Better Than Expected Inflation Headlines

- The Consumer Price Index rose just 0.1% in November, bringing the year-to-year change down to 7.1%.

- Prices excluding food and energy items rose 0.2%, following a 0.3% rise the prior month. The core CPI is up 6.0% over the past year.

- Falling gasoline prices (-2%) and used car prices (-2.9%) were two of November’s largest moderating influences.

- Services prices less energy, rose 0.4%, with higher housing costs and labor-intensive services accounting for the increase. Prices for hotels and medical care services fell.

- While inflation is moving in the right direction, persistent wage gains will make it difficult to bring down services prices.

Better-Than-Expected Inflation Arrives Right on Cue

The Consumer Price Index rose less than expected in November, removing one of the last pieces of uncertainty ahead of today’s FOMC meeting. The Fed now has a green light to slow the pace of its rate hikes. We continue to expect the FOMC to raise the federal funds rate half a percentage point, which would put the new range at between 4.25-4.50%.

The overall CPI rose just 0.1% in November, while the core CPI rose 0.2%. Market expectations had called for a 0.3% gain in both. While November’s data were better than expected, inflation remains 7.1% higher than it was a year ago. Moreover, some of the factors pulling inflation lower the past few months, most notably the slide in health insurance cost, are reconciliations and will prove temporary.

Even if part of the improvement is temporary, there is no getting around the idea that inflation is moderating. We have seen the peak in the CPI. A growing number of the most problematic areas of the CPI have improved. Gasoline and used car prices are the most notable, but other areas where prices have fallen include airfares and rental cars.

Health insurance costs eased further in November, falling 4.3% following a 4.0% drop the prior month. The drop in health insurance costs reflects a reconciliation of the way insurance costs are calculated, which is based on the earnings of health care providers. Even after the most recent declines, health insurance costs remain up 13.5% year-to-year.

The modest improvement in the CPI is evident from the year-to-year data. The overall CPI peaked in June at 9.1% and has decelerated in each of the past 5 months, most of which has come from lower gasoline prices. The core CPI appears to have peaked in September at 6.6%, with declines in used car prices accounting for a large share of the improvement. Medical care costs also slowed, with hospital costs falling 0.3% and physician services flat. While welcome, the moderation here seems suspect.

There is a raging debate as to how much weight the Fed should give to the more modest improvement in the core CPI, given the heavy sway housing costs, which show up with a lag, have on the core CPI. Residential rent and owners’ equivalent rent account for just 40% of the core CPI. Both continue to increase at an elevate pace, mostly reflecting past increases. Market measures of current rents show rents are now declining in much of the country and moderating virtually everywhere else. Home prices are also falling.

While we have some sympathy for this argument, the Fed is almost certainly keeping an eye on market rents and fully understands the lags in the CPI’s housing components. That said, tenants renewing leases today are seeing their rents increase, often dramatically. Owners’ equivalent rent is also moderating far less than market measures of home prices, as only a fraction of homeowners purchase a home each year.

In short, the housing measures in the CPI are performing the way they are supposed to.

Inflation is most problematic in areas where wages account for the bulk of costs.

The Fed is more concerned about the persistence of inflation in labor-intensive sectors. Prices for personal care services rose 1.4% in November. Motor vehicle maintenance and repair (1.3%), recreational services (1.1%), professional services (0.9%) and restaurants (0.5%) all posted outsized price gains as well. Moreover, prices at full-service restaurants are up 9% year-to-year, while prices at less labor-intensive limited-service restaurants rose a more modest 6.7%.

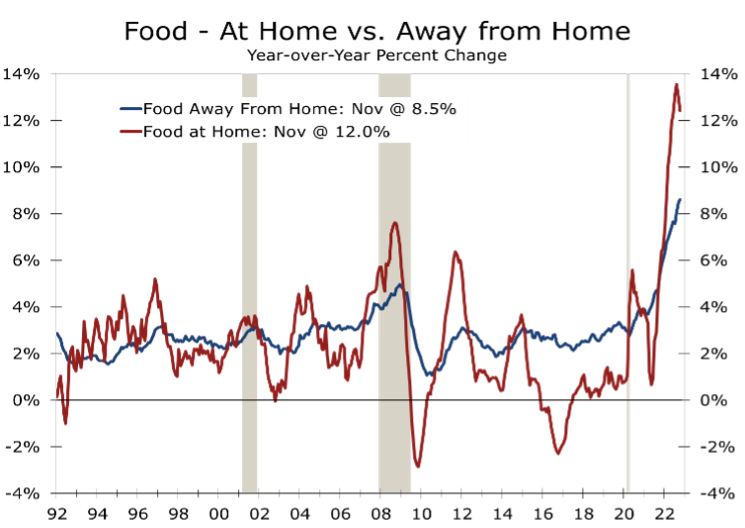

The cost of dining at home has risen even faster, with prices climbing 12% over the past year. Prices have moderated somewhat more recently but still posted a 0.5% increase in November. Prices rose the fastest for cereals and bakery products, which climbed 1.1% and are now up 16.4% over the past year. By contrast, prices for beef (-5.2%) and pork (+1.2%) have fallen this past year. By contrast, poultry prices fell in November but remain up an astounding 13.1% over the past year. The split highlights a cruel irony at grocery stores, where prices for lower cost proteins have risen dramatically. Prices for lunchmeats are up 18.4% over the past year, while the price of frankfurters has risen 13.4%. The price of eggs is truly in a league of its own, however, having soared 49.1% over the past year.

The subcomponent that best captures today’s inflationary pressures is the CPI, excluding food, energy, and shelter. The trend here is moderating as well and closely follows the share of businesses raising prices. The latter is being driven by soaring labor costs.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.