Softer Economic Data Headed into the Fall

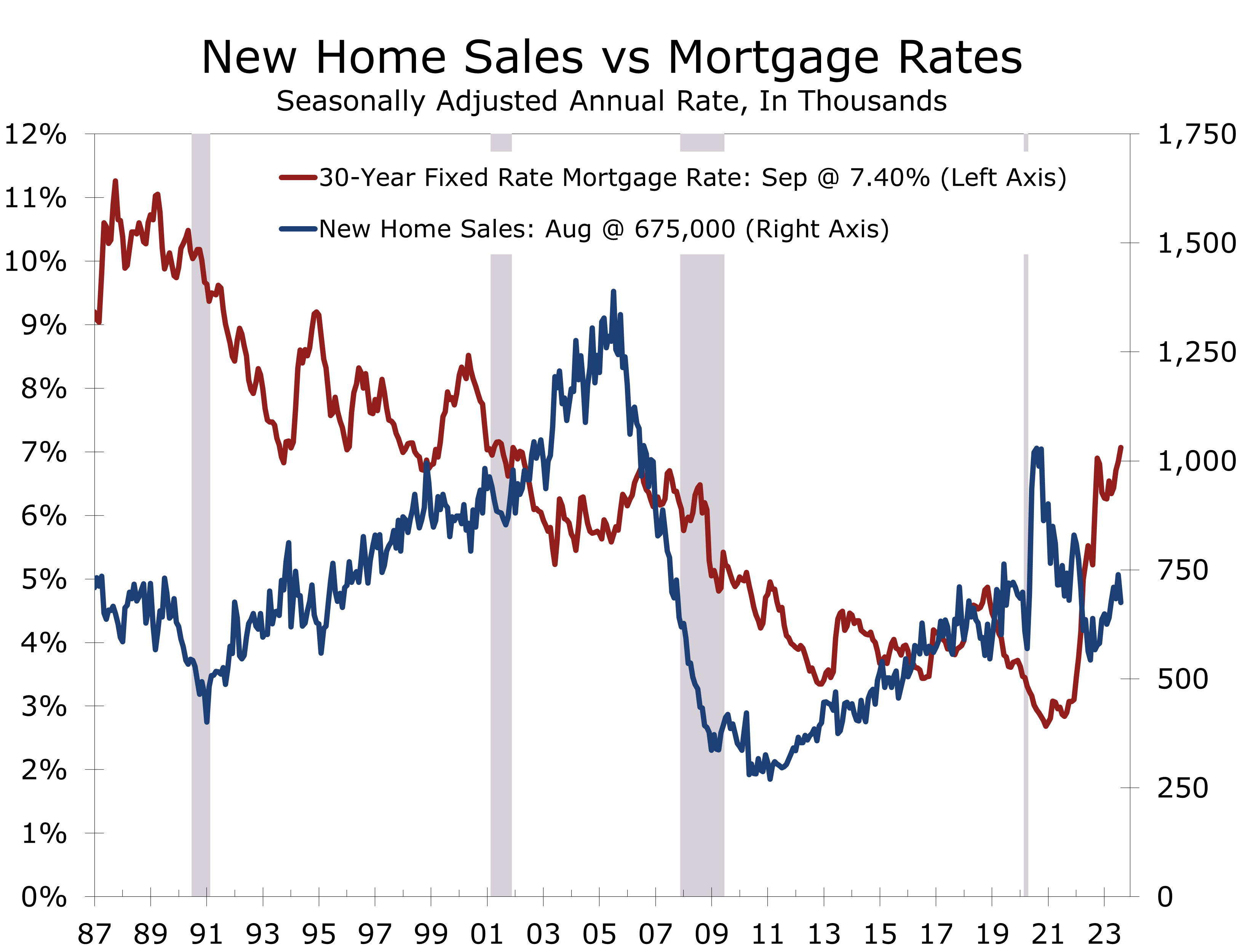

- New home sales fell 8.7% in August to a 675,000-unit pace. July sales were revised higher, which reduces much of the sting from the larger-than-expected August drop.

- Sales rose in the Northeast (+6.7%) but fell in the Midwest (-17.2%), West (-9.4%) and South (-7.5%).

- The inventory of new homes rose slightly in August to 436,000 homes, which translates into a 7.8-month supply.

- The median price of a new home fell to $430,300 in August and is down 2.3% over the past year.

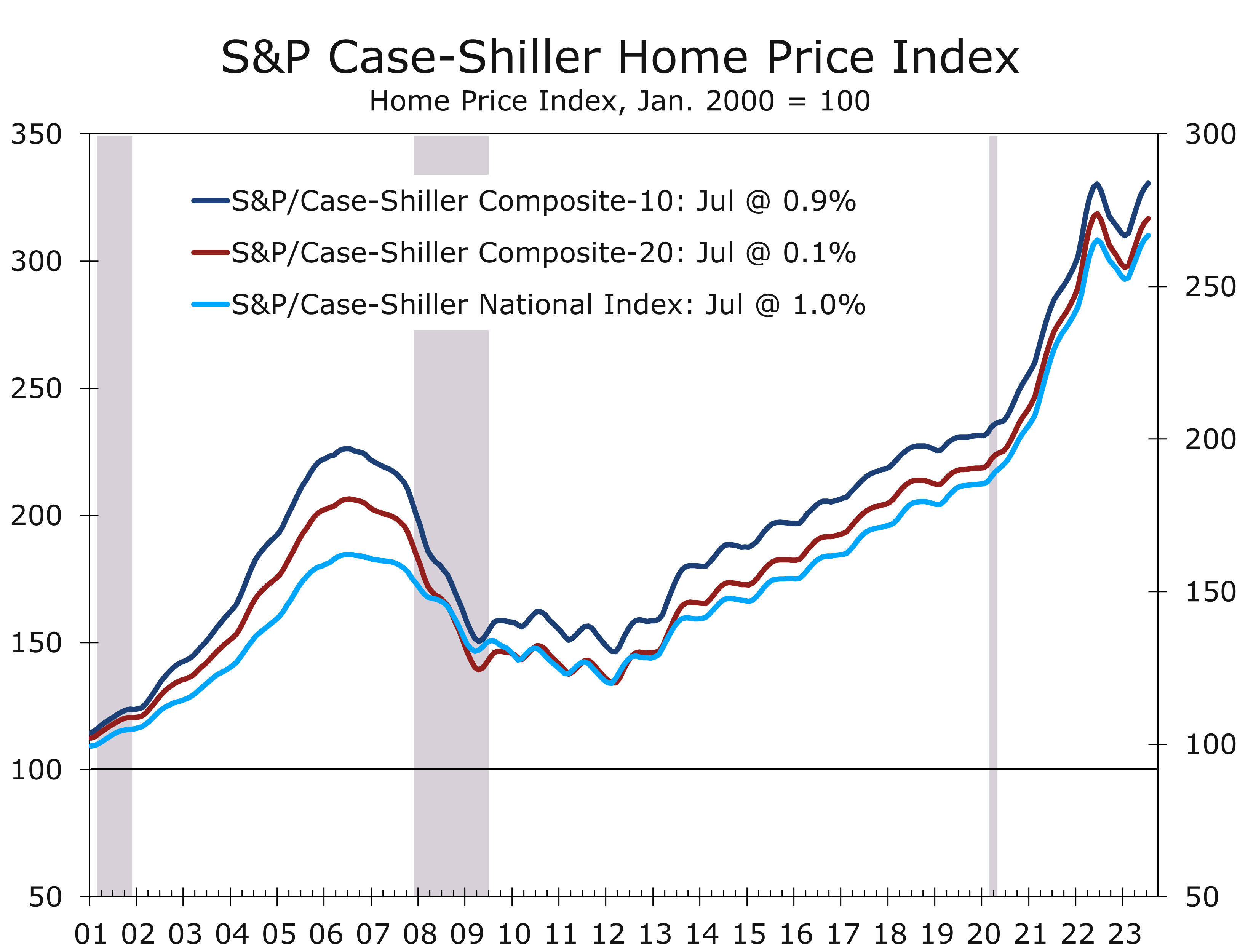

- Home price data was released separately this morning, which continues to show strong price appreciation for existing homes.

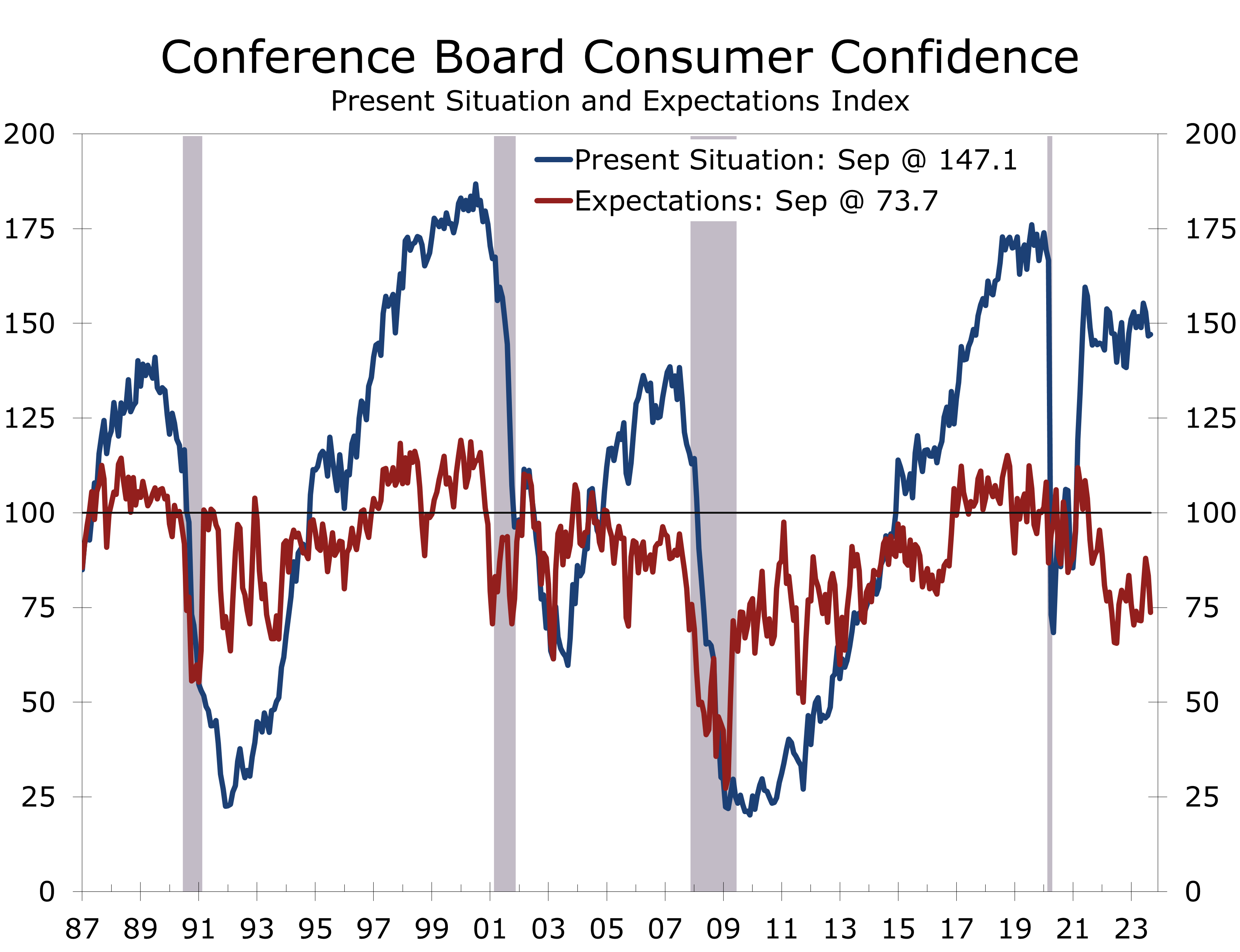

- Consumer Confidence declined more than expected in September, reflecting growing concerns about higher food and energy prices, and rising interest rates.

- On balance, today’s economic reports show higher interest rates and higher gasoline prices are beginning to chip away at the economy’s surprising resilience. After what looks to be a strong Q3, we look for growth to slow in the final quarter of this year.

New home sales fell 8.7% in August to a 675,000-unit pace. The drop was slightly larger than expected but an upward revision to the July data left sales fairly close to consensus expectations. New home sales are coming under pressure from higher mortgage rates, which rose above 7.50% in late September.

Home builders have benefitted from the persistent shortage of existing homes throughout much of this year, which allowed new home sales to rise even as mortgage rates increased. Sales have been under pressure ever since mortgage rates topped 7%, however. Earlier this month, home builders reported that buyer traffic fell 5 points in September to 30, following a 5-point drop in August. Realtors also reported an uptick in contract cancelations on existing homes, as mortgage rates rose more than expected ahead of closing.

New home sales have come under pressure ever since mortgage rates rose above 7%.

Builders are becoming more cautious. Higher interest rates, higher home prices and higher construction costs mean housing affordability is likely to remain stretched for some time. Builders are responding by discounting prices and buying down mortgage rates. This helps at the margin and may help stave off an avalanche of cancelations but becomes less effective as rates move even higher.

The latest CoreLogic S&P Case-Shiller Home Price Index reported another sizeable rise in home prices in July, with the National Index, 20-City, and 10-City indices each rising 0.6%. The National Index has risen 1.0% over the past year and is now slightly above its prior peak, hit in June 2022. The 10-City Index has also risen back above its prior peak. While 19 of the 20 metros in the 20-City Index rose in July, this index has lagged and is up just 0.1% over the past year. Several metro areas in the West included in the 20-City Index, such as San Francisco, Phoenix, and Portland, saw sharper declines during the second half of last year and have seen smaller rebounds this year.

Home prices have rebounded since bottoming out in January and are now at a new high.

The Midwest lays claims to three of the nation’s top five markets for home price appreciation. Home prices have risen 4.4% over the past year in Chicago and are up 4.0% in Cleveland. New York (+3.8%), Detroit (+3.2%) and Atlanta (2.2%) round out the top five.

Higher home prices have boosted household wealth, with households now holding a collective $31.6 trillion in equity, up from $22 trillion prior to the pandemic. The rise in home equity helps explain the resilience of consumer spending, even though consumers are not tapping equity anywhere near as much in prior cycles.

We suspect home prices are now weakening. The Case-Shiller data lag by a few months, the most recent data are for July. Other more timely price measures. such as those provided by Zillow, are beginning to show signs of slowing once again. The culprit is higher mortgage rates, which are leading to slew of cancelations for new and existing homes, resulting in more discounting by builders and concessions by sellers.

Consumer Confidence fell a larger than expected 5.7 points in September to 103. All of the drop was in the expectations series, which tumbled 9.6 points to 73.7. An expectations index reading below 80 is generally consistent with a recession. The expectations series is more closely tied to swings in consumer behavior and points to some cooling in consumer spending and home buying later this year.

Consumers’ assessment of current economic conditions edged 0.4 points higher to 147.1, largely due to another strong assessment of current labor market conditions. The current conditions index remains at a level historically consistent with strong economic growth and the improvement in current labor market conditions is consistent with a slight drop in the unemployment rate during September.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.