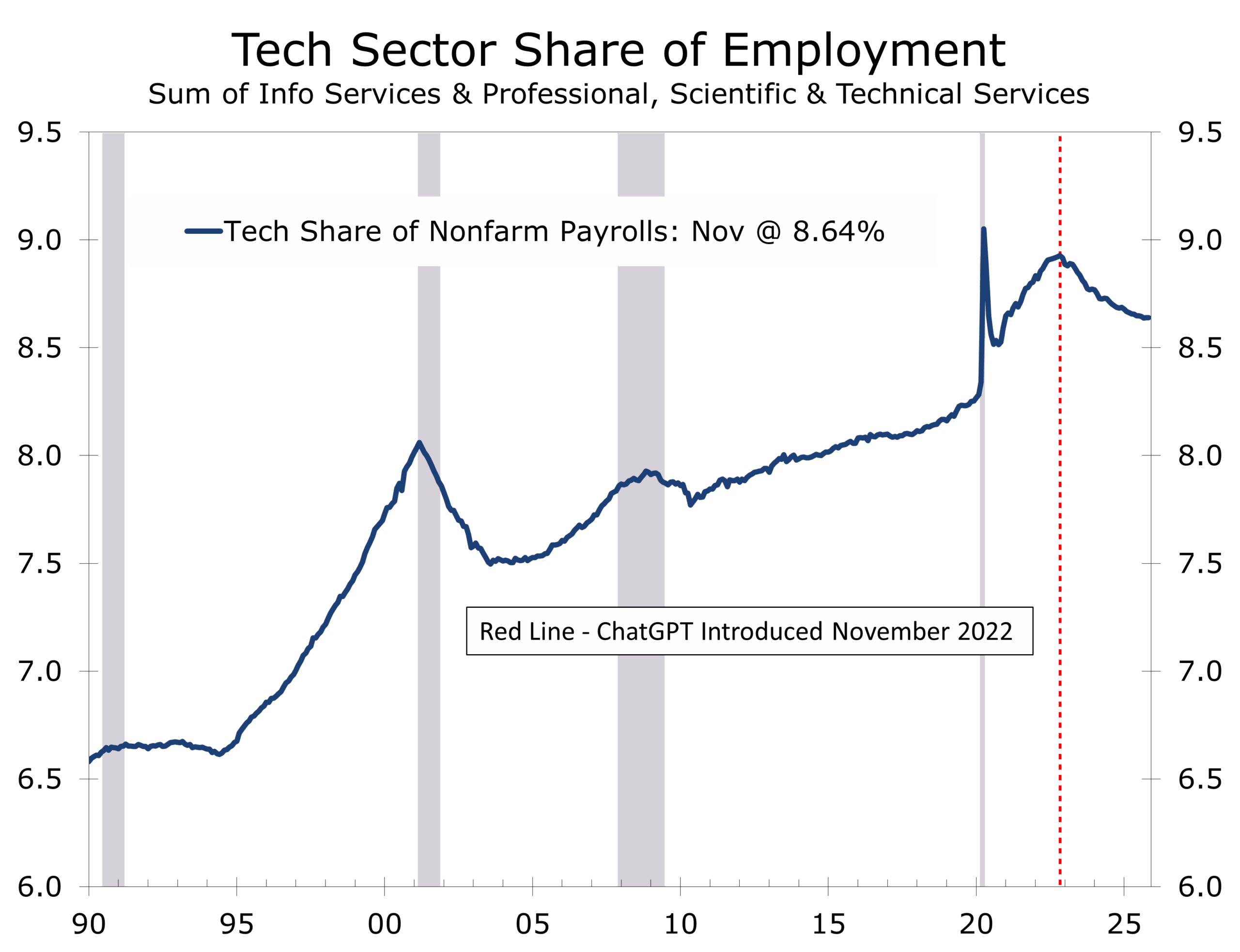

Second, the data increasingly support the view that AI adoption is beginning to suppress employment in certain tech-related sectors, with possible spillovers into parts of the entertainment industry. While AI investment continues to bolster capital spending and productivity, employment in information, professional services, and adjacent creative fields remains soft. Financial services warrants close monitoring as automation, cost discipline, and productivity gains converge over the coming quarters.

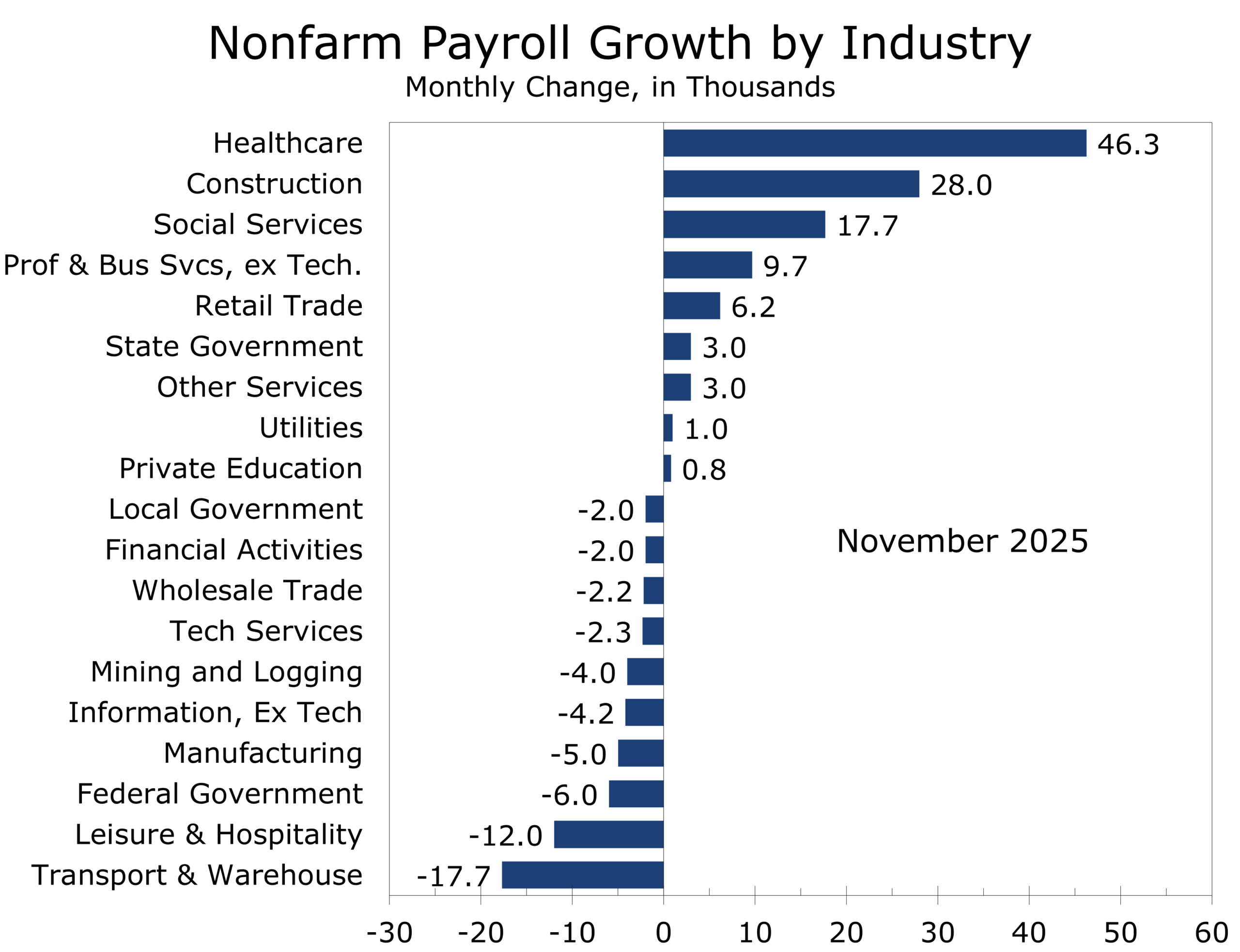

Sectoral detail underscores the late-cycle character of the labor market. Hiring remained concentrated in a narrow set of service industries. Health care added 46,000 jobs, consistent with its longer-run trend, while social assistance rose by 18,000, led by individual and family services. Construction employment increased by 28,000, driven largely by nonresidential specialty trade contractors. While construction employment has been largely flat over the past year, November’s gain suggests backlog completion and infrastructure-related activity are still providing support.

This is not broad-based hiring—it is an economy leaning on a narrow set of labor-intensive services.

Outside these areas, momentum faded. Transportation and warehousing shed 18,000 jobs, entirely due to losses among couriers and messengers. Employment in the sector is now down 78,000 from its February peak, reflecting cooling goods demand. Most other major industries—including manufacturing, retail, wholesale trade, professional and business services, financial activities, and leisure and hospitality—showed little or no change, highlighting the lack of breadth in hiring.

Household survey data reveal additional signs of slack building beneath the surface. While the headline unemployment rate was unchanged on the month, the number of people unemployed for less than five weeks increased by 316,000, suggesting rising job separations or shorter job tenures. More striking was the surge in part-time employment for economic reasons, which jumped by 909,000 to 5.5 million, indicating that firms are increasingly managing labor costs by cutting hours rather than headcount.

This dynamic is also evident in broader measures of labor underutilization. The U-6 unemployment rate, which captures not only the unemployed but also discouraged workers and those working part time for economic reasons, has continued to edge higher, reinforcing the message that underemployment is rising even as the headline unemployment rate appears stable. Historically, sustained increases in U-6 tend to precede more visible deterioration in payroll employment, making this an important late-cycle signal.

Underemployment is rising even as the headline unemployment rate appears stable.

The composition of unemployment has also shifted in a notable way. The rise in the unemployment rate from 4.4% in September to 4.6% in November—the highest level since October 2021—appears to have been driven largely by reentrants to the labor force, potentially including displaced federal workers or their spouses. At the same time, unemployment is increasing disproportionately among younger workers aged 16–24, a group that typically absorbs labor-market adjustments first when hiring slows.

By contrast, labor market conditions for core workers remain comparatively resilient. The prime-age (25–54) employment-population ratio has held relatively steady at historically elevated levels, and the unemployment rate for workers 25 and older has risen by just 0.2 percentage point over the past year to 3.7%. This divergence—rising slack at the margins alongside stability among prime-age workers—is consistent with late-cycle softening rather than a broad-based downturn, suggesting a labor market that is cooling gradually, not breaking.

The composition of unemployment also shifted in a notable way. The rise in the unemployment rate from 4.4% in September to 4.6% in November—the highest level since October 2021—appears to have been driven largely by reentrants to the labor force, potentially including displaced federal workers or their spouses. Unemployment is also increasing disproportionately among younger workers aged 16–24, while the unemployment rate for those 25 and older has risen by just 0.2 percentage point over the past year to 3.7%. This pattern is consistent with late-cycle softening rather than a broad-based downturn.

Wage and hours data reinforce the cooling trend. Average hourly earnings rose just 0.1% in November and are up 3.5% over the past year—well aligned with the Federal Reserve’s inflation objective. The average workweek edged up to 34.3 hours, while manufacturing hours and overtime were unchanged, suggesting that labor demand is easing gradually rather than collapsing.

Wages are no longer the Fed’s key problem, sluggish job growth is.

Taken together, the November report depicts a labor market that has clearly transitioned from expansion to plateau. Hiring remains narrow, underemployment is rising, federal payrolls are shrinking for structural reasons, and wage pressures have faded. Shutdown-related data gaps complicate interpretation, but the direction of travel is unmistakable.

For policymakers, the implication is nuanced. The labor market is no longer generating inflationary pressure, and slack is accumulating at the margins through rising underemployment and cooling wage growth. At the same time, the absence of October data and the distortions embedded in November’s release argue for caution. Policymakers are being asked to make forward-looking decisions with a backward-looking and incomplete dataset. To bridge that gap, we simply averaged the September and November results to approximate October conditions—a method that produces intuitively reasonable results, at least until more complete data become available.

The direction of travel is clear—even if the data are not.

The case for eventual easing remains intact: wage growth has decelerated to a pace consistent with the inflation target, labor-utilization measures are softening, and hiring momentum has narrowed materially. The timing, however, remains less certain. With limited confirmation ahead of the December meeting, the Fed may prefer to wait for cleaner, post-shutdown data early in 2026 before acting, even as the risk of falling behind the curve gradually increases.

While the Fed will receive a substantial amount of new information before its late-January meeting, we believe the odds of a cut at that meeting are higher than current market pricing (just under 25%) suggests. Most of the downside risk to the economy is concentrated in the near term, while the offsetting support from larger tax refunds, capital-spending incentives, and greater clarity on tariffs and trade policy is unlikely to become evident until spring or early summer 2026.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 16, 2025

Mark Vitner, Chief Economist

(704) 458-4000