A Negative CPI Print, a New Chair on the Hill and a Fraying Ceasefire

A View from the Piedmont — Weekly Economic & Financial Commentary

This Week's Key Points

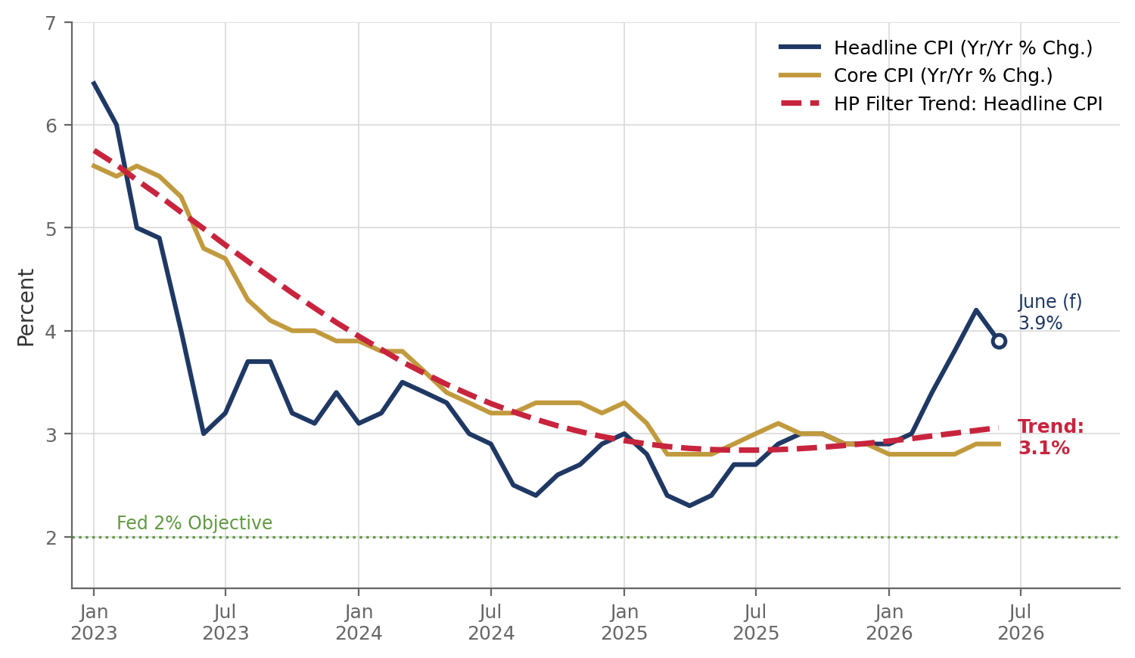

- June CPI (Tuesday) is set up for the first negative headline print of this expansion. A drop of roughly 10 percent in retail gasoline prices should pull the headline index down; we forecast a 0.14 percent decline, trimming year-over-year inflation to about 3.9 percent from 4.2 percent.

- Do not let the headline fool you. We forecast a 0.26 percent rise in core CPI, holding the core rate near 2.9 percent, and our HP filter gauge puts underlying inflation right around 3 percent, well above the Fed's objective. One area we will be watching closely is technology products, where the AI buildout is driving chip costs higher, which is showing up in consumer electronics and laptops.

- Chair Kevin Warsh delivers his first semiannual monetary policy testimony, before the House on Tuesday and the Senate on Wednesday. Futures markets price roughly 50 basis points of tightening through mid-2027; we continue to look for the Fed to remain on hold this year, with the next move more likely a hike than a cut.

- The US-Iran ceasefire frayed badly this past week. US forces struck more than 300 targets over three nights after Iranian attacks on commercial shipping, and traffic through the Strait of Hormuz has slowed to a trickle. Oil still ended the week near $71 for WTI, about 30 percent below its spring peaks.

- Senator Lindsey Graham passed away Saturday evening, one day after announcing a White House-endorsed agreement on his bipartisan Russia sanctions bill. Momentum to pass the measure as a tribute has grown quickly, with meaningful implications for global oil supply. Senator Graham served as a bridge between the Trump Administration and the Senate, and vice versa. Whoever takes up that role will greatly determine what the Administration will accomplish before the midterm elections.

The Week in Perspective

The coming week packs more event risk into five trading days than we have seen since the Iran war began. Tuesday brings the June CPI report and the first of two days of semiannual monetary policy testimony from Federal Reserve Chair Kevin Warsh, followed Wednesday by the PPI, the Beige Book and Warsh's Senate appearance. Retail sales, housing starts and the start of second quarter earnings season round out the docket. All of this arrives against a geopolitical backdrop that shifted considerably over the weekend, with renewed US strikes on Iran, a diplomatic push in Muscat, Oman, and the sudden passing of Senator Lindsey Graham just as his Russia sanctions bill appeared headed for the floor.

The macro story we have been telling all year remains intact. This is a capital-led, employment-light expansion, or, as we are fond of saying, protein rather than carbohydrates, powered by AI infrastructure spending, reshoring and productivity gains rather than by hiring. The war-driven energy spike that pushed headline inflation to 4.2 percent in May is now unwinding, but underlying inflation is running near 3 percent and the Fed has little room for error. That tension, between a falling headline rate and a firm underlying trend, is the central theme of the week ahead.

Markets and Financial Developments

Equities carried strong momentum into the weekend despite the renewed fighting in the Gulf. The S&P 500 rose 0.4 percent Friday to close at 7,575, its fourth consecutive winning week and within roughly half a percent of its June 2 record of 7,621. The Nasdaq added 0.3 percent to 26,282, while the Dow gained 150 points to 52,637, though the blue chips lagged on the week. The AI trade continues to set the tone. Nvidia rose about 4 percent Friday and Meta jumped 6 percent, capping its best week since early 2024, after reports suggested the company is building AI capacity at a much lower cost per gigawatt than the Street had assumed. SK Hynix's American depositary receipts surged in their Nasdaq debut after the memory chipmaker raised $26.5 billion in the largest US listing ever by a foreign company, a clear signal that investor appetite for AI hardware remains deep. The stock sold off sharply in Korea on Monday, setting a weak undertone to Nasdaq trading this week.

Fixed income tells a more cautious story. The 10-year Treasury yield rose nine basis points on the week to 4.57 percent, its highest close since late May, and has risen in eight of the past nine sessions. Futures markets have swung from pricing cuts earlier this year to roughly 50 basis points of hikes through mid-2027, a shift that reflects both the May inflation surprise and the hawkish tone of Chair Warsh's first FOMC meeting in June, when the committee lifted its median 2026 inflation projection to 3.6 percent and nudged the dot plot higher. Equities have historically struggled in the opening months of tightening cycles, with an average 2 percent decline over the first three months across the past seven episodes, and this capital-intensive cycle is unusually sensitive to the cost of capital. A soft CPI print and measured testimony from Warsh could relieve some of that pressure; the S&P 500 has moved about 0.6 percent in absolute terms on the average CPI day over the past year.

Commodities reflected the week's geopolitical whiplash. WTI crude rose about 4 percent on the week on renewed Hormuz disruptions but settled Friday at $71.41, with Brent at $76.01, both roughly 30 percent below their spring peaks. Prices rose further on Monday, with WTI climbing to $78 and Brent rising to $82. The UAE lifted crude output to a record last month, and other Gulf producers continue to route around the strait where they can. The dollar firmed modestly, while the yen bounced off 40-year lows after Tokyo signaled it would encourage pension funds to hold more domestic assets.

Inflation Watch: Reading Through the Gasoline Swing

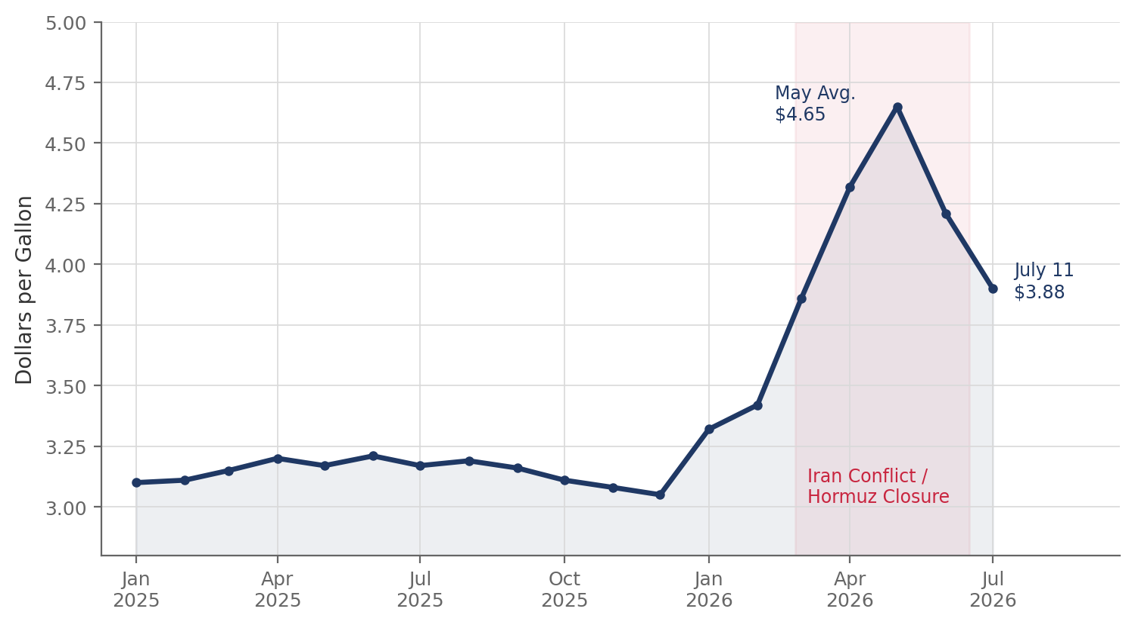

The June CPI should deliver the rare sight of a declining price level, and we would caution readers not to read too much into it. Retail gasoline prices fell roughly 10 percent from May to June as the mid-June memorandum of understanding reopened the Strait of Hormuz and crude prices tumbled from their wartime highs. With gasoline carrying a weight of nearly 4 percent in the CPI and June's seasonal factors offering little offset, the pump-price decline alone should subtract 0.35 to 0.40 percentage points from the headline index. We look for headline CPI to fall 0.14 percent for the month, pulling the year-over-year rate down to about 3.9 percent from May's 4.2 percent, which had been the fastest pace in more than three years.

Core inflation is another matter entirely. We forecast a 0.26 percent rise in core CPI in June, a touch below the 0.3 percent consensus, either of which would hold the core rate near 2.9 percent, essentially where it stood a year ago. Shelter costs continue to moderate only gradually, and services inflation remains sticky. Within core goods, we will be watching technology products closely. May brought the first monthly decline in core goods prices in 14 months, suggesting the bulk of tariff pass-through is behind us, but a new source of goods inflation is building. Surging memory chip and component costs tied to the AI buildout are working their way into consumer electronics, and Apple has announced price increases averaging about 20 percent on some of its most popular products. Information technology commodities carry a weight of only about three-quarters of a percent in the CPI, so the top-line effect will be modest, but the swing in direction matters: core goods are more likely to add to inflation over the second half than subtract from it.

Our HP filter gauge of trend inflation now sits right around 3 percent, up from 2.8 percent at the turn of the year. The Hodrick-Prescott filter strips the monthly noise out of the inflation data and gives us a cleaner read on where prices are trending once temporary shocks wash out. The message is uncomfortable for the Fed. Even after the war-related energy spike unwinds, the underlying pace of inflation appears to have drifted up toward 3 percent rather than settling back toward 2 percent. The trimmed-mean gauges we favor, from the Cleveland and Dallas Feds, tell a similar story, with both running near 0.3 to 0.4 percent monthly in recent readings. A negative June headline will make for friendly newspaper coverage, but the underlying trend explains why the FOMC struck such a hawkish tone in June and why futures markets are entertaining hikes rather than cuts.

Geopolitics: A Fraying Ceasefire and a Sudden Loss

The US-Iran ceasefire came under severe strain this past week, though markets are treating the flare-up as containable. Iranian forces fired missiles at three commercial vessels transiting the Strait of Hormuz early in the week, the first such attacks since the 14-point memorandum of understanding was signed in mid-June. US Central Command responded with three nights of strikes on more than 300 Iranian targets, including missile and drone sites, naval assets and coastal surveillance positions, with roughly 140 targets hit in the latest round early Sunday. Iran retaliated against US military facilities in Jordan and elsewhere in the Gulf, and the IRGC has again declared the strait closed. Commercial transits have slowed dramatically, with no large vessels broadcasting their positions along the Oman-hugging southern route since July 7.

Diplomacy has not broken down, and that distinction matters for markets. Iranian Foreign Minister Araghchi traveled to Muscat, Oman, on Saturday for talks with his Omani counterpart, and Oman has drafted a proposal to manage traffic through the strait. President Trump has declared the memorandum of understanding over but says talks will continue, and Qatari mediators remain engaged. The commodity market response has been telling: oil rose about 4 to 5 percent on the week but remains far below the spring peaks, gasoline held steady at $3.88 per gallon nationally, and jet fuel and Gulf petrochemical exports are still well off their wartime highs. Our composite read is that the passthrough from the conflict to core inflation peaked in the second quarter and should fade through year-end, provided the current exchange does not escalate into something larger. A sustained return to triple-digit oil would add only a few basis points per month to core inflation directly, but the expectations channel is the risk worth watching, and it is the one Chair Warsh will surely be asked about on the Hill.

The war between Russia and Ukraine may be approaching an inflection point. President Trump held a cordial meeting with President Zelensky on the margins of the NATO summit in Ankara on July 8, and Washington has agreed to license Patriot missile production in Ukraine, a significant step in Kyiv's drive toward defense self-sufficiency. Ukrainian long-range drones have struck oil infrastructure as far away as St. Petersburg and the Urals, contributing to gasoline shortages inside Russia, an economy now flirting with recession and a budget crisis. Moscow, for its part, claims continued gains in the Donbas and has, if anything, expanded its territorial demands. Both diplomatic momentum and escalation risk have increased at the same time, which is precisely the kind of environment in which energy and defense markets can move quickly.

Senator Lindsey Graham's sudden passing on Saturday evening adds a poignant and consequential twist. Graham died of an aortic tear at 71, one day after announcing in Kyiv that he had reached agreement with the White House on a version of his long-pending Russia sanctions bill, co-authored with Senator Blumenthal, that the administration will support. The bill would give the President broad authority to impose tariffs and secondary sanctions on countries purchasing Russian oil and gas, aimed squarely at China, India and Brazil, which imports diesel and other refined products from Russia. Colleagues in both parties, including Senators Blumenthal, Shaheen and Wicker, are now urging swift passage as a tribute to Graham's legacy, and prospects for enactment appear to have improved markedly. For energy markets, secondary sanctions that meaningfully curtail Russian crude purchases would tighten global supply at a moment when Gulf flows are already disrupted, one more reason a risk premium is likely to remain embedded in oil prices even if the Hormuz situation stabilizes. Closer to home, Graham's passing opens a South Carolina Senate seat and sets up a special election that will reshape the Palmetto State's congressional delegation. South Carolina will hold a special primary on August 11, with a host of candidates fresh off a contested governor's race likely to enter.

Monetary Policy: Warsh Goes to the Hill

Chair Warsh's first semiannual testimony is the week's most important policy event, CPI notwithstanding. Warsh testifies before House Financial Services on Tuesday and Senate Banking on Wednesday, delivering the monetary policy report the Fed submitted to Congress on Friday. His June FOMC debut was decidedly hawkish: the committee lifted its median 2026 inflation projection to 3.6 percent from 2.7 percent and moved the median funds rate projection up to 3.8 percent, signaling higher for longer. Yet his remarks at the ECB Forum leaned the other way, emphasizing declining inflation risks, the supply-side benefits of AI and a firm commitment to the 2 percent objective. Lawmakers will press him on the gap between those two messages, on how the Fed intends to treat energy shocks it cannot control, and on the August methodological changes that are expected to lower the measured year-over-year core PCE rate by roughly 0.2 percentage points.

Our view has not changed. We expect the funds rate to finish the year in its current 3.50 to 3.75 percent range, and we continue to believe the next move is more likely a hike than a cut, though we would put the probability of tightening this year at only about one in four. This week's inflation data and Warsh's Humphrey-Hawkins testimony will go a long way toward determining whether the Fed retains the flexibility to hold off on any rate hikes until 2027, which is what we currently expect. Anything worse than a 0.3 percent rise in the core CPI, or even a broadening in the breadth of price increases within the core, would weaken the case for waiting until next year. Futures markets pricing roughly 50 basis points of hikes through mid-2027 strikes us as an overcorrection to the May inflation data, just as pricing for multiple cuts early this year was an overcorrection in the other direction. The June core PCE, due later this month, is likely to print around 0.24 percent for the month, slightly firmer than core CPI owing to the lagged financial services component.

The Global Backdrop

The durability of the US-Iran agreement has become the hinge on which the global outlook swings, and it was the through-line of Oxford Economics' quarterly roundtable last week. Oxford judges the latest escalation too small to change its baseline for growth, inflation or policy and expects the US economy to regain momentum in the second half as lower fuel prices repair household purchasing power, a read that lines up with our own capital-led thesis. We share that extended-pause baseline, though we would tilt the risks somewhat more toward tightening, and we take the recent Fed minutes, focused on inflation rather than employment, as leaving the door open to a hike. Europe looks a bit better on their read as well, with the eurozone having weathered the energy shock better than feared even as the ECB keeps stressing inflation risks. The near-term impulse we are watching most closely is the goods inflation from the AI buildout that Oxford itself flags, the same impulse that should surface in the technology components of Tuesday's CPI.

Labor and Housing: Steady Jobs, Rate-Sensitive Housing

The labor market continues to hold its ground without adding much to it. Initial jobless claims edged down to 215,000 last week, in line with expectations, and the four-week average improved. Layoffs remain low even as hiring stays subdued, the signature of this employment-light expansion. Businesses are building capacity without adding headcount, and the productivity data continue to validate that strategy.

Housing remains the economy's most rate-sensitive corner. Existing home sales fell 2.4 percent in the latest month to a 4.09 million-unit annual pace, defying expectations for a gain, as mortgage rates near 6.5 percent continue to sideline buyers. The median price was essentially flat and months' supply held at 4.3. Friday's housing starts report should bounce, with the consensus looking for a gain of roughly 12.5 percent after a weak prior month, but the single-family trend remains soft. Inventory gains are the missing ingredient; until resale supply improves meaningfully, affordability will remain stretched and sales will stay range-bound. We may see a slight bounce in sales in coming months, as buyers pull demand forward on fears that mortgage rates are headed higher.

The Week Ahead

Monday, July 13. Fed Vice Chair Bowman speaks on regulation; Governor Waller speaks. No major data. Quarterly earnings season begins in earnest Tuesday.

Tuesday, July 14. June CPI (PCC forecast: headline -0.14%, core +0.26%). Chair Warsh's semiannual testimony before House Financial Services. Fed speakers include Barr (AI), Goolsbee and Cook. Big bank earnings kick off the reporting season.

Wednesday, July 15. June PPI (consensus +0.2% headline); Empire State manufacturing; Chair Warsh testifies before Senate Banking; Beige Book (watch for regional color on energy volatility and shipping costs).

Thursday, July 16. June retail sales (consensus +0.1% headline, +0.4% control group); initial jobless claims; Philadelphia Fed manufacturing; pending home sales; Dallas Fed's Logan speaks.

Friday, July 17. June housing starts (consensus looks for a rebound of roughly 12.5%); industrial production (+0.2%); import & export prices; University of Michigan consumer sentiment (preliminary July).

CFO & Treasurers Corner

Rates and borrowing: Futures markets pricing hikes creates both optionality and volatility risk. With this cycle unusually capital-intensive, sensitivity to the cost of capital is elevated. We favor locking in longer-term financing while spreads remain attractive or pairing floating-rate structures with hedges. The window around Tuesday's CPI and testimony could produce the best or worst issuance conditions of the month.

Inflation and energy: The fading passthrough from the Gulf conflict is constructive for input costs, but the renewed fighting is a reminder that the tail risk has not gone away. Treasurers with Gulf-exposed supply chains should revisit hedging programs now, while forward energy prices remain well below the spring peaks. Watch electronics and component costs separately from broad energy costs; AI-driven chip demand is a distinct and durable source of input inflation.

Russia sanctions contingency: Passage of the Graham-Blumenthal sanctions bill now looks considerably more likely. Firms with exposure to Chinese, Indian or Brazilian counterparties should assess how secondary sanctions on Russian energy purchases could ripple through shipping rates, customer costs and compliance obligations.

Consumer and housing: Thursday's retail sales report should show a resilient but selective consumer. Plan around a two-Americas (K-shaped) demand environment: upper-income households continue to spend on services and experiences while rate-sensitive and lower-income segments trade down.

Cash and liquidity: Steady claims and solid spending keep recession signals muted. Maintain flexibility for opportunistic moves if equity volatility rises around the CPI-testimony window.

Regional Perspective: The South Shows Well in CNBC's Top States

The South was well represented in CNBC's latest America's Top States for Business study, even as top honors traveled north. Ohio claimed the No. 1 ranking for the first time in the study's 20-year history, propelled by the nation's best infrastructure, low business costs and a deepening data center pipeline. But North Carolina, which finished second by a mere nine points, earned the distinction that matters most to us: the nation's strongest economy. The Tar Heel State ranked first outright in the Economy category, on 3.2 percent first quarter growth and 3.7 percent unemployment, climbed to third for workforce and eighth for technology and innovation, and has now finished first or second overall for six consecutive years. Virginia placed third and Texas fourth, giving the South three of the top four spots, and Arkansas, which is riding a wave of industrial development, took Most Improved honors.

The results read like a scorecard for the themes we have been writing about for years. Capital, people and production continue to flow toward the South, the same Great Reshuffling of households and firms that has powered the region's outperformance through this capital-led expansion. It is telling that CNBC re-weighted its methodology this year to make infrastructure the heaviest category and to score permitting for the first time; site readiness, power availability and speed to build are precisely the terrain on which the AI and reshoring investment waves are being fought, and precisely where the Southeast has invested ahead of demand. Ohio's win, built on shovel-ready sites and a 10-gigawatt SoftBank data center campus, is a reminder that the Midwest is now competing hard for the same projects. North Carolina's slip to 35th for cost of living is the flip side of its own success, a strain we have chronicled across our Charlotte and Raleigh-Durham outlooks, and the strongest argument for the housing and infrastructure investment the state's newly signed budget can now advance.

The near-term regional backdrop remains favorable. The retreat in gasoline and jet fuel prices from their wartime peaks is a meaningful tailwind for the region's logistics, manufacturing and household budgets, and Wednesday's Beige Book will offer fresh color from the Richmond and Atlanta districts on how firms are absorbing energy volatility and shipping costs. Housing across the major Carolina metros echoes the national pattern of rate sensitivity, though resale inventory has improved more here than nationally, which should help moderate price pressures. The loss of Senator Graham also carries regional weight beyond politics: South Carolina loses considerable Senate seniority at a moment when the state is competing aggressively for defense, port and advanced manufacturing investment.

Strategic Takeaway

We remain constructive on the expansion, and this week will test that view from several directions at once. A negative headline CPI paired with measured testimony from Chair Warsh would reinforce the extended-pause narrative, support lower yields and likely extend the equity rally. The greater risk is the opposite combination: a firm core print alongside hawkish testimony would validate the futures market's drift toward hikes and pressure the rate-sensitive corners of the market. Underneath the weekly noise, our reading is unchanged. Growth is solid and increasingly broad, underlying inflation is closer to 3 percent than 2, the Fed will be patient but is not finished, and geopolitics will continue to set the tempo for energy markets. We will update our views immediately following Tuesday's data and testimony.

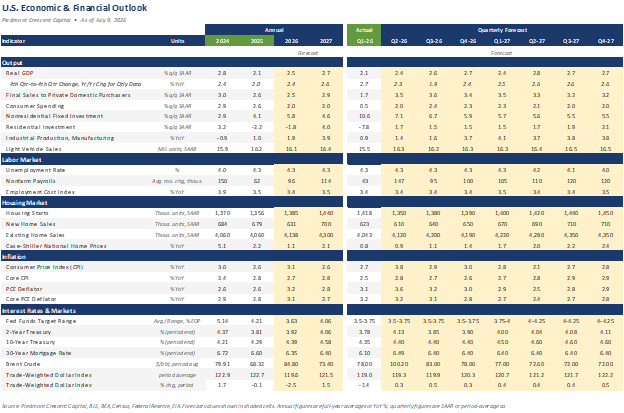

U.S. Economic & Financial Outlook

Source: Piedmont Crescent Capital, BLS, BEA, Census, Federal Reserve, EIA. Forecast values shown in shaded cells. Annual figures are full-year averages or YoY %; quarterly figures are SAAR or period-average as noted in Units.

Forecast disclaimer: The projections above reflect Piedmont Crescent Capital's views as of the date shown and are subject to change without notice. They are provided for informational purposes only, are not a guarantee of future results, and do not constitute investment advice or a recommendation to buy or sell any security. Actual outcomes may differ materially. © 2026 Piedmont Crescent Capital.

About Piedmont Crescent Capital. Piedmont Crescent Capital provides economic research and advisory services covering U.S. and regional economic conditions, financial markets, housing and commercial real estate. A View from the Piedmont is published weekly. This report is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. Views expressed are those of the author as of the date of publication and are subject to change without notice. © 2026 Piedmont Crescent Capital. All rights reserved.