Moving Beyond the Post Pandemic Economy

- We are moving beyond the post-pandemic economy, which was driven by extraordinary monetary and fiscal stimulus and pent-up demand for housing, consumer goods, travel, and experiences. What comes next is an open question. While a soft landing appears to be the most likely outcome, the margin of error for policymakers is narrow and the upcoming presidential election and geopolitical events might shift risks preferences in a way that upends the economy.

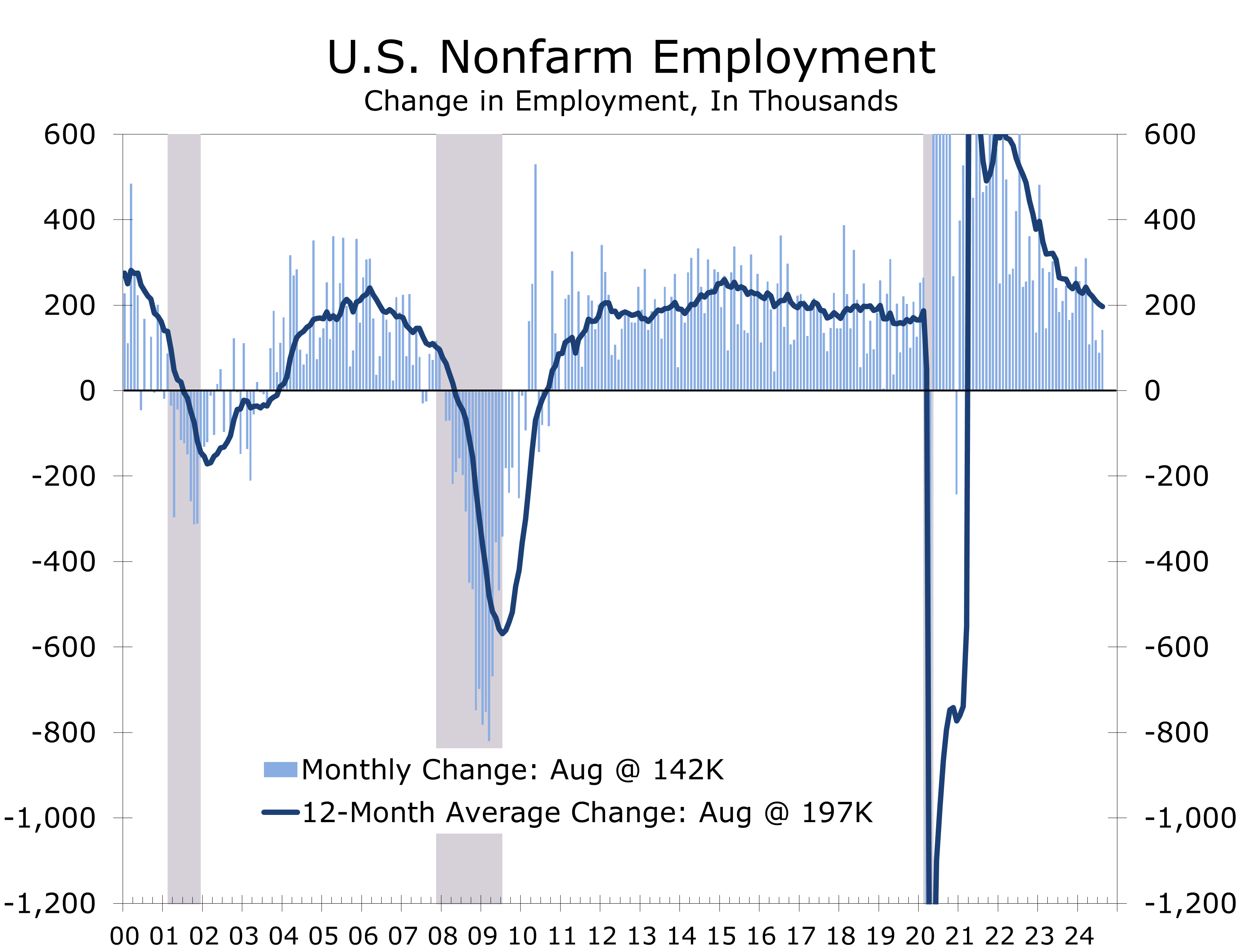

- Nonfarm employment rebounded in August, alleviating fear that the Fed had waited too long to begin to reduce the federal funds rate. Downward revisions to the previous two months’ data, however, suggest the labor market remains fragile, with modest job gains limited to just a handful of sectors. The Atlanta Fed’s GDPNow forecast projects Q3 real GDP growth at 2.1% annually, signaling continuing economic growth. Despite this, bond yields are pricing in more rate cuts than we expect, setting up a possible correction following the FOMC meeting.

- Consumer spending began the third quarter well above its prior quarter average, which provides an easy path for Q3 economic growth. Business fixed investment in equipment also appears to have the wind at its back, as the colossal buildout of factories to produced EVs and related parts, solar panels, and microchips fuels the production of equipment to outfit those factories.

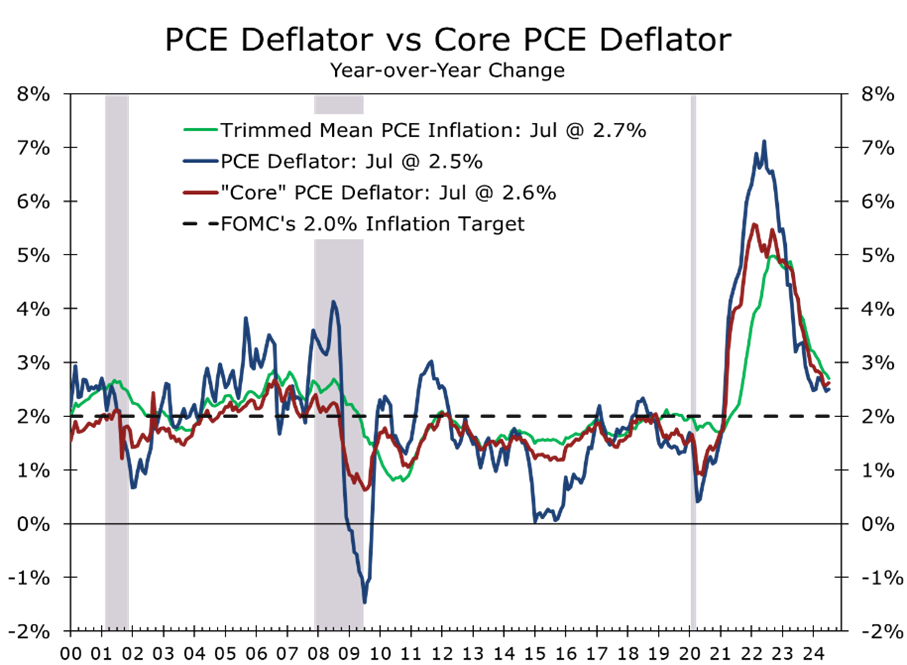

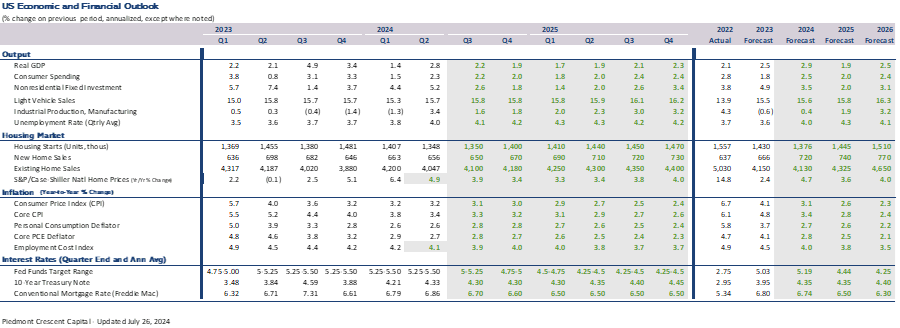

- Inflation appears to be subsiding, easing the squeeze on household budgets. We see the Consumer Price Index receding down to 3.0% by the end of the year and look for the core PCE deflator, the Fed’s preferred price gauge, to the year at 2.7%.

- The geopolitical landscape is fraught with risks. Kamala Harris leads slightly in national polls, benefitting from a huge post-nomination bump. Trump is ahead in several key swing states. The GOP appears poised to regain control of the Senate and likely retain the House. Tensions between Israel and Iran remain tense and a cease fire between Israel and Iranian and Hamas remains elusive. Russia’s war with Ukraine is intensifying as both sides fortify their positions ahead of potential negotiations after the U.S. presidential election.

The post-pandemic economy is transitioning. The surge in demand driven by extraordinary monetary and fiscal stimulus, combined with pent-up demand for housing, consumer goods, travel, and experiences, has largely subsided. The pressing question now is: what comes next? While a soft landing appears the most likely outcome, the margin for error is narrow. Historically, soft landings are rare and difficult to achieve. Over the past fifty years, the U.S. economy has experienced only two successful soft landings—one in the mid-1980s and another in the mid-1990s. In both cases, the Federal Reserve managed to raise interest rates just enough to slow the economy and curb inflation without triggering a recession. The economy narrowly missed soft landings in 1990 and 2000/2001, as exogenous shocks upended slower growing economies.

A crucial factor in ensuring a soft landing is the Federal Reserve’s ability to pivot policy at the right moment, easing pressure on the economy without reigniting inflation. Jerome Powell seems intent on pursuing this approach, as suggested by his speech at the Fed’s annual Jackson Hole symposium in late August. His remarks indicate that inflation concerns are waning and that the Fed is now focusing on a cooling labor market. A quarter-point cut in the federal funds rate seems almost certain at the Fed’s upcoming September 17-18 FOMC meeting. While a larger cut is possible and could be argued for by some committee members, we believe a 50-basis point cut is unnecessary and could unsettle financial markets by creating unrealistic expectations for future meetings.

Recent economic reports and comments from various Federal Reserve officials offer much to digest. The overall consensus appears to be that the economy is moving beyond the post-pandemic period, which was characterized by massive fiscal stimulus, pent-up demand for goods, services, and experiences, and highly accommodative monetary policy. This combination led to the highest inflation the U.S. had seen since the late 1970s and early 1980s, shaping the Fed’s response under Jerome Powell.

Inflation has since moderated, with the core PCE deflator—the Fed’s preferred inflation gauge—falling from a peak of 5.6% in 2022 to 2.6% recently. Other price measures have fallen in similar proportion. Considerable debate remains, however, about the appropriate policy to complete the final stage of the inflation fight. The labor market, a key driver of inflationary pressure, is cooling. Job growth has slowed, and unemployment has risen to 4.2%, which is at the upper end of what the Fed considers full employment, elevating the downside risks to economic growth. Job losses, as measured by weekly jobless claims and layoff announcements, remain moderate by historical standards, however, suggesting that the rise in unemployment is due more to an increase in job seekers and slower hiring. Wage growth has also eased, alleviating concerns about a wage-price spiral.

One key reason the Fed is likely to proceed cautiously is that the economy emerging from the post-pandemic period is fundamentally different from what preceded it, heightening risks. Structural shifts from the pandemic are still reverberating. Supply chains have been reshaped, labor force participation remains below pre-pandemic levels, and the balance of power between labor and capital has shifted. Financial and economic resources also continue to be reallocated, reflecting new risk-reward dynamics. All of this is happening in a business cycle that has seen just two months of recession in the past 15 years, leaving the economy somewhat fatigued.

Expansions do not die from old age; they typically succumb to imbalances or policy mistakes. As Rudi Dornbusch once said, “none of them died a natural death; they were all murdered by the Federal Reserve.” The Fed aims to avoid such errors by carefully weighing risks to both growth and inflation. This process becomes more complicated during times of heightened geopolitical tensions or financial instability, which often increase during presidential election years. Recently, the Fed indicated that the risks of high inflation and a weakening labor market were becoming more balanced. However, at the upcoming September FOMC meeting, we expect the Fed to view the weakening labor market as the more pressing concern.

Nonfarm payrolls increased by 142,000 in August, a rebound from July’s paltry 89,000-job gain, but still part of a trend of weakening employment reports. Revisions to June and July subtracted 86,000 jobs, bringing the three-month average down to 116,000—the slowest pace since the pandemic and well below the 12-month average of 197,000 jobs per month. These figures do not yet account for the latest Quarterly Census of Employment and Wages (QCEW), which suggests job growth from March 2022 to March 2023 was overstated by 818,000 jobs. The corrected data will be reflected in the January 2025 report, released in February.

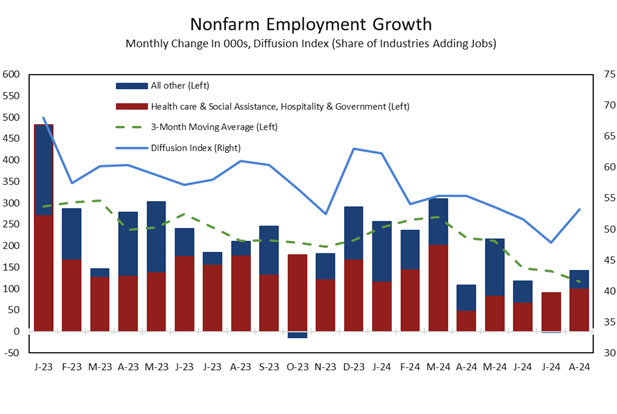

Job growth remains concentrated in just a few industries, led by leisure and hospitality (+46,000), construction (+34,000), health care (+31,000), and government (+24,000). Meanwhile, manufacturers cut 24,000 jobs, primarily in durable goods, and retailers lost 11,100 jobs. The diffusion index rose 5.4 points to 53.2 in August, though the prior month’s reading was revised down to 47.6, indicating more industries cut jobs than added them—a rarity outside recessions. This narrowing breadth of job gains is contributing to a rise in long-term unemployment, as job losers and new entrants into the workforce are taking longer to find jobs.

Long-term unemployment held steady at 1.5 million, accounting for 21.3% of the unemployed, up from a cycle low of 1.05 million in March of last year. The increase is largely due to slower job growth in professional services. Hiring has also slowed in financial services and other occupations requiring a college degree. College graduates have disproportionately contributed to the rise in unemployment this past year, and labor force participation among them has fallen. While professional employment has weakened, job growth in trades, particularly construction and health care, remains strong.

Recent Fed comments suggest confidence in the economy. Fed Governor Christopher Waller, after the August employment report, stated that while he supports rate cuts, their pace and scale would depend on upcoming data. Although Waller favors ‘front-loading’ larger cuts, if necessary, he doesn’t see the need yet, citing strong retail sales and the ISM Non-Manufacturing Survey. He remains focused on employment data, noting that job growth has slowed past the breakeven point required to maintain the current unemployment rate.

Waller and other Fed officials have emphasized that the rise in unemployment—from 3.4% 16 months ago to 4.2% today—is due to slower hiring, not increased layoffs. First-time unemployment claims will be closely monitored to gauge further labor market softening. Waller expressed concern that risks are now more tilted to the downside, potentially affecting the Fed’s maximum employment mandate.

We believe the labor market is weaker than Waller suggests. Two key concerns are the narrowing of job gains, reflected in the diffusion index, and potential large downward revisions to employment data, which could show 818,000 fewer jobs when updated in February 2025. Since March 2023, job growth has been concentrated in sectors like leisure and hospitality, healthcare, social services, and government, while professional services and finance have seen modest hiring. Many workers in these fields, primarily office-based college graduates, are seeing slower employment growth. Moreover, hiring in the hospitality and health care industries is showing signs of slowing. Construction payrolls are also likely to lose some steam, as the backlog of residential, commercial and industrial projects winds down.

While college graduates still fare better than those with less formal education, the labor market has shifted. Since April 2023, the unemployment rate for college graduates has risen by 0.6 percentage points to 2.5%, while it has remained steady at 4% for high school graduates without college experience. College graduates have accounted for nearly half of the increase in unemployment since April, likely due to cost-cutting, slower economic growth, and a return to pre-pandemic staffing levels. The rise of artificial intelligence may also be reducing opportunities for administrative and IT roles. Unemployment among those without a high school diploma has also increased sharply, particularly in regions like California where minimum wages have spiked. By contrast, unemployment for those with a high school diploma and some college has remained stable, thanks to strong growth in construction and specialty trades.

We believe the recent labor force divergence is being overlooked by policymakers, with the narrowing breadth of job gains signaling a broader employment slowdown. This shift highlights underlying weaknesses in what seems like a healthy economy, particularly in professional and financial services, where high-paying jobs are concentrated. Slower white-collar job growth is likely to worsen the office market downturn, especially for older buildings struggling to retain tenants. Weaker growth in these sectors will also reduce the impact of lower mortgage rates, with much of the recent rise in applications coming from refinances. Similarly, lower interest rates may have less impact on motor vehicle sales if white-collar job growth remains weak.

As a result, we now expect the Fed to cut rates more aggressively this fall and winter, forecasting five to six quarter-point cuts at consecutive FOMC meetings starting in September, bringing the federal funds rate to 3.88% by spring 2025. The November meeting is less certain due to its proximity to the presidential election, as the Fed will likely avoid entangling itself in political uncertainty.

The extent and duration of rate cuts will depend on the severity of the current economic dislocation—whether it’s a growth scare, a soft landing, or a full-blown recession. A growth scare is a brief slowdown without contraction, usually driven by external factors, requiring minimal Fed action. A soft landing involves prolonged, below-average GDP growth with rising unemployment and easing inflation, prompting a more significant Fed response. A full-blown recession, or hard landing, features a sustained decline in GDP, rising unemployment, and reduced spending, necessitating major policy intervention. Currently, the economy appears to be somewhere between a growth scare and a soft landing.

The economy has faced several growth scares in recent decades, including the 2023 Silicon Valley Bank crisis, the 2022 inflation shock, concerns over China’s slowing economy in 2015, and the 2011 European debt crisis. Despite heightened uncertainty, the Fed largely maintained its policy stance, they refrained from hiking rates in 2015. The most recent soft landings occurred in the mid-1990s and mid-1980s, when Fed rate hikes slowed GDP growth below its long-term average. Once inflationary pressures eased, the Fed responded by cutting rates.

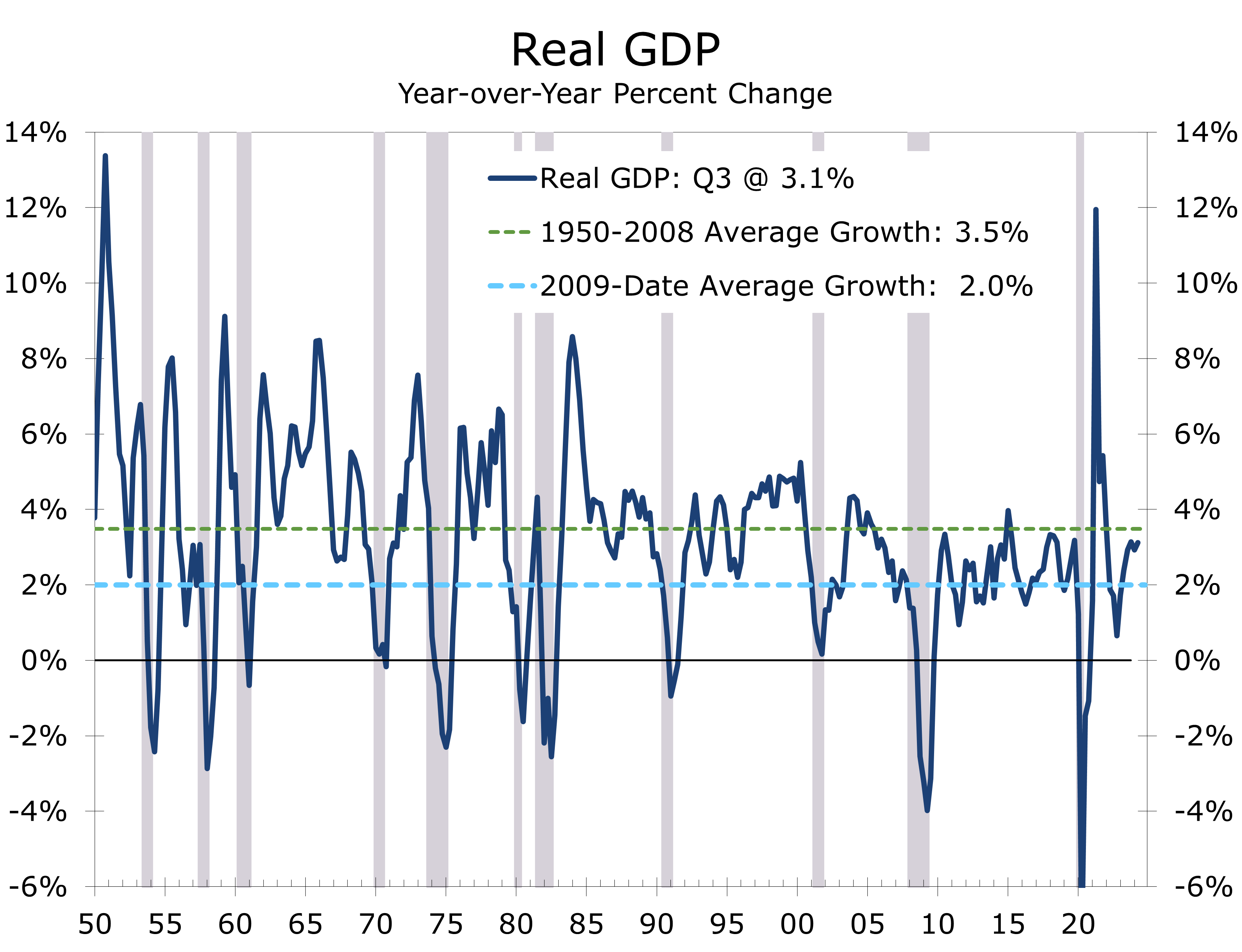

One of the reasons we feel the economy is entering a phase somewhere between a growth scare and a soft landing is that economic growth has been so solid. Real GDP has risen 3.1% over the past year, and private final domestic demand has grown at a 2.5% annual rate. Retail sales started the fourth quarter strongly, and high-frequency data like TSA traffic, restaurant dining, and credit card use remain robust. However, financial markets are jittery, with stocks falling sharply in early September before rebounding after reflecting on August’s employment report and other data. Additionally, concerns about China’s struggling economy are impacting commodity prices.

The most evident sign of a soft landing is the 0.8 percentage point increase in the unemployment rate to 4.2% since March 2023, mainly due to slower hiring rather than increased layoffs. The weaker QCEW data through March, which suggests a downward revision of 818,000 jobs to current nonfarm payrolls, supports the ‘soft landing’ view, as does the slowdown and narrowing breadth of job growth. Despite strong real GDP growth, we expect upcoming revisions to reveal slower growth than currently reported and anticipate that the gap between Gross Domestic Income (up 2.0% over the past year) and real GDP (up 3.1%) will narrow.

Growth scares often lead to increased financial market volatility as investors struggle to interpret mixed economic signals. The close presidential election and ongoing uncertainties about the economies in China, Japan, and Europe add to this volatility. We expect the yield curve to modestly steepen as it becomes clearer that economic growth is merely moderating. Lower interest rates should set the stage for a cyclical rebound in housing, consumer durables, and business investment.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice. Any forward-looking statements or forecasts are not guaranteed and are subject to change at any time. Information from external sources have not been verified but are generally considered reliable.

© 2024 CAVU Securities, LLC

September 12, 2024

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000